Some thoughts on European monetary policy

In America, it’s not easy to figure out exactly what’s going on with monetary policy. Europe is even more opaque. Indeed we still don’t know the third quarter figures for Eurozone NGDP, and won’t find them out for months. Nonetheless, I’ll take a stab at the question, as well as a few observations on the UK.

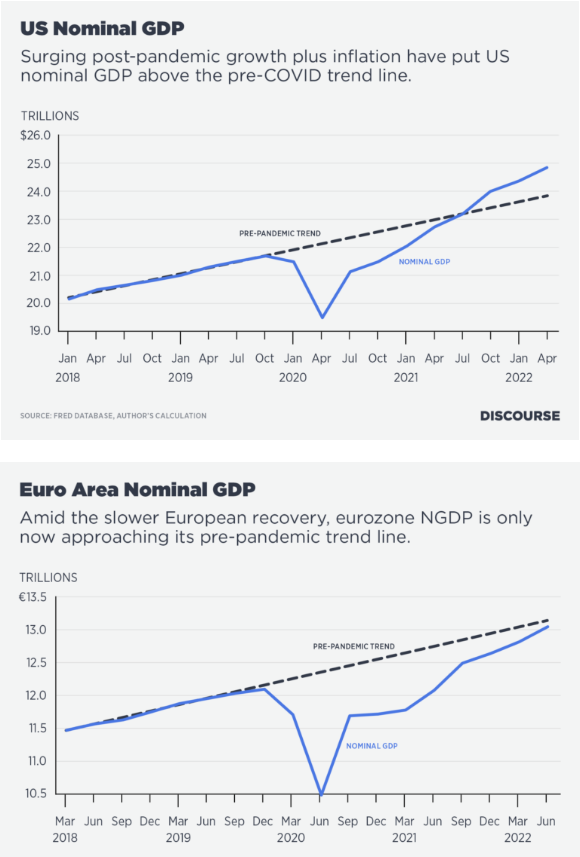

David Beckworth has an excellent Discourse article on inflation, which contains these graphs:

At first glance, it look like the US economy has overheated and the Eurozone economy is back on track. The US is quite overheated, but the Eurozone picture is a bit more complicated, for several reasons:

1. The Eurozone NGDP data is quite dated, and (AFAIK) recent NGDP growth has been quite high.

2. The pre-pandemic trend is not necessarily the optimal policy path. Suppose the Fed favored a NGDP growth target of 2% plus trend RGDP growth (a reasonable idea.) And suppose they noticed that America’s RGDP rose at an annual rate of 2.25% between 2009:Q4 and 2019:Q4. They then decided to target NGDP growth at 4.25%. Unfortunately, that policy would not succeed in the Fed’s objective of ensuring 2% long run inflation, as they’ve overestimated trend growth. The unemployment rate was 10% in late 2009, and fell to 3.5% in late 2019. They would have estimated trend growth over the expansion phase of the cycle, not the entire cycle. The actual trend RGDP growth rate in America is now about 1.5%, and lower still in Europe and Japan.

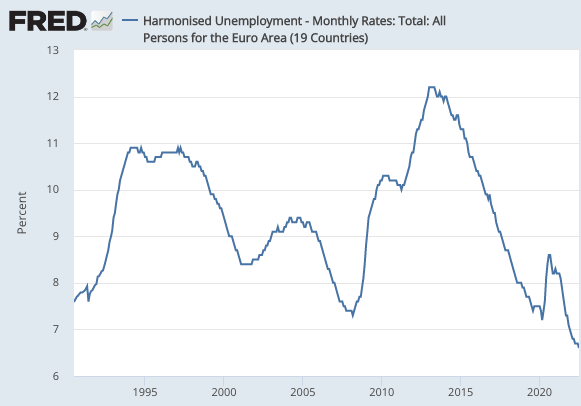

Notice that Eurozone unemployment had been falling rapidly prior to Covid, reaching a record low of 7.2% in March 2020. During the recent recovery, it’s fallen even lower:

So the Eurozone trend RGDP growth rate is also lower then its pre-Covid trend.

When people say something cannot go on forever, they are often wrong. The US trade account deficit can go on forever, or for at least as long as our multinationals earn big profits overseas. But a falling unemployment rate really cannot go on forever. So the trend rate of Eurozone NGDP growth might overstate the optimal rate by at least a little bit.

On the other hand, I see two pieces of evidence pointing the other way, against the view that the Eurozone is overheating:

1. Even if David’s graph incorporates a trend line for NGDP with slightly above average RGDP growth, the Eurozone has also been mostly undershooting its 2% inflation target. So perhaps that trend line is about right.

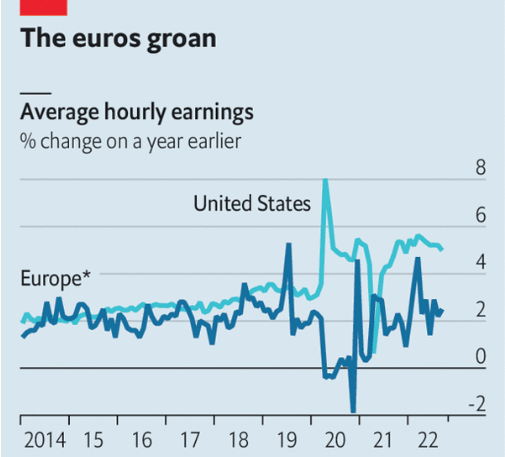

2. There’s little evidence thus far of demand-side overheating in the Eurozone wage date:

On the other, other hand, there are composition effects to consider, as well as lags. The Economist warns us that Eurozone wage inflation may be about to take off:

So far, European pay has increased little. Unlike in America, six in ten workers have collective-bargaining agreements, which tend to run for a year or more—meaning it takes time for economic conditions to influence their pay. Trade-union negotiators have limited demands, aware that a wage-price spiral would come back to haunt them. But negotiators’ patience is beginning to wear thin. Germany’s public-sector unions will enter forthcoming negotiations seeking a raise of 10.5%.

The problem for bosses is that the labour market remains exceptionally tight. The share of firms reporting that staff shortages are limiting their production is near record highs in both the manufacturing and service sectors. One reason is the enormous backlog of orders from the pandemic. Manufacturing firms have on average more than five months of work on their order books, according to a recent survey, up from four before covid struck. Add to that the cohort of workers retiring each year in ageing countries such as Italy and Germany, and a recipe is in place for a tight labour market throughout 2023.

All of this means the peak in inflation is probably some way off.

So I remain agnostic on the wage question. I’m quite willing to accept the view of Eurozone doves that the inflation problem has been almost entirely supply-side up through mid-2022. I’m less sure of the situation now and going forward, and indeed am puzzled as to why the Economist predicts tight Eurozone labor markets in late 2023. I thought all the experts were telling us that a Eurozone recession was inevitable in 2023? The situation remains confusing, at least to me.

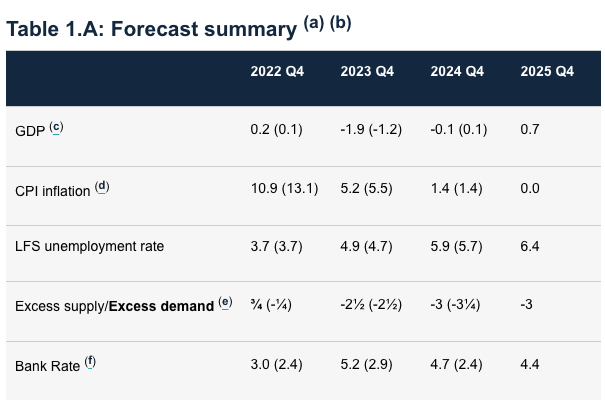

The situation in the UK is equally perplexing. Here’s a table from the BoE:

By adding GDP growth and CPI inflation, we get a very crude estimate of expected NGDP growth, which slows from 11.1% in 2022 to 0.7% in 2025. The average growth rate over that 4-year period (about 4.1%) is relatively high compared to the roughly 3% to 3.5% (post-Brexit) trend NGDP growth required in the long run for the BoE to hit its 2% inflation target. On the other hand, much of the fast growth in 2022 is a recovery from the Covid slump.

The British case raises a number of tricky questions. Is NGDP level targeting even appropriate? If so, where should we draw the trend line? If you look at RGDP growth and unemployment, 2023-24 looks like a recession. So why are forward markets forecasting a Bank Rate of 4.7% in late 2024? I’m genuinely puzzled.

I suspect that over the next few years I’ll revise some of my assumptions about how the macroeconomy works. One casualty might be Okun’s Law, which has performed very poorly in the US during 2022. Another might be my assumption about secular trends in interest rates, TIPS markets, and the Phillips Curve. Right now, US forward markets are forecasting high interest rates in 2023 and 2024. They are also forecasting PCE inflation falling back close to 2%. Larry Summers says that that sort of fall in inflation cannot happen without a recession. His claim seems plausible, but then why are fed futures so high in 2024? Wouldn’t interest rates fall sharply in a recession? And if the answer is that markets don’t trust the Fed to bring inflation down, then why don’t the TIPS spreads reflect this?

Over the next few years, at least one of our major assumptions about how the macroeconomy works is likely to need revision. A few years back, Tyler Cowen spoke of a Great Stagnation. I wonder if the world isn’t about to enter an even greater stagnation. Very low RGDP growth, and yet a surprisingly low unemployment rate. We will see.

Tags:

4. November 2022 at 10:46

Fascinating post.

I guess the economic disaster that the “New Right” types (e.g. as defined or described by TC) are predicting for Germany and Europe this winter is not going to happen, then?

4. November 2022 at 11:35

“Over the next few years, at least one of our major assumptions about how the macroeconomy works is likely to need revision.”

We don’t need any more years to know the ‘mainstream’, i.e. leftist, economics profession is more than just completely useless to humanity, it is positively destructive. It is an apologia for communist two pronged attack of monetarist defenders of ‘central banking is good’ and Keynesian defenders of ‘government spending is good’.

Fee markets my derriere.

It’s the same endless pattern. One generation or wave of ‘macro’ economists posture themselves as ‘ok this time we got it’, pointing out the flaws in prior generation or wave of ‘macro’ economist’s reasoning, as BILLIONS of people are harmed worldwide as lab rats, then oopsy we need to adjust the crude ‘models’ of complex social human beings, and then the ‘old’ models are contradictorily both retained and negated (‘sublimated’) and ‘new’ models synthesized, but same inconsistent (by design) logic is extending over and over.

This time we got it.

Then oops.

No no, now this time we got it.

Then oops.

The whole time some human beings impose power and intimidation on the rest of humanity who are harmed for no good reason. Power and money are not good reasons, and any attempt to push for that with ‘hey that’s just the way things are’ is just ITSELF a pretext attempt to INTRODUCE and justify power in the world.

A “seeing” in the world what is all along a desire to introduce from the self. The Iron Law of Woke Projection never misses.

After more than 100 years of symbol manipulations based on arbitrary rulesets to justify socialist power, having nothing to do with the actual thoughts beliefs or behaviors of those targeted and smeared as too stupid to not live under communist money, there has not been a single discovery of any model CONSTANTS that applies to any human being let alone billions of human beings.

Billions of dollars, thousands of PhDs, a hundred years, and they got bupkus. It is nothing but a con job ’employment’ excuse.

In the hard sciences, which ‘mainstream’ economics arrogantly tries to steal from and emulate, there are MANY constants discovered and established through repeat experiment. Go to the back of any first year physics textbook and you’ll see a ton of them.

But for ‘mainstream’ economics? ZERO. NONE. NADA. Not a single constant.

Why do the morons keep using the same logic? It’s because they’re wedded to the conspiracy theory that this is the only way.

Einstein said the definition of insanity is doing the same thing over and over and expecting a different result. By that definition, mainstream economics is insane. Contrary to the claims from within mainstream economics that all sorts of ‘new discoveries’ are being made, it’s all just the same system LOGIC directing the dialectic extensions, with changing definitions, changing symbols, and changing arbitrary rulesets of those symbols to make it look like it’s ‘new’.

I find that label of ‘insane’ is not likely to resonate with the victims of insanity, so I prefer the also accurate label of ‘conspiracy nuts’. The conspiracy theory plaguing the ‘mainstream’ economics profession is that the PRIMARY driver of all humanity is POWER, and so the conspiracy is that the ‘only’ path for anyone going forward is to accept that conspiracy, live the conspiracy, fund the conspiracy, and then propagandize about the ‘mechanism’ of the conspiracy. And if you dare challenge it, the conspiracy nut logic requires projecting that onto anyone who challenges the core logic.

It can’t be forgotten: The ‘macro-economy’ doesn’t have any internal ‘workings’, everything we see in the ‘macro’ is fully determined by the actions of individuals taken together collectively. Every ‘movement’ in the current observed ‘macro’ economy is fully determined by the prior actions of individuals taken together. The aggregate outcomes don’t themselves determine anything, it is itself fully determined.

Proof is that past ‘models’ have by the site owner’s admission been exposed as flawed such that ‘major assumptions’ need to change.

Too late. Damage done.

4. November 2022 at 11:36

Anon, I wouldn’t expect the natural gas shortage to cause a disaster. As for the business cycle, that’s well beyond my ability to predict.

4. November 2022 at 11:54

“The actual trend RGDP growth rate in America is now about 1.5%”

Can you please tell me exactly how you came up with 1.5%?

4. November 2022 at 13:24

Post #2

Another dark cabal conspiracy exposed, this time in Finland (but we know it’s worldwide):

https://trendingpolitics.com/finland-exposes-massive-covid-reporting-scandal-nearly-40-of-covid-deaths-were-fraudulent-knab/

Before this was exposed, the vaccine cheerleading conspiracy nuts projected and labelled you a conspiracy theorist for merely questioning the ‘official’ statistics.

And another dark cabal conspiracy exposed which I have yet to see a blog post or comment about (I’m just imagining if it was the other way around, if the timeline had the FBI and DHS telling Twitter and Facebook to censor a ‘Trump Jr laptop from hell’ that proved Trump committed treason, the blog owner and the entire liberal media would be calling for Trump to be put into the electric chair, but because this all favored the Democrat Party, we’re supposed to just pretend it never happened, and call ‘opponents’ of the communists ‘conspiracy theorists’ while ignoring the treason of Biden, can you say PERSONALITY CULT?)

https://theintercept.com/2022/10/31/social-media-disinformation-dhs/

The government censoring SOBs use the terms ‘mis-‘ ‘dis-‘ and ‘mal-information’ as their excuse for their own political power. Site owner often uses the term ‘conspiracy nut’. Same logic. It’s just a label designed to cover up uncomfortable truth of corruption from within the self.

CISA exposed in court filings as deeming YOUR THOUGHTS as THEIR ‘cognitive infrastructure’ to control and direct. Think about that for a moment. For any government agency to assert itself as effectively owners of your mind, as their property, is something that should concern every American regardless of race, religion, class or political affiliation.

The DHS was even exposed going to the census bureau to find the PII of people to then forward to social media companies with a LIST OF NAMES demanding that they target and censor them for ‘wrongthink’. Everything from election integrity, to covid, to vaccinations, to Joe Biden, to Hunter Laptop, any talk that is not in lock step with the ‘approved’ leftist narrative, were targeted BY THE GOVERNMENT for censorship, using big tech as their ‘plausible deniability’ proxy mechanism.

THIS IS A PROVEN FACT FROM THE COURTS.

IMAGINE IF THE DHS AND FBI DID THIS TO HELP TRUMP INSTEAD. IMAGINE TRUMP KNEW JUST LIKE BIDEN KNOWS. IMAGINE THE MEDIA’S REACTION, IMAGINE THE SITE OWNER’S REACTION.

Now think what your reactions are NOW, now that you KNOW they did this to help Biden win 2020.

Is that the country you want to live in? Imagine ‘right wingers’ implementing that power instead. Those Democrats who do know this and many other things are switching registration to Republic en masse.

Turns out the loudest accusers of ‘conspiracy theorist’ were themselves the conspiracy theory pushers all along. The conspiracy theories of communist infiltration of our government and election systems.

Reminds me of the Pink Floyd song Echoes:

“Strangers passing in the street”

“By chance two passing glances meet”

“And I am you and what I see is me”

PS Bolsonaro still hasn’t conceded. Coincidence? 😉

4. November 2022 at 13:41

kt, It’s an estimate. First you look at growth over a long period, comparing years of similar unemployment rate to avoid business cycle effects. Over the past 22 years, RGDP growth has averaged 1.9%. So why don’t I use that figure?

Labor force growth has slowed dramatically over that period, due to boomers retiring and much lower rates of immigration. That’s likely to knock about 0.5% to 1.0% off the trend growth rate.

Do I have evidence for that claim? Well, RGDP growth has averaged 1.65% over the past 15 years, from the pre-Great Recession peak of 2007:Q3. And labor force growth has slowed even over that 15 years, so the current trend rate is probably below 1.65%.

But yes, it’s an estimate, not a precise figure.

4. November 2022 at 13:53

Scott,

“Low RGDP growth and low unemployment rates”. I don’t think it is shocking. Low RDGP growth is true, but from a high base. US adds like $2-3k real dollars in per-capita growth every year now, which is probably enough money to supply a structurally low unemployment rate.

I feel like the “stagnation” that is described in Western Countries is much of an exaggeration. Most of those countries are adding far more than developing places but people get fooled by the rate.

4. November 2022 at 13:57

Anon, Yes, that’s a reasonable view. I was discussing stagnation in terms of the metrics used by many people, such as the RGDP growth rate.

4. November 2022 at 15:28

Could the futures markets be reflecting a sort of average of two uncertain but wildly divergent outcomes? Outcome 1 being a recession with low inflation and lower interest rates and outcome 2 would be persistent high inflation and much higher interest rates. And outcome 1 and 2 have approximately equal likelihood so the consensus is the average of the two.

4. November 2022 at 16:15

why should any information value be given to what tips project? a small corner of the bond market half owned by the fed, who have obvious motivations to manipulate its signal.

4. November 2022 at 19:02

Democrat apologist liars will call this a lie because they lie about when the truth is not helpful to the Democrat Party:

https://www.dropbox.com/s/65oqpj6elugudb7/HJC%20STAFF%20FBI%20REPORT.pdf

Babylon Bee, censored by Twitter which we now know is an agency of the state, nails it:

https://babylonbee.com/news/democrats-worried-republicans-may-take-lead-beyond-margin-of-cheating

4. November 2022 at 20:44

No honest person can (hence incoming red wave):

https://nypost.com/2022/11/03/seriously-can-anyone-name-a-well-run-democratic-city/

Crazy happenings in China (I wonder if incriminating evidence needing to be destroyed prompted this…interesting timing isn’t it):

https://truthsocial.com/@shadygrooove/posts/109288569200002528

These are the same people suing Clean Elections USA to stop them from observing ballot drop boxes. Now they want to prevent a county from hand-counting ballots.

Do tell, why would either of these things be something they would want to pursue?

We know. We all know:

https://truthsocial.com/@CognitiveCarbon/posts/109287876303152544

5. November 2022 at 01:14

What is the point of talking about clean elections USA on a post about European Monetary policy? I don’t get it.

Maybe limiting one to two messages should also be accompanied with relevancy. It’s one thing to point out Sumner’s philosophical inconsistency and political bias — and he’s incredibly biased — but his crazy politics and ranting about cults and trump supporters has nothing to do with this particular post.

5. November 2022 at 05:09

The EU guaranteed more bank holding company debt, and they hold more savings in their banks. That reversed the velocity of circulation.

5. November 2022 at 05:50

Ricardo in answer to your comment directed at what I commented:

The answer is simple. The network controlling EU money is the same network that funds NGOs and ‘philanthropic’ organizations to weaken election integrity in America and most countries throughout the world.

The world is more connected than you appear to appreciate. What you believe are two ‘separate’ things are in fact connected.

What process did you believe was causing the expenditure of millions and millions of dollars over years and years, funding the MANY phony lawsuits (lawfare) attacking election integrity? Did you believe it was all ‘organic’ from other voters? Where is all that money really coming from? Why go through all the trouble of…preventing hand counting?

I follow the money trails. Where you see a disconnect, others see patterns.

It has EVERYTHING to do with why there is ‘suddenly’ high inflation in America and the EU. There is a WAR going on just underneath the ‘surface’ of what you only see as haphazard random ‘nothing to with each other’ observations that ‘just happen ok?’.

The same reason the EU population is being attacked with high inflation to weaken the people’s ability to rise up and fight back against those causing it, is the same reason the US population is being attacked with lawfare to weaken the integrity of elections.

Feel free to skip over what you are tacitly seeking to have censored.

5. November 2022 at 07:06

Great, clear post. Thank you!

5. November 2022 at 09:45

“US forward markets are forecasting high interest rates in 2023 and 2024. They are also forecasting PCE inflation falling back close to 2%….if the answer is that markets don’t trust the Fed to bring inflation down, then why don’t the TIPS spreads reflect this?”

For the last several months, TIPS breakevens have been quite stable, fluctuating around 2.50% for 5 yr and 2.25% beyond that. Yet, nominal rates have continued to climb, reflecting a rise in real rates. So, markets seem to expect the Fed to bring inflation down. That would leave non-monetary factors to explain the rise in real rates. I’m not sure whether those would be growth expectations, govt debt/deficit, or something else. Although inflation has been grabbing the headlines, the real story — pun intended — seems to be real.

5. November 2022 at 12:27

Interesting stuff!

5. November 2022 at 12:33

Yes, it’s all a bit of a puzzle. One thing you left out was the 10-2 year bond yield inversion, which is the biggest it’s been for 40 years, during which time it has reliably presaged a recession. Somehow, markets seem to be predicting a very soft landing, notwithstanding some relatively dramatic rises in nominal policy interest rates that are expected to peak sometime late in 2023. Perhaps this view is helped along by an expectation that more of the problem is supply-related than perhaps you and Summers have claimed.

As for real interest rates rising while real GDP growth remains slow, I’m not sure how that can be squared with US equities (S&P500), which although 20% down from their highs of a year ago, are still more than 10% above pre-pandemic highs. To be fair, the Russell 2000 index is closer to its February 2020 level. But overall, it seems to me that either long bond yields are too high or equities are too high, or both.

5. November 2022 at 14:05

The interest rate forecasts for the US sure are strange.

Here’s my attempt at a scenario where they make sense: a neutral monetary policy would mean t-bill rates of around 5.5%. Inflation drops to about 3% in mid 2023, with 4% NGDP growth. The Fed declares victory, and starts slowly reducing interest rates. Inflation creeps back up above 3%, and NGDP growth creeps up to 5%. That makes stable 4% t-bill rates somewhat plausible.

Doesn’t the Taylor Rule suggest that something like that is plausible? Markets might be taking something resembling the Taylor Rule seriously.

I disagree with those markets. I’m betting on interest rates below 4% in 2025 (via buying Eurodollar futures).

5. November 2022 at 19:24

Scott, why are you comparing BoE forecasts to market forecasts and perplexed? Isn’t the answer that the BoE forecasts are wrong?

5. November 2022 at 19:30

Wow, are you hinting here that you might reconsider some of your most essential views, including NGDP level targeting???

I am glad that this brazen commentator from Greece, Portugal, Brazil, wherever, who stressed at every inopportune moment how rich he supposedly was, is no longer around. He would surely jump on this and do a happy dance over the next three pages.

6. November 2022 at 04:04

https://www.clevelandfed.org/indicators-and-data/inflation-nowcasting

October 2022 8.09% y-o-y CPI

2022:Q4 7.20% CPI

Stagflation, business stagnation accompanied by inflation.

6. November 2022 at 05:24

Agree with Christian.

I read Scott’s comment about 5 times and was obviously confused. I thought NGDP targeting was Scott’s anchor re monetary policy.

Nothing wrong with changing one’s views per se. But I am continually coming to the conclusion we know very little about so many things, economics obviously included.

I am sure someone has written about the following topic——-“how often are economists forecasts re:policies correct ex-ante?”

I have no idea. But my guess is the answer is no better than random.

But I would not be surprised if they are worse than random——which if true would be quite an interesting phenomenon.

6. November 2022 at 05:46

George said:

“It’s the same endless pattern. One generation or wave of ‘macro’ economists posture themselves as ‘ok this time we got it’, pointing out the flaws in prior generation or wave of ‘macro’ economist’s reasoning, as BILLIONS of people are harmed worldwide as lab rats, then oopsy we need to adjust the crude ‘models’ of complex social human beings, and then the ‘old’ models are contradictorily both retained and negated (‘sublimated’) and ‘new’ models synthesized, but same inconsistent (by design) logic is extending over and over.”

— Convincing a monetary economist that his lifes work is a big fat joke, that the entire discipline is pseudoscience at best, and ponzi scheme gangsterism at worse, is like telling a 17th century astrologist that they cannot predict terrestrial events and discern human affairs by studying celestial objects.

In the 22nd century, people will laugh at the so-called “monetary economists” but until that time you can expect to be called a heretic, a nonbeliever, and maybe even a “cultist” for disagreeing with what most people already recognize (even on the left) as a ponzi-scheme.

But naturally, if you devote your whole life to something, then you will erect certain barriers to entry, certain defense mechanisms to protect your fragile ego and your lifes work, which makes it impossible for people Sumner’s age to see the light. And it’s not just him; that’s true in general.

It’s why most innovations, and academic breakthroughs come from youth, not from the old who have their wheels perpetually stuck in the mud.

The best of course action is to adopt decentralized currency; that is the only way to free ourselves from the Federal Reserve with a massive world war.

6. November 2022 at 05:48

**Without

6. November 2022 at 08:12

Dale, Yes, that’s possible. There might be other markets (options?) that have something to say on that issue.

Rajat, You said:

“Could the futures markets be reflecting a sort of average of two uncertain but wildly divergent outcomes?”

What do you mean by “the problem”? There’s not much doubt that inflation is now mostly demand side, as the NGDP overshoot since 2019 is almost identical to the PCE inflation overshoot. But if “the problem” refers to stagnation, then I think that is quite possible, as does Summers.

Peter, Yes, that’s possible but it would mean no recession in 2023. And a recent Bloomberg headline said a recession in 2023 is 100% certain. (LOL)

Sina, That’s possible, but don’t many private forecasters also expect a recession?

Christian, LOL, I see you haven’t lost your ability to imagine things.

6. November 2022 at 12:48

Sara:

“But naturally, if you devote your whole life to something, then you will erect certain barriers to entry, certain defense mechanisms to protect your fragile ego and your life’s work, which makes it impossible for people Sumner’s age to see the light. And it’s not just him; that’s true in general.”

I could only imagine what it would feel like to experience acknowledging truths that would negate not only decades of ‘work’ but of investment in a faulty method of perceiving reality. Perhaps I too would behave, think, and react in a similar way. Self-preservation like.

“The best of course action is to adopt decentralized currency; that is the only way to free ourselves from the Federal Reserve with[out] a massive world war.”

The true definition of ‘decentralized’ includes decision making at the individual level. When individuals are free to choose, we know that throughout history it is precious metals that have always been the commodity of choice. Durable, homogenous, high value per unit weight, and safe.

The best path, IMHO, to abolishing the communist crime syndicate called ‘central banking’, is for Gold/Silver to be legal tender, and if people want to accept ‘notes’ from banks for use in exchange, then as all contracts the reality of those notes must be explicit, so if people want to accept a risky unbacked paper note, they can do so, but they would know it’s not backed by gold or silver. Transparency in banking would prevent what historically opaque “don’t worry everyone, the Fed will ensure banks behave” encouraged from banks to lend what they don’t have but ‘promise’ to pay.

Gold would destroy the Fed. And that is PRECISELY why there is a manufactured narrative from the same crime syndicate being exposed worldwide today who attack, smear and slander Gold. It’s why “monetarists” have never ‘debunked’ gold as money. They have tried, but it all boils down to smears, slanders and fear mongering, not economic science.

6. November 2022 at 15:37

Hi Scott, question on a different topic:

I just noticed an NYT chart that showed cumulative employment since 1/2020. According to the chart we equaled pre-pandemic employment in June ’22. Presumably, had life preceded normally, we’d be a few percent or so ahead of that now. Is the idea of the number of people working returning to “normal” playing a roll in the Fed’s view of interest rates and inflation?

6. November 2022 at 17:31

Scott, in responding to me, I think you took a quote from Dale. But yes, I was trying to think of a way of reconciling all the market signals. If stagnation is expected to get worse, should real rates be rising? I think we’ve seen falling real rates and slower growth moving hand in hand for so long that I presumed that they should continue to do so. But maybe that’s wrong. If government spending is expected to remain high or keep rising, then I suppose the private sector needs to be encouraged to hold its own spending back, and the only way that can happen is with higher real rates. In other words, no more global savings glut?

6. November 2022 at 18:59

Jim, That would be extremely foolish of the Fed, as life certainly did not proceed normally after 2019. For instance, we almost completely stopped accepting immigrants. But yes, that might have been one factor in their poor decision making.

Sorry Rajat, This was the quote I was responding to:

“Perhaps this view is helped along by an expectation that more of the problem is supply-related than perhaps you and Summers have claimed.”

Yes, budget deficits are one factor in rising rates, but it’s unlikely they can fully explain the high rates expected in 2023 and 2024.

7. November 2022 at 05:20

Scott, private forecasts also aren’t market forecasts. This is something I learned from you.

7. November 2022 at 14:40

A few observations.

1. All the policy rules (Taylor Rule, AIT, etc) are fictional. Central Bank policy can be summarized by a) if unemployment goes up, tap on the gas, or b) if inflation goes up, tap on the brake.

2. Central bank policy always lags the actual economy.

3. If you have had a disruption to the economy (like Covid), you can’t and shouldn’t try to get back to your original NGDP trend line. You’ll get inflation if you try. Instead you need to shift the trend line down.

4. If, even worse, you let NGDP go over the trend line, it proves my theory that the Fed is almost always incompetent and that the FOMC should be replaced with an iPhone app. (We’ll have to wait to see how incompetent the BoE is.)

5. If you let NGDP go over the trend line when the LFPR has significantly dropped, there is no adjective in the English language to adequately describe your stupidity.

6, There is a significant element of hysteresis in inflation, it’s probably quite a lot different than in the 80’s, and no one (including Summers) really understands it.

7. November 2022 at 17:46

@dtoh:

I’m sure Scott will have a good critique of your post but this actually sounds fairly close to the truth to me. I’m nowhere near an authority on this though.

8. November 2022 at 04:26

Scott,

You should add a word count limit to your two post rule.

8. November 2022 at 08:56

Sina, As I said, I’m agnostic about the Eurozone/UK situation. It’s possible that recession isn’t inevitable, despite the media telling us every day that it is inevitable. Who knows?

dtoh, NGDP per capita level targeting is a good compromise.

8. November 2022 at 09:08

Scott,

Totally agree or maybe NGDPLT per capita very occasionally adjusted for long term changes in LFPR, tax rates and other major structural changes.

And BTW – I don’t think there is much excuse for lags in implementing policy. Satellites photos of Walmart and factory parking lots would probably probably be just as accurate as an NGDP futures market.

8. November 2022 at 23:51

Scott,

two points/questions:

1. how can the EURO NGDP be at trend growth, if average CPI inflation is around 10 percent and there has been no recession so fard? I doubt the GDP deflator is 6 points below the CPI.

2. even if it were correct that EURO NGDP is at trend growth, the fact that the US is above suggests a more restrictive Fed and thus an increasing interest rate differential – with potentially destabilizing consequences on the FX an all that comes with it – how to deal with that, or do you suggest to ignore FX spillovers?

P.S. hope you enjoyed your stay in Austria

9. November 2022 at 09:34

dtoh, Not sure what you mean by “structural changes”

Vienna, First of all, I assume the Eurozone GDP deflator is well below the CPI, as imported energy is a huge issue. Second, trend RGDP has probably slowed substantially under Covid.

9. November 2022 at 09:42

@Scott

In this context, “structual changes” would be things that impact the RGDP growth trend…. e.g. higher immigration, reduced capital gains tax rates, aging population that causes a change in the LFPR, etc.

10. November 2022 at 00:11

Scott,

yes, the GDP deflator seems to be around 4-5% (annualizing ytd. quarterly changes).

Agree with you that structural growth should be below pre-pandemic levels as sanctioning trade with the biggest energy/commodity supplier certainly reduces overall growth (apart from Covid).

This, however, could mean that Beckworth is wrong, as the trend line would have to be corrected downward substantially with monetary conditions still loose…