There may be a benefit in the short term, too, to raising targets now. Reducing stubbornly high inflation requires cooling the economy, which generally involves raising the unemployment rate. The lower the inflation target, the more unemployment central banks need to generate to get there. If the costs of inflation at 3% really are not much different from inflation at 2%, central banks will be generating additional unemployment for little benefit. . . .

Set against this, however, are the consequences of reneging on a 30-year promise. The experience of the past year has made clear that the public detests inflation; both finance ministries and central banks are being excoriated for losing control of price growth. To shift the goalposts now could give the impression of giving up the fight entirely. . . .

As long as inflation is so far off-target, such considerations seem likely to stay the hand of any would-be monetary reformers. Yet once it peaks, restoring a degree of central banks’ credibility, the pain of further disinflation, together with the promise of well and truly escaping the zero lower bound, could just start to make the idea of higher targets more alluring.

I’m not convinced that raising the inflation target is a good idea. But let’s say I’m wrong and that the benefits of moving to a 3% inflation target outweigh the costs. When should the target be raised?

The Economist suggests that it might be wise to do so in the near future, when inflation has fallen to 3% and further disinflation would lead to higher unemployment. I disagree.

If we are to move to 3% inflation, then we should wait until inflation has fallen back to 2% before making that intention public. At that point the Fed should announce that it will keep the 2% inflation target for immediate future, but plans to shift to a 3% inflation target during the next recession. That would make it seem more like a principled decision, and less like an expedient to avoid unpleasant choices, which would reduce policy credibility. If we make the change when inflation is overshooting the Fed’s target, why would anyone believe the new target would be adhered to?

PS. You may want to check out the 22nd Amendment to the Constitution, which was enacted before America became a banana republic. (Or the 27th Amendment). When people say they want to expand the Supreme Court, I respond, “As long as the new rule doesn’t take effect at a time which would benefit the current administration.”

Andersen said the studies don’t definitively disprove the lab leak theory but are extremely persuasive, so much so that he changed his mind about the virus’ origins.

“I was quite convinced of the lab leak myself, until we dove into this very carefully and looked at it much closer,” Andersen said. “Based on data and analysis I’ve done over the last decade on many other viruses, I’ve convinced myself that actually the data points to this particular market.”

Worobey said he too thought the lab leak was possible, but the epidemiological preponderance of cases linked to the market is “not a mirage.”

“It’s a real thing,” he said. “It’s just not plausible that this virus was introduced any other way than through the wildlife trade.”

In my view, this interpretation is far more embarrassing to the Chinese government than a lab leak, which is why the CCP continues to cover-up evidence that the pandemic began at one of China’s animal markets.

The BLM protests of 2020 (and subsequent “defund the police” movement), will end up worsening global warming. On the other hand, I don’t want to suggest that the woke are anywhere near as bad as the environmentalists, who continue to oppose low carbon nuclear, hydro, wind, solar and geothermal power.

3. And speaking of the woke, Wesley Yang provides a platform for a left wing teacher who reports on the state of our public schools. It’s even worse than you thought:

I’ve had liberal friends of mine dispute (to my face!) straightforward accounts of what my colleagues have said. They’ll tell me school districts could never embrace such obviously unworkable policies; what else can I do except shrug my shoulders and say, “I’m sorry, but yes, they can?” They’ll tell me I sound like one of those right-wing grifter types; what else can I do except sigh and tell them the grifters have a point?

This is where I have to stop and make one thing very clear: I’m a leftist. Like, a big one. I hate capitalism, I support abortion on demand, and I unironically use phrases like “systems of oppression” and “the dominant culture.” The last big paper I put together for my undergraduate degree was on critical race theory, for the love of God! I’m not the sort of person who can be easily dismissed as a conservative crank. But plenty of my fellow leftists are still willing to try, on the grounds that anyone who thinks there might be any problem with DEI policies must necessarily be a slack-jawed MAGA troll.

Read the whole thing. Still think I’m crazy for wanting to abolish the public schools?

4. It’s weird how politics evolves. When I was young, I used to praise Houston’s no-zoning policies. Progressives would roll their eyes at my fanatical libertarianism. Now it’s increasingly the conservatives who defend zoning, while progressives like Matt Yglesias want to abolish the practice. Here’s M. Nolan Grey:

Far from the doomsday predictions made by the zoning pushers in bygone eras, unzoned Houston works just fine. Between 1970 and 2020, the city nearly doubled in population from 1.2 to 2.3 million, assuming the title of America’s fourth-largest city. Attracting a blend of working- and middle-class Americans and international migrants seeking opportunity, Houston is now our nation’s most diverse city.

Thanks in part to a lack of zoning, Houston builds housing at nearly three times the per capita rate of cities like New York City and San Jose. It isn’t all just sprawl either: In 2019, Houston built roughly the same number of apartments as Los Angeles, despite the latter being nearly twice as large. This ongoing supernova of housing construction has helped to keep Houston one of the most affordable big cities in the U.S., offering new arrivals modest rents and accessible home prices even amid seemingly endless demand.

Most people are tribal, and conform to their tribe. I try to stick with my principles. Zoning is bad whether it’s being pushed by progressives or conservatives.

It’s also bad for politicians to tell teachers what to teach, whether they are forcing them to teach woke stuff or banning them from teaching woke stuff.

But Truss has the whiff of market monetarism about her. She has proposed a review of the Bank of England’s mandate. If the Bank didn’t have an inflation target, what would it have? Rather than targeting inflation, market monetarism involves targeting income. This is called a “nominal GDP target” — the Bank would be looking not just at inflation, but inflation and growth. It is the overall size of the economy that matters, not just the inflation rate. That is likely what Truss is looking for from her review of the Bank. In the Channel 4 debate, she pointed to Japan’s central bank as a model, which switched to nominal GDP targeting in 2015. (Economists like Scott Sumner recommend using market indicators to set interest rates; it’s not clear whether Truss supports that.)

Just to be clear, I favor NGDP level targeting, with the level targeting part of the policy being much more important than the NGDP part of the regime.

BTW, I don’t know enough about UK politics to have an opinion on the race for PM. As I’ve gotten older, I’ve come to view the zeitgeist as being much more important than personalities. (And yes, that also applies to Trump. I’m far more worried about Trumpism than I am about Trump.)

6. Penn Jillette is one of my favorite people. Reason is one of my favorite magazines. So what could be better than a 2-hour Reason magazine interview of Penn Jillette? (By Nick Gillespie.)

(Things I have in common with Jillette: Born in 1955, tall, obsessed with Bob Dylan, libertarian, atheist, annoyed with the recent right wing drift of libertarianism. Differences: Jillette is really talented.)

7. Here’s Razib Khan, who self-identifies as conservative:

8. Putin must be smiling as he contemplates our stupidity:

The U.S. is considering sanctions that would target a United Arab Emirates-based businessman and a network of companies suspected of helping export Iran’s oil, part of a broader effort to escalate diplomatic pressure on Tehran as U.S. officials push to reach a deal on Iran’s nuclear program.

Why not just send a check directly to Putin?

9. File this under “Politics is downstream of (Anglo-Saxon) culture”. Here’s the FT on the new Conservative Party:

But Tories want the fairy tale. For many, the test is no longer what you have done but whether you believe. There is no place for questioning. Approbation comes by faith alone. . . .

Doubt is such a heresy that both candidates must now deny any link between Brexit and delays at Channel ports, or its role in the labour shortages and weak pound which are exacerbating inflation.

It would be like a Republican who spent early 2016 calling Trump a fraud, suddenly become a true believer and spouting theories about a stolen election because the GOP base demanded it.

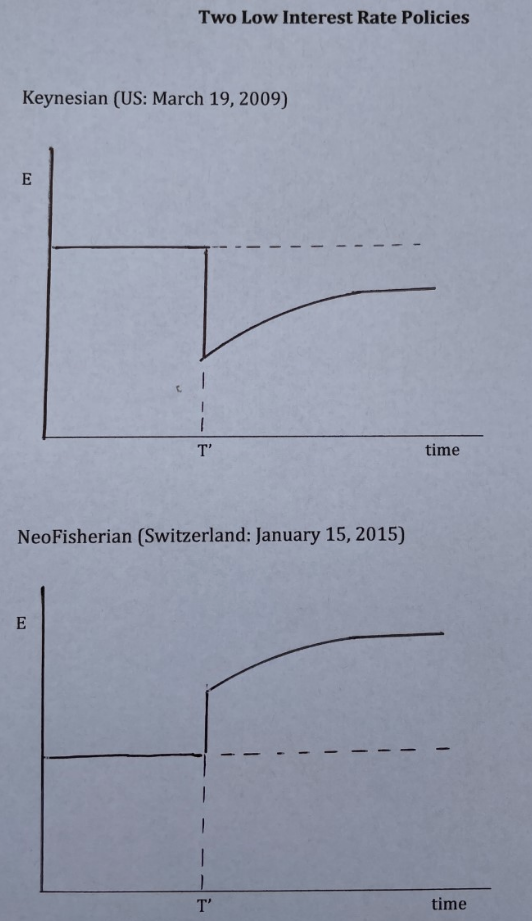

Some commenters struggled with my previous post, which looked at two types of low interest rate policies, one expansionary and one contractionary. In that post, I focused on the expected path of exchange rates.

Today, I’ll tell the same story in New Keynesian language, focusing on the role of the natural rate of interest. Consider the following two policies:

1. The Fed reduces market interest rates at a time when there is relatively little change in the natural rate of interest.

2. The Fed reduces the natural rate of interest. It also reduces market interest rates, but by less than the decline in the natural rate of interest.

These are both “low interest rate polices”, but the first is expansionary while the second is contractionary. When Keynesians speak of a low interest rate policy, they have in mind the first type. When NeoFisherians speak of a low interest rate policy, they visualize the second type.

In my previous post, I gave an example of a central bank that simultaneously appreciated their currency and generated expectations of further currency appreciation (as with Switzerland in January 2015.) The currency appreciation sharply reduced the natural rate of interest. The promise of further currency appreciation led to lower nominal interest rates. Because the natural interest rate fell by more than the market interest rate, the policy ended up being contractionary.

Keynesians often forget that central banks can move the natural interest rate by more than they move the policy rate. NeoFisherians often forget that central banks can move the market interest rate relative to the natural rate.

I try to remember both truths.

PS. The National Review just announced that the US is in recession because of two quarters of negative RGDP growth. Who’s going to tell them?

PPS. NGDP grew at a 7.85% annual rate in Q2. That’s way too fast.

Most people judge monetary policy in terms of the level of interest rates. Low rates are easy money and high rates are tight money. More sophisticated pundits suggest that you need to look at the expected path of interest rates over time. If one knew the exact path of interest rates from now to the end of time, wouldn’t that describe the path of monetary policy?

Not really.

Consider two central banks. Assume that both use exchange rates as the instrument of monetary policy. At time T’, each announces an unexpected change in the path of the (formerly stable) nominal exchange rate (not interest rate) as follows:

In the first case, the exchange rate depreciates sharply in the short run, and somewhat less so in the long run. It’s an unambiguously expansionary monetary policy. In the second case, the exchange rate appreciates sharply in the short run, and even more so in the long run. It’s an unambiguously contractionary monetary policy.

Now here’s what might surprise you. In both cases, the change in the nominal interest rate is exactly the same from T’ to the end of time. In both cases, short-term nominal interest rates fall and long run forward interest rates are unchanged. If you think of monetary policy as a path of interest rates, then the two policies are absolutely identical. (This is due to the interest parity condition, which implies that nominal interest rates reflect the expected change in the exchange rate.)

I often see people talk about how a particular monetary policy shock impacted interest rate futures. They might see a rise in the three or six-month forward fed funds rate and assume that means that markets interpreted the shock as the Fed intending to tighten monetary policy.

You cannot do that! It’s just wrong. Interest rates do not describe the stance of monetary policy, and they do not describe changes in the stance of monetary policy.

And don’t say, “The monetary policy is the same in both cases above, but there was a non-monetary shock that caused the two macro outcomes to differ.” In this case, the different outcomes is obviously due to differences in the initial change in the exchange rate, but we are assuming the central bank uses the exchange rate as the policy instrument, so one certainly cannot argue that this is a “non-monetary shock”. Indeed that argument is equivalent to making the equation of interest rates and monetary policy into a tautology. If you define monetary policy as nothing but the path of interest rates, then you will be correct in claiming that monetary policy is nothing but the path of interest rates. And you will have a completely useless model.

Suppose the Fed has been struggling with its control of inflation. Markets view Powell as being too dovish, lacking in credibility. There’s speculation that the Fed will have to raise rates by another 300 basis points to get ahead of the curve, to control inflation. Then Powell makes a forceful statement at a press conference. With anger in his voice, he insists the Fed will do whatever it takes to bring inflation down rapidly, even if it results in recession.

Suddenly, the markets begin to believe he’s serious. Expectations of recession rise sharply. As recession fears mount, the expected future natural rate of interest falls rapidly. If the expected path of the Fed’s interest rates falls less sharply than the expected natural rate, then two things happen:

1. The path of interest rates falls.

2. Monetary policy has become tighter.

Everything Powell does is monetary policy. His votes are monetary policy. His words are monetary policy. The stern tone of his voice is monetary policy—separate from the words. And these words are not monetary policy because they impact the future path of interest rates, or at least not entirely for that reason. They are monetary policy because they also move the expected path of the economy, and hence the expected path of the natural rate of interest. (Think of Powell’s FOMC vote on the interest rate target as the Keynesian part of his policy, and the stern tone of his voice as the NeoFisherian part of his policy.)

I can’t emphasize enough that all this speculation about how high the Fed will need to raise rates is utter nonsense. The path of interest rates is not monetary policy. If the Fed has a credibly effective anti-inflation policy then it will end up raising rates by much less than if it drifts into a sort of G. William Miller-style passivity.

PS. These two graphs are not mere theoretical curiosities; they are stylized representation of actual real world monetary shocks in 2009 and 2015.

PPS. The central bank of Singapore uses exchange rates as its policy instrument. As (in a sense) do countries on a fixed exchange rate regime, such as Hong Kong and Denmark.

Sunak and Truss are both struggling to establish their credentials with a party membership that still appears to be lamenting the resignation of Boris Johnson earlier this month.

A Mail on Sunday/Deltapoll survey found that 33 per cent of members thought Johnson would be the best prime minister, compared with 26 per cent for Truss and 24 for Sunak.

Johnson will step down as prime minister after a new Tory leader is announced on September 5.

His “hasta la vista” farewell to the House of Commons last week, raised hopes among his supporters that he might make a comeback at some point in the future.

How is it possible that a disgraced and eminently unqualified politician is the single most popular choice for leader of the Conservative movement? And why are they “lamenting” his ouster? Can’t they let go of the past? And how is it possible that this person could be contemplating a comeback after being ousted from office? What is wrong with the British Conservatives?

PS. According to wikipedia:

A kakistocracy (/kækɪˈstɒkrəsi/, /kækɪsˈtɒ-/) is a government run by the worst, least qualified, or most unscrupulous citizens.

Welcome to a new blog on the endlessly perplexing problem of monetary policy. You’ll quickly notice that I am not a natural blogger, yet I feel compelled by recent events to give it a shot. Read more...

My name is Scott Sumner and I have taught economics at Bentley University for the past 27 years. I earned a BA in economics at Wisconsin and a PhD at Chicago. My research has been in the field of monetary economics, particularly the role of the gold standard in the Great Depression. I had just begun research on the relationship between cultural values and neoliberal reforms, when I got pulled back into monetary economics by the current crisis.

"This man is the devil. Look at his eyes. Same as Soros. All baggy and nasty. Good people dont age like that. Its the sign of a madman. A negativity..."

"I watched Satantango on video over 3 days. I found it absolutely gripping, but one must surrender for a time one's idea of what a movie should be. Instead, you..."