[Over at Econlog, I have a post explaining 3 MMT fallacies.]

In my recent Mercatus paper I criticized interest rate targeting and also suggested an alternative. One problem with interest rate targeting is that it doesn’t work well when nominal rates fall to zero, or slightly below zero. Fortunately, there are many possible alternatives.

One famous alternative is money supply targeting, as proposed by Milton Friedman. But even Friedman moved away from this idea late in his career. Here I’d like to focus on alternative asset price targets. After all, if you target short-term interest rate then you are also implicitly targeting the price of assets such as one-month T-bills. Here are some better options:

1. Exchange rates: This is the system that Singapore uses:

Fourth, the choice of the exchange rate as the intermediate target of monetary policy implies that MAS gives up control over domestic interest rates (and money supply). In the context of free capital movements, interest rates in Singapore are largely determined by foreign interest rates and investor expectations of the future movements in the Singapore dollar.

The downside of the policy is that it probably doesn’t work for big economies—the trading partners would object.

2. A stock price index: This is the system that Roger Farmer advocates. The downside is that stocks can move for reasons unrelated to changes in NGDP, such as a corporate tax cut that increases the share of after-tax GDP going to corporations.

3. A gold price target: This was the method used by FDR during November 1933. The problem is that it worked because markets understood that movements in gold prices were an indicator of the future path of monetary policy, once convertibility was restored (in February 1934). That’s not the case today.

4. A commodity price basket: Supply siders used to occasionally advocate targeting the price of a basket of actively traded commodities. The problem is that even a diversified basket of commodities can have a very unstable relative price.

5. The TIPS spread: First proposed in 1989 by Robert Hetzel, this idea was recently revived by John Cochrane. One problem is that there might be a time varying risk premium on TIPS spreads. Another is that it doesn’t address the Fed’s dual mandate.

6. NGDP futures targeting, guardrails version: This is my preferred policy, with no IOER and OMOs used as the policy instrument. It doesn’t really have any downsides (as you’d expect of a policy that I favor) except that central banks are reluctant to adopt such a radical policy.

7. Hybrid model/market-based policy; The central bank targets the NGDP forecast, with 50% weight given to a prediction of NGDP based on basket of asset prices and 50% weight given to a prediction of NGDP from Fed models and private forecasters. Once the non-asset price part of the forecast is established, policy targets the basket of asset prices at a level expected to produce on-target NGDP, when averaged in with the non-asset price NGDP forecast.

All these approaches should use level targeting.

For some reason, MMTers often seem to think that the Fed can’t target anything but interest rates. Singapore shows that’s not the case. In Singapore, both money and interest rates can be viewed as endogenous, as it should be.

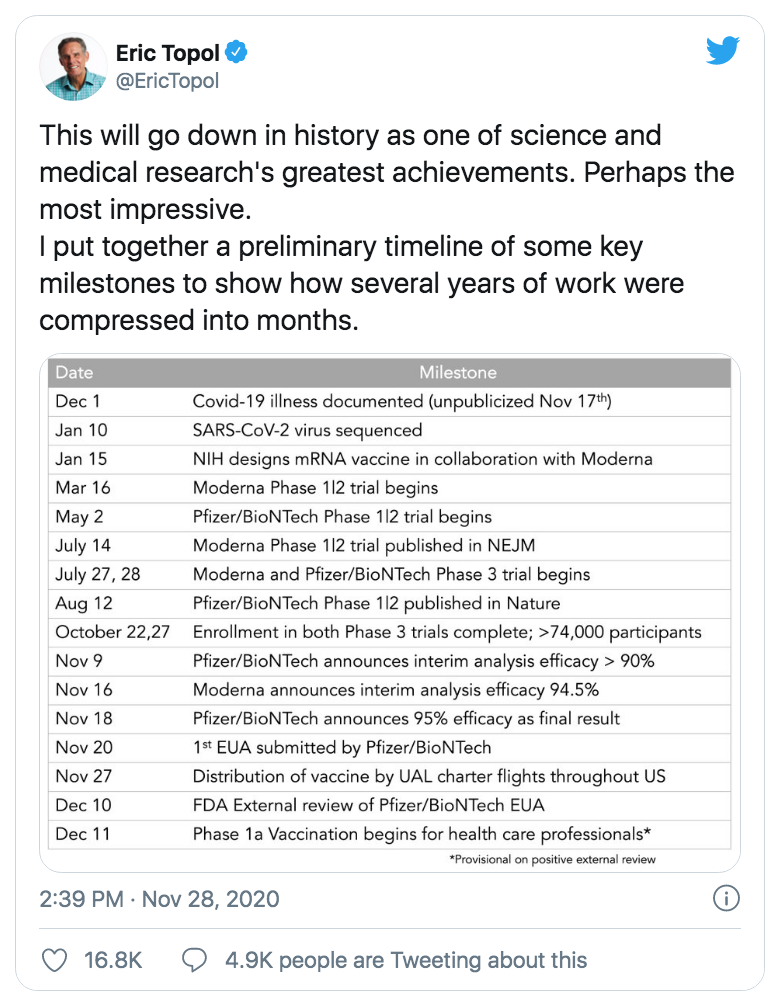

Topol describes this as a great achievement, and he’s right. (My wife used to work in vaccine development, so I’m well aware of how long this usually takes.) At the same time, I can’t help thinking that the following would have been an even greater achievement, one that would have saved the lives of 100,000 Americans and also prevented many small business bankruptcies. (Yes, Trump would have been re-elected, but that’s a price worth paying):

Mar 16: Moderna phase 1/2/3 challenge trial begins.

May 2: Pfizer/BioNtech phase 1/2/3 challenge trial begins.

July 14: Moderna phase 1/2/3 published in NEJM.

July 31: FDA approves Moderna vaccine.

August 12: Pfizer/BioNtech phase 1/2/3 published in Nature.

August 31: FDA approves Pfizer/BioNtech vaccine.

PS. Tyler also linked to an article on the developer of Novavax’s promising new vaccine candidate, created by a team led by Nita Patel:

Patel has come a long way from her beginnings in Sojitra, a farming village in India’s Gujarat state. There, when she was 4 years old, her family fell into poverty after her father nearly died from tuberculosis (TB). He never worked again and told Patel she should become a doctor and find a cure.

Patel set about doing that, wearing the same ragged dress to school day after day. She had no shoes. She begged bus fare from a neighbor—at whose house she also devoured the newspaper because her family couldn’t afford a subscription.

Her academic excellence propelled her through college on government scholarships. She later picked up two master’s degrees, in India and the United States, in applied microbiology and biotechnology.

Moderna’s Pfizer’s vaccine was developed by the children of Muslim immigrants to Germany, and this one by an immigrant from a “shithole country”. Funny how things work out.

Some commenters who are sympathetic to MMT seem unfamiliar with the standard view of why money matters. They argue that swapping base money for an equal dollar value of bonds doesn’t matter, because the recipient of the new money is no better off than before. It’s true they are (approximately) no better off, but that’s NOT why economists think money matters. It would be nice if commenters showed they understood the traditional view, and then explained why it’s wrong and MMT is right.

Conventional economists believe that an injection of new base money creates a situation of excess cash balances. Keynesians believe the attempt to get rid of these excess cash balances causes bond prices to rise (i.e. interest rates to fall), and this boosts AD. Monetarists believe that the attempt to get rid of excess cash balances causes the price of a wide range of assets to rise, not just bond prices. Thus the Fed announcements of January 2001 and September 2007 caused only a small decline in short-term interest rates, but a big rise in stock prices. (BTW, long-term rates actually rose both times due to the Fisher effect—a factor ignored by MMTers.)

Monetary stimulus boosts the prices of T-bills, stocks, commodities, real estate and foreign exchange. I.e., it depreciates a currency. During normal times such as the 1990s, the difference between Keynesians and monetarists is just a theoretical curiosity. They both agree that monetary policy drives NGDP; they merely differ in how they see the transmission mechanism.

When rates fall to zero, however, the monetarist model is clearly superior. In March 2009, the Fed announced a QE program and as a result stocks rose and the dollar sharply depreciated against foreign currencies. That’s consistent with the monetarist model and inconsistent with the (extreme) old Keynesian view that monetary injections don’t matter at zero rates. (In fairness, New Keynesians have a more nuanced view.) MMTers seem to think money never matters, even at positive interest rates, although as I pointed out in this post it’s hard to be sure, as their statements are so contradictory.

Here’s an analogy. When there’s a big apple crop, the new apples are sold at market prices. The wholesalers who buy the apples do so at competitive prices and thus don’t feel any richer. They see no need to go out and spend more. But they do have excess apples, which puts downward pressure on the value of apples.

Inflation is a fall in the value of cash. A big crop of new money puts downward pressure on the value of cash. If the government sells me a briefcase full of $1 million cash in exchange for an equal value of bonds, I’m no richer than before. I won’t go out and buy a new Ferrari. But I will have much more cash than I prefer to hold, and I’ll get rid of that extra cash.

And here’s where the fallacy of composition comes in. While I can get rid of the extra cash by purchasing bonds, stocks, commodities, real estate or foreign exchange; society as a whole cannot get rid of the excess cash by purchasing other assets. Doing so is merely “passing the buck”.

But the public’s attempt to get rid of excess cash balances will drive up the price of a wide range of assets, leading to more total spending, more NGDP. Eventually NGDP will rise high enough so that people are willing to hold the larger cash balances, and a new equilibrium is established.

All of this is ignored by MMTers. They seem to think that swapping cash for bonds is “irrelevant”, even when interest rates are positive.

In fact, an exogenous and permanent increase in the money supply of X% will cause prices and NGDP to rise by X% in the long run. Money is neutral in the long run; just as changing a country’s measuring stick from feet to meters doesn’t change the actual (“real”) length of objects.

In the weeks before the election, I viewed Wisconsin to be the most likely “tipping point state”, as it was in 2016. It turns out I was correct on that point. So goes Wisconsin, so goes America.

In September, I had expected Trump to win. But when I saw the following story on October 28, I couldn’t in good faith predict that Trump would win. Thus in the end I wimped out and predicted nobody.

Biden up 17 points in new Wisconsin poll

Democratic presidential nominee Joe Biden holds a commanding lead over President Trump in Wisconsin in a new poll of the key battleground state released less than a week before Election Day.

The ABC News-Washington Post poll found Biden supported by 57 percent of likely voters, far ahead of the president’s 40 percent.

Unlike Nate Silver (and many of my commenters), I knew that polls were understating Trump’s support. The betting markets knew this too. And I knew there is a 3% margin of error in polls. But surely polls can’t be off by 17%!

And I was right. The WaPo/ABC Wisconsin poll was not off by 17%. It was off by 16.4%. That’s why Biden won.

PS. I’m not a conspiracy theorist, but if I were I’d be asking how Trump could have done 16.4% better than the WaPo/ABC poll. Massive GOP election fraud in a failed attempt to steal the election?

I believe the answer is yes, due to “transitivity”. But what do MMTers believe?

Let’s say A is: Big open market operations occur when interest rates are positive.

And B is: Interest rates change by a large amount.

And C is: Has a significant impact on the economy.

The MMT textbook I’ve been reading suggests that A does not imply C:

Monetarists are hostile to the creation of base money to finance deficits because they claim it is inflationary due to the Quantity Theory of Money (QTM). MMT advocates would first highlight institutional practice, namely that net treasury spending initially causes an equal increase in base money.

Second, they would challenge the theory of inflation based on QTM, and argue that if a fiscal deficit gives rise to demand pull inflation, then the ex post composition of ΔB + ΔMb in Equation (21.1) is irrelevant. Overall spending in the economy is the driver of the inflation process, and not the ex post distribution of net financial assets created between bonds and base money.

When I first read this I thought:

1. This is a shocking claim.

2. This is clearly wrong.

So I set out to try to discover why they hold this highly controversial heterodox belief. Do MMTers believe that OMOs don’t have a big effect on interest rates, or do they believe that big changes in interest rates are irrelevant?

On page 364, the authors clearly indicate that they believe a big open market purchase could immediately drive interest rates sharply lower, perhaps to zero:

However, this mainstream argument [for a money multiplier] fails to recognise that the added reserves in excess of the banks’ desired reserves would immediately drive the interbank rate to zero or to a non-zero support rate

The term “non-zero support rate” presumably refers to IOER, but we can ignore that since I’m considering a big OMO in 1998, a time when IOER was zero. It is possible that a huge monetary injection could raise interest rates due to the Fisher and/or income effects, but we can rule that out as the authors are claiming “irrelevance”. A policy that has a big impact on inflation and/or real income is clearly not irrelevant. So they are obviously assuming the liquidity effect is the only relevant consideration after an OMO, in which case this MMT claim is certainly true. A big OMO would drive rates much lower, probably to zero.

OK, so MMTers correctly understand that big OMOs can have a major impact on interest rates. But perhaps interest rates don’t impact the economy?

On page 366, we find that big changes in interest rates do impact the economy:

While small changes in long-term interest rates (following corresponding changes in the target rate) may have little impact on spending, higher and higher long-term interest rates will eventually diminish domestic spending that is interest rate sensitive.

On page 369 they discuss the downside of a tight money policy:

Often too tight if it [i.e. monetary policy] is is geared to a low inflation rate (or target range), which can impose major economic and social costs of higher unemployment

(MMTers continually engage in the fallacy of reasoning from a price change, but I don’t want to be too hard on them on that point, as so do Keynesians, Austrians and NeoFisherians.)

The two key points are that OMOs can have a big impact on interest rates, and big changes in interest rates can have a “major” impact on the economy. A –> B and B –> C. But A does not imply C.

So I’m still confused.

In the comment section, people sometimes fall back on the claim that the Fed cannot arbitrarily adjust the monetary base because they target interest rates. They are mixing up several unrelated points:

Money is endogenous when you peg interest rates at a constant level.

A sudden change in the base could be disruptive for the banking system/economy.

Both claims are true, but have no bearing on the question of what would happen if you did a big OMO and didn’t care what happened to interest rates or the economy.

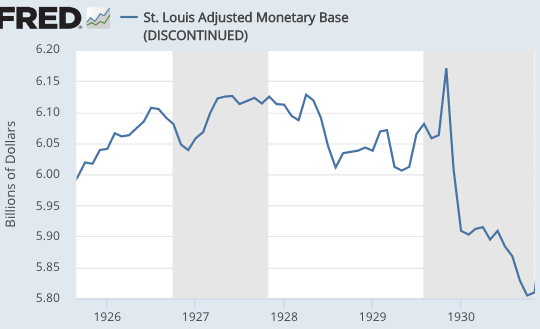

Yes, it would be very foolish to suddenly decrease the monetary base, as they did in 1929-30. That could drive the economy into a depression. But that doesn’t mean the Fed can’t reduce the monetary base. They have done so on several occasions. And it certainly doesn’t mean they cannot sharply increase the monetary base.

[The November 1929 spike is liquidity added right after the stock market crash.]

The textbook authors did not say that monetarists are wrong because the Fed has no technical ability to do discretionary open market purchases, they said that this action would be “irrelevant” if it were done. Monetarists know that money becomes endogenous if you peg interest rates, indeed that’s precisely why monetarists oppose interest rate pegs. So saying an interest rate peg makes money endogenous is not an effective critique of monetarism. Indeed monetarists either oppose interest rate targets entirely, or they favor adjusting the interest rate target frequently, as needed to keep the money supply on a non-inflationary path.

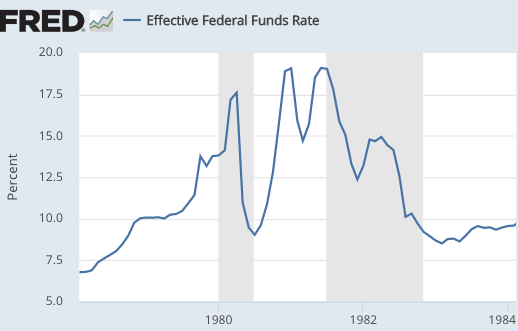

One commenter argued that the Fed continued to “set” interest rates even during the 1979-82 monetarist experiment. I’m OK with that as long as people understand that by “set” they mean this:

The Fed “set” the fed funds rate at 17.5% in April 1980, and then they “set” the fed funds rate at 11% in May 1980. A 650 basis point drop in one month. Is it just possible that the Fed had other objectives at the time, such as slowing money growth enough to reduce inflation?

And the textbook presentation of the monetarist experiment (p. 362) leaves much to be desired:

Many central banks, including those in the USA, UK, Canada, Germany and Australia, targeted a monetary aggregate that is a measure of the money supply in the late 1970s and early 1980s. They did so because through the Quantity Theory of Money (QTM), the growth rate of the money supply in the long run was alleged to determine the inflation rate. However, by the mid-1980s they had all discovered that they were unable to control the money supply, and abandoned this major plank of Monetarist thinking.

They didn’t “discover” they were unable to control the money supply, they came to believe that it was not a good idea. (Correctly, in my view.)

But that’s not my major complaint. Do you see the big problem in that paragraph? Students are informed that central banks such as the Fed adopted a monetarist policy in order to control inflation. But then students are not told the outcome of this policy experiment. Did the major central banks actually succeed in controlling inflation? Here’s the data they do not present:

Dec. 1978 – Dec. 1979: CPI rose 13.3%

Dec. 1979 – Dec. 1980: CPI rose 12.4%

Dec. 1980 – Dec. 1981: CPI rose 8.9%

Dec. 1981 – Dec. 1982: CPI rose 3.8%

And inflation has stayed fairly low ever since 1982. In other words, the monetarists were right that the Fed needed to abandon its previous interest rate smoothing policy and let rates rise as high as necessary to control the money supply growth rate. And the monetarists were wrong that a stable money supply target was a good idea (as they underestimated the volatility of velocity.) When inflation fell during the 1980s so did velocity, and the Fed rightly abandoned money supply targets and accommodated the increased demand for money

But students are not even told that the monetarist experiment succeeded in controlling inflation. Even if a textbook author (wrongly) believes it was just luck, and that the fall in inflation was unrelated to monetary policy, don’t you think that students would be interested in knowing how this famous anti-inflation experiment actually turned out?

Throughout the book you keep encountering sentences like:

The central bank would have no choice but to add reserves back into the banking system to keep the market (interbank) rate at its target level

Yes, but what if they were willing to let rates gyrate wildly, as in 1979-82? Are they still unable to inject or remove reserves on a discretionary basis? I cannot find an answer.

If you are willing to abandon interest rate pegging and let rates move around, then you can control the money supply. You should not have a strict money supply growth rule, but you should adjust the monetary base each day as necessary to keep market expectations of NGDP growth at 4%. And let interest rates be set by the market.

Welcome to a new blog on the endlessly perplexing problem of monetary policy. You’ll quickly notice that I am not a natural blogger, yet I feel compelled by recent events to give it a shot. Read more...

My name is Scott Sumner and I have taught economics at Bentley University for the past 27 years. I earned a BA in economics at Wisconsin and a PhD at Chicago. My research has been in the field of monetary economics, particularly the role of the gold standard in the Great Depression. I had just begun research on the relationship between cultural values and neoliberal reforms, when I got pulled back into monetary economics by the current crisis.

"This man is the devil. Look at his eyes. Same as Soros. All baggy and nasty. Good people dont age like that. Its the sign of a madman. A negativity..."

"I watched Satantango on video over 3 days. I found it absolutely gripping, but one must surrender for a time one's idea of what a movie should be. Instead, you..."