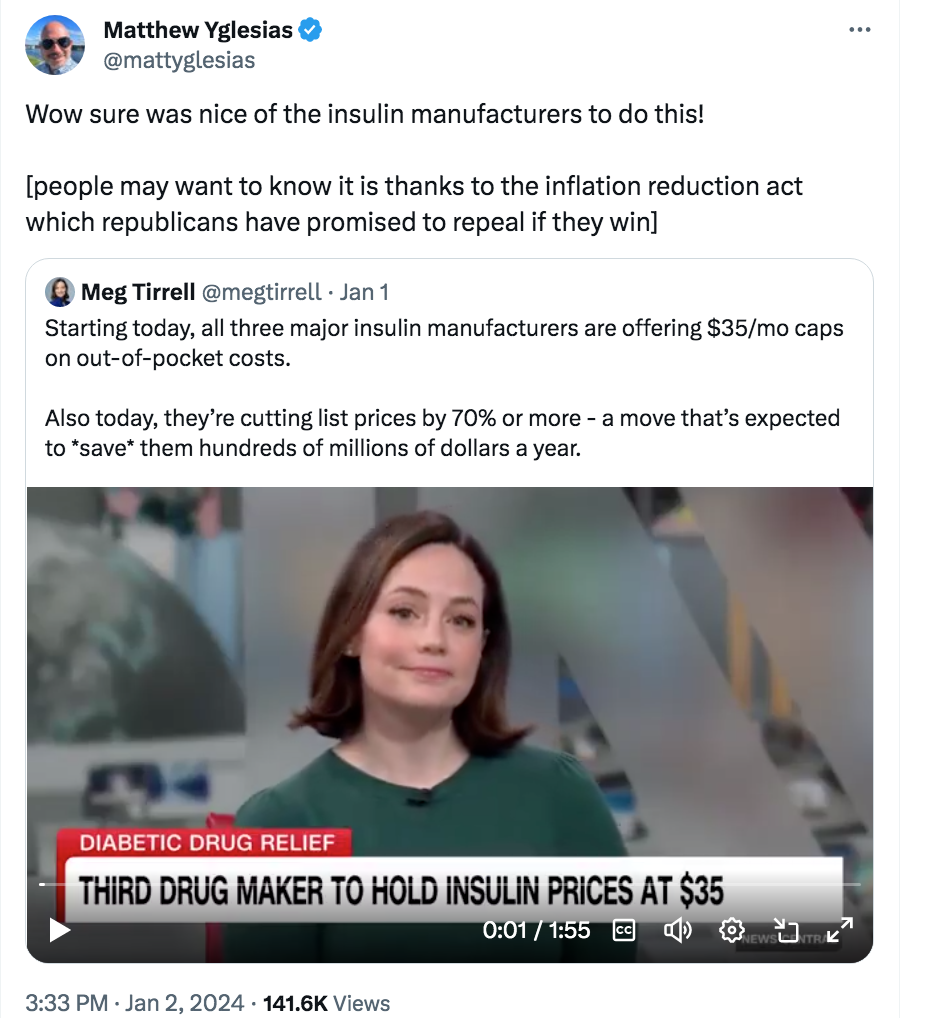

In an earlier post, I explained one reason why Trump will win. But the ineptness of the Biden campaign is so comical that I cannot help piling on a bit. Consider this tweet by Matt Yglesias:

CNN is generally a fairly left-of-center network, and yet even they report this news in a way that helps the Trump campaign. You don’t see Fox News spinning the news in a pro-Biden direction. (Fox reporters seem to think the economy is in the midst of another Great Depression.) If this is the coverage Biden can expect from the left, he’s got no chance.

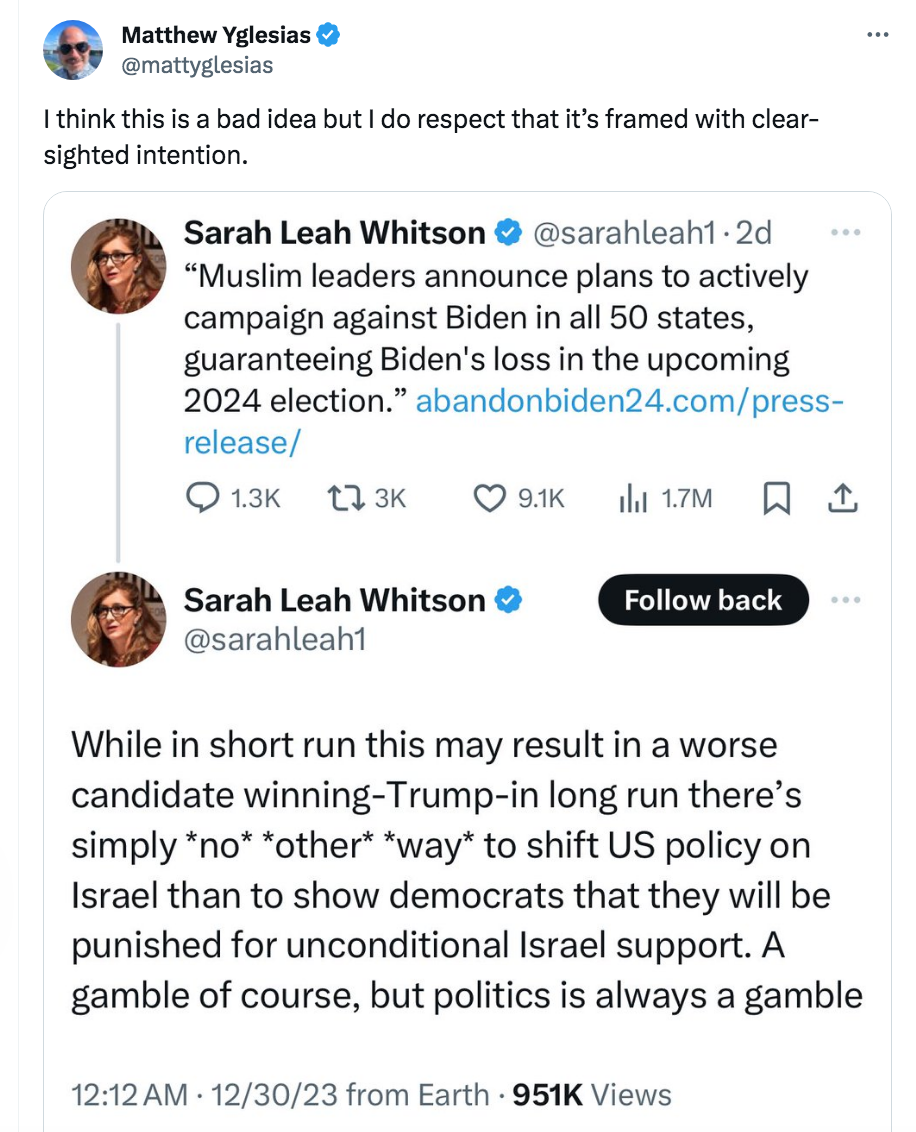

So a candidate who is campaigning on a viciously anti-Muslim platform, which includes a proposal to ban visitors from Muslim countries (and from Gaza), is about to be supported by America’s Muslim leadership.

Remember those TV commercials where an old person would say “I’ve fallen and I can’t get up”? That’s what Biden reminds me of. It’s mind-boggling to see such an inept campaign from a leading political party. I’m old enough to recall when the Dems would nominate skilled politicians (Clinton, Obama, etc.)

When the public is in a fascist mood, all news helps the fascists. The GOP in Congress refuses to appropriate funds to control the border? That just shows that we need a GOP president, so they won’t be so obstructionist!

On the internet, I see endless debate about the so-called soft landing. Many people seem to believe that some sort of law of economics has been violated. Inflation has come down substantially, and yet the labor market remains strong.

I see all sorts of problems with this debate. One problem is that we are assuming that a soft landing has occurred, which is premature. The second problem is that we are using a “Phillips Curve” approach that is based on fluctuations in inflation, when we should be focussing on NGDP growth.

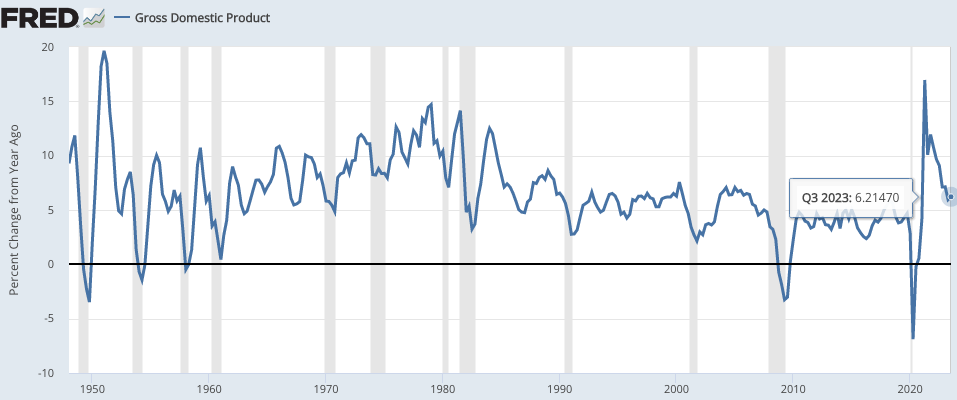

If you focus on NGDP growth, then things become much clearer:

In the past, recessions tend to occur when NGDP growth falls sharply. But not always. There was no recession in 1952, 1967 or 1986. And even better indicator of recession is a fall in NGDP growth to a level well below the average of the previous decade. That doesn’t explain the 1974 recession (when the economy was distorted by the removal of wage/price controls), but it basically explains all the others.

The most recent data shows a 12-month NGDP growth rate of 6.2%, which is well above the average of the previous decade. Yes, that’s much lower than two years ago, but as we saw in 1951-52, a big drop in NGDP growth doesn’t necessarily cause a recession if it’s a return to normal growth after an abnormal spike. Instead, recessions tend to occur in years like 1953, 1957 and 1960, when NGDP growth falls to well below normal. But that hasn’t happened . . . yet.

If NGDP growth were to stay at 6.2%, then inflation would level off at about 4.4%. But I don’t believe NGDP growth will level off—I expect further declines. People talk about how surprising it is that NGDP growth could fall to levels consistent with 2% inflation without triggering a recession, but maybe we should wait for that to actually happen before patting ourselves on the back.

And it might happen! There’s never been any logical reason why a soft landing is impossible—you need to disinflate at a gradual rate. So far the Fed has done that. (Keynesians are wrong in thinking that recessions cause the disinflation, they are a side effect of overly rapid disinflation. Tighter money causes the disinflation.)

Some might argue that the 6.2% NGDP growth rate for the past 12 months is overstated, as NGDI growth has only been about 3.0%. But the GDP figure seem much more plausible. For instance, reported RGDP is up 2.9% while RGDI is actually down more than 0.1% over the past year. Given that job growth has been far above trend, and trend RGDP rises at 1.8% even when job growth is normal, which figure seems more plausible?

So far, the economy’s performance is far less surprising if you focus on NGDP rather than inflation. NGDP growth has not fallen to a rate that would typically trigger a recession, it’s still well above trend. Yes, inflation has done a bit better than one might have expected given NGDP growth, just as inflation did worse than expected up until mid-2022. Both can be explained by temporary supply factors, which artificially boosted inflation in 2021-22 and have artificially depressed it over the past year. Those are head fakes. Don’t let misleading inflation figures screw up your understanding of the economy—ignore inflation and focus on what really matters—NGDP growth.

To achieve its 2% inflation target, the Fed must get trend NGDP down to about 3.8%. Perhaps it will do so without triggering a recession. Maybe it’ll over tighten into a recession. Forecasting is a game for fools. Right now, markets see a soft landing as the median outcome, but either an undershooting or an overshooting is certainly possible.

K.I.S.S.—Focus on NGDP and ignore inflation.

Happy New Year, and may all your landings be soft.

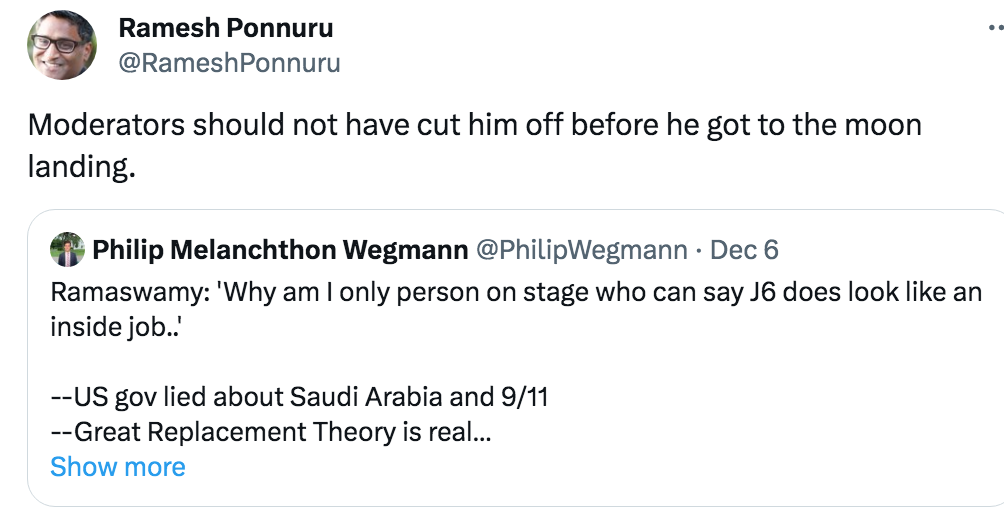

I know what Ponnuru is getting at, but isn’t this a rather odd comment? Of course J6 was an inside job; the conspiracy went right to the very top of the US government. The president and his henchmen encouraged a violent mob to storm the capital with the goal of intimidating Congress into not certifying Biden’s victory.

I find it odd that when people talk about “the government”, they tend not to include the president. Consider:

During the Trump administration, campus leftists called for government laws against hate speech. And yet I doubt that those leftists actually wanted President Trump to regulate hate speech.

During the Trump administration, “the government” pressured Twitter to “combat misinformation” regarding Covid. Yet Trump was widely seen as being against cancel culture.

BTW, during the Trump administration, lots of Trump supporters liked his approach to lockdowns. But Trump supported the lockdowns back in the spring of 2020, and explicitly criticized the Swedes for avoiding lockdowns. It’s as if Trump’s supporters drew a distinction between Trump and “Trump”.

There is probably no politician in US history that spoke out more forcefully than Trump in favor of using “the government” to take political candidates off the ballot. Trump used this argument against Obama, Hillary, Ted Cruz, among others. And yet his supporters see him as a critic of “the government” meddling in elections. They were outraged by the Colorado and Maine rulings. (It’s the Dems who should be outraged, as the courts are handing Trump the presidency on a silver platter.)

There are some questions that are so absurd that no pollster would ever think of inquiring what the public believes. But they should! How about a poll on these questions:

1. Should the government be able to determine what’s taught in the public schools?

2. Should the government stop interfering with Medicare?

3. Should the government determine military policy on gays and transgender people?

You might be surprised to find out what “the public” actually believes.

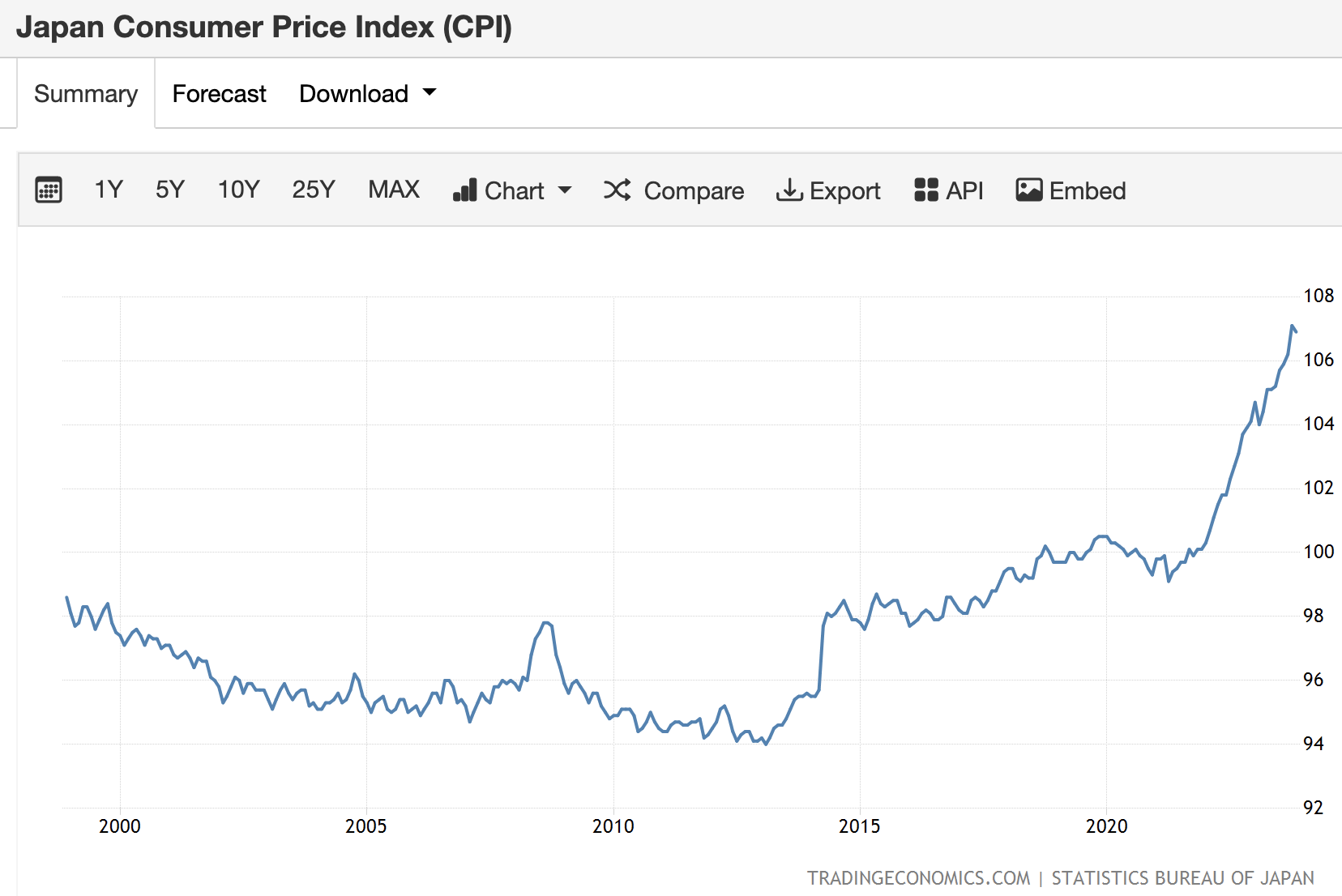

Some people have asked why I supported Japan’s decision to raise their inflation target from 0% to 2%. After all, money is roughly neutral in the long run and by 2013 Japan had mostly adjusted to their near zero inflation rate.

I made a couple of arguments. Central banks tend to use interest rates as a policy instrument, and this works better if nominal rates are not stuck at zero. In addition, Japan’s equilibrium real interest rate was so low that the Fisher effect is not fully operative. Raising inflation from 0% to 2% might only raise nominal interest rates from zero to 1%, or even less. This would help public finances. A 2% inflation rate would also lead to a smaller central bank balance sheet.

Bloomberg has an article where new BOJ Governor Kazuo Ueda makes some similar points:

“The most obvious benefit of a slightly positive inflation rate is larger room for monetary policy responses to an economic downturn,” Ueda said in a speech Monday at a conference hosted by the Keidanren, Japan’s biggest business lobby, in Tokyo. . . .

While Ueda refrained from dropping a clear hint on the timing of any potential policy change, he joins his deputy Ryozo Himino in highlighting some of the benefits that would come in a world without negative rates, including an improvement in net interest income.

I’m not certain which net interest income he’s referring to, but he clearly agrees that the Fisher effect is not fully operative.

I’ve also argued that it is wage inflation that matters, and without wage inflation any price inflation is transitory. In the US, the recent focus is on getting wage inflation down to a level consistent with 2% inflation. But as Ueda points out, Japan needs higher nominal wage growth to ensure that recent price inflation is sustainable:

The central bank kept the world’s last negative rate at a policy meeting last week. Ueda said Monday that a key point to watch is whether wages will continue to rise “markedly” in next year’s annual spring wage talks.

[Recall that I’m not a hawk or a dove. It depends on the situation. Lower wage growth in America, higher in Japan.]

Prime Minister Abe switched to a positive inflation policy at the beginning of 2013. Since that time, inflation has averaged a little over 1%. That’s well below the BOJ’s 2% target, but far better than the deflation that existing prior to 2013. And despite the higher inflation, short-term interest rates remain at zero. For Japan’s fiscal authorities, this is like picking up 10,000 yen notes off the sidewalk.

I’m glad to see that Ueda is continuing Kuroda’s policies at the BOJ.

PS. Japan’s NGDP has also been increasing in recent years, a sign the higher inflation is not just reflecting high import prices due to a weaker yen.

It’s natural to categorize people—put them into little boxes with other people sharing similar characteristics. And there are certainly a few boxes into which I might comfortably fit. But I often see commenters put me in the wrong box, based on a misreading of my actual views.

For the most part, I’m neither an optimist nor a pessimist about the macroeconomy. I’m neither a monetary hawk nor a dove. I’m neither a foreign policy hawk nor dove. I’m neither a left-winger nor a right-winger. I’m neither a Democrat nor Republican. I’m neither pro-Israel nor pro-Palestinian. I could go on and on.

That’s not to say I’ve never offered an optimistic or pessimistic take on the economy. But my baseline view is that the market forecast is optimal, despite the fact that the market forecast almost never turns out to be precisely correct.

As an analogy, if the Eagles were favored by 3 over the Chiefs in the Super Bowl, then I would forecast the Eagles to win by 3. But I’d also assume that the odds of that precise outcome occurring are probably less than one in ten. For the economy in 2024, I see some risk of both recession and excessive inflation, even as a soft landing appears to be the market forecast.

This is why I believe it is impossible to reliably predict the business cycle; you’d be predicting Fed failures. I can predict that drunk drivers and inflation targeters will have more accidents than sober drivers and NGDP level targeters, but I cannot predict precisely when those accidents will occur. People try to avoid having accidents!

Similarly, I may seem hawkish at some times (2022) and dovish at others (2009), but my basic view favors 4% NGDP growth, level targeting. Because many people have a strong dovish or hawkish bias at almost all times, I get lumped into a box with people who interpret something I said as suggesting that I have a consistent policy bias in one direction or another. I do not.

On foreign policy, I oppose neoconservative adventurism. Instead, I favor blocs of like-minded non-aggressive nations that promise mutual help in the event an evil outside power invades one of their members. If that group becomes large enough, then no outside power would dare to invade. As an analogy, 48 states came to the aid of Hawaii in 1941, despite the fact that Iowa had little fear of a Japanese invasion. The bigger this mutual self defense group becomes, the better.

This view makes me seem hawkish when the alliance is attacked, and dovish when it is not attacked. (Yes, there are ambiguous cases, such as when to provide financial aid to non-members that are being attacked, or what to do about piracy on the high seas, terrorism, etc.)

Although I am neither particularly optimistic nor pessimistic about the near-term course of the macroeconomy, I do have views on other issues. I’m relatively pessimistic about the fiscal situation, which is likely to get worse in the medium term. I’m also pessimistic about the medium term global political situation, as the rise of nationalism is likely to produce bad outcomes. These worries are related, as populism underlies both trends.

In the long run, the global political cycle will turn again. I just hope it doesn’t take a disaster such as the two world wars before people wake up to the folly of nationalism.

Merry Christmas everyone. And when you go into the voting booth in 2024, remember to ask yourself: What would Jesus do?

Welcome to a new blog on the endlessly perplexing problem of monetary policy. You’ll quickly notice that I am not a natural blogger, yet I feel compelled by recent events to give it a shot. Read more...

My name is Scott Sumner and I have taught economics at Bentley University for the past 27 years. I earned a BA in economics at Wisconsin and a PhD at Chicago. My research has been in the field of monetary economics, particularly the role of the gold standard in the Great Depression. I had just begun research on the relationship between cultural values and neoliberal reforms, when I got pulled back into monetary economics by the current crisis.

"Tom, I quoted Orwell on that point a few months back in another post. https://www.econlib.org/the-world-weve-lost/ Lizard, Switzerland is not protectionist. They have very high rates of immigration. They don't invade..."

"Switzerland? Didn’t they ban minarets a few years ago? I get that they have relatively high levels of immigration, but I kind of assumed that they aren’t very cosmopolitan. Not..."

"Have you read Orwell’s essay on Nationalism (contrasted with patriotism) in which he says that all Nationalists have to believe something false, eg that the UK was just as strong..."