Back in August and September 2022, the German unemployment rate was only 5.5%. Then Germany plunged into recession. Here’s Bloomberg:

Germany suffered its first recession since the start of pandemic, extinguishing hopes that Europe’s top economy could escape such a fate after the war in Ukraine sent energy prices soaring.

First-quarter output shrank 0.3% from the previous three months following a 0.5% drop between October and December, the statistics office said Thursday. Its initial estimate, last month, was for stagnation.

As a result of this “recession”, the German unemployment rate has soared to 5.6%.

Perhaps this data sheds a bit of light on the point I was making in my previous post.

PS. If you prefer the other German unemployment measure (the harmonized unemployment rate), it’s fallen from 3.1% to 2.8% during the “recession”.

Over the past year, I’ve read one pundit after another offer a recession prediction. I’m not impressed.

It’s not that these predictions are necessarily incorrect—a recession might well occur in the near future. It’s that these predictions are useless. What am I supposed to do with the forecast? We already have market forecasts of a wide range of macro indicators.

History suggests that recessions occur every so often and are largely unforecastable. Economists as a group have failed to predict any recent US recession. Last year, lots of economists thought we’d be in a recession by now. Instead, we have the lowest unemployment rate since 1969. (But they also thought we had a “tight money policy” because interest rates were rising. Hmmm . . . please read my new book.)

I’d be much more interested in an unemployment rate forecast. The Fed currently expects the unemployment rate to rise to 4.6% by year end. It would take a recession for that to happen. But a recession could also lead to 7% unemployment, as in the relatively normal 1991 downturn. And yet a 4.6% unemployment rate is much closer to our current situation than it is to 7% unemployment. Simply saying “recession” tells me relatively little about what you expect to happen to the economy. What sort of recession?

Don’t get me wrong. I concede that the recession forecasts will eventually match reality. At some point we will have a recession. Until then, I wish pundits would just keep their mouths shut. I can see the fed funds futures market for myself. I don’t need anyone telling me what they think is likely to happen.

Knee-jerk retaliation runs the risk of violating WTO rules and exposing G-7 members to charges of hypocrisy. While that may not faze US leaders, they should understand that they will have an easier time persuading other nations to unite behind a common effort if it’s aimed at preserving the rules-based system of global trade, not demonizing China. To fight bullying, there’s no need to become a bully.

I’m afraid it’s too late; both political parties now favor bullying smaller nations.

3. The FT reports that unemployment is falling in Greece:

“The macroeconomic progress has been undoubtedly mad in the past four years in terms of growth, reduced unemployment and falling debt-to-GDP ratio,” said Dimitris Papadimitriou, professor of political science at the University of Manchester.

“The flip side is the cost of living . . . Greek average wages remain very low despite the fact that unemployment has come down, leading to the second-worse purchasing power in the EU, only better than Bulgaria,” he added.

The use of “despite” makes me smile. Sort of like when the NYT reported that prison populations were soaring despite a fall in crime.

A few weeks back, I wrote a post making a similar point:

Because of the way that we perceive time, when we are in the midst of a problem we don’t tend to perceive it as a blip in history, which will soon be replaced by another set of concerns. For this reason, there can be real benefit to foreign policies that “kick the can down the road,” if we are able to avoid outright war. Today, it seems as though places like Russia, China, Iran, North Korea, Cuba and Venezuela will never become free. But who knows what the world will look like in another 30 years.

5. New Hampshire used to grow faster than Massachusetts, for some pretty obvious reasons. It had no income tax, and is right in the path for suburban overflow development outside of the crowded Bay State. But in the 2010s, Massachusetts started growing faster than New Hampshire. That puzzled me, until I read this post by Matt Yglesias:

Okay, it’s New Hampshire. It’s not for us urbanists, and it doesn’t seem like there’s much demand for dense urbanism there. But how about “normal” detached single-family housing — a house and a yard that’s near another house with another yard? Well, it turns out that lots smaller than one acre are only allowed on 16% of the state’s buildable land.

So in this case it’s not smart, walkable urbanism that’s been banned across the majority of New Hampshire — it’s suburbanism.

6. Back in the days of Margaret Thatcher, I thought of the Tories as the pro-growth party and viewed Labour as anti-growth. Now things seem to have flip-flopped. Here’s The Economist:

Labour is posing as the party of Builders. Places that most support housing are in the places Labour needs either to hold or win back at the next general election, according to Mr Ansell’s study. Support for home-building is concentrated in London and smaller cities as well as in Scotland and the so-called Red Wall, a ribbon of northern constituencies that Labour lost in the 2019 election. Plenty of natural Labour supporters may balk at building. But this is a fight the party wants to have. For Labour, nimbyism is another abstract noun to be abolished, like crime or poverty.

The Conservatives have ended up as a party of Blockers.

When it comes to British growth prospects, housing is pretty much the only issue that matters.

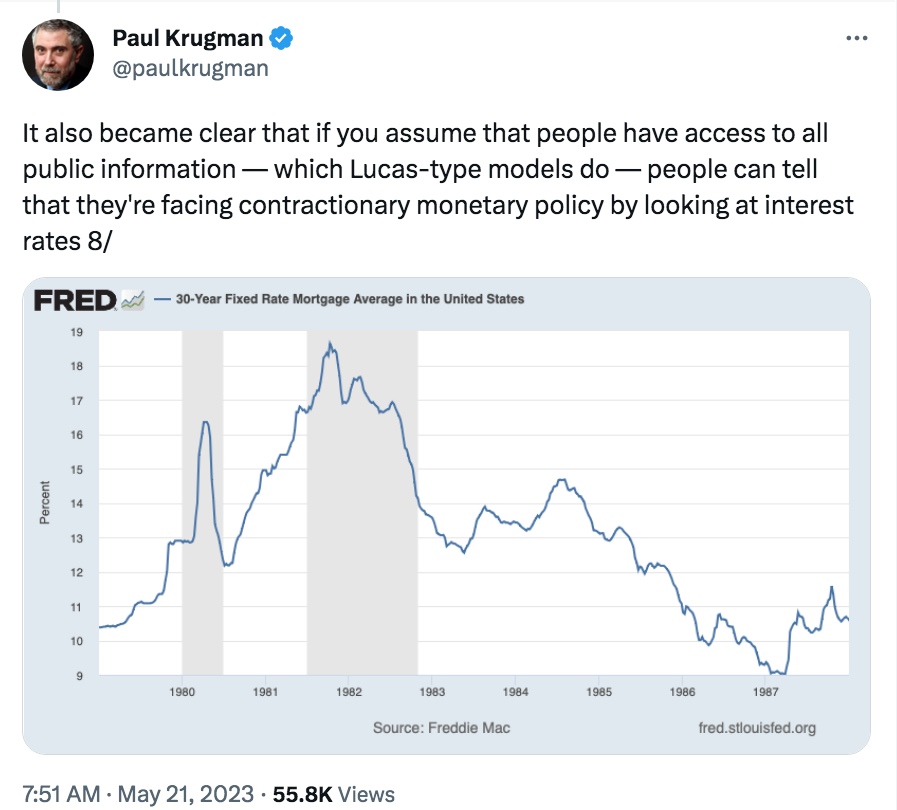

By this logic 2022 should have been a recession year. No, you cannot ascertain the stance of monetary policy by looking at interest rates, which would be “reasoning from a price change”. To be fair, the same applies to money supply growth, which was the key variable in Lucas’s 1972 business cycle model. Velocity is too unstable.

If people thought that the technology was going to make everyone richer tomorrow, rates would rise because there would be less need to save. Inflation-adjusted rates and subsequent GDP growth are strongly correlated, notes research by Basil Halperin of the Massachusetts Institute of Technology (MIT) and colleagues. Yet since the hype about AI began in November, long-term rates have fallen. They remain very low by historical standards. Financial markets, the researchers conclude, “are not expecting a high probability of…AI-induced growth acceleration…on at least a 30-to-50-year time horizon.”

That’s not to say AI won’t have some very important effects. But as with the internet, having important effects doesn’t equate to “radically affecting trend RGDP growth rates”.

9. The FT has a piece on how the US is losing ground to China in Latin America:

The US and EU, meanwhile, have been focusing on corruption, democracy, the environment, human rights and the risks of doing business with China. The EU’s Global Gateway initiative, envisioned as a response to the BRI, has pledged just $3.5bn to Latin America.

Among the US’s talking points with Latin America is an entreaty to avoid 5G phone networks built by China’s Huawei, which is sanctioned by Washington — but US and European alternatives to Huawei are often more expensive.

A Latin American foreign minister last year compared the American approach to the Catholic religion, telling the Financial Times that “you have to go to confession and you still may end up being damned”.

The Chinese, by contrast, were like the Mormons who “knock on your door, ask how you are feeling” and “want to help”.

Of course the US has been explicitly trying to sabotage Huawei, and in doing so is indirectly damaging the economies of Latin America. But at least they get to hear our sanctimonious lectures on human rights!

10. Another FT story warns that our war on China’s chip industry might backfire:

Speaking to the Financial Times, Jensen Huang said US export controls introduced by the Biden administration to slow Chinese semiconductor manufacturing had left the Silicon Valley group with “our hands tied behind our back” and unable to sell advanced chips in one of the company’s biggest markets.

At the same time, he added, Chinese companies were starting to build their own chips to rival Nvidia’s market-leading processors for gaming, graphics and artificial intelligence.

“If [China] can’t buy from . . . the United States, they’ll just build it themselves,” he said. “So the US has to be careful. China is a very important market for the technology industry.”

Anti-Chinese bigotry seems to get worse each year. The leading contender for the GOP presidential nomination mocks people with Chinese names. Biden’s Washington is increasingly hysterical about the China threat.

Some people push back by claiming that they object to the Chinese government, not the Chinese people. If only that were so. Here’s Bloomberg:

The American Civil Liberties Union sued Florida over a law championed by Governor Ron DeSantis that bars most Chinese citizens from buying homes in the state.

The law, set to take effect July 1, violates the equal protection and due process guarantees under the Constitution by prohibiting landownership based on “race, ethnicity, color, alienage, and national origin,” according to the suit filed Monday in federal court in Tallahassee.

The ACLU sued on behalf of four Chinese citizens, claiming the law “stigmatizes them and their communities, and casts a cloud of suspicion over anyone of Chinese descent who seeks to buy property in Florida.”

More than a dozen state legislatures have introduced similar bills, with many targeting people from China, the ACLU said.

Hardly a day goes by without a news story describing how DeSantis wants to ban one thing or another. One day he bans corporations from setting their Covid policies. Another day he restricts the freedom of teachers to talk about gender issues. The next day he’s restricting the speech rights of Disney. Then an abortion ban. Then he tries to prevent Gainesville from deregulating to allow more homebuilding. He’s against legalizing pot.

More importantly, the Fed has yet to adequately recognize two important ways monetary policy contributed to the crisis.

First, by committing to keep short-term interest rates near zero until the economy reached full employment and inflation exceeded 2%, the Fed ensured that it would be very late in tightening monetary policy. When inflation overshot, it had to raise rates faster and higher than it would if it had been more preemptive. As a result, it delivered a significantly larger shock to banks’ funding costs and to the value of the banks’ longer-term investments.

Second, the Fed’s quantitative easing program, by exchanging cash for securities, flooded the banking system with reserves and deposits. In the low-rate environment of 2020 and 2021, this naturally tempted some banks to boost earnings by buying higher-yielding, long-term, fixed-income assets.

But I disagree with Dudley’s conclusion:

I see three lessons for the Fed. First, the Federal Open Market Committee should consider financial stability risks in its monetary policy decisions.

Dudley correctly observes that the same Fed policy that led to a bad outcome for banking also led to a bad macroeconomic outcome. The alternative policy that he recommended would have led to a better macro outcome. Focusing like a laser on stable NGDP growth won’t eliminate banking problems, but at least it will avoid having monetary policy exacerbate those problems.

PS. Speaking of Bloomberg, it really annoys me when reporters misstate the Fed’s inflation target, which applies to the PCE, not the CPI:

US consumer prices rose 0.4% in April with headline CPI up 4.9% on a year-on-year basis, its first reading below 5% in two years. That’s still well above the 2% level targeted by the Fed as central bank officials juggle the need to curb rampant inflation against a potential recession and banking sector angst.

Welcome to a new blog on the endlessly perplexing problem of monetary policy. You’ll quickly notice that I am not a natural blogger, yet I feel compelled by recent events to give it a shot. Read more...

My name is Scott Sumner and I have taught economics at Bentley University for the past 27 years. I earned a BA in economics at Wisconsin and a PhD at Chicago. My research has been in the field of monetary economics, particularly the role of the gold standard in the Great Depression. I had just begun research on the relationship between cultural values and neoliberal reforms, when I got pulled back into monetary economics by the current crisis.

"This man is the devil. Look at his eyes. Same as Soros. All baggy and nasty. Good people dont age like that. Its the sign of a madman. A negativity..."

"I watched Satantango on video over 3 days. I found it absolutely gripping, but one must surrender for a time one's idea of what a movie should be. Instead, you..."