Never reason from a quantity

I see lots of commenters making an EC101 error. They notice that Canadians are much more likely to live in high rises, and assume that this reflects a difference in preferences. It’s certainly possible that preferences differ in one country from another, but to demonstrate that to be true you’d first have to consider supply factors.

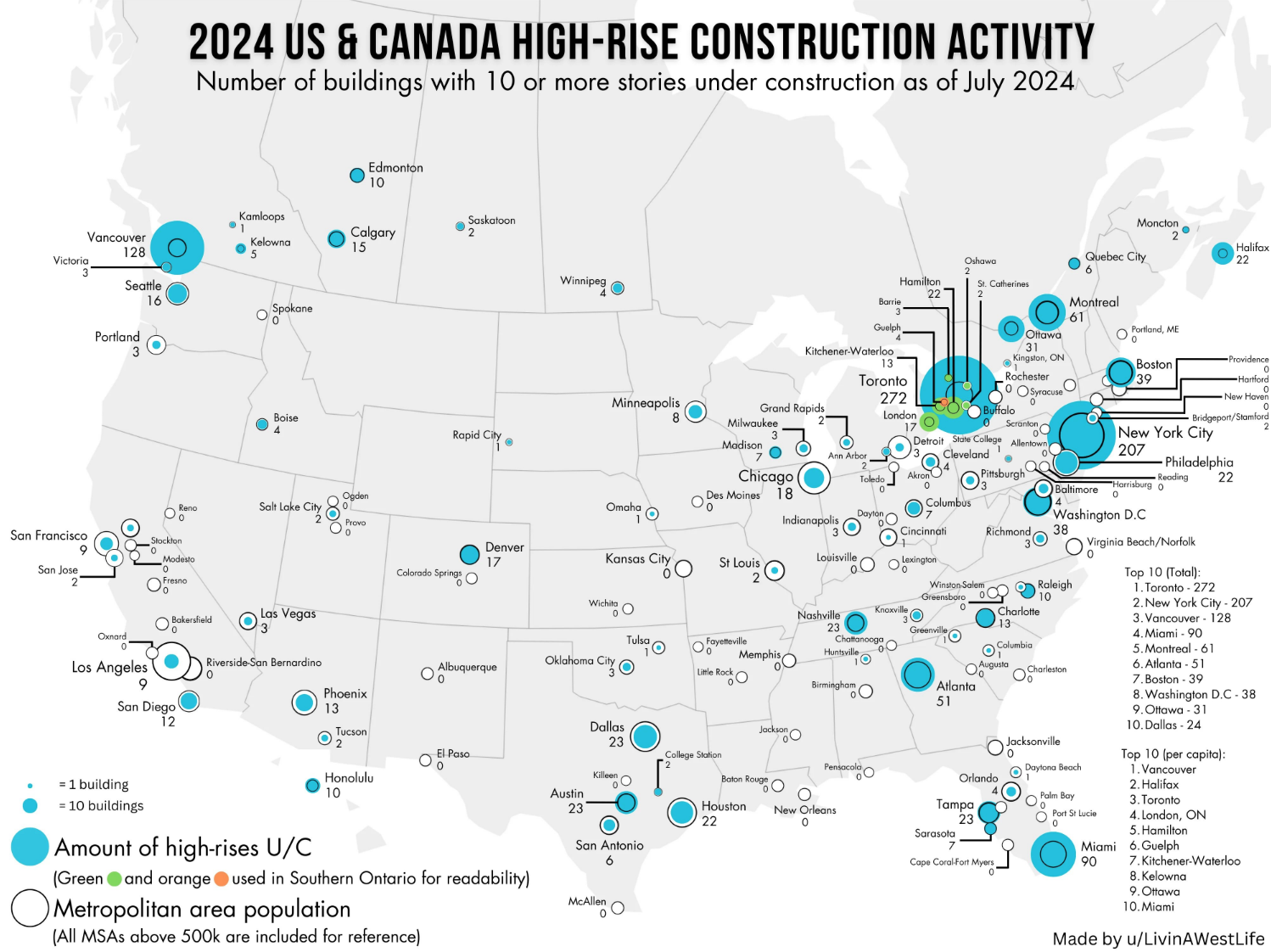

Canada builds almost 20 times as many high rises as California, despite having a similar population. It might be true that Californians don’t like high rises. But if that were the case, then why are high rise condos in California so incredibly expensive? Even a very small condo in San Francisco costs well over a million dollars. The high price of apartments and condos in California is a pretty good indication that there is strong demand for such units.

So why are they not being built? Presumably because it’s too expensive, or perhaps it’s impossible to get permission to build due to zoning regulations. I suspect it’s a bit of both. Construction costs might be a bit higher due to earthquake risk, but by far the most important factor is regulation, which increases the cost to build in all sorts of different ways. (Lots of high rises were profitably built in places like Santa Monica and Marina Del Rey before regulation made it almost impossible to get approval.

People mentioned that Canadian cities have restrictions on suburban development. Well California has extremely restrictive limits on suburban development.

What would low demand for high rise living look like? Check out the market for condos in places like St. Louis, Detroit and Cleveland, where you can find units at very reasonable prices. Those are cities where it makes sense to suggest that low demand explains a dearth of construction. But San Francisco? San Jose? Los Angeles? San Diego? There’s an extreme need for more housing. The same is true in New York and Boston. Lots of high rises have been going up in Jersey City precisely because their regulations are less strict.

No, it’s not a lack of demand—the price of housing here in California is insanely high, and getting higher, and yet very little construction is occurring. Orange County now has the fastest rising house prices in America, and yet (outside Irvine) construction seems to be slowing down. It’s almost all due to zoning and regulation.