Haruhiko Kuroda will go down in history as one of Japan’s greatest central bankers. His policies were not perfect, but given the political constraints he operated under he achieved a great deal.

He will be replaced by Kazuo Ueda, a 71-year old academic with an MIT background (one of Stanley Fischer’s students). Some describe him as mildly hawkish, but this Bloomberg piece suggests a more complex picture:

The first impression by the market has been that a surprise choice indicates a hawkish turn by [Prime Minister] Kishida. . . .

That may yet prove wide of the mark. . . .

As a BOJ board member, he dissented from that controversial decision in 2000 to raise the benchmark rate. That step by the bank was opposed by the government, and quickly turned into a fiasco. The global economy was already slowing down and the BOJ was forced to reverse course the following year. The incident deeply scarred the bank, and made policymakers in Japan extremely wary of backing away from easy money. It subsequently tried again in the lead-up to the global financial crisis, only to cut when the world economy tanked.

The decision by the BOJ to tighten policy in 2000 was a terrible mistake. I am pleased to learn that Ueda opposed the decision—it’s a strong indication that he has good judgment.

I recently flew down to Punta Arenas, Chile. A few comments about latitude (and these are guesstimates on my part; correct me if I’m wrong.)

People talk about a North/South split in development, but it’s really more North/Central. Africa runs from about 37 degrees north to 34 degrees south. That’s central. The actual south is mostly empty.

It’s interesting to contrast the north and south of the planet. Take the region from 38.5 degrees up to the arctic circle. That’s from Lisbon up to the northern tip of Iceland. Over in the US, 38.5 is about a line from Sacramento across to DC, and the arctic circle is way up in northern Alaska. So this northern region includes most of North America and most of Eurasia.

The world is 71% water and 29% land, but I’d guess the region from 38.5 degrees up to the arctic circle is more than 50% land. In contrast, the middle section of the world is much more water intensive, and the southern section (from 38.5% south to the antarctic circle) is almost entirely ocean. Down there you have most of New Zealand, Tasmania, a tiny piece of Antarctica, the Falkland Islands and Patagonia. But all that together comprises perhaps 3% (or less?) of the surface area of this southern region. And the vast majority of land in this region lies in Patagonia, which begins roughly at the 38.5 degree south latitude (the Rio Negro.)

The south is like Ursula Le Guin’s Earthsea. It’s a water planet with hardly any people. The Earth is very “top heavy” in terms of land, people, power, almost everything. That’s why world maps often put the equator about 2/3rds of the way down.

I like to read. Most normal students stop reading for fun when they enter grad school and begin to seriously focus on economics. I did the opposite in my first year at Chicago (1977). I suddenly began reading lots of novels and travel books. Here are a couple of examples; both came out at about the same time:

Right before this trip, I reread the Chatwin book. It’s every bit as good as I recall—a travel masterpiece. But is it true? When it’s this good, who cares?

Us northerners tend to associate the term “south” with “hot”. But the southern part of this planet is really cold. In Punta Arenas, the average high during mid-summer is only 60 degrees (15 or 16C), whereas an equal distance north of the equator (say Hamburg, Germany) is 73 during the summer (23C). The great Southern Ocean is like a big bowl of water with a giant ice cube floating in the center. And nothing to break the relentless wind. The south is too cold for me. Soon we’ll head up north to warmer regions.

The native people of Fireland (which the local people call “Tierra del Fuego”) lived mostly outdoors, with almost no clothing. The cold, wet and windy climate in this area is similar to that of Reykjavik. In contrast:

1. I live in Southern California.

2. I live indoors.

3. I have warm clothing.

4. I have a furnace.

And for four months, I’m still &$#@&% cold all the time!

A while back I recall reading that residents of San Diego complain more about the cold than people of any other city. At one time, that made no sense to me. Now that I’ve moved to Southern California, I finally understand.

This is just one more illustration of why economic growth doesn’t make people happier. Hedonics. Set points. And don’t tell me that you’d hate living without clothing in Patagonia. Of course you would—you’re soft! But the natives didn’t hate their lives. Painkillers? It’s all relative. Here’s Montaigne:

Most of Mankind spend their lives without experiencing poverty; some without even experiencing pain or sickness

He wrote that in the 1500s. What do you think Montaigne regarded as “poverty”? What definition of poverty would cause one of the world’s wisest men to make that claim during the 1500s? What definition of “pain or sickness”. A toothache? A cold?

You say that teenage girls are depressed by social media? I bet the teenage girls of Fireland were not depressed.

PS. I am currently reading a memoir entitled “Uttermost Part of the Earth”, written by Lucas Bridges, one of the first European settlers of Fireland. An amazing book. Imagine something like Kipling’s “The Man Who Would Be King”, except a true story. (Not the same plot, but an equally thrilling adventure.) Fascinating stuff on the native Patagonians, who have mostly disappeared.

PPS. After Punta Arenas we visited Puerto Natales. The weather was even worse than normal; cold, windy and rainy. Wind tends to come from the west, and there’s no land going west from the Falklands–all the way around the world until you reach the west coast of Chilean Patagonia.

When I was young I liked looking at maps and dreamed of visiting the southern tip of South America. So here I am. But I waited too long. Hiking near Grey glacier yesterday I was all bundled up and still felt cold—in mid-summer! Don’t wait to travel—do it when you are young. Patagonia is “no country for old men”.

BTW, it gets dark at 9:30 and light again at 6:30, which means their time is shifted two hours forward. One hour is because Chile is currently on daylight saving time, and the other because Puerto Natales is in a time zone one hour ahead of New York and Boston, despite lying directly south of those eastern US cities. It’s like Chile normally has DST, and then double-DST in the summer.

If you plan to travel to this area, I’d suggest staying up at Torres del Paine, not Puerto Natales. Otherwise, you’ll have very long and bumpy bus rides between your hotel and the best scenery. If you are old, I’d consider NZ’s south island before Patagonia—it’s much easier.

We visited the cave that motivated Chatwin’s trip, where his grandmother’s cousin had found the remains of a mylodon skin (one of those many large mammals wiped out by the early human inhabitants of the Americas.)

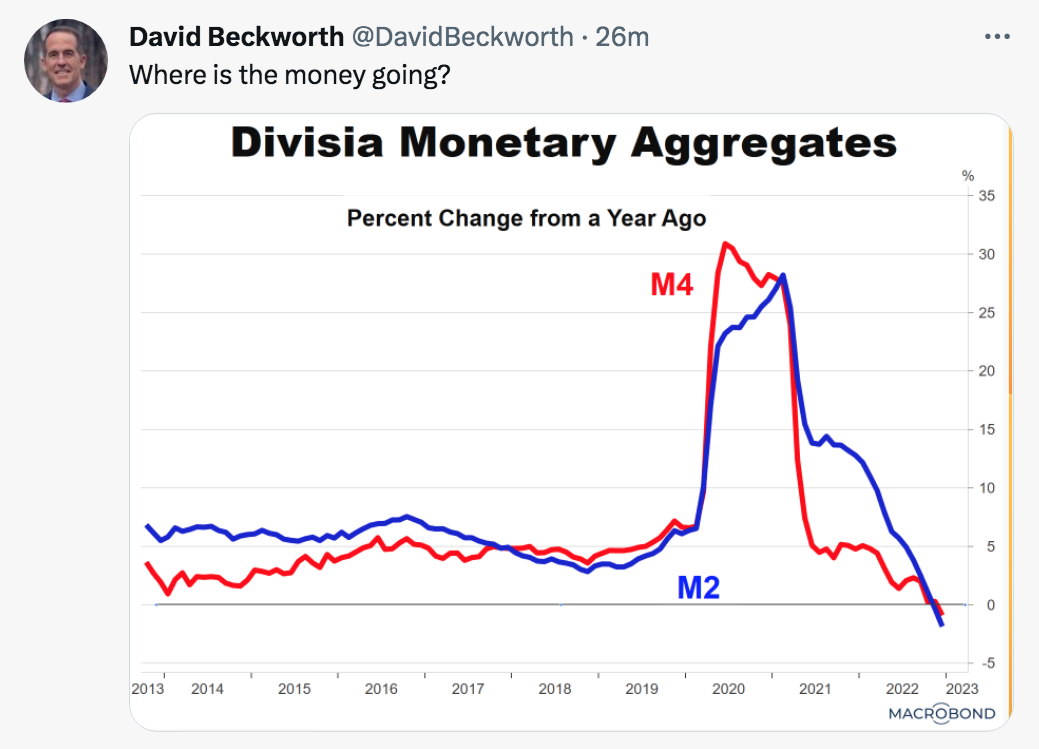

If inflation had stayed stable at 2%, this question would have a simple answer. In that case, changes in the money supply growth rate would reflect changes in real money demand. In other words, the Fed would have been accommodating shifts in money demand with equal changes in the money supply growth rate.

It would also be easy to provide a simple explanation if inflation were perfectly correlated with the money supply growth. In that case, changes in money growth would reflect exogenous changes in monetary policy, which destabilized the price level.

In this case, the truth is somewhere in between. Inflation rose sharply in 2021 and has fallen off a bit in recent months, but the change in inflation is much smaller than the change in money growth. This means that most of the change in money growth reflects the Fed accommodating a shift in the real demand for money, and a smaller portion reflects an exogenous monetary policy that caused inflation to rise sharply and then fall back somewhat.

Here I’d like to focus on the shift in real money demand, which explains most of the pattern we observe in the graph. Why did the public wish to hold larger real cash balances in 2020 and 2021, and why has the real demand for cash balances fallen off somewhat in recent months?

The answer seems clear. Nominal interest rates plunged from 2.5% to zero during the Covid crisis of March 2020, and nominal interest rates rose sharply during 2022. The fall in nominal interest rates sharply increased the demand for real cash balances (although other factors such as stimulus checks might have also played a role.)

With the recent rise in nominal interest rates, investors are moving from relatively lower yielding bank accounts to higher yielding alternatives.

I don’t pay much attention to the monetary aggregates, as I believe the Fed mostly accommodates shifts in money demand. One counterargument is that those who do focus on the monetary aggregates saw the inflation problem before the rest of us.

I would respond as follows. If the Fed had adopted an appropriate monetary policy during 2020 and 2021, the money supply still would have risen extremely rapidly, albeit a bit less rapidly than it actually did. And in 2022 the money supply growth rate might well have fallen more quickly. If that had occurred, those who focus on the money supply growth rate would have warned about an inflation crisis that (by assumption) never occurred.

There are certainly occasions when the money supply gives an accurate read on the stance of monetary policy, or at least the direction of a policy shift. Nonetheless, I find other indicators to be more useful, on average. (But not the Phillips Curve!!)

PS. Keep in mind that while the 30% M4 growth rate did accurately signal an upsurge in inflation, it did not give us any useful information on how high inflation would get.

On Saturday, the F-22 scored its first-ever victory against an airborne adversary when it shot down…a balloon.

There may not be a better metaphor for the costly grandiosity of the American military than the use of a multi-million-dollar fighter jet to dispatch an unarmed, unmaneuverable opponent. But the fact that the F-22 had never won a dogfight before its decisive victory over what may or may not have been a Chinese spy balloon is a nice illustration of why the United States has the world’s most expensive military by a massive margin.

In short, it’s because the Pentagon buys lots of expensive toys that have no use.

The balloon in question is absolutely massive, with “an undercarriage roughly the size of three buses,” as The New York Times put it. This would be an absolutely bonkers way to spy on the United States—especially since the images it picks up are reportedly no better than those it can obtain through satellites. One defense official said, as summarizedThe Washington Post, that the images a balloon like this could obtain “wouldn’t offer much in the way of surveillance that China couldn’t collect through spy satellites.”

Anyone on the ground could see the balloon in the sky without any sort of specialized equipment. To believe this was meant as a secret spycraft, you’d have to believe the Chinese authorities are just absolute morons, which (whatever else they might be) clearly isn’t true.

The US labor market burned red-hot in January as hiring unexpectedly surged and unemployment fell to a 53-year low, defying recession forecasts and adding pressure on the Federal Reserve to keep raising interest rates.

Nonfarm payrolls increased 517,000 last month after an upwardly revised 260,000 gain in December, a Labor Department report showed Friday. The unemployment rate dropped to 3.4%, the lowest since May 1969 and average hourly earnings grew at steady clip.

Welcome to a new blog on the endlessly perplexing problem of monetary policy. You’ll quickly notice that I am not a natural blogger, yet I feel compelled by recent events to give it a shot. Read more...

My name is Scott Sumner and I have taught economics at Bentley University for the past 27 years. I earned a BA in economics at Wisconsin and a PhD at Chicago. My research has been in the field of monetary economics, particularly the role of the gold standard in the Great Depression. I had just begun research on the relationship between cultural values and neoliberal reforms, when I got pulled back into monetary economics by the current crisis.

"I am SURE that that high speed rail line will only need a grant of $3 billion. Maybe less, if they underspend. High speed rail construction in developed countries has..."

"Apparently you agree with Masha Gessen. From Sam Harris Episode 131 with Masha Gessen. Here's the quote... "I'm not saying that public opinion can't be judged. I'm not saying that..."

"Thomas, GDP growth was 4.7% in Q1, that's still too strong. (RGDP doesn't matter.) AI might affect productivity at some point, but we are still at least a few years..."