The best

The perfect male hero must be strong, sexy, and quick-witted. In the 1960s, Sean Connery was the man every other man wanted to be:

From Russia With Love and The Man Who Would Be King are good places to begin.

A slightly off-center perspective on monetary problems.

The perfect male hero must be strong, sexy, and quick-witted. In the 1960s, Sean Connery was the man every other man wanted to be:

From Russia With Love and The Man Who Would Be King are good places to begin.

So I’m just confused by one thing. Given that Covid is now exploding in rural states in the north central US, and given that doctors are often well liked in small towns, just why does Trump think this kind of headline (4 days before the election) will help him to win Iowa?

Trump Claims at Rally Doctors Lie About Virus Dead for Money

He’s not saying that one or two doctors lie, he’s says our high reported Covid fatality rate is due to doctors lying for money.

Paging Scott Adams.

This is awkward for me because I picked Trump to win, and he seems to be going out of his way to make me look like a fool for the second time in 4 years. I’m starting to give up ho . . . er, I mean fear.

Bloomberg has a good (but sad) story about how Covid is now ravaging rural Montana:

Covid-19’s sweep across rural America is forcing small regional hospitals and far-flung facilities like these, many with few doctors and no ventilators, to combat a virus that has stressed even the world’s biggest health-care systems.

In Hardin, the seat of the Connecticut-sized county, Mayor Joe Purcell doubles as head of nursing for a long-term care home. He’s worked all but two days since the end of July thanks to the triple burden of caring for Covid patients, enforcing lockdown regimes and a lack of staff.

“You kind of get a feeling of helplessness,” said Purcell, 54. “You’re just looking for that light at the end of the tunnel.”

I guess mayor Purcell doesn’t understand that it’s all a hoax.

As of July 7, Montana had a total of 23 deaths over 4 months. Today they had 27.

Oh, I have just one more question. Trump aides are now basically admitting that the preferred strategy is herd immunity, i.e. do nothing. Trump says a herd immunity policy would have resulted in 2 almost million deaths. So is Trump’s campaign platform now, “vote for me and I’ll deliver 2 million corpses”? (Yeah, the 2 million figure is excessive, and presumably they still want to protect nursing homes, but will voters pick up on these nuances? What’s his point?)

Oh, and just one more question (from commenter D.O.):

Republicans insist that the popular vote is meaningless and that the actual Election Day should and does occur on December 14, when 538 electors elector our next president. So when Trump says he wants all votes counted on Election Day, he means precisely what?

Oh, and one more question. Republicans make a big issue about how Trump is tough on Iran. So how does Trump leaning on the Justice Department to go soft on Turkey for violating the Iran sanctions because Trump has valuable investments in Turkey actually help this policy?

OK, maybe that wasn’t the reason. Some claim Trump just likes authoritarian thugs like Erdogen more than he likes our democratic allies in Europe. So the European banks get hit with tougher sanctions.

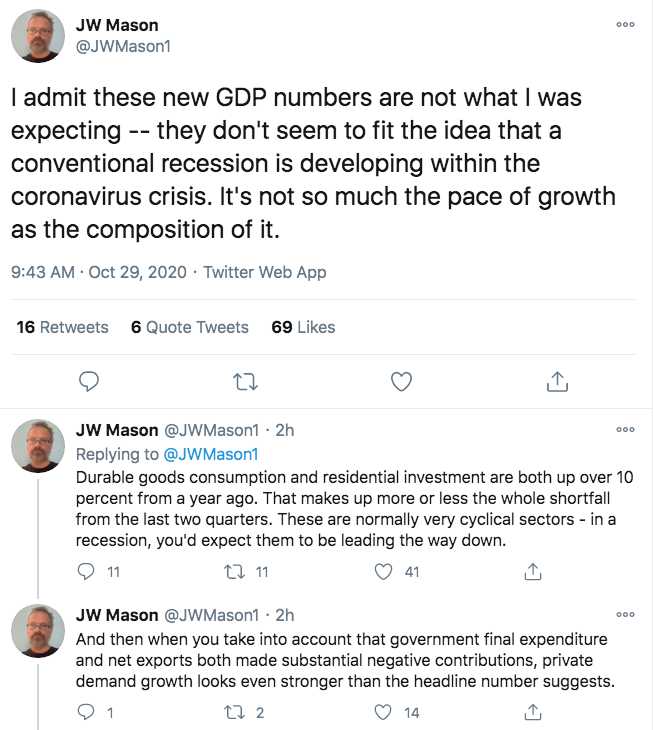

As I keep saying, not only is this not your granddad’s recession; it’s not like any recent recession. Check out these tweets from JW Mason:

Those of us who teach basic macro generally use a AS/AD model where recessions can be caused by either demand or supply shocks. Students might get the impression that both types are fairly common. In fact, almost all recessions in the US are due to demand shocks. So when a bona fide supply shock (aka real shock) comes along, we don’t know what to make of it.

If the Covid pandemic were to end soon, the economy would recover quickly. If not (and of course it’s not likely to end soon), then there’s a real danger that this morphs into a demand-side recession. But as of today, it still looks like a real shock.

In 2009, it was hard to get people to buy houses, cars and boats. If Covid ends, it won’t be hard to get people to go out to eat, go on vacations, or get haircuts.

HT: Matt Yglesias

Check out this headline:

Ted Cruz says the swelling national debt will reemerge as a major concern for Republicans

I have frequently argued that the Electoral College (EC) makes disputed elections far more likely, and a new study (or “model” if you insist) shows this to be the case. And not just slightly more likely, this sort of electoral fiasco is 40 times more likely to occur under the EC.

For a certain type of intellectual, it’s fashionable to take the contrarian stand on the EC and argue that it is actually a good system. They often rely on “Chesterton fence”-type arguments. The framers must have had good reason to put this system in place.

But the Chesterton fence argument is actually not very relevant to this issue. Other countries generally elect their president by majority vote (although a few “ceremonial” presidents are picked by an EC, as in India). So if you plan to a rely on an argument that, “for some mysterious reason real world societies have adopted the EC, despite the fact that it seems undemocratic”, you will lose. Almost all real world societies have done the opposite.

Then you might argue, “But the US is a special place, and the EC fits our unique situation.” But again, that’s a losing argument. The US in 2020 is much more like France in 2020 than it is like the US in 1787. Back then, the US was a collection of loosely attached states that were viewed as semi-autonomous. There was a small and weak central government. We were largely rural. There was slavery, and a debate over how slaves should impact a state’s political weight. (The EC had the effect of boosting the power of slaveowners, as slaves could not vote.) Communication between the states was difficult. A reliable national vote count would have been logistically difficult.

Both modern America and modern France have a huge national government. They are highly urban societies and do not have slavery. There is instant communication and we have the technology to conduct national elections. We are nothing like the America of 1787. The only reason we still have the EC is that our Constitution is very hard to amend, particularly when the amendment would reduce the power of smaller states.

Suppose the Framers had decided that each county would have one electoral vote. Would you still assume that the framers knew best? Would you be OK with a remote west Texas county of 169 people having the same influence as LA county’s 10 million? If not, why assume the current system is appropriate, just because the framers set it up that way under radically different conditions?

Yes, the Constitution says there shall be an Electoral College. The Constitution also says that a future Democratic administration can make 5 more states out of tiny Pacific Islands. Or NYC can be turned into 5 states. I don’t want that. That’s banana republicanism.

I’m not in favor of frequently amending the Constitution, but an amendment getting rid of the EC seems long overdue.

The EC caused the election fiasco of 2000, and some day it will cause another (and perhaps more violent) fiasco. It’s useless, undemocratic and destabilizing. Get rid of it.

Update: Here are 14 short essays by critics of “Critical Social Justice” who oppose Trump. Recommended.