Jay Powell has a bland speaking style, but if you listen carefully to the content then his press conferences can be quite interesting. I don’t have a written transcript, so the following is not precisely word for word, but pretty close:

Inflation expectations are quite central in how we think about inflation.

We need them to be anchored at a level consistent with our 2% inflation goal. . . . We need to conduct policy in a way that supports that outcome.

So he wants to set policy at a position where the public expects 2% inflation. What about level targeting?

We are also as a part of our review . . . looking at potential innovations, changes to the framework that would be more supportive of achieving inflation on a symmetric 2% basis over time. . . . That’s at the very heart of what we are doing in the review.

Translation: The Fed is edging closer to level targeting, or average inflation targeting. Later, he indicated that the policy review would last until the middle of next year. I doubt they’d change policy right before the election, so look for a late 2020 announcement.

What about real growth?

Our outlook overall is for moderate growth of around 2%, which is pretty close to trend . . . and we feel like our current stance of policy is appropriate as long as that remains the outlook.

Translation: Policy is currently set at a level expected to produce roughly 2% RGDP growth. If expected RGDP growth changed then policy would need to be adjusted.

Let’s summarize these “dots”. Policy is set at a level where the Fed expects 2% RGDP growth. Policy is set at a level where the public expects 2% inflation. Hmmm, what sort of expected NGDP growth does that imply?

Powell also indicates that the policy framework needs to change in a direction where the misses are “symmetric”, which is what happens with level targeting. That change will likely be announced later next year.

More than 10 years ago, I began blogging on the need for stable growth in NGDP, with level targeting. I argued that policy should be set at a position where the markets expected 5% NGDP growth, later changed to 4% when the Great Stagnation kicked in and the Fed said it wanted to stick with a 2% inflation target.

We do not yet have a policy regime where the Fed sets policy at a position that the market expects will result in 4% NGDP growth, with level targeting. But we are a heck of a lot closer to that regime than we were in February 2009.

Can I say we are 50% of the way there? And what about the other 50%? We need to shift from a focus on the public’s inflation expectations to a focus on the financial market’s inflation expectations. And we need to shift from a focus on the Fed’s RGDP growth outlook to the market’s RGDP outlook. And we need to add the two.

Two plus two is four. That’s not so complicated, is it?

Three more years of steady NGDP growth and America will have its first ever soft landing. In that case, I’ll declare victory and go home.

Many people (actually almost everyone) have trouble interpreting growth data. There’s a tendency to conflate the normal rate of growth in an expansion with the long run trend rate of growth in RGDP. Actually, the trend rate of growth in RGDP is measured over the entire cycle, including both expansions and recessions.

The real growth rate in the US over the past 10 years has averaged slightly above 2%. A few years ago I predicted that it would have slowed to less than 2% by now. I was wrong. Today’s data shows that growth continues right at 2% over the past 12 months.

But I was not wrong because productivity has grown faster than I expected; I was wrong because the economy continues to expand at a rate well above its underlying trend rate of growth. (Here we should cut the Fed a bit of slack, as they made the same sort of error that I made.)

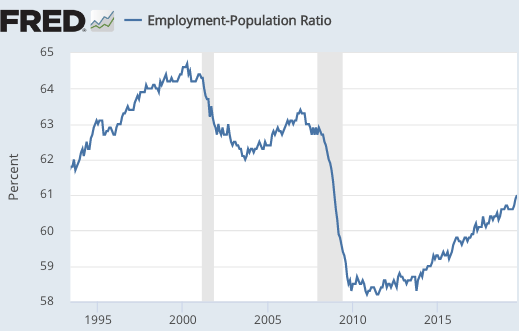

In an accounting sense, the strong 2% growth rate has been produced by slow productivity growth combined with a rising employment-population ratio:

You might think that this graph shows that the employment population ratio remains sharply depressed. Not so, adjusting for demographic changes it is near the 2000 peak. As baby boomers retire, you’d expect to see a decline in the ratio, as only about 24% of healthy people over 65 are still working (and even fewer disabled people). The ratio is modestly below peak for ages 25-54, and well above peak for 55-64 and over 65.

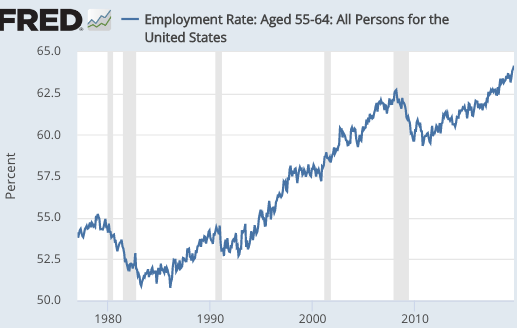

Take a look at the employment ratio for the 55-64 age group:

Notice that this ratio is now 64.2%, far above the 58% ratio at the peak of the 2000 tech boom. The over 65 ratio is also rising briskly. (Think about all those old codgers working for Uber.)

This is what I got wrong. I thought that growth would slow to 1.5% by now, because I didn’t expect so many old people like me to be working. Indeed, 5 years ago I fully expected to be retired by now—-so I didn’t even correctly forecast my own labor force participation rate at age 64! (Actually, I would be retired if my Mercatus opportunity had not come along.) Old boomers are harder working than previous generations (albeit in much softer jobs.)

Can this surge in labor force participation continue for some time? Yes, I’m duly chastened by my inaccurate forecasts of 5 years ago. But here’s what I do know, the labor force participation rate cannot go above 100%. We’ll need more immigration at some point if we want to maintain 2% RGDP growth—a lot more.

Here’s the most important point I’d like to make. The trend rate of growth is the growth rate that occurs when the age-adjusted employment-population ratio is stable. Because this ratio has recently been rising briskly, even faster than the aggregate data show due to composition effects, we are now growing at well above the economy’s long run trend rate of growth.

That’s right, the recent 2% RGDP growth derided in the media as “weak” is actually very strong, reflective of an unsustainable boom. It might last for several more years, but it’s ultimately unsustainable. The Great Stagnation continues.

PS. I rarely agree with the Germans on monetary policy, but this is an exception:

The head of Germany’s central bank has said he opposes using monetary policy to tackle climate change, setting up a potential clash with Christine Lagarde, who plans to explore the idea after she becomes European Central Bank president on Friday.

In the 1990s, this sort of Bloomberg headline would be assumed to be a spoof from The Onion:

Taxing the Rich to Fund Welfare Is the Nobel Winner’s Growth Mantra

Just because it seems whacky doesn’t mean it’s wrong. My views on the Great Recession (tight money caused it) are also widely viewed as being whacky. But in this case, the Nobel Prize winner’s views are wrong for two reasons.

Abhijit Banerjee recommends higher taxes on investment, with the money redistributed to lower income people. The argument is that the rich have a lower propensity to spend and hence redistribution to the poor will boost aggregate demand.

One obvious problem is that the Fed will engage in monetary offset, either raising interest rates or cutting them less rapidly, and hence there will be no impact on aggregate demand. This is true even if the Fed is consistently undershooting its 2% inflation target by a few tenths of a percent, due to over-reliance on Phillips curve models.

But even if the Fed does not adjust interest rates in response, the policy is likely to fail. It’s a mistake to focus only on the different marginal propensities to spend. A tax on investment will depress the propensity to investment, and this will reduce the equilibrium interest rate. So even if the Fed keeps interest rates constant, money will become effectively tighter. Indeed we’ve seen something like this over the past 12 months, albeit due to the trade war, not higher taxes on investment. And the opposite occurred during 2017-18, when lower corporate taxes boosted business investment demand and raised the equilibrium interest rate.

Banerjee is relying on a model that Paul Krugman used to call “vulgar Keynesianism”. It’s just as wrong today as it was in the late 1990s.

PS. I’m not suggesting that redistribution is a bad idea; progressive consumption taxes and low wage subsidies have a lot of merit.

Chicago’s guaranteed annual stipend level as of now is $31,000. The new funding model begins next fall and will take two years to fully adopt. Once it is in place, all students will have paid health insurance premiums and full tuition coverage, in addition to the guaranteed stipend.

What!?!?!

For all you millennials who think we boomers had it so much easier, here’s my experience at the UC during the late 1970s. A total stipend of $1000 for three years, vs. $93,000 today. No health insurance. I had to pay full tuition. I borrowed the money to pay my tuition and worked a job to pay for my food, rent, clothing, health costs, etc. (No money from my parents.) I bought almost no clothing during my three years there, my diet was basically hot dogs and bread, and I cut my own hair to save money. I eventually paid back all of my loans. So excuse me if I don’t get out in the streets and march in favor of forgiving all college debts.

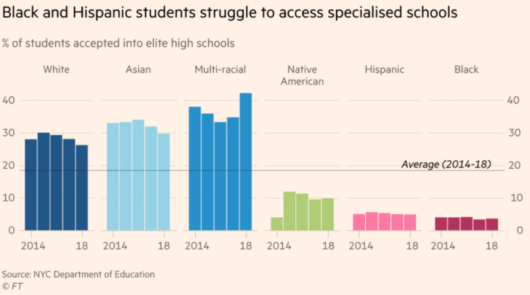

White supremacists sometime argue against interracial marriage, worrying that it will dilute the gene pool of their precious white race. But it looks like multi-racial kids might be better students than white kids:

Ivon widiahtuti’s job is, on the face of it, straightforward. As an auditor at the Food, Drug and Cosmetics Assessment Agency (lppom), an organisation in the leafy city of Bogor, Ms Widiahtuti reviews the applications of companies hoping their products will be deemed halal, meaning that their consumption or use does not break any of the strictures of Islam. . . . some applications concern products that aren’t edible. As she lists the musical instruments and sex toys that she and her team have inspected recently, she giggles at the absurdity of asking: is this vibrator halal?

All of the world’s 73 residential towers over 250 metres high were built after the year 2000. Another 64 are under construction.

This is obvious when you think about it, but still seems odd:

The result is a paradoxical relationship of the left to industry and industrial workers. Democratic votes today, Rodden shows, are geographically correlated with manufacturing employment a century ago, while Republican votes are correlated with contemporary manufacturing.

From the same issue of the NYR of Books, there’s an interesting article on a white nationalist who later rejected this hateful ideology. Unfortunately, his family did not:

The redemption story of Stormfront’s former crown prince has been a quiet one. Derek Black still sees his parents, although there are deep strains when they talk politics. He has chosen to continue his graduate studies in history rather than, as so often happens in America, to make a new career out of his extraordinary change of heart. But he did allow himself to be interviewed on radio and television several times when Saslow’s book appeared, soberly taking responsibility for the violence he had helped stimulate earlier in his life, and saying that he was not entitled to any praise merely for having ceased preaching hate. In one TV appearance, he mentioned that his parents were now frequent viewers of Fox News: “My family watches the Tucker Carlson show once and then watches it on the replay because they feel that he is making the white nationalist talking points better than they have and they’re trying to get some tips.”

The Economist recent had a thoughtful and well-written piece on poverty, which still ended up being rather disappointing:

Severely reducing or eliminating child poverty through the simplest means imaginable—unrestricted cash transfers—can seem starry-eyed until one studies the details. David Grusky of Stanford University says that the state of California, which has the highest share of poor people after accounting for taxes, transfers and cost of living, could end deep child poverty with targeted cash transfers that amount to a mere $2.8bn per year. This is “insane”, he adds. It is a quarter of the sum the state spends on prisons.

I have a different view. I think it’s “insane” to believe that after everything we’ve learned since the 1960s, throwing money at poverty will solve the problem. It is insane to believe that a state that spends $600,000 building housing units for homeless individuals will be skilled enough to cure child poverty. Having said that, if they want to release every drug crime prisoner in California and divert the money to poor children, I’m all for it.

Yet all that is less reassuring than might be hoped. Post-crisis, both governments and markets have proved surprisingly tolerant of risky borrowing. Despite household deleveraging, companies have taken on enough debt to keep private borrowing high; at 150% of gdp in America, for instance, roughly the level of 2004. In America the market for syndicated business loans has boomed, to over $1trn in 2018, and loan standards have fallen. Many loans are packaged into debt securities, much as dodgy mortgages were before the crisis. Regulators have declined to intervene—remarkably, considering how recent was the crisis.

Remarkable? I suppose it seems that way if you believe the myth that the 2008 crisis was due to “deregulation”. I happen to believe that government regulators in the US like it when banks make lots of risky loans, which is why in the early 2000s the entire financial system was set up to encourage risky lending, and still is.

In no previous century had the human population doubled. In the 20th century it came within a whisker of doubling twice. In no previous century had world gdp doubled. In the 20th century it doubled four times and then some.

I suspect that in no future century will the world’s population even double.

In the UK, authorities recently discovered 39 dead bodies in the back of a truck. To people like Trump these illegal migrants are scum, lots of “rapists and murders” or “people from shit-hole countries.” But regardless of your view of illegal immigration (and there are good arguments on both sides) it’s important to be aware that these are real people:

The UK police had given “an initial steer” in the early stages of the investigation that the victims were believed to be Chinese nationals. But on Friday, Hoa Nghiem, a Vietnamese human rights activist, said that one of the people found dead in the truck might have come from Vietnam.

She said she had been contacted by the family of Pham Thi Tra My, 26, who were trying to determine whether she was among those in the truck after receiving text messages from her saying that she “can’t breathe” and was dying, saying: “I’m sorry Mom. My path to abroad doesn’t succeed.”

David Beckworth has a recent podcast with Frances Coppola that discusses the case for a “People’s QE”. Not having read her book, I am not certain about the details of her proposal, but I gather it’s a sort of combined monetary/fiscal stimulus, where the new money is distributed to a cross section of society, not just a few big institutions.

This sort of policy might well “work”, and it might well have been better than what the Fed actually did during the Great Recession. Nonetheless, I remain skeptical of the claim that helicopter drops are superior to stimulus policies that rely exclusively on ordinary monetary policy, such as open market purchases of assets.

Coppola suggests that Japan’s experience provides support for the basic concept:

Beckworth: Frances, do we have any examples of helicopter drops, say pre-2008?

Coppola: Various governments have used forms of what we might call helicopter money, and in the book I do distinguish between different forms of it. But for example, in the 1930s, Japan actually, quite successfully used monetary financing of its government, very successfully, amid dire warnings from American pundits that it was all going to end in hyperinflation, and they were heading for the Weimar wheelbarrows, and they didn’t. They actually came out of the Depression rather more quickly than America did.

And then a bit later this:

I mean Japan, the Japanese Central Bank has been fighting deflation for a quarter of a century. I think we sometimes forget that. So been totally unable to get inflation off the floor.

I have a very different interpretation of the Japanese case. There was a combined monetary/fiscal stimulus in the early 1930s, but the key factor was probably Japan’s (wise) decision to leave the gold standard (in 1931), not the fiscal stimulus. During the Great Depression, countries tended to recover after leaving the gold standard. And Japan was one of the first to leave.

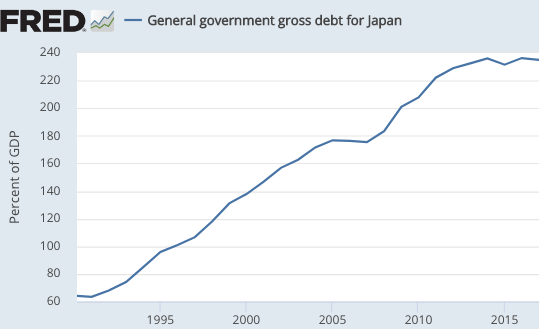

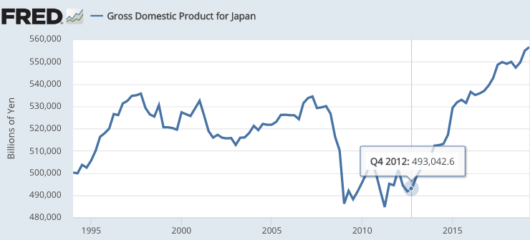

If you want to point to combined monetary/fiscal stimulus, a much better example occurred during the early 2000s, when Japan combined QE with massive budget deficits. Indeed the Japanese fiscal stimulus of 1993-2012 might have been the biggest in world history, for a country not at war. The national debt soared, until Abe introduced fiscal austerity via tax increases:

Ironically, Japanese NGDP began to finally recover at almost the same time that Japan ended its two decade long program of fiscal stimulus.

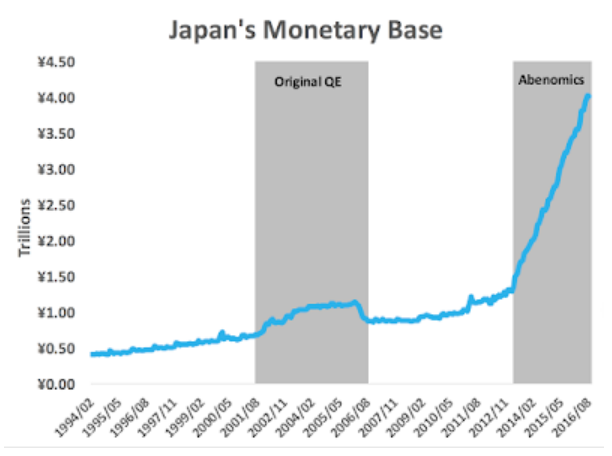

Why did NGDP rise after 2012? Because the Abe administration took office and instituted a policy of monetary stimulus. Most notably, the BOJ began a more aggressive policy of QE (graph from a David Beckworth post):

In fairness, the new BOJ policy has not been completely successful. While Japan is no longer mired in deflation, and both NGDP and employment have been rising, the inflation rate remains far below the 2% target. The new BOJ policy is far from optimal.

Some readers might wonder if my market monetarist outlook is leading to a biased analysis of the Japanese case. OK, consider what Paul Krugman had to say in 2000, when the BOJ raised interest rates:

Consider the contrast: in this country the markets expect the Fed to hold off for a while on interest rate increases even though inflation is running at more than 3 percent. Meanwhile the B.O.J. has just raised interest rates in an economy where consumer prices are actually falling, G.D.P. is lower than it was three years ago, and unemployment is at a postwar high. This says something about what kind of policy Japan can expect from its central bank in the future — and it’s not the sort of thing that would encourage people to go out and spend.

My personal guess is that in the near future, whatever optimism people are now feeling about Japan’s economy will evaporate, and the nation’s malaise will be deeper than ever — thanks in large part to Friday’s action. And while others are more sanguine, both the International Monetary Fund and Japan’s own Ministry of Finance pleaded with the Bank of Japan not to raise rates.

So why did the Bank of Japan do it? Its officials have been talking up the need for higher rates for months, yet have never been able to provide any coherent rationale. Mainly, they claim that ZIRP makes life too easy for corporations, that it lets them put off tough decisions. But there’s no evidence for this — on the contrary, despite the zero interest rate, corporate Japan has lately been experiencing an unprecedented series of high-profile bankruptcies. And anyway, since when is it the central bank’s job to strengthen the private sector’s moral fiber?

And it gets even worse. The BOJ again raised interest rates in 2006. And even worse, they withdrew much of their previous QE (see monetary base graph above.) While the popular view of Japan is roughly what Coppola suggests, i.e., that they tried and failed to stimulate their economy for decades, the truth is that until Abe took office in 2013 they made no serious attempt to push inflation above higher. Whenever inflation seemed about to rise above zero they tightened policy.

In 1998, Krugman had argued that central banks stuck at the zero bound needed to “promise to be irresponsible”. The BOJ did the exact opposite, promising to be ultra “responsible”. I use scare quotes because in this case being “responsible” is not responsible. And of course Krugman’s prediction came true. By not following his advice they pushed Japan much deeper into its zero rate trap, requiring much greater effort when a change of policy did finally occur (in 2013.) If Japan had pushed trend inflation up to 2% in the early 2000s, at a time when it would have been much easier to do so, their job today would be much easier.

In my view, the Japanese case of 1993-2012 shows that combined monetary/fiscal stimulus is no panacea. Rather we need to do monetary stimulus in the right way. Back in 2000, Krugman seemed to agree:

The government’s answer has been to prop up demand with deficit spending; over the past few years Japan has been frantically building bridges to nowhere and roads it doesn’t need.

In the short run this policy works: in the first half of 1999, powered by a burst of public works spending, the Japanese economy grew fairly rapidly. But deficit spending on such a scale cannot go on much longer. Japan’s government is already deeply in debt (about twice as deep, relative to national income, as the U.S. was before our own budget turned around). For the policy to do more than buy a little time, the recovery must become “self-sustaining”: consumers and businesses have to start spending enough to allow the government to return to fiscal responsibility without provoking a new recession.

Carping critics (like me) warned that there was no good reason to think this would happen. Sure enough, it hasn’t; as the big public works projects of early 1999 have wound down, so has the economy.

What can Japan do? . . .

Although the Bank of Japan has already reduced the short-term interest rate to zero, Western economists have pointed out that there are other things it can and should do: buy longer-term bonds, announce a positive target for inflation to encourage businesses to borrow. Indeed, textbook economics tells us that to adhere to conventional monetary rules in the face of a liquidity trap is not prudent; it is irresponsible. (Full disclosure: I personally have been the most visible and vociferous advocate of inflation targeting).

In 2000, Krugman clearly believed that monetary stimulus was more prudent than fiscal stimulus. I think he was right. But he also understood that monetary stimulus would not be effective if it were viewed as temporary. Rather the key is in shifting expectations. Abe’s BOJ has been modestly more effective than the previous version, but much more needs to be done. A good place to start would be “level targeting” of Japanese NGDP along a 3% growth path, with a “whatever it takes” approach to open market operations. Do that and you don’t need fiscal stimulus.

One final point. Some people believe it’s “fairer” to give money to the public as a whole, and not just to big institutions. But ordinary QE doesn’t give money to anyone; it sells money to big institutions at market clearing prices.

A more sophisticated version of this argument is that QE boosts asset prices. There are two problems with this view. Bond yields often rise with expansionary monetary policy, and this reduces bond prices. That was obviously true in the 1960s and 1970s, but even in the mid-2010s you can argue that when Bernanke did a more expansionary policy than the ECB’s Trichet, the long run effect was to produce stagnation in the Eurozone, and ultimately this produced lower long-term interest rates in Europe. If the ECB had been more aggressive when Bernanke was doing QE, rates in the Eurozone today might actually be higher than they currently are.

The second problem is that when QE boosts the prices of assets such as stocks, it’s largely because QE helps the economy. But a people’s QE would also help the economy, and thus boost stock prices. So “fairness” is not the right way to evaluate alternative monetary strategies.

Certainly the big issue is the need to maintain adequate growth in demand, and on that big issue Frances Coppola and I largely agree. But on the technical question of helicopters drops versus ordinary monetary policy, I still see little need to add fiscal stimulus to the equation, and on efficiency grounds I prefer a clean monetary stimulus.

If there’s a shortage of safe assets, then borrow money to create a sovereign wealth fund. But with trillion dollar budget deficits I doubt there’s a shortage of safe assets.

Welcome to a new blog on the endlessly perplexing problem of monetary policy. You’ll quickly notice that I am not a natural blogger, yet I feel compelled by recent events to give it a shot. Read more...

My name is Scott Sumner and I have taught economics at Bentley University for the past 27 years. I earned a BA in economics at Wisconsin and a PhD at Chicago. My research has been in the field of monetary economics, particularly the role of the gold standard in the Great Depression. I had just begun research on the relationship between cultural values and neoliberal reforms, when I got pulled back into monetary economics by the current crisis.

"This man is the devil. Look at his eyes. Same as Soros. All baggy and nasty. Good people dont age like that. Its the sign of a madman. A negativity..."

"I watched Satantango on video over 3 days. I found it absolutely gripping, but one must surrender for a time one's idea of what a movie should be. Instead, you..."