Stocks moved sharply lower on the disappointing forward guidance, which suggested “one and done”, and then recovered a bit when Powell clarified his remarks. It’s sort of surreal when reporters ask Powell to comment on the fact that hundreds of billions in wealth is being destroyed as he speaks, indeed because he speaks.

I was disappointed in the general thrust of questions from reporters. The markets clearly believe the move was too little, but most of the questioners seemed skeptical of the need for any move at all.

One reporter suggested that this move gave the Fed less room to cut rates in a future recession, which is nonsense. To his credit, Powell rejected the “premise” of her question, pointing out that the purpose of the move is to strengthen the economy, and thus give them more room to cuts rates in a future recession.

I would cut Powell a bit of slack, as I believe his remarks were probably somewhat constrained by splits on the FOMC committee. Overall it was a miss, but not a major one.

The Fed cut rates by only 0.25%, which looks like a mistake. Here’s why:

1. This will make it even more difficult to hit the 2% inflation target.

2. Because the tightening was associated with a cut in the target interest rate, many pundits will wrongly conclude that policy eased. When this move does nothing to boost inflation, these same pundits will wrongly conclude that monetary policy is ineffective.

Why they think a policy that pushed up the dollar in forex markets is “expansionary” is beyond my comprehension, but that’s the world we live in. Thus monetary policy discourse is set to become even dumber. A fifty basis point cut would have made the discourse slightly less dumb. The general rule is that when the Fed moves rates in the same direction as the equilibrium rate, but more slowly, the discourse gets dumber.

3. Congress is currently running the most expansionary fiscal policy in history (given peace and prosperity), and this move will lead to calls for an even more expansionary fiscal policy. More fiscal stimulus will not help, rather it will be offset by monetary policy.

4. Long-term bond yields fell, but not because policy was easier than anticipated. Just the opposite. Yields fell because policy was more contractionary than expected. I.e., the income and Fisher effects are driving long-term yields lower.

I may add something later, after the press conference.

The bond market has already delivered the Fed cut everyone’s been waiting for

Interpretations:

1. The public is “waiting for” easy money, but it won’t happen because the declining bond yields reflect a tightening of monetary policy. NRFPC

2. The declining bond yields reflect anticipation of the liquidity effect from monetary easing. As Nick Rowe likes to say, policy is 1% concrete actions and 99% expectations. So it does represent monetary easing.

3. The Fed doesn’t even need to cut rates, as the bond market’s already accomplished the goal. That’s probably false, as a lack of follow through by the Fed will either lead to a spike in interest rates or a further decline in rates due the the income and Fisher effects.

4. The declining interest rates have nothing to do with monetary policy and do not help the overall US economy, but they do help the housing sector. This interpretation best fits 2001-4. During that period, interest rates fell due to weakness in business investment (not easy money), boosting the housing sector.

5. Rates are falling due to global economic weakness, not economic weakness in the US. This will lead to more investment in the US (both business and residential.) The resources used to produce this investment will come out of the production of consumption goods in the US. The funds to finance the investment will come from foreign saving. As American consumers increasingly rely on foreign consumer goods, the trade deficit will increase.

Over at Econlog, I discuss some recent comments attributed to Peter Thiel, who seems to be edging from libertarianism toward national conservatism.

Recently, I’m seeing quite a bit of that sort of transition, in all sorts of places. Here’s an example of an essay from Law and Liberty:

Conservatives need Thiel because he has a positive vision for the federal government in industrial policy and basic scientific research, to say nothing of the ways he might revive the Cold War-era conservative seriousness regarding national security. . . .

But Thiel is weak on what to do about defending a stable way of life, which for many Americans is the main purpose of politics. . . . Indeed, his very attack on the liberal institutions that aim to form character, the media and academia, should lead him to realize America needs more social conservatism of the right kind: that which prepares Americans to live worthwhile lives in freedom. . . .

Whether he knows it or not, Thiel’s political vision necessarily depends on American politics, and therefore on the Founding. We really do believe, most of us, in natural rights that come before government and therefore treasure certain freedoms. Consequently, we prefer not to be administered by vast institutions, political or otherwise. Even when we feel stuck being the way we are, we do not contemplate living like other nations, for we do not want to be circumscribed by the state.

Here’s another essay by a different author, from the same Law and Liberty site:

It’s not at all clear to me how an industrial policy promotes “liberty”.

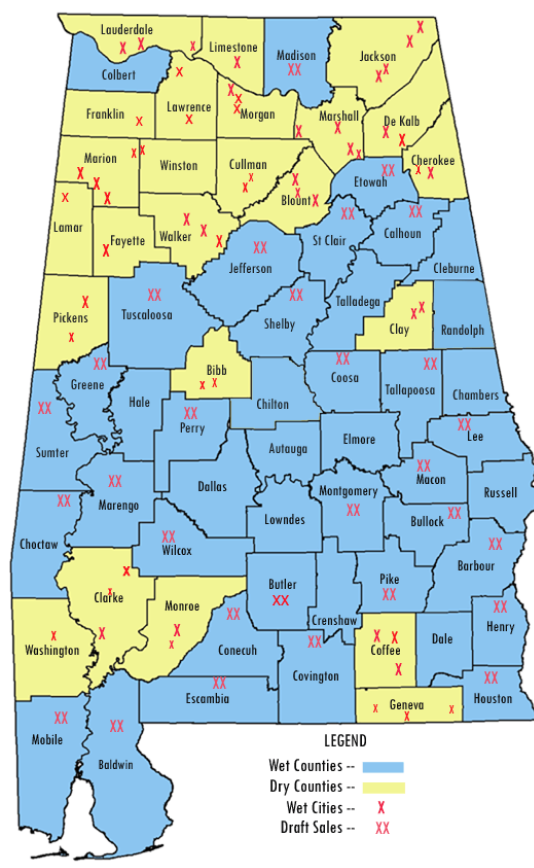

Some people ask me why I moved to the West Coast, with its highly intrusive government policies. It is true that my state (California) is over-regulated and overtaxed. But things are not that simple. Consider Alabama, largely governed by conservative Republicans that like to talk about “liberty” and “freedom”.

In Alabama, pot is illegal. So is physician-assisted suicide for the terminally ill. So is prostitution. In much of northern Alabama, you can’t even buy alcohol:

And Alabama recently banned abortion.

Most of these things are legal on the West Coast (except prostitution, which is only legal in parts of Nevada.) I am 15 minutes from a California Tesla dealership, but in Alabama it’s illegal to sell Teslas.

Admittedly, the West Coast is much less friendly to most businesses than Alabama. But despite those intrusive regulations, many of America’s most productive people in industries like computers, software, biotech, entertainment and aerospace choose to live on the West Coast. Maybe our most creative people prefer not to live in a Christian theocracy. Maybe they’d prefer to avoid a state where a recent GOP nominee for the US Senate advocated criminalizing homosexuality and is opposed to Muslims serving in Congress, and still won most of the white vote. Maybe Alabama’s “liberty” is an empty cliché. Alabama’s economy certainly doesn’t seem to be attracting many people:

With reapportionment looming after the 2020 Census, Alabama is on the cusp of losing one of its seven seats in the U.S. House of Representatives, a development that could reduce the state’s voice in the lower chamber. It would be the first loss of a seat for the state since 1970.

Wouldn’t that be sad.

The Trump administration is up in arms over France’s decision to impose a tax on internet services. But that’s not because the Trump people like high tech. After all, most of the profits from high tech flow to blue states like California, Massachusetts and Washington. Rather, Trump wants the US government (which means Trump) to grab more of those profits. Look for an antitrust crusade against high tech, with some heavy fines. Then the money can be distributed to people in red states hurt by Trump policies, such as farmers.

Conservatives correctly point out that progressivism has a potentially unlimited list of “unmet needs”, which is an open door to never ending growth in government. Traditionally, the opposition to this sort of big government has come from the libertarian wing of the GOP. But if the GOP is taken over by “national conservatives” who favor industrial policy, then we will be in an entirely new world. Two big government ideologies will be fighting over the “golden goose”.

Just as there is no limit to “unmet needs”, there is no limit to “enemies”. Nationalists will find an unending number of groups to fight against, including foreigners, Hollywood, universities, drug companies and high tech firms. Big government will be used as a tool to favor the economic interests of their tribe—say Alabama auto dealers who don’t want to compete against Tesla—and will also be used to enforce their vision of “social conservatism”.

I’d rather not have to choose between these two competing statist visions. But if forced to choose, I’ll opt for the tribe that doesn’t tell foreign-looking people like my wife to go back to where they came from. The one that prefers to redistribute income to the poor and public employees, not to politically favored businesses.

PS. I hope it goes without saying that the title of the post is not an attempt to accuse conservatives of supporting slavery, it’s an accusation of hypocrisy.

PPS. Slightly off topic: North America has nearly 500 million people, and more than half live in places where pot is legal. Please don’t talk about legal pot in Colorado; it’s no longer special. Pot is legal in Peoria, Illinois, in Grand Rapids, Michigan and in Bakersfield, California. BTW, kudos to Trump for his 5 recent pardons. Let’s have some more pardons for people with pot violations that have already served absurdly long sentences.

Yesterday, I did a post discussing a recent WSJ article on inflation that was partly motivated by research by James Stock and Mark Watson. They found evidence that the recent apparent flattening of the Phillips curve may reflect price stickiness in some important sectors of the economy.

The WSJ article suggested that these findings might help to explain why the Fed was having trouble hitting its inflation target. In the previous post I expressed doubt that a flatter short run Phillips curve explains why the Fed has fallen short of the 2% inflation target, although perhaps there is some model where that is an issue.

Tyler Cowen has a new post that quotes from the WSJ article. Tyler’s post is entitled:

Recent studies have shown prices in some sectors—such as housing—do indeed rise faster when growth is in full swing, unemployment low and markets frothy. But a large chunk of the economy, from health care to durable goods, appears insensitive to rising or falling demand.

A paper published last month by economists James Stock of Harvard University and Mark Watson of Princeton University found prices accounting for nearly half of the Fed’s preferred inflation gauge, the personal-consumption-expenditures price index, don’t respond to changes in economic activity. In 2017 economists at the Federal Reserve Bank of San Francisco found such “acyclical” goods and services made up a whopping 58% of that index.

Do you see the problem? The study does not make any claims about demand being difficult to stimulate, rather the study finds evidence that demand stimulus has less short run impact on prices than one might have expected.

This is an important distinction. Are we confused because the Fed seems unable to stimulate demand, or because when the Fed does stimulate demand there seems to be little impact on prices? Those are radically different issues.

In fact, the Fed could easily boost demand with an easier monetary policy, and if they did so then inflation would increase. Because prices are sticky, the initial effect of extra demand would mostly show up in higher output, but the long run effect would be higher prices.

The Stock and Watson paper focuses on the relationship between “slack” and inflation. In my view, it’s better to focus on the relationship between NGDP growth and inflation. From that perspective, there is no mystery that needs to be explained. Inflation has been low because NGDP growth (i.e. demand) has been low. Thus from an NGDP perspective, there is little evidence that prices are insensitive to demand. We haven’t had much growth in demand.

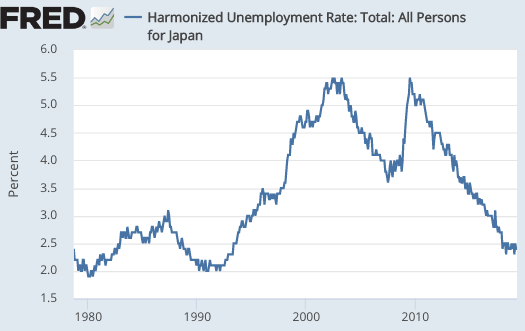

If prices appear to be insensitive to “slack”, then that’s probably because our current estimates of slack don’t track demand very closely. The currently low unemployment rate in the US does not reflect a high level of aggregate demand. Instead, it reflects a labor market that is increasingly able to reach equilibrium at low rates of NGDP growth, a situation where (as in so many other areas) Japan has been a path breaker.

PS. The OECD claims that Japan has had three recessions since 2010. I say they’ve had zero. That’s why Abe has been so popular.

Welcome to a new blog on the endlessly perplexing problem of monetary policy. You’ll quickly notice that I am not a natural blogger, yet I feel compelled by recent events to give it a shot. Read more...

My name is Scott Sumner and I have taught economics at Bentley University for the past 27 years. I earned a BA in economics at Wisconsin and a PhD at Chicago. My research has been in the field of monetary economics, particularly the role of the gold standard in the Great Depression. I had just begun research on the relationship between cultural values and neoliberal reforms, when I got pulled back into monetary economics by the current crisis.

"Couldn't find the substack and if it's moderated just as well... Voted for Trump and he won. Sorry liberal Scott Sumner who believes in money non-neutrality, which is akin to..."

"Scott, Quick note of thanks. I've hugely enjoyed your blog and the intellectual stimulation I gotten from it. Also it was pleasure getting to know you and your wife. Hope..."