On Saturday, the F-22 scored its first-ever victory against an airborne adversary when it shot down…a balloon.

There may not be a better metaphor for the costly grandiosity of the American military than the use of a multi-million-dollar fighter jet to dispatch an unarmed, unmaneuverable opponent. But the fact that the F-22 had never won a dogfight before its decisive victory over what may or may not have been a Chinese spy balloon is a nice illustration of why the United States has the world’s most expensive military by a massive margin.

In short, it’s because the Pentagon buys lots of expensive toys that have no use.

The balloon in question is absolutely massive, with “an undercarriage roughly the size of three buses,” as The New York Times put it. This would be an absolutely bonkers way to spy on the United States—especially since the images it picks up are reportedly no better than those it can obtain through satellites. One defense official said, as summarizedThe Washington Post, that the images a balloon like this could obtain “wouldn’t offer much in the way of surveillance that China couldn’t collect through spy satellites.”

Anyone on the ground could see the balloon in the sky without any sort of specialized equipment. To believe this was meant as a secret spycraft, you’d have to believe the Chinese authorities are just absolute morons, which (whatever else they might be) clearly isn’t true.

The US labor market burned red-hot in January as hiring unexpectedly surged and unemployment fell to a 53-year low, defying recession forecasts and adding pressure on the Federal Reserve to keep raising interest rates.

Nonfarm payrolls increased 517,000 last month after an upwardly revised 260,000 gain in December, a Labor Department report showed Friday. The unemployment rate dropped to 3.4%, the lowest since May 1969 and average hourly earnings grew at steady clip.

Recall the metaphor “shooting ducks in a barrel”? It’s the phrase I think of when I see thoughtful progressives criticize the excesses of wokism. Their critiques are so obviously correct it’s hard to believe that anyone disagrees. So do the ducks ever shoot back? Are there any thoughtful rebuttals?

And yet we are told that the woke have taken over almost all of our key institutions.

[I suppose something analogous has happened on the right. Almost all thoughtful conservatives have written highly persuasive critiques of Trump, and yet Trumpism has taken over the GOP.]

These progressive critiques of woke excesses almost write themselves. I mean, how hard is it for an intelligent intellectual to write an op-ed full of stuff like this (From Nicholas Kristof):

As for my friends who are homeless, what they yearn for isn’t to be called houseless; they want housing.

The basic stance of the social justice set, for a long time now, has been that they are 100% exempt from ordinary politics. BlackLivesMatter proponents have spent a year and a half acting as though their demand for justice is so transcendently, obviously correct that they don’t have to care about politics. When someone like David Shor gently says that they in fact do have to care about politics, and points out that they’ve accomplished nothing, they attack him rather than do the work of making their positions popular. Well, sooner or later, guys, you have to actually give a shit about what people who aren’t a part of your movement think. Sorry. That’s life. The universe is indifferent to your demand for justice, and will remain so until you bother to try to change minds. Nobody gives you what you want. That’s not how it works. Do politics. Think and speak strategically. Be disciplined. Work harder. And for fuck’s sake, give me a simple term to use to address you. Please? Because right now it sure looks like you don’t want to be named because you don’t want to be criticized.

Language is arbitrary and always changing, so personally I find “getting mad at language change” to be one of the lowest forms of reactionary politics. At the same time, it’s worth just applying a little bit of common sense to the question of who is and isn’t included by saying “practicum” instead of “field.” Highly educated people and white-collar workers who spend a lot of time bored at the office staring at computer screens and reading articles are well positioned to have large and flexible vocabularies. We are used to learning new words and learning how to use them.

I am quite fluent in why we don’t characterize non-white people as “minorities” anymore, and even why affirmatively characterizing them as “people of color” is in favor rather than saying “non-white,” which tends to center whiteness. I know what it means to “center” something. I know that URM stands for under-represented minorities, and that we tend not to spell it out because “minorities” is out of favor. I also know what URM means (not Asians) and how URM is distinguished from BIPOC. I don’t talk about third-world countries.

I know these things in large part for the same reason I know how to tie a bow tie. And while everyone knows about Skull & Bones, I also know about Scroll & Key and can tell you which school has eating clubs. But while there may be merit to cultivating a set of esoteric practices for the sake of maintaining a national (or these days, increasingly, global) elite class that can recognize its fellow members, that’s like saying (à la John Rawls) that there may be reasons for even egalitarians to support a certain amount of inequality.

These elite institutions and codes of manners are not egalitarian, not just because manners are insufficient but because their purpose is to be inegalitarian. Changing “field” into “practicum” doesn’t include more people — it’s a new means of excluding people whose information is out of date.

Relative to these thoughtful progressives, I am skeptical of many left-of-center public policies. But even if became converted to progressivism, my view of wokism would not change at all. In fact, I might become even more critical, as they would be hurting my cause.

Some old school progressives seem to believe that wokism is a sort of secret plot by the neoliberal elite to divert attention away from economic inequality. That’s probably nonsense, but in some respects wokism does serve the material interest of the neoliberal elite, by making voters turn away from left wing political parties (not just in the US, but throughout the world.)

If you’re looking around online for criticism of Musk, you’ll find more in terms of pure volume that engages in culture war – going after him for the dumbshit rightwing memes he shares – than that which criticizes the position of billionaires in our economy, their disproportionate influence on our political process, and the connection between their riches and the poverty of others. This is a pretty effective gloss on the poverty of progressive priorities right now; even with one of the richest men in the world, people can’t look past culture war and see the structural problems underneath.

Montaigne pointed out that the barbarians that conquered Greece had a disdain for intellectuals. Surprisingly, they decided not to burn Greece’s libraries. One of their leaders pointed out that Greece was their enemy and that their intellectual pursuits would keep the Greeks from pursuing the sort of “vigorous and soldierly” lifestyle that would make them formidable military foes. I don’t know if Trump is funding the woke movement, but if he’s not then he’s even dumber than I thought.

PS. And it isn’t just progressives that get this point:

PPS. The Economist also sees how the scolds on the left are their own worst enemy. Remember when being left wing was cool?

The left once drew energy from scorning authority and bourgeois convention. But as it becomes America’s enforcer of social norms, it increasingly treats the arts as a tool for instruction. As a result it is surrendering what puts the arts in society’s vanguard, the capacity to question and shock.

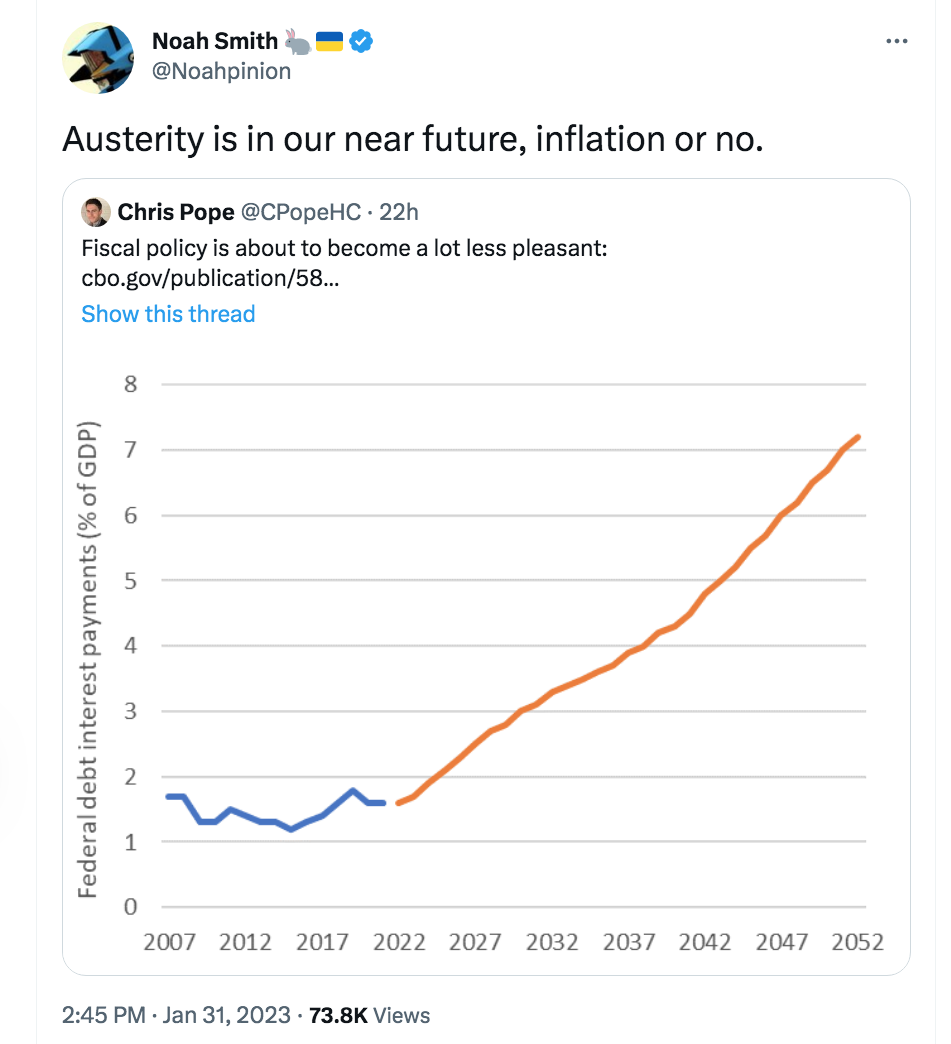

For years I’ve been warning that reckless fiscal policy (under Trump and Biden) would lead to future tax increases. And for years I’ve been attacked as an old fogey who doesn’t understand that we are in a new era of zero interest rates, a new era of free credit forever.

Monetary policy is about aggregate demand. Fiscal policy is about efficiency. The profession made a huge mistake in conflating the two policies.

PS. There are a few signs the economy might actually be speeding up:

Vacancies at US employers unexpectedly increased at the end of 2022, illustrating a solid appetite for labor that the Federal Reserve sees as one of the last hurdles to bring down inflation.

The number of available positions climbed to a five-month high of just over 11 million in December from 10.4 million a month earlier, the Labor Department’s Job Openings and Labor Turnover Survey, or JOLTS, showed Wednesday. The increase was the largest since July 2021 and mostly reflected a jump in vacancies in accommodation and food services.

(While I’m doing my annoying “I told you so” routine, I might as well add that I ridiculed those who claimed two falling quarters of GDP meant we were in recession during early 2022. I don’t recall any previous recessions with record job openings.)

Tyler Cowen has a post discussing the possibility of the economy reheating, and has this to say:

Another possible pathway for these scenarios involves interest rates. During a normal disinflation, the Federal Reserve raises rates and keeps them high for a long period of time while the economy adjusts slowly — often passing through recession. But inflation has fallen more rapidly than expected, and so the market may expect the Fed to lower interest rates sooner than planned. And an expected cut in interest rates can encourage expansionary pressures just as much as an actual cut in interest rates.

It is a funny world in which slow inflation can cause faster inflation. It’s the logic of expectations that makes it possible, albeit far from certain.

Of course this would not be a case where low inflation is directly causing high inflation. Rather, if this happened it would be a case of the Fed looking at inflation when it should be looking at NGDP growth, and wrongly concluding that monetary restraint is no longer needed. Persistently excessive inflation is always and everywhere a monetary policy failure.

David Beckworth has a new podcast where he interviews John Roberts, who spent 36 years at the Federal Reserve Board as a macroeconomist. At one point in the interview he was asked about how the Fed should tweak its policy regime in the next review period (which is scheduled for 2024):

Roberts: So I think in that statement of longer-run goals, that constitutional document, I would keep, for the reasons I was just saying, the shortfalls language on maximum employment. But I’m not sure I would keep the shortfalls language on the average inflation targeting. My reasoning is that, if you think about it, that puts an upward bias to inflation. When they adopted that, it seemed like it was a good idea to have an upward bias on inflation, because their concern was getting stuck in a low inflation world because of the low interest rates. Today, it doesn’t look like we have a problem with inflation never being able to be high. It looks like that’s perfectly possible. So I don’t think, from today’s perspective, they need that asymmetry in the constitutional document anymore.

Roberts: And then in terms of if they ever do hit the lower bound again, what statement language they should use… So I think in retrospect, it looks like having those two criteria for liftoff, both the maximum employment and the price level-related one, led to monetary policy being too loose for too long. So a really simple change in my view would be to change the “and” in that conditionality to an “or.” So you would say then that, “We will keep the federal funds rate at the effective lower bound until either we’ve achieved maximum employment or some kind of average inflation targeting criterion has been reached.” So that would’ve stood them in good stead this last time around, because by the middle of 2021, they had already made up the shortfall in prices. So that promise would not have gotten in the way this last time. And it would’ve stood them in good stead in the previous cycle where it took a long time to get to maximum employment and inflation kept undershooting. So it would work for each of the last two cycles. Who knows? Maybe some other thing will come up that would make it not work in the future, but at least, it would have worked, I think, in the last couple of times. So the tweak there would simply be to change “and” to “or.”

Given his career path, I imagine that Roberts has much more insight than I do into where policy is headed. While these are his own views, I suspect the final decision will be not too dissimilar to his proposal. After all, the Fed knows they erred in allowing inflation to get too high, and thus the obvious place to adjust FAIT is in making it symmetrical, at least for inflation.

It’s unfortunate that the Fed is probably unwilling to adopt NGDP level targeting. I suspect they believe that their mandate forces them to target inflation and employment, but that is not the case. The mandate is the goal of policy; if the Fed believes (as I do) that NGDPLT is the best way to achieve that goal, then NGDPLT is fully consistent with the dual mandate.

The change from “and” to “or” does make the employment part of the regime less bad, but there’s still room for mischief. And it’s a mistake to make any promises about the path of interest rates, including a promise not to raise rates until some threshold for inflation or employment is met. To see why, consider Roberts’ explanation of what went wrong in 2021:

So they said that they would keep the funds rate at zero until the unemployment rate reached their estimate of maximum employment. They didn’t spell that out, but that could well have been, say, 3.5% unemployment because that’s where they were pre-COVID and that was not inflationary.

He’s probably right about the 3.5%, but of course that’s a terrible way to do policy. During the 1970s and early 1980s, the unemployment rate was far about 3.5% and yet we had a severe inflation problem. The Phillips Curve is not a reliable guide for policymakers.

Again, the Fed needs to stabilize NGDP growth along a level path. All policies that lead to highly unstable NGDP will fail to stabilize the macroeconomy.

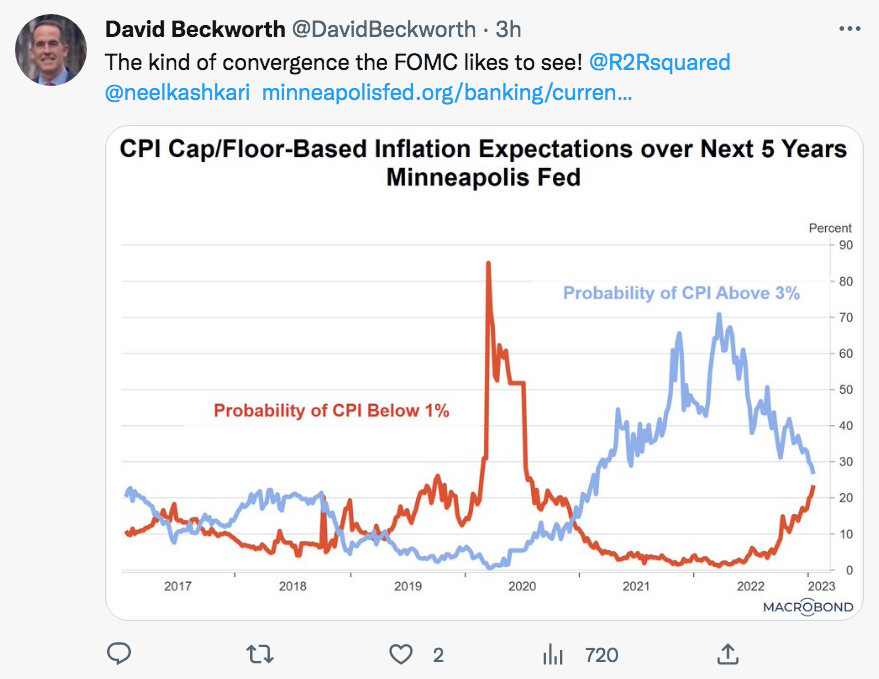

I mostly agree, but would delete the phrase “kind of”. The Fed wants to see convergence, but the kind of convergence they’d like to see is down below 10% chance of each type of overshoot, not roughly 25% chance of each.

PPS. In a new article I wrote for the National Review, I point out that low and stable NGDP growth is a necessary and sufficient condition for the Fed to achieve its policy goals:

The Fed does not currently target nominal spending. But as a practical matter, the Fed cannot achieve its goal of low inflation and high employment without stable nominal-spending growth. Whenever spending growth is far below 4 percent, unemployment will rise sharply. Whenever it is far above 4 percent, inflation will rise. Because spending growth is the sum of inflation and real GDP growth, it is the best single indicator of the Fed’s performance.

A policy target of 4 percent spending growth is much more credible and transparent than a vague policy aimed at 2 percent inflation and high employment. How should high employment be defined? The Fed doesn’t tell us. How does it balance the goals of avoiding high inflation and encouraging high employment? The Fed doesn’t tell us. What does it do if it misses a policy goal? Again, the Fed doesn’t tell us.

Read the whole thing.

PPPS. New new NGDP figures show 7.3% growth over the past four quarters, which is far too high. I warned you all back in early 2022 not to assume that just because the Fed had embarked on a series of rate increases they were tightening monetary policy. Interest rates are not monetary policy. Money was extremely loose in 2022.

Welcome to a new blog on the endlessly perplexing problem of monetary policy. You’ll quickly notice that I am not a natural blogger, yet I feel compelled by recent events to give it a shot. Read more...

My name is Scott Sumner and I have taught economics at Bentley University for the past 27 years. I earned a BA in economics at Wisconsin and a PhD at Chicago. My research has been in the field of monetary economics, particularly the role of the gold standard in the Great Depression. I had just begun research on the relationship between cultural values and neoliberal reforms, when I got pulled back into monetary economics by the current crisis.

"This man is the devil. Look at his eyes. Same as Soros. All baggy and nasty. Good people dont age like that. Its the sign of a madman. A negativity..."

"I watched Satantango on video over 3 days. I found it absolutely gripping, but one must surrender for a time one's idea of what a movie should be. Instead, you..."