Which country abolished the home mortgage deduction in 2001?

Update: Commenter Brent pointed out that this post seems to be based on an error on my part. Canada did not abolish the home mortgage deduction in 2001. My apologies. (I got this information from someone who may have confused Canada with the UK.)

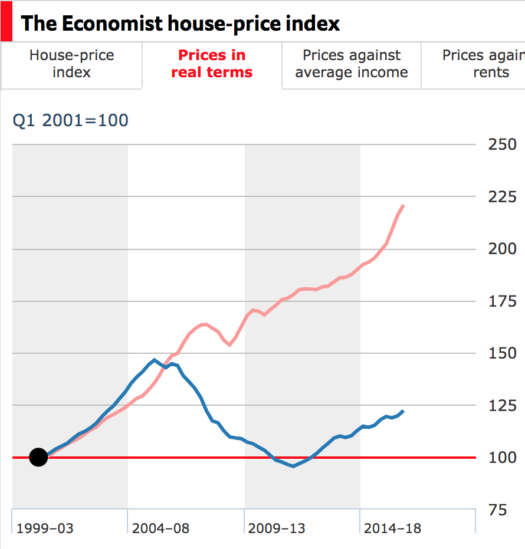

The pink in line is Canada and the blue line is the US.

The pink in line is Canada and the blue line is the US.

The proposed bill would only take away the deduction for the top 5% of US mortgages.

PS. Our media has an ironclad rule that the middle class must always be described in glowing terms, or treated as victims. Thus if they are talking about things that benefit the top 5%, this group is called “rich”. After all, the government never does anything good for the middle class, only the rich.

But if they take away a benefit from the top 5%, suddenly that group is called the “middle class” and we are all supposed to shed tears for their suffering:

The 429-page GOP tax plan, called the “Tax Cuts and Jobs Act” was revealed on Thursday and is being billed as a boon for hard-working middle class Americans.

But Republicans have proposed paring down popular homeownership incentives, which would likely affect millennials and millions of people living in high-cost housing markets.

The tax plan cuts the $1 million limit for the home-mortgage-interest deduction in half. The deduction allows homeowners to write off the interest they pay on home loans, effectively reducing their taxable income. The bill would apply to new home purchases and make it so homeowners can only deduct interest payments on up to $500,000 worth of home loans.

In previous generations, that may have been a typical mortgage amount for a first-time homebuyer, but today’s young people are different. Millennials are “skipping starter homes,” Zillow CEO Spencer Rascoff said, and moving straight to the $1 million range when its time to buy their first house. . . .

“Eliminating or nullifying the tax incentives for homeownership puts home values and middle-class homeowners at risk, and from a cursory examination, this legislation appears to do just that,” William E. Brown, president of the National Association of Realtors (NAR), said in a statement.

So sad!

Tags:

8. November 2017 at 08:24

Why are higher home prices a good thing? Seems possible that it’s rather bad for the 40% of the population who dont own a home. Further, the rise is mirrored by price/rent ratios so you can’t make some argument about home prices reflecting some improved demand for housing. Seems to me that if you capitalize an earnings stream at ever lower rates, you are highly vulnerable to any shift that necessitates higher real rates.

8. November 2017 at 08:26

Scott,

If it were up to me, I’d wouldn’t just eliminate the deduction, I’d put a surcharge on mortgages over $500k.

8. November 2017 at 08:34

I’ve had a chance to digest the tax proposal and have a few observations:

1. The mortgage interest change probably doesn’t impact that many people as single filers would be the only ones who could viably use the mortgage interest deduction (and how many single filers have a million dollar mortgage balance?). For a couple, the new standard deduction would be likely be greater than the amount of interest they would pay on their $500k mortgage.

2. The elimination of the student loan interest deduction is annoying but probably harmless. Low-earners with big loans would do better off with the big standard deduction anyway, big earners might still not care as they won’t be taking line-item deductions, and those who are taking line-item deductions should just refinance their student loans with a HELOC and deduct it that way.

3. The bulk of the tax cuts go to changes that most help the President. It’s sickeningly transparent.

And of course, the plan adds $1.5 trillion to the deficit at a time when there’s no reasonable argument for fiscal stimulus. A revenue-neutral version of this plan could be good, especially one without the handouts for Trump Inc.

8. November 2017 at 08:53

Effem, You said:

“Why are higher home prices a good thing?”

I have the same question.

8. November 2017 at 09:41

The issue with blindly looking at said 5% is that it’s really three different demographics: People making their money off of capital, the top of wage earners in most of of America that just choose to live in gigantic mansions (my neighbors), and two very high salary families living in areas with nonsensical property values (see, the bay area). It’s those people that are the incidental losers here, as 3 bedrooms will easily hit the million dollar mortgage.

Ultimately though, I don’t think that the issue is that raising taxes on those people is something that the country shouldn’t do though: Let tech figure out why in the world they want so much in the workforce in a place that is so hostile to building housing. But it’s difficult to justify to those people that they will be doing worse (they are also hit by the state and local deduction thing), while the tax reform is full of gifts for people that are even better off. See the fun loophole regarding state taxes that Tyler Cowen mentioned a few days ago.

8. November 2017 at 09:42

99% of Millennials make less than $100,000 a year. On what planet are they able to qualify for a million dollar home?

8. November 2017 at 10:41

I’m confused by the title of this post. I’m pretty sure that mortgage interest for homeowners hasn’t ever been deductible in Canada and has always been deductible in the United States; neither country abolished it in 2001. While there was a 2001 Canadian court case affecting mortgage interest deductibility (Singleton v. Canada), its effect was to allow mortgage interest to be deducted in certain cases when the funds were converted to a business or investment purpose. Explanation?

8. November 2017 at 11:54

The politics of home ownership is completely absurd to me. Why is increasing ownership supposed to be a worthy goal? What’s so inherently bad about renting? And why do renters (disclaimer: I’m a renter) tolerate benefits to owners at our expense? This deduction is a transfer from lower quantiles to higher (even if technically ‘middle class’) ones. Why is that good? Why does anyone think that’s good?

Oh, and did the UK get rid of a home mortgage deduction then? And if so, what does that graph look like?

8. November 2017 at 12:24

Mark asked, “Oh, and did the UK get rid of a home mortgage deduction then?”

According to an OECD Survey, “The United Kingdom fully phased out the tax deductibility of mortgage interest payments over 25 years (1974-1999). First a nominal ceiling was introduced on the size of mortgages eligible for interest deductibility. Second, the tax rate at which interest on debt below the ceiling could be deducted was gradually lowered to zero.”

8. November 2017 at 15:54

Canada house prices have gone crazy due to inflows of foreign capital. And property zoning.

After China enacted capital controls, house prices in Vancouver cracked from $1.5 million to $1 million.

If you think high house prices are a problem, then the discussion is not about mortgage income tax deductions but rather property zoning and international capital flows.

8. November 2017 at 16:36

Ben Cole,

Chinese purchases of Canadian property were 2% of the total value in 2016. A few select cities does not represent most of the country.

If you remember, a decade ago Americans managed to raise housing prices 200% in five years all by themselves. That’s how it is for Canada/NZ/Australia and it remains true in the USA. Domestic buyers are far more important in the property market.

Oh, and based upon the graphic used by Scott, has anyone seen how the average Chinese home price/average annual wage has fallen from 150% in 2000 to 60% today? I hear a lot about a property bubble over there on clickbait websites and mainstream news, yet they all ignore the 10% growth in wages China has each year.

Scott pointed that out earlier this year when he showed how China’s average wages are now higher than in many of its former peers. Or maybe he was linking to Krugman.

8. November 2017 at 17:14

I was under the impression that the reason that mortgage interest is deductible is that all interest related to investment activity is deductible. It treats the homeowner and the landlord equally.

The goal of promoting home ownership is a rationalization that came after the fact, because it makes for a good soundbite.

8. November 2017 at 18:41

Alec and all:

http://vancouversun.com/opinion/columnists/douglas-todd-is-china-popping-vancouvers-housing-bubble

But China buyers are big in every major Canadian city. Canada is regarded as a safe and prosperous place to live, along with Australia and New Zealand, which are also now sporting $1 million average house prices in Auckland and Sydney.

After a while, one has to face facts: International capital flows and property zoning can have explosive upsides in housing costs. Why all the make-believe that something else is exploding house prices?

Property zoning alone can do some very serious damage—see Shanghai, Hong Kong and the West Coast of the US.

It is remarkable that the orthodox macroeconomics profession pays such scant attention to property zoning.

You get an occasional Moretti at Berkeley, but most of the profession is obsessed with minute inflation, with the evils of the minimum wage and rent control, and the virtues of running large current-account trade deficits.

You see, rent control is bad-bad-bad-bad, but property zoning is not really a topic.

8. November 2017 at 18:43

One really bad idea in the bill is to eliminate the alimony deduction for the payor while making alimony received nontaxable. Current law is the opposite: if I pay alimony I can deduct it from my taxable income, but it’s taxable income to.my ex.

So why bother changing it? Because if the payor is in a higher tax bracket than the payee, total tax paid will be higher.

Alimony is court-ordered. The person paying it has no choice, he or she pays or goes to jail. It is not income to the payor, as he has nothing to say about how it is spent. It is income for the receiver, so that’s where the taxation belongs.

8. November 2017 at 21:35

Found an article Scott might like, especially considering his recent post about the bitcoin “bubble.

https://www.bloomberg.com/news/articles/2017-11-09/in-2017-investors-can-either-buy-bubbles-or-be-left-far-behind

‘The best way to crush the crowd in 2017? Buy the things everyone insisted would never keep going up.”

9. November 2017 at 00:09

– Sweden abolished the tax deduction for interest on mortages in 1990. And as a result of that Sweden had a (small ??/large ??) depression in the early 1990s. It’s not surprising because then real estate becomes less affordable for A LOT OF people.

– Higher prices for e.g. home prices, copper and iron ore is good because it stimulates credit growth for investment in more homes, copper mines and iron mines. Credit growth means more spending and more employment (think: Steve Keen)

– But the flipside side is that the consumers have to pay more for the things they consume like homes. And when prices rise more than wage/income then there’s a point where those same consumers simply can’t afford that stuff anymore.

– Talking about rising prices: It took A LOT OF time but now real estate in Australia is in the 1st stages of tanking. E.g. some apartments in Sydney have dropped some 18 % in price.

https://www.macrobusiness.com.au/2017/11/spoilt-sydney-venders-slash-asking-prices/

Other articles suggest that some apartments have come down in price by some 30%.

@SSumner: Do you still believe that Steve Keen was wrong when he predicted that australian home prices would come down (back in 2011 ??) ??

9. November 2017 at 04:20

Jeff: Great point about alimony.

Doug M: “I was under the impression that the reason that mortgage interest is deductible is that all interest related to investment activity is deductible. It treats the homeowner and the landlord equally.”

Case 1: You and I each buy a 100k house with a 5% IO mortgage and live in our respective houses. We each have to pay 5k/yr in interest payments and we get a 5k write-off on our taxes. Net cost is something less than 5k/yr (depending on our MTRs).

Case 2: You and I each buy a 100k house with a 5% IO mortgage and rent it to each other. Each of us has to charge the other 5k/yr rent to cover the interest payments. The interest payments are a business expense which is offset by the rent. Net cost is a full 5k/yr.

So we’re much better off in case 1 even though they should be identical. The interest deduction really does seem to favor buyers over renters. If you throw in the property tax deduction, it gets worse. (The landlord has to charge the renter the full amount of the property tax whereas the owner gets a write-off, just like with

interest.)

Yes, there’s depreciation and other miscellaneous tax effects, but I think that’s a second-order effect that just affects the timing of tax payments.

9. November 2017 at 08:07

One difficulty with back-of-the-envelope tax analysis in the US is the oddity of the standard deduction. So many tax incentives would have obvious effects on behavior, if only people could take advantage of them.

Canada (errors about mortgage deductibility aside) is also unlike the US in that many of the Canadian ‘deductions’ are instead tax credits: they’re first-dollar reductions in tax paid rather than last-dollar reductions, so they have the same marginal benefit across income groups.

9. November 2017 at 08:14

Scott, off topic money question:

If quantity of money is fixed, doesn’t a real GDP increase cause deflation? Like, if an economy has $100 and 100 products and then the products increase to 110 but still in terms of $100, that’s deflation right?

If so, why do Keynesians believe the Phillips curve? With fixed money quantity, shouldn’t an increase in employment/output decrease inflation?

9. November 2017 at 09:42

Mervyn King makes some interesting points in this NBER talk, especially about 30 minutes in;

http://www.nber.org/feldstein_lecture_2017/feldstein_lecture_2017.html#

9. November 2017 at 14:37

@The Original CC:

case 2 is better, because you can effectively shift income into the future, depending on the delta between rent and cost of owning the house. If you expect your future tax rate to be lower, that is a plus. Also, in the case you set the rent to be exactly the interest cost + depreciation, you are now able to deduct property tax plus maintenance on your income tax. The powers that be understand this, therefore there is a provision in the tax code for rents that are below market rent:

http://rontaxcpa.com/showtip.php?newsid=139

In your example (case 2) of only charging the interest expense, the tax consequences are way better, as you would have the full standard deduction, and be able to deduct the losses (property tax + maintenance + depreciation).

9. November 2017 at 18:28

Viking, case 1 is vastly better. I’m just trying to keep it simple and assume that each person rents out the house at cost. In this model, the only cost is interest.

In one case, it costs 5%*100k and in the other it’s 5%*100k*(1-MTR).

If you get rid of the home mortgage interest deduction, then the cases are the same, which is how it should be.

People completely miss this and they think that the home mortgage interest deduction is somehow fair b/c a landlord would also be able to write off interest. What they miss is that the landlord also has to pay taxes on the rent. (I used to have this misconception too until a friend straightened me out.)

Of course, there could be other arguments for allowing this deduction.

10. November 2017 at 04:48

Steve F – Please don’t say that the “Keynesians” back the Phillips curve, that’s the New Keynesians. Post Keynesian economics totally rejects the Phillips curve, because, as your example makes clear, inflation is caused by increased nominal money competing for goods and services, and not by anything else.

Sumner isn’t really the person to ask about this since he thinks inflation is caused by banks sitting on excess reserves, but eh.

10. November 2017 at 07:40

Am I too big to say I told you so;

https://sports.yahoo.com/everyone-knows-lonzo-ball-cant-shoot-right-now-even-lakers-rookie-190949125.html?.tsrc=daily_mail&uh_test=1_07

————-quote————

We’re less than two weeks removed from Lakers coach Luke Walton assuring us he’s not concerned about [Lonzo] Ball’s jumper. Since then, Ball took just two shots against the Portland Trail Blazers, missing both to become the first top-five pick to go scoreless in at least 28 minutes since 1992, and then followed that up with 3-for-15 and 3-for-13 outings against the Brooklyn Nets and Memphis Grizzlies.

Still, Walton assured us, via the Los Angeles Times, that there’s no reason to be alarmed. “Hopefully soon; hopefully in Boston it will turn around,” the coach said. “But I know that he’s out here working. I know that he’s been a good shooter his whole life. I’ve seen him make 10 straight spot shooting. He’s got the skill and the ability. It will only be a matter of time when that percentage starts to go up.”

That’s also when Ball first mentioned, “I think it’s just in my head.”

————-endquote————

10. November 2017 at 07:48

Oh yeah, the fifth best player on last year’s Gonzaga team hasn’t even scored a point yet in the NBA;

http://www.espn.com/nba/player/splits/_/id/4066650/zach-collins

10. November 2017 at 12:15

Thanks Brent, I screwed up. There is a correction now.

Doug, No, that’s why it should not be deductible. Rental property income is taxable, whereas the implicit rents earned by homeowners is not.

JM, You said:

“Sweden abolished the tax deduction for interest on mortgages in 1990. And as a result of that Sweden had a (small ??/large ??) depression in the early 1990s.”

Abolishing the mortgage deduction caused a depression? Who knew?

You said:

“Talking about rising prices: It took A LOT OF time but now real estate in Australia is in the 1st stages of tanking. E.g. some apartments in Sydney have dropped some 18 % in price.”

I’ve had about 20 similar comments over the past 8 years—all were wrong. Who knows, maybe you will be correct. But I doubt it.

Steve F, The PC assumes demand shocks, your example assumes supply shocks.

Patrick, Yes, the first few games in the NBA of a former college freshman tell you all there is to know about a player.

13. November 2017 at 10:04

Canada housing bubble

https://www.bloomberg.com/view/articles/2017-06-21/canada-s-housing-bubble-will-burst

It seems to me you want to subsidize renting. Or is the interest deduction on rental income also be to eliminated?

Finally, the issue is not whether mortgage interest is deductible or not, but that many homeowners bought their houses and took out mortgages under the assumption that interest would be deductible. Thus, the value of their house will drop immediately, and their tax expense will rise.

Do the Republicans have 52 votes for all this? Will Flake, McCain and Corker all go along?

13. November 2017 at 10:49

Steven, No, as I’ve explained 100 times the deduction for rental property is because rental income is taxable. Owner occupied houses are not taxed, so it makes no sense to deduct interest. My proposal would level the playing field. This isn’t rocket science.

And people in this comment section have been predicting a Canadian collapse since I started blogging. Why should I pay any attention to the predictions of any commenter in this comment section? Please tell me, I’d love to know.

Even if Canadian house prices fell 20% tomorrow the Canadian bubble theories would have been 100% wrong.