George Selgin has a couple of new posts on the 1937-38 depression, which are part of his excellent series on the New Deal. I cannot find anything significant with which to disagree. He directed me to a new paper by Christopher Hanes, which studies the impact of New Deal policies on the labor market. Here’s the abstract:

Wage inflation surged in the 1930s though unemployment remained high and output below trend—an anomaly in terms of the usual “Phillips curve” relationship. Proposed explanations include New Deal labor policies, hysteresis in unemployment, downward nominal wage rigidity, and a new Keynesian expectational mechanism through which Roosevelt’s monetary policies would have boosted real activity and created anomalous inflation by raising the expected future price level. I find that labor policies fully explain 1930s wage inflation anomalies. Thus the 1930s United States should not be cited as evidence for the new Keynesian expectations mechanism, hysteresis in unemployment, or downward nominal wage rigidity.

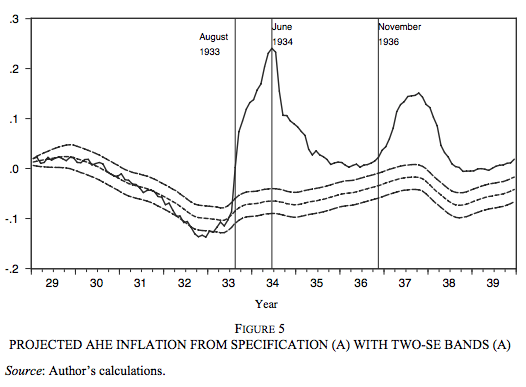

This confirms what I suggested in The Midas Paradox, but Hanes justifies the claim with econometric analysis. This graph from the paper shows the NRA wage shock of late 1933, and then another wage shock associated with the post-Wagner Act unionization drives of 1936-37, relative to the path of wages predicted in the absence of labor policy changes:

Here’s a “cinematic” presentation of the policy implications:

Did Sinema really have vote against a $15 minimum wage for 24 million people like this? pic.twitter.com/Jv0UXLKLHI

A new WSJ article suggests that they are beginning to zero in on the origin of the Covid-19 virus:

At least four recent studies have identified coronaviruses closely related to the pandemic strain in bats and pangolins in Southeast Asia and Japan, a sign that these pathogens are more widespread than previously known and that there was ample opportunity for the virus to evolve.

Another new study suggests that a change in a single amino acid in a key component of the virus enabled or at least helped the virus become infectious in humans. Amino acids are organic compounds that form proteins.

Public-health officials say it is critical to identify the origin of the pandemic to take steps to avert future outbreaks, though it may take years to do so. These latest pieces of research add to evidence that the virus, called SARS-CoV-2, likely originated in bats and then evolved naturally to infect humans, possibly through an intermediary animal.

The studies also help explain why members of a WHO team that in February completed a four-week mission to Wuhan—the Chinese city where the first known cases of Covid-19 were found—advocate searching for the origin of the pandemic in other countries in addition to China, particularly those along its border in Southeast Asia. . . .

Using the test, he and a team of researchers found strong neutralizing antibodies that blocked SARS-CoV-2 in bats and a pangolin in Thailand. That likely means the animals were exposed to a coronavirus similar to the pandemic version, said Dr. Wang. The team also found a coronavirus closely resembling the pandemic strain in bats in a cave in eastern Thailand.

Certain nationalistic politicians tried to smear China by labelling Covid the “China virus” or the “Kung flu”, before all the evidence was in. If this new information is correct, should we now call it the Siam flu?

It seems increasingly unlikely that the virus came from a Chinese lab, although that hypothesis has certainly not been definitively ruled out. (The WHO team did not have access to all of the information it needed):

Chinese scientists reported soon after the pandemic began that the Wuhan Institute of Virology had a virus whose genome is a 96.2% match with that of the Covid-19 virus. But the difference between the two viruses would have been too great for researchers to successfully engineer the pandemic virus, said Dr. Wang, who is an expert in bat-borne viruses.

“It would explode your calculator,” he said of the difference. “If the best scientists all worked for me for the rest of my life, I would not be able to create it.”

Nor would it have been straightforward to figure out the mutation in the virus that Dr. Weger-Lucarelli and his colleagues found. “There is no literature, at least that no one has published, showing that this site in coronaviruses is very important for human infection,” Dr. Weger-Lucarelli said.

The newly found coronaviruses support the argument that “nature developed this virus without requiring any human intervention,” said Stanley Perlman, a University of Iowa virologist who has studied coronaviruses for four decades but wasn’t involved in the latest studies. He serves on the Lancet Covid-19 Commission set up to speed solutions to the pandemic.

Robert Garry, a virologist at the Tulane University School of Medicine who was involved in that research, said he and other colleagues had initially considered the possibility of a leak or accident from a laboratory, but ultimately deemed it “nearly impossible.”

PS. A while back I linked to an excellent set of Phillip Lemoine posts on China’s role in the pandemic. Now he has produced a powerful critique of “lockdowns”. (I put the term ‘lockdown’ in quotes because it’s a rather vague concept, which covers both actual lockdowns and some milder interventions.) I’ve always felt that lockdowns should only be used under very extreme circumstances. In my view, our big policy mistakes were in the areas of masks, testing and especially vaccines. I’m happy for the British, but why couldn’t we have done the same?

Years ago, I used to read a book to my (half-Chinese) daughter entitled, “And to Think That I Saw It on Mulberry Street”. It was Geisel’s first children’s book. As you probably know, that book has now been cancelled. Others have already pointed to the utter insanity of this book still being under copyright. (It was first published in 1937.) Extending copyright protection beyond 20 years makes America both less efficient and less equal—a lose/lose proposition.

The story itself is a celebration of diversity. The world is so much more interesting when there are all kinds of people to look at. Here’s the offending picture:

The picture is a bit offensive by today’s standards, but most of the problems were solved years ago. Here’s what the picture looked like in the edition I own, from 1991:

America used to be able to do things. We sent men to the moon, built subways and airports and interstate highways. We built houses for working class people in coastal cities. Now we’ve forgotten how to do those things, although it’s rumored that there are manuscripts explaining how that are preserved in lonely monastaries hugging the windswept coast of Maine.

In the old days, we knew how to fix a book that had become dated. Perhaps “sticks” should be “chopsticks”. But it doesn’t matter, as today we’d rather just cancel the book and engage in self-righteous moral grandstanding.

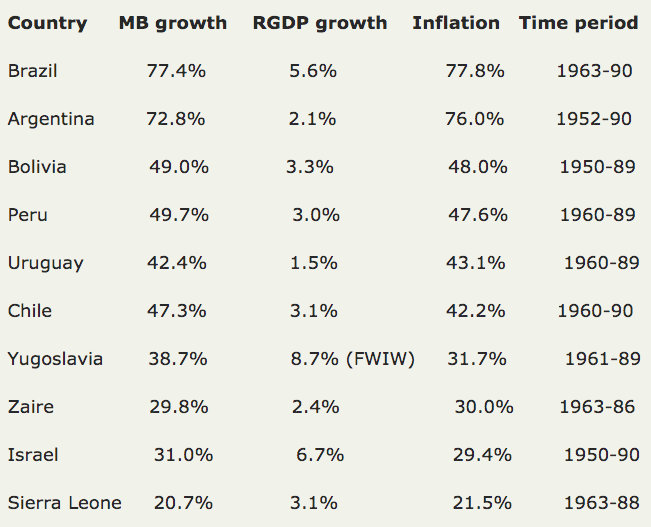

If attempting to control the supply of food kills one hundred million people, then why do economists think controlling the supply of money will yield a better result?

I presume Lin is referring to the Fed controlling the supply of Fed money. This is how markets work. Ford controls the supply of Ford cars, Apple controls the supply of iPhones, and the Fed controls the supply of Fed money.

It’s a free country and alternatives such as travelers checks, Bitcoin, one ounce bars of silver, and other types of money are freely available if you don’t like using Federal Reserve Notes.

3. Until I read this four part series, I knew nothing about the guy who was recently fired by the NYT for supposedly being a “racist”. Now I know that his views are pretty much like mine. I’ve also learned that someone with my sense of humor and/or my political views is not welcome at the NYT. And that’s fine with me. Most of all, I’ve learned that a sizable fraction of the people who work at the NYT are totally insane. Especially the younger employees. And I’ve learned that some teenage girls have no sense of humor. The Great American Bourgeois Cultural Revolution rolls on.

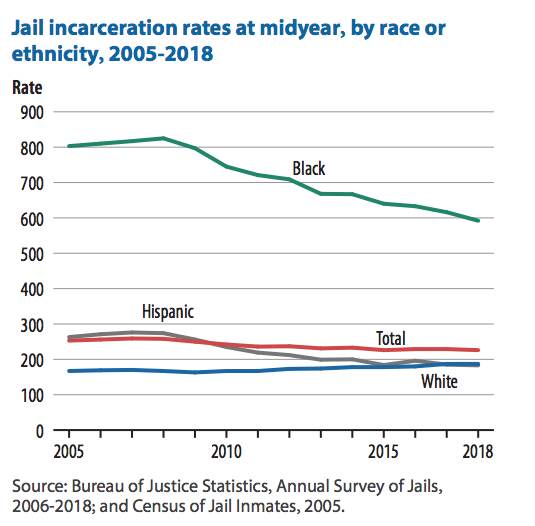

4. I also recently learned that Hispanics living in America are imprisoned at a lower rate than whites, but only since Trump took office in 2017. Before then, Hispanics were imprisoned at a higher rate than whites.

If you like Trump you’ll say this proves that he’s not bigoted against Hispanics. If you despise Trump (like me), you’ll say it shows he was wrong to characterize Hispanic immigrants as rapists and murderers.

And if you work for the NYT, you’ll insist it should be spelled “Hispanix”.

Arnold Kling has a new article on monetary and fiscal policy. Because he slightly mischaracterizes my views, I should probably respond:

Scott’s argument for monetary dominance is that the Fed, which sets monetary policy, is way more agile than Congress, which sets fiscal policy. It’s like a game of rock, paper, scissors in which if Congress shows rock, the Fed shows paper. Or if Congress shows scissors, the Fed shows rock. The Fed can always win.

I do think the Fed is more agile, but the decisive factor is that the Fed is much stronger. If you want a metaphor that is better than rock, paper, scissors, imagine I’m driving my car and my 6-year old daughter pushes the steering wheel to try to change direction. I’d simply push back more strongly.

I believe in fiscal dominance. That is because I do not think that Peter cares all that much whether he hangs on to his T-bill or exchanges it for money. Scott thinks that Peter will spend more in the latter case. I am skeptical.

This isn’t the right thought experiment. I don’t doubt that if you give the average person a briefcase with a million in cash they’ll go on a shopping spree, and that’s equally true if you give then a million dollars in T-bills. That’s not the issue. Money is special not because it is regarded by individuals as wealth, rather because it is the medium of account exchange.

If you add more cash to the economy than people want to hold, they can get rid of the excess cash balances only by pushing up the price level. In contrast, if you add more T-bills than people want to hold, they can drive down the price of T-bills, with no change in the price level. You merely need to assume that they aren’t perfect substitutes. (At least when nominal interest rates are positive, and Arnold seems to be arguing for fiscal dominance even during periods where interest rates are positive.)

Scott, like almost all mainstream economists, sees inflation as having a continuous dose-response pattern. Give the economy a higher dose of money and it will respond with higher inflation. Other economists measure the “dose” as the employment rate.

I think of inflation as an autocatalytic process. Inflation is naturally low and stable. But it can be jarred loose from that regime and become high and variable. Then it takes a lot of force to bring it back to the low and stable regime.

Nominal variables don’t have natural rates. It’s a policy choice. Inflation was not low and stable for most of American history, but became low and stable after 1990, when the Fed decided to target inflation at roughly 2%. These things don’t happen automatically. That’s why most central banks have set inflation targets, to prevent this:

Here’s Arnold:

Once inflation gets going, the only way to stop it is to slam on the economic brakes. Usually, this means drastically cutting government spending. But in the U.S. in the early 1980s, we slowed the economy without cutting government spending. Instead, the foreign exchange market put on the brakes by raising the value of the dollar, stimulating imports and making our exports non-competitive. And the bond market put on the brakes by raising interest rates, so that nobody could afford the monthly payment on an amortizing mortgage. After a few years of high unemployment, inflation receded.

Most economists attribute these developments to Fed policy under the sainted Paul Volcker. Scott could say that this was exhibit A for monetary dominance. The economic consensus may be right, but I would raise the possibility that the financial markets were the main drivers.

The price of goods (CPI) the price of foreign currency (E) are two ways of measuring the value of money (actually its inverse.) Here Arnold is saying that monetary policy did not make the dollar strong, a stronger dollar (exchange rate) made the dollar stronger (purchasing power). OK, but the two most plausible theories for the strong dollar were tight money and fiscal deficits. Obviously, Arnold is not saying that big fiscal deficits brought inflation down in the 1980s.

Exhibit A? Volcker was perhaps Exhibit J for monetary dominance; there are so many other examples that one hardly knows where to begin. Remember LBJ raising taxes and pushing the budget into surplus in 1968 in order to bring down inflation? How’d that work out? Budget deficits were pretty low in the 1970s, as a share of GDP. What happened to inflation? Then inflation fell as Reagan pushed the deficit much higher. A big reduction in the budget deficit from $1061 billion in calendar 2012 to $561 in calendar 2013 should have slowed the economy according to the fiscal dominance theory. Instead NGDP growth sped up in 2013. Then the deficit ballooned to a trillion dollars in 2019, and yet inflation stayed below 2%.

Overseas you find the same thing. Japan runs some of the biggest fiscal deficits ever seen in peacetime from the mid-1990s to 2013 and both the price level and NGDP actually fell. Then a new government switched to fiscal austerity and monetary stimulus, and NGDP begins rising (albeit still too slowly.)

Sorry, but fiscal dominance is not remotely plausible, at least with positive interest rates and an independent central bank.

Almost every major school of thought—monetarist, Keynesian, and Austrian, etc.—believe that monetary policy has a major impact on nominal variables. The financial markets respond to monetary policy announcements as if they are extremely important, often adding or destroying hundreds of billions of dollars in wealth within seconds. The history of economics is full of examples of monetary dominance over fiscal policy. Basic theory predicts that a $100 bill is not identical to a T-bill yielding 2% interest; otherwise they’d have the same yield. If Arnold Kling and the MMTers want to convince the me, the rest of the profession, and the financial markets that open market operations don’t matter when interest rates are positive, they are going to need something better than dubious thought experiments about the substitutability of cash and T-bills.

Welcome to a new blog on the endlessly perplexing problem of monetary policy. You’ll quickly notice that I am not a natural blogger, yet I feel compelled by recent events to give it a shot. Read more...

My name is Scott Sumner and I have taught economics at Bentley University for the past 27 years. I earned a BA in economics at Wisconsin and a PhD at Chicago. My research has been in the field of monetary economics, particularly the role of the gold standard in the Great Depression. I had just begun research on the relationship between cultural values and neoliberal reforms, when I got pulled back into monetary economics by the current crisis.

"This man is the devil. Look at his eyes. Same as Soros. All baggy and nasty. Good people dont age like that. Its the sign of a madman. A negativity..."

"I watched Satantango on video over 3 days. I found it absolutely gripping, but one must surrender for a time one's idea of what a movie should be. Instead, you..."