Watch what they predict, not what they say

Lots of commenters make a big deal about the fact that some Fed officials, and Ben Bernanke in particular, often make statements implying that they don’t engage in monetary offset. One response is that they also make statements implying that they do engage in monetary offset. Talk is cheap, and there’s no doubt the Fed would prefer that Congress do more of the heavy lifting, so they could do less (and hence be less controversial.)

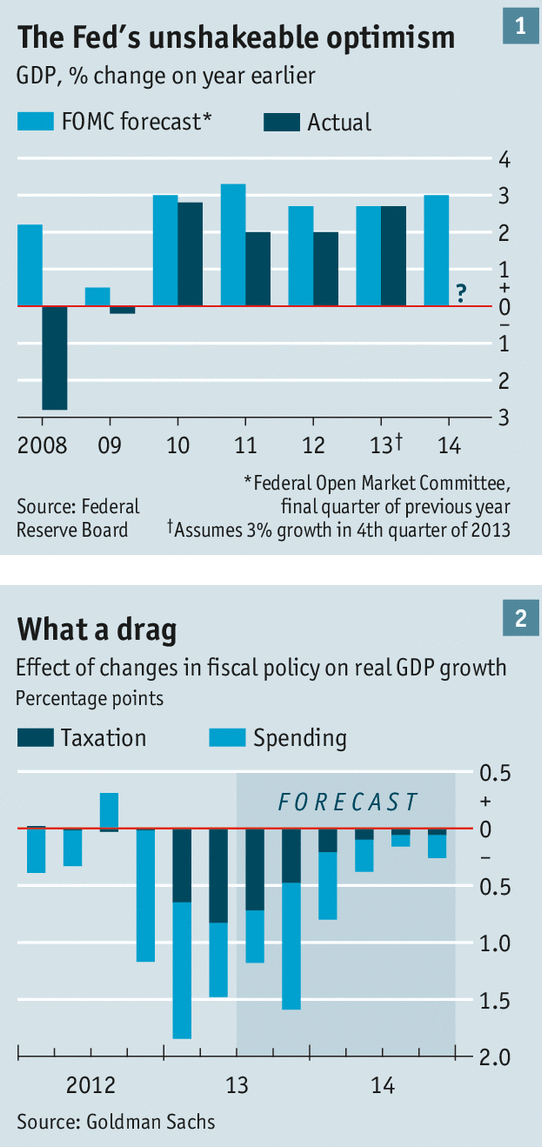

But actions speak louder than words. How does the Fed change its forecast of RGDP growth in 2013, as a result of the big tax increases plus sequester? Take a look at the following, from The Economist:

Lots of people have noticed that actual GDP growth accelerated in 2013, as compared to 2012, despite all the austerity we were warned about. But of course lots of unexpected things can happen over a 12 month period. I find it much more interesting to look at the expected effect of austerity. Notice that expected 2013 growth is identical to expected 2012 growth.

Now some will argue that that’s only because other things were changing to offset the effect of austerity. For instance, the Fed did QE3 and forward guidance in late 2012.

Which is exactly the point.

PS. In fairness, I’m not sure how fully they understood the extent of fiscal austerity in their December 2012 forecast. They did cite looming fiscal austerity when justifying their monetary stimulus of late 2012, so it was clearly understood that austerity would occur. But in March they lowered their RGDP growth forecast from 2.65% to 2.55%, perhaps because of more information about the severity of the austerity.

The Fed lowered its GDP forecast slightly downward in the March FOMC meeting

The Fed is forecasting from 2.3% to 2.8% in GDP growth for 2013, taking down the top end of the range from 2.3% to 3.0%. The Committee noted that the private economy was growing a little faster than anticipated, and that would nearly offset the fiscal drag imposed by the Jan 1st tax hikes and the sequester. They did adjust their 2014 and 2015 forecasts lower as well, although not dramatically.

On the other hand Q1 growth was very weak, so it seems equally likely that that triggered the downgrade in forecasts, not the sequester. Fiscal austerity might or might not have lowered the Fed’s growth forecast by 10 basis points. That’s far from the apocalyptic forecasts of the Keynesians.

Tags:

6. March 2014 at 10:26

Scott, I’m a huge fan, but this post actually seems to be a step back for you. Fed real GDP forecasts aren’t worth the paper they’re written on. This classic post by Evan Soltas illustrates the point very well:

http://esoltas.blogspot.com/2012/08/the-fed-as-little-orphan-annie.html

The Fed, for four solid years, was predicting that recovery was only a day away. The fact was that there was a disconnect between what the fed forecast in RGDP growth versus what it was willing to allow in terms of inflation and NGDP growth. The nominal variables are obviously the ones over which the fed has the most direct control, so with the Fed stupidly celebrating its failure to hit its 2% inflation ceiling, it’s no wonder that the catch-up RGDP growth failed to materialize.

If we really wanted to look at the fed’s “actions” we would look at how they evaluate their performance relative to market forecasts of appropriate nominal variables (NGDP!). Unfortunately the Fed still fails to target the right variable, so everyone is more or less in the dark.

6. March 2014 at 11:30

The Fed staff has steadfastly predicted high on growth, high on inflation and way too high on unit labor costs for five years running…you know, only the basics. But they have something like 700 economists churning out reports…and mysterious contracts with even more…to what end?

Why did Market Monetarism evolve outside the Fed? To this date, has the Fed ever held a conference or symposium on Market Monetarism?

Is the Fed an example of cloistered ossification?

6. March 2014 at 11:37

Scott,

Off Topic.

JazzBumpa has a thoughtful and clearly written post that takes on Market Monetarist interpetations of 2008. If I have the time I may respond to his substantive points.

http://angrybearblog.com/2014/03/did-the-fed-cause-the-great-recession.html

But for the moment the following claim caught my attention:

“In mid 2008, core inflation was running at 2.3 to 2.5%, not far off its decade-long average of 2.2%, and had been pretty stable year to date.”

I knew right away this was incorrect in several respects and I had a hard time figuring out why until I realized that he was looking at core CPI and not core PCEPI.

The Fed has never targeted core CPI. It targeted headline CPI from 1988 until 1999. In 2000 it switched to targeting PCEPI. In 2004 it switched to targeting core PCEPI.

Why does this matter? Because the behavior of core CPI and core PCEPI was radically different over the period in question:

http://research.stlouisfed.org/fred2/graph/?graph_id=164121&category_id=0

Note that core PCEPI was significantly lower than core CPI until 2003. Year on year core PCEPI had been as low as 1.0% in June 1998. It averaged just under 1.9% in the decade through June 2008. It reached 2.3% in May through August 2008 and that was only a tenth of a percentage point below the highest level it had been in the previous 15 years.

The reasons for the divergence of core PCEPI from core CPI relate to healthcare and housing but that’s not really important in my opinion. Nor am I trying to justify the inflation hawks’ behavior in 2008. But I do think it’s important that we look at the inflation measure that the Fed was actually paying attention to.

6. March 2014 at 12:57

SG, It make be a step backwards, but I think you missed the point. I agree that GDP forecasts are often inaccurate. But they do reveal the forecaster’s view of which factors affect GDP. So in that sense they are quite revealing, despite their inaccuracy.

Ben, I presented a paper on NGDP targeting with futures markets at the Fed. I was told they don’t need your help, they know how to control AD.

Mark, Very good point.

6. March 2014 at 14:38

Scott,

Off Topic.

More on JazzBumpa’s post.

http://angrybearblog.com/2014/03/did-the-fed-cause-the-great-recession.html

JazzBumpa on David Beckworth:

“I have a hard time accepting this ignore what I do, pay attention to what I say [or don’t say] argument.”

In my opinion this mischaracterizes what David Beckworth is saying. He’s saying that the Fed needed to do more than mere actions. It needed to clearly communicate its intentions, and it needed to communicate the *right* intentions.

JazzBumpa on David Beckworth:

“It has to assume that people are deciding their actions by thinking months or years into the future based on what they think the Fed might do then, instead of reacting to what is happening today. Maybe I’m just disoriented by the time travel, but in a world where the major focus is on the current quarter’s returns, I don’t think very many actual people behave that way. Nor do I believe that the hoi polloi have even the vaguest awareness of Fed activities, let alone their words.”

Private physical investment is sensitive to expectations of growth and is vulnerable to changes or even proposed changes in monetary policy. It *is* the volatile component of GDP whose decrease *is* the immediate cause of recessions:

http://www.applet-magic.com/recessioncause2.htm

Private physical investment decisions are largely made by corporations, not the hoi polloi.

JazzBumpa on Marcus Nunes:

“The Market Monetarist response, from Marcus is, “Interest rates are a terrible (even misleading) indicator of the stance of monetary policy.” At his article linked in the first paragraph of this post, Marcus indicates that the true stance of monetary policy is the resulting growth in NGDP – which I believe, as post-hoc as it may be, is the axiom on which Market Monitarism rests.”

This is precisely why we need market based measures of NGDP expectations, just as we already have for inflation expectations. Unfortunately the nearest substitute is the Survey of Professional Forecasters (SPF) which only comes out every three months, and probably is far less sensitive than a market base measure would be.

The median forecast for one year NGDP growth by the SPF peaked at 5.8% in 2003Q4. It consistently fell below 5.5% by 2006Q1 and below 5.0% by 2007Q3. It fell from 4.50% in May to 4.08% in August 2008. This was the largest decline since the 0.43 point decline in 2004Q1 when the forecasted one year NGDP growth rate was much higher.

By November 17 the one year NGDP forecast had fallen to 2.59%, a decline of 1.49 points. That is the largest decline ever in the one year NGDP forecast by the SPF on records going back to 1968. It was also a full 1.15 points below the previous record low in one year NGDP expectations of 3.74% in 1998Q4.

How much of that decline occured between August 12 when the 2008Q3 forecast was made and the September 16 FOMC meeting is hard to say. But if inflation expectations as measured by TIPS spreads are any indication, the decline was evenly distributed throughout those three months. So NGDP expectations probably had been falling at the fastest rate on record for over a month from an already low level, but there was no direct way of knowing this at the time.

6. March 2014 at 16:55

“That’s far from the apocalyptic forecasts of the Keynesians.”

Which Keynesians do you have in mind-a name or two? What was the forecast? I ask this because I don’t know which Keynesians you have in mind who allegedly said growth would fall off a cliff in 2013.

If Congress had really failed to do a deal on the fiscal cliff it would have been plausible that GDP would have fallen off a lot. However, what most ‘Keynesians’ I’m aware of said was that that the austerity was needless and that it would lower growth to less than it would otherwise have been. Growth had been predicted to be more in 2013.

6. March 2014 at 16:57

” there’s no doubt the Fed would prefer that Congress do more of the heavy lifting, so they could do less (and hence be less controversial.)”

So when people like Krugman urge Congress to do more of the heavy lifting why do you object? Whenever there is criticism of fiscal austerity you criticize the piece because the Fed can allegedly fully offset it. If the Fed doesn’t want to do this-assuming they can-why are you insisting on it?

6. March 2014 at 17:46

A bit off topic. If NGDP has been significantly subpar for 5 years now why is inflation still above 1%? Prices should be declining right? Sticky prices is only a short term phenomenon.

6. March 2014 at 17:56

There she blows! Set the sails! va va voom! va va voom!

6. March 2014 at 20:08

“Which Keynesians do you have in mind-a name or two? What was the forecast? I ask this because I don’t know which Keynesians you have in mind who allegedly said growth would fall off a cliff in 2013.”

Krugman, Delong among others would have predicted that the 1-2% of GDP austerity would have simply caused a 1-2% drop in RGDP. They support the idea of more QE, but believe monetary policy only has a small effect by reducing long-term rates and committing to keeping rates at zero.

Austerity went up significantly in Q4-2012 while RGDP growth appears completely flat from 2012-2013. Ezra Klein tried to explain this with increased state/local expenditures, but state/local expenditures have to follow tax revenues due to balanced budgets. And tax revenues follow mostly from private economic activity.

Therefore, the private sector would have had to go on to a 1-2% RGDP boom right when the federal government cut 1-2% of RGDP. In the past, Krugman has attributed private economic growth in liquidity traps only to the effect of long-term interest rate reduction or to the eventual failure of durable consumption and capital. With little movement in long-term interest rates, then suddenly a lot of failures happened in durable/capital stock must have coincided with austerity.

…Or the multiplier is zero.

6. March 2014 at 20:16

“A bit off topic. If NGDP has been significantly subpar for 5 years now why is inflation still above 1%? Prices should be declining right? Sticky prices is only a short term phenomenon.”

NGDP growth since 2009 is typical of NGDP growth we had 1991-2007. The issue is the level, for both NGDP and prices, is far below what their track would be without the deflation of 2008-09.

As far as sticky prices, sticky price/wage theory holds that there will always be some of the economy that is not sticky. Oil had no issue dropping precipitously in 2008. These non-sticky markets will inflate and deflate along with NGDP, while most companies with declining revenues (their part of NGDP) will reduce headcount rather than wages. Even with reduced headcount, the company needs to make a profit on the marginal cost of the employees’ labor. Therefore, prices are sticky as well as wages.

The more depressed industries need the most NGDP growth in order to “unsticky” their prices/wages. Each industry has a different point where their prices/wages become unsticky.

6. March 2014 at 20:23

Wages are made far more sticky because of inflation, as well as Marxist exploitation theory, minimum wage laws, and welfare.

All of these problems are solvable without violence. Most of the inflationists on this blog are just intellectually lazy and refuse to think of better solutions that SWAT teams and legalized counterfeiters.

7. March 2014 at 00:46

Confessions: Sometimes when Scott says things like “I’m going to take a break from blogging for a while” I’m actually naive enough to believe him.

7. March 2014 at 00:51

😛

7. March 2014 at 00:53

In all seriousness though when even the openminded Adam Gurri is complaining (https://twitter.com/adamgurri/status/441215959747932160) it is probably a sign that saturation has been reached. The Guardian is spacing out the release of Snowden’s leaks for a reason, you know. And I say this as someone who rarely misses any of Scott’s posts and who thought that the recent Econlog post (http://econlog.econlib.org/archives/2014/03/ngdp_targeting.html) was one of Scott’s best ever in a catalogue of what, thousands now?

7. March 2014 at 00:54

Nick Rowe continues his streak of beautifully explaining things I thought only I believed (the nature of the demand for money): http://worthwhile.typepad.com/worthwhile_canadian_initi/2014/03/coordination-and-the-demand-for-money.html

7. March 2014 at 01:26

Mario Draghi: “We have been everything but inactive.”

http://www.nytimes.com/2014/03/07/business/international/european-central-bank-holds-rates-steady.html?smid=tw-share&_r=0

7. March 2014 at 02:18

Scott Sumner:

I tried a Federal Reserve literature search through the St. Louis Fed website, and evidently the Fed or the Fed System has never published a paper on Market Monetarism.

Now, Woodford did address a Fed conclave last year and more or less say NGDP targeting was best.

And you gave your presentation.

More than Fed 700 economists, and an unknown number of economists either on contract or retainer—but not one has ever written on Market Monetarism.

It is like trying to find a monograph on surface ship vulnerability published by the US Navy.

7. March 2014 at 02:32

Mark Sadowski-

Good point about the PCIPI—but!

Okay, the 2 percent target is supposed to be an average target, not a ceiling. That means the Fed undershot the target all those years leading up to 2008. Where were the klaxons? The hysteria?

And, that also means when the PCEPI reached the 2.2 percent or so, the Fed stomped on the brakes.

This was about the time the FOMC used the word “inflation” more than 500 times in a single meeting.

I still say the stats and transcripts (now that we citizens are “allowed” to look at the transcripts) reveal a Fed that is probably comfortable with inflation around one percent, and a ceiling of 1.5 percent. At two percent the FOMC loses its bowels (Richard Fisher attends the FOMC meetings in adult diapers).

I don’t believe in inflation targeting, but if I did, I would day those targets are too low to allow robust real growth

7. March 2014 at 03:18

lxdr, A good reason to pay no attention to inflation. Sticky prices do not imply a sticky CPI.

Saturos, Just for that I’ll write another post today.

7. March 2014 at 05:25

Scott,

Fair enough, I guess my hang up is that Fed forecasts of steady growth are just as likely to reflect incompetence as they are to reflect the future path of monetary policy. You point to a forecast revealing that the fed believed that the impact of fiscal austerity would be limited, but the pre-crisis and early-crisis forecasts revealed that they believed the recession would be much shorter than it has been. Those forecasts were wildly, ludicrously optimistic, so it’s not as if they represented anything akin to useful forward guidance. Rather, the fed took other actions (letting Lehman fail, followed by failing to cut interest rates) that convinced the market that it was happy to let NGDP fall 9% below trend.

If we’re talking about actions demonstrating the Fed believed it could offset fiscal austerity, exhibits A, B, and C are the postponement of the taper in the fall.

7. March 2014 at 06:02

Honest question:

With stock futures up on this news, is the stock market no longer rooting for inflation?

http://www.businessinsider.com/jobs-report-analysis-2014-3

“there was a big gain in average hourly earnings (+0.4%), the strongest in a long time. This is a sign of a tightening labor force, which is something markets have been talking about lately, that the market is tighter than people realize.

Bottom line: A solid, goldilocks report that the market will like. But the average hourly earnings is a big story.”

7. March 2014 at 09:40

Dear Commenters,

Does anyone else find Greenspan’s rapid change in view on inflation in the 90’s as extraordinary? In 1996, he was interested in pursuing ZERO inflation. Then, suddenly, as unemployment approached 6%, he decided not to tighten and accepted higher inflation.

How The Hell did Greenspan make such a rapid intellectual shift? Can anyone explain it?

Below are some links with background:

http://www.econjobrumors.com/topic/reminder-yellen-personally-responsible-for-2-inflation-target

http://slate.me/1ea2tfG

7. March 2014 at 09:51

Major_Freedom,

See this famous post by Prof. Sumner: “Long and Variable LEADS”

http://www.themoneyillusion.com/?p=6693

Is Prof. Sumner correct about “long and variable leads” or only partially correct? Where does his model go wrong?

Whose views are closer to the truth: those who believe in “long and variable lags” or those who don’t believe in them?

P.S.: Blast from the past: In the comments section of the “long and variable leads” post, notice Morgan Warstler’s praise of Lacy Hunt of Hoisington, who loves loves loves long-term U.S. treasuries. Hmmmmmmm……..

7. March 2014 at 09:57

Ha! Check out Prof. Sumner’s reply to Morgan Warstler in September 2010!

http://www.themoneyillusion.com/?p=6693#comment-29472

“You said;

“Moreover, the demand problem is rapidly transforming into a structural problem as

1. unemployed workers lose skills,”

Which is why we need more demand.

“2.bad debts accumulate,”

which is why we need more demand

“3. and the fiscal deficit explodes (70-80% due to NOMINAL tax revenue losses, stimulus, and automatic stabilizers).”

which is why we need more demand

Did I remember to tell you we need more demand?”

Morgan deserves TONS of credit for being so open-minded about this subject since 2010…….

7. March 2014 at 11:47

SG, Good point about the taper.

Travis, I think markets still want more NGDP, not sure about inflation.

I think Mark Sadowski has a link showing that Yellen may have helped nudge him toward 2%.

7. March 2014 at 11:55

TravisV:

I suspect the reason why Sumner adheres to the flawed approach of rejecting “long and variable lags” is due to a need to cover up the exploitative nature of inflation, for political strategy purposes. Inflation only “works” because it is exploitative. By that I mean inflation were instead a miraculous system that raised everyone’s incomes equally at the same exact time, then inflation would have little to none of the effect that you guys tend to call “stimulative.” It is precisely because inflation affects some incomes first, and then other incomes next, over time, which is what economists call “long and variable lags”, that we might see a correlation between higher inflation and higher employment or output. In short, inflation “works” only because not everyone knows, understands, or experiences it the same.

Couple that with the vulgar version of EMH that purports all prices rapidly adjust to changes in the money relation, and it is not surprising that he would find himself knee jerking against what is so obviously true it should not even be debatable.

The model goes wrong because it is a brainchild, or should I say stepchild, of general equilibrium theory. If you notice, there is a conflation between the events leading to the idea of a general equilibrium, with the equilibrium itself. This eay of thinking is encouraged because the general equilibrium framework cannot accommodate the market process. It deals only with final states of rest, and the corollaries of final states of constant change.

If you instead view the market as an ongoing process, then it is easier to understand long and variable lags.

An example: Did the Fed’s OMOs yesterday result in my company’s revenues instantly increasing by an equivalent percentage? No, of course not. It takes time for that new money to leave the banking system to a single borrower, who then takes time to exchange it with someone else, who then takes time to exchange it with someone else, and so on, before it reaches the last person. This is precisely why even the Fed acknowledges that it generally takes about 12 months or so after loosening or tightening before a change in “the economy” becomes noticeable and drowns out the other factors to a degree of confidence.

Inflation is always and everywhere a micro phenomenon. Yes, it is true that if the income of group A goes up, then ceteris paribus so will the total of all incomes go up. But it is not true that if total incomes have gone up, that everyone’s incomes have gone up equally, or at all. The totality of incomes does not, cannot, describe relative or individual incomes.

To answer your question of whose views are closer to the truth, those who accept or those who reject long and variable lags, the answer is trivial: Those who accept it.

7. March 2014 at 12:42

Major_Freedom,

What do you think is the probability that the U.S. experiences 20%+ inflation within the next ten years?

7. March 2014 at 12:49

TravisV,

One Austrian willing to make such a prediction is Vincent Cate: he says Japan will have > 2% inflation per month (> 26% a year) within 2 years from now.

The only other predictions I’ve seen like that are from Peter Schiff, who when confronted about his predictions being wrong, simply said HIS definition of inflation is expansion of the base, and the base expanded, just like he warned would happen if the base expanded, and thus he was right all along. Lol.

7. March 2014 at 13:56

Re: Greenspan’s change of heart, here’s another great blog post illustrating how extraordinary it seems:

http://www.cepr.net/index.php/blogs/beat-the-press/did-janet-yellen-argue-with-greenspan-for-higher-or-lower-interest-rates

“‘Janet and I were both worried about inflation, even though it was very well contained at the time,’ Mr. Meyer wrote in a blog post last month. ‘We told the chairman that we loved him but could not remain at his side much longer if he continued, as he had been doing for some time, to push the next tightening action into the next meeting, and then not follow through.’

“Mr. Meyer and Ms. Yellen ultimately stood by Mr. Greenspan, who had correctly predicted that technological change was fueling a boom in productivity and alleviating inflationary pressures. The Fed did not raise its benchmark interest rate until the following March.”

7. March 2014 at 16:01

Mark A. Sadowski, O/T: one remaining question I had regarding our previous discussion of the CB taking over banking in a cashless society: you drew a sharp distinction between nationalizing the banks under a single national bank run by the gov (but still there’s a separate CB). And the CB directly taking over. You cited some evidence from France regarding how nationalization itself makes very little difference. My question to you though is from a “black box” perspective (i.e. everything inside gov is in the black box), it doesn’t seem very different to me. Post nationalization, if the CB were to slowly start to take over the nationalized bank, one tiny step at a time: move the bank’s HQ to the CB’s HQ. Replace bank staff with CB staff. etc. So that at the end of this process, the national bank is fully incorporated into the CB w/o a trace of independence left. At what point do bank liabilities become “money?” Is it a gradual process, or does it happen all at once in one critical step? If one step, what would be that critical step or steps? Thanks.

7. March 2014 at 18:48

Tom Brown

“At what point do bank liabilities become “money?””

The bank liabilities where always money. Money isn’t considered money just because it is state issued. It is considered so because it is a medium of exchange, store of value and unit of account.

7. March 2014 at 19:41

dannyb2b, thanks. I’m looking for the MM answer though. I know Scott only considers MOA to be money. Normally MOA in the US is currency and reserves: both liabilities of the Fed. Currency, reserves, and bank deposits are all MOE, but only the first two are MOA.

I presented the above hypothetical to Mark & Scott a week or so ago: i.e. starting from a cashless society, then the CB takes over the banking sector. So before the CB takes over, only reserves are money because that’s the only MOA. But after the CB takeover reserves are meaningless. This makes sense: imagine merging the CB’s balance sheet with that of the commercial banks’ balance sheets: reserves would go away. But now the bank deposits become direct CB-deposit liabilities. Mark and Scott agreed that these CB-deposits are the closest thing to money left, so they take on that role. I think that means we could call them the MOA at that point (of course they are still MOE).

Nick Rowe calls MOE “money” so I guess I’m really after the Sumner/Sadowski view here. But I think Nick would agree about what we can call MOA in this hypothetical, both before and after the CB takes over.

Mark was very clear, however, that if instead of the CB taking over the banks, the banks had been merely nationalized, then reserves would have continued to have their original role and that I couldn’t claim that the quantity of “money” had changed. I think this means that nationalized bank deposits would continue to be only MOE and not MOA and that reserves would continue to be both MOA and MOE. The MOE part is not really important: We only need concern ourselves with what constitutes MOA at any one point in time.

Now I want to know exactly where the magic happens… exactly when we can call those bank deposits “money” (i.e. MOA) as we gradually CB-itize the nationalized bank.

7. March 2014 at 20:07

I see banks deposits, reserves and currency as money. They are all components of the USD with different limitations, features and purposes. They have different issuers so IMO you could say broader and narrow money monetary policy is controlled by commercial banks and the CB.

Reserves are limited in that only banks with fed accounts can hold them. They are used to transact amongst depository institutions.

Currency is limited in that it can only be physically transacted. It can only come into circulation as far as I know into the broader non banking system by means of banking intermediaries.

Deposits are limited in that issuers require to hold a proportion of reserves in order to issue in countries like US (Australia doesn’t impose RR). Deposits are a more efficient means of transacting when compared to currency and more widely held than reserves.

7. March 2014 at 20:54

dannyb2b, … in case you’re interested in all that, here’s what else I learned, although I haven’t gotten buy-in on the language I use here, but I have some evidence that all three: Rowe, Sadowski and Sumner (and even David Glasner), might bless this basic story:

Cashless society:

time=t0, reserves=R, bank deposits=D, CB-deposits=0.

I think we can claim that M(t0)=M0=R here. “CB-deposits” don’t really exist yet prior to the CB takeover, thus they’re 0. If P at time=t0 is P0, then should M change to M1 at time t1, then eventually P1 = P0*M1/M0 (the long term neutrality of money), all else being equal. So, for example, if the CB were to buy some bonds and increase R to R1, then P1 would eventually go to P1=P0*R1/R.

However, if the CB now takes over the banks we get this:

time=t1, reserves=0, bank deposits=0, CB-deposits=D

Assume that R is not equal to D, and that R > 0 and D > 0.

As Mark argued, the reserves go away. So do bank deposits because the banks are gone, and they are replaced with CB deposits. Thus M1=D.

Here’s the rub though: P1 does NOT eventually go to P0*D/R. Why not? Nick Rowe explained: demand is transferred between bank deposits and CB deposits (i.e. between non-MOA and MOA) in this case thus invalidating the simple QTM formula. I *think* another way to say that is that velocity at time t1 has also changed due to the way in which M was changed. In fact V1=V0*R/D. QTM is only true if V1=V0 and Y1=Y0. Thus M1*V1 = M0*V0, and thus the price level doesn’t change, i.e. P1=P0 (assuming all else equal, or in this case that Y0=Y1). So the QTM formula fails in this case but of course the exchange equation: M*V=P*Y is still true, as it must always be since it’s a tautology. Another way to say that is that QTM is true when all else is equal, but in this case all else wasn’t equal. The way in which M was changed also changed V such that the change in M was perfectly offset.

Again I’m trying to understand the MM view here, but in terms of these simple formulas and concepts, and that’s what I have so far. Of course it’s intuitive that P1=P0. Why would P change? I just wanted to work out the reason why it stays the same here even though M changed.

Another thing I’d like to know is if there are other cases in which demand is transferred between MOA and non-MOA as a result of the method used to change the quantity of MOA (i.e. the method used to change M). For example, what if the CB were to take over something else and replace it with CB deposits (something other than bank deposits)? Are bank deposits unique here in the non-MOA world of goods?

My previous thread with Mark, Scott, and Nick is here:

http://www.themoneyillusion.com/?p=26213

7. March 2014 at 21:01

dannyb2b @ 7. March 2014 at 20:07

That sounds like a fairly common set of ideas that you have there, but again, I don’t think it comports with the Sumner version of MM. To Sumner, bank deposits are credit and definitely NOT money! I’m not saying your ideas are incorrect (I’m in no position to judge!), but I’m interested in learning Sumner MM orthodoxy. 😀

7. March 2014 at 22:45

Im pretty sure MM orthodoxy gets thrown off by a country like Australia that has no RR. For example since 1990 MB is up about 5-fold while CPI has less than doubled. P1 = P0*M1/M0 isn’t showing up in the empirical data. If V is stable in long run as I understand then I dont know how MM explains this. I could be missing something not sure where though.

“I just wanted to work out the reason why it stays the same here even though M changed.”

Using my reasoning, not MM reasoning I would say that’s because the money supply hasn’t actually changed. Credit (deposits) is money. Just becuase the deposits are held at a commercial bank or central bank doesnt change the fact they are money if they circulate through the economy in an identical manner. Why would the commercial bank deposits (credit according to MM) affect prices differently than physical money (currency) circulating through the system?

How inconsistent is MM terminology with most people’s understanding of money? The deposits in you bank aren’t money its just credit and currency is only physical not what is in your deposit account. I would say currency is deposits at commercial banks and physical money and all dollars are money.

8. March 2014 at 01:35

dannyb2b, MM works fine with RR=0% and no cash. In theory anyway. MM isn’t about lending or “channels” or broad money or any kind of “money multiplier.” Read that link I provided… not for the comments, but for Sumner’s article. The “Channels to nowhere” post.

Actually, this one on the HPE is even better:

http://www.themoneyillusion.com/?p=23314

“Channels to nowhere” makes a LOT more sense once you read the HPE one.

Especially see case 7, the cashless society case. That’s ALWAYS my baseline case when thinking about MM, because I personally don’t like thinking about cash: it just makes the story messier IMO. I like to think about a cashless society with just a single commercial bank and where RR=0%: where MOA never moves anywhere in the private sector (other than the one bank) and never gets in the public’s hands. In fact now that Sadowski says it doesn’t make any difference if the commercial banks are nationalized, my new baseline case will be Case 7 with a CB and a single separate nationalized bank. Then I can truly say that MOA will NEVER touch the private sector’s hands, and yet according to theory MM still works. It brings the important aspects of the HPE to the fore w/o all the messiness of cash and banks and channels to worry about.

To be sure, Sumner and Sadowski in no way think that currency (by which I mean physical cash: paper notes and coins) is unimportant. They think it’s very important, and frequently point out that prior to 2008 it comprised the bulk of the MOA in the US. And yet, when it comes right down to it, the theory works fine w/o it.

I think Sumner just threw in case 7 to humor people like me who find it hard to believe that currency actually is important and who thus always bring up the “cashless case.” Well he’s very explicit there: cash is definitely NOT required for HPE or MM to work.

So again, I understand there’s different ways to interpret what happens, but if you really want to digest the Sumner MM way, that HPE article above is a great place to start. Read that, and everything else here will make a lot more sense. 😀

8. March 2014 at 02:12

It seems impossible to avoid transmission mechanisms. For example S doesn’t change if the new gold discovery cant enter the economy. Expectations only adjust if it is expected that the gold will enter the system or transmit into the system. Imagine the gold discovery is simply inaccessible then expectations wont budge because the gold supply cant be transmitted from underneath the earth to the economy.

Supply can only move once gold or money is transmited into the system otherwise its the same as not having discovered any gold. Expectations are based on something actually happening in the economy in terms of S and D in the future.

“my new baseline case will be Case 7 with a CB and a single separate nationalized bank. Then I can truly say that MOA will NEVER touch the private sector’s hands, and yet according to theory MM still works. It brings the important aspects of the HPE to the fore w/o all the messiness of cash and banks and channels to worry about.”

Yes I agree. But There is a transmision mechanism. For example if the CB increases reserves it will affect rates of return on holding these and induce portfolio rebalancing into other assets. I’m not sure what I’m missing. Maybe Im wrong or maybe we have different ideas of what the transmision mechanism is. Expectations will move economy wide based on how people expect banks will react to changes in MB. Bank reactions are expected to transmit into the economy by affecting prices of assets and hence spending.

8. March 2014 at 07:52

Tom Brown,

“My question to you though is from a “black box” perspective (i.e. everything inside gov is in the black box), it doesn’t seem very different to me. Post nationalization, if the CB were to slowly start to take over the nationalized bank, one tiny step at a time: move the bank’s HQ to the CB’s HQ. Replace bank staff with CB staff. etc. So that at the end of this process, the national bank is fully incorporated into the CB w/o a trace of independence left. At what point do bank liabilities become “money?” Is it a gradual process, or does it happen all at once in one critical step? If one step, what would be that critical step or steps? Thanks.”

First of all, what do you mean by “money”? There are different ways of defining money and in the original hypothetical problem you posed, we were talking specifically about the monetary base. by definition he monetary base consists of currency and reserve balances. None of the physical steps you explicitly describe here affect either the amount of currency or the amount of reserve balances. Thus they have no effect at all on the monetary base.

Secondly, whether or not something is a liability of the government is simply not a useful criteria when talking about the monetary base. There are many examples both historical and current of commercial banks that are state owned. By definition the deposits of these banks are a liability of the government. However, the deposits of these banks are not reserve balances with the central bank and hence are not part of the monetary base. There are also historical examples of central banks which were privately owned. In those examples the reserve balances were not a liability of the government.

In short, this fixation on whether something is a liability of the government or not (inside the “black box”) seems to me to be an artifact of the MMT predilection for consolidating the treasury and central bank balance sheets, which MR, by essentially being a spinoff of MMT, has preserved for whatever reason. But it is not at all a useful distinction when thinking about monetary aggregates.

8. March 2014 at 08:06

dannyb2b, You write:

“Imagine the gold discovery is simply inaccessible then expectations wont budge because the gold supply cant be transmitted from underneath the earth to the economy.”

I don’t think Sumner would disagree. It’s only if it’s *expected* to increase supply at some point that it has an effect. That’s one of the only “channels” Sumner acknowledges. Here’s Scott in the “Channels to nowhere” post:

“Because money is a durable asset, expectations of the future value of money play an important role in its current value. I suppose that is a channel of sorts, but it’s merely a channel connecting future expected NGDP to current NGDP.”

So if one day the existence of the gold is announced, expectations rise perhaps, but if the next day it’s determined to NEVER be accessible, then they fall again.

“For example if the CB increases reserves it will affect rates of return on holding these and induce portfolio rebalancing into other assets.”

I *think* that’s the kind of explanation commentator “dtoh” might have made. dtoh spent a lot of time explaining things to me when I first started learning MM and he does not agree with Scott’s explanation. In particular he does not like the HPE. I thought I’d saved a link to my long thread with him, but I can’t find it. However, I did a site search on “dtoh” here:

http://tinyurl.com/nxvnby3

Maybe some of that is useful for you. I used to base my understanding off of dtoh’s ideas, but ever since Scott’s HPE article I’m OK thinking in terms of the HPE.

Also, you’re “rates of return” argument is similar to JP Koning’s concepts of “convenience yield.” You might check him out too (the following is the result of clicking on the “convenience yield” tag in Koning’s right hand column):

http://jpkoning.blogspot.com/search/label/convenience%20yield

A lot of good articles in there. In fact just yesterday I asked JP his opinion of my hypothetical above and how I should count M. Here’s his response (it involves the return on gold… and he brings up the idea of another competing jewel being introduced, thus lowering the return):

http://tinyurl.com/kycxa2f

So you may not be missing anything! But Sumner has a particularly simple way of explaining it which is attractive. Well, let’s finish the quote above from Sumner:

“To go from there to real variables such as output and employment, you simply need sticky wages and prices; channels like lending and interest rates add no explanatory power.”

So that’s the easy part! If wages & prices weren’t sticky then changes in M or expectations of changes in M would have no real effects! P would move, but so what? It’s the stickiness that causes (usually) damaging transients to be set up. Eventually steady state will be reached again, but why let the intervening damage happen? If various shocks are creating the long term pressures on P, and the fact that P doesn’t move instantaneously is a problem, then adjusting M can undo those pressures now before the transients get going. It won’t cure the economy from booms and busts, just the unnecessary real effects caused by nominal shocks and stickiness combined. That’s the idea. Remember to MMs the reason for unnecessary recessions is that there’s an excess demand for money. Sumner, Rowe, and even DeLong, and even Keynes (according to Sadowski) have said that the goal of good monetary policy is to make it appear as if Say’s Law is true (even though we all know that stickiness means it’s not actually true). Lars Christensen has put it slightly differently, saying good monetary policy should make it seem like real business cycle (RBC) theory is true. David Glasner won’t get on board those trains… he has a more nuanced view, which I don’t fully understand yet:

http://uneasymoney.com/2014/02/20/whos-afraid-of-says-law/

I hope some of that helps. My goal here is to fully understand the internal MM logic. I think Sumner and Rowe give particularly simple explanations for that logic, so why fight it? Put your purple robe on and grab yourself a cup of Cool-Aide. Lol. If you need empirical support, just ask Sadowski: he’s a fountain of empirical support.

Sometimes I do have trouble even with the internal logic, which is why I like my weird hypotheticals… to see if it all continues to stand up, at least internally. My goal is not necessary to believe it all when I’m done! 😀

8. March 2014 at 08:38

Mark, in my original hypothetical I had the banks nationalized, which was a problem as you pointed out. When I changed it to the CB taking over, we did have a long side discussion about the monetary base, but in the end it seemed to me that regardless of the label “monetary base” that direct CB deposits liabilities (replacing commercial or nationalized bank deposit liabilities) for private sector entities would qualify as “money” if not monetary base. Actually, in a follow up comment, Sumner seemed to be OK calling these CB deposits “monetary base” … but no matter. Your objections are why I dropped the term “monetary base” in favor of the more general concept of MOA. I *think* direct CB deposits qualify as MOA here (especially given that there’s no cash and no reserves), and MOA is money according to Sumner. ONLY MOA is money according to Sumner. It makes sense to me because these deposits are under the direct control of the CB. They now essentially define what a $ is. Also, they’ve never stopped being an MOE. So you’re right: being a liability is not important, but being the most liquid $ denominated goods in this hypothetical, whose quantity is under the direct control of the CB I think does make them a good candidate for MOA here. What do you think? Saying they’re a liability of the CB is only important in that it implies the CB has complete control over them.

So my though experiment is when does the MOA magic start for them? Is it when the balance sheet of the nationalized bank is formerly merged with the CB balance sheet for example? What is the essential quality here that defines MOA when the CB runs the banking system? And why doesn’t a nationalized bank have it? What is the crucial step in CB-itization of a nationalized bank at which the deposits flip to being MOA? Forget about “base money”… that proved to be a problematic term for this particular hypothetical. MOA is what’s important, and that’s what I want to focus on.

8. March 2014 at 08:47

dannyb2b, one last thing about weird hypotheticals: I don’t feel the least bit bad about introducing them into the discussion: Read any Nick Rowe post to see why! 😀

8. March 2014 at 08:48

Tom Brown,

“I’m looking for the MM answer though. I know Scott only considers MOA to be money. Normally MOA in the US is currency and reserves: both liabilities of the Fed. Currency, reserves, and bank deposits are all MOE, but only the first two are MOA.”

You are of course referring back to the seemingless endless MOA/MOE debates which are usefully summarized by David Glasner here:

http://uneasymoney.com/2012/11/25/its-the-endogeneity-redacted/

The debate was not over what *is* money but “about whether the medium of account or the medium of exchange is the essential characteristic of money, and whether monetary disequilibrium is the result of a shock to the medium of account or to the medium exchange”.

Incidentally, it might be useful to say something about the MOA.

Open any elementary textbook discussing monetary economics and it will tell you that the three functions of money are 1) as a unit of account, 2) the MOE and 3) a store of value. The term “medium of account” however, is rarely used in textbooks.

Where does it come from?

“Medium of account” appears to have been coined by Jürg Niehans in “The Theory of Money” in 1978 (although, as Niehans notes, Wicksell seems to have inferred the concept as early as 1906):

http://www.amazon.com/The-Theory-Money-J%C3%BCrg-Niehans/dp/0801823722

Whereas unit of account refers to the word used to quote prices, make contracts, and keep accounts (e.g. dollar, euro, yen, pound etc.), Jurg Niehans defined “medium of account” as the good that defines the unit of account. For example, going from a silver to a gold standard changes the medium of account, with the unit of account remaining the same.

In a purely fiat system, as the US has had since 1971, currency is the medium of account. Moreover, since the central bank can issue currency at will, there is no constraint on the creation of reserve balances. That is why monetary economists typically consider both currency and reserve balances to be the medium of account.

Commercial bank deposits however, are not the medium of account. Banks are contractually required to redeem their deposits at par value, but deposits in insolvent or illiquid banks have been known to trade at a discount (e.g. Cyprus). This cannot happen to the medium of account, as its price is fixed, and the central bank is the lender of last resort, by definition.

8. March 2014 at 09:50

Tom Brown,

“I’m looking for the MM answer though…I’m looking for the MM answer though.”

I think it might also be useful to say a word or two about what it is exactly that characterizes the beliefs of Market Monetarism.

Wikipedia is not the best authority, as it is subject to the whims of Wikipedia editors (I know firsthand, as I am the Wikipedia editor known as “Sadowski”). But it is reasonably up to date, and Market Monetarism is a rather new term. Here’s how MM is defined by Wikipedia:

“Market monetarism is a school of macroeconomic thought that advocates that central banks target the level of nominal income instead of inflation, unemployment, or other measures of economic activity, including in times of shocks such as the bursting of the real estate bubble in 2006.[1] In contrast to traditional monetarists, market monetarists do not believe monetary aggregates or commodity prices such as gold are the optimal guide to intervention. Market monetarists also reject the New Keynesian focus on interest rates as the primary instrument of monetary policy.[1] Market monetarists prefer a nominal income target due to their twin beliefs that rational expectations are crucial to policy, and that markets react instantly to changes in their expectations about future policy, without the “long and variable lags” highlighted by Milton Friedman.[2][3]”

So, the first sentence tells you that MM believes in NGDPLT. The second sentence seems primarily designed to point out that MM is not your grandfather’s monetarism. The third sentence tells you that MM rejects the focus on interest rates as the primary instrument of monetary policy. The fourth tells you that MM prefers NGDPLT because of rational expectations, and what I like to call (thanks to Noah Smith) the “random markets idea” (i.e. EMH).

With the sole exception of NGDPLT all of these beliefs are standard textbook monetary economics of the type that you will find in Mishkin’s “The Economics of Money, Banking and Financial Markets”.

For example, Mishkin says the following about the traditional real interest rate channel of the monetary transmission mechanism:

“…many researchers, including Ben Bernanke of Princeton University and Mark Gertler of new York University, believe that the empirical evidence does not support strong interest rate effects operating through the use of capital.[1] Indeed these researchers see the empirical failure of traditional interest-rate monetary transmission mechanism as having provided the stimulus for search for other transmission mechanism of monetary policy…” (p. 618 of the 7th edition)

And an entire chapter (28) of Mishkin is devoted to rational expectations and their implications for monetary policy.

NGDP as an *intermediate target* of monetary policy is discussed with some skepticism on page 418, due to the fact that “the central bank has little direct control over nominal GDP”. But there is no discussion of NGDP as the *final target* of monetary policy, at least in the 7th edition (2004).

In other words, when you get right down to it, Market Monetarism is simply standard textbook monetary economics with the addition of NGDPLT.

This is in fact how I view what Scott Sumner has been trying to do the last few years. He is trying to get the (monetary) economics profession to climb out of the collective amnesia it seemed to fall into with the start of the Great Recession. Up until 2008, apart from NGDPLT, none of these ideas were considered strange or new.

In many ways this is deja vu all over again, as in the Great Depression most economists forgot all that they seemed to know, as exemplified by the ideas of Hawtrey and Cassel, only a few years previously.

8. March 2014 at 09:52

Mark, yes, that’s a very good summary. I don’t think I disagree with any of that, having read it once through. I prefer JP Koning’s summaries to Glasners though, only because they are slightly more complete: he folds in Rowe, Sumner, Glasner, and Woolsey, and his own thoughts, which are evolving by the way.

But here’s the reference to Scott’s article that you gave me a few days ago in the “Channels to nowhere” thread:

http://www.themoneyillusion.com/?p=17357

“I most certainly do think the medium of account is money, and I do think the equation of exchange applies to the medium of account-indeed it’s a tautology.” -Scott Sumner

“Nick, Yes, I agree with your second comment. Although I’d prefer you call the base the “medium of account” not the “unit of account.”” -Scott Sumner

So I think it’s very clear where Scott stands here and what language he likes to use. Since I’m in the house of Sumner, I’ll try to use Sumner’s language. And why not? It’s clear and easy to understand. 😀

Also, although Nick Rowe disagrees with Scott about what to call “money” (Nick includes goods which are MOE but not MOA, like bank deposits), it’s also pretty clear that Nick agrees with Scott in the “long term” … meaning to me that for long term effects, just look at the unit of acc…. er, sorry, the medium of account. 😀

8. March 2014 at 10:01

… BTW, JP Koning *I believe* has gradually moved closer and closer to adopting Scott’s language here, although he used to be quite critical of it. That’s interesting to me because he seemed to be the one paying the most attention to the endless MOE vs MOA debates and, like I say, drawing up the most succinct, comprehensive and to the point summaries of the various party’s positions and how they related as the debates drug on.

8. March 2014 at 10:13

Mark, thanks for the review of what MM is. I certainly did not know all of that, but I am not surprised by any of it. I always considered MM to be mainstream in many respects, with the addition of NGDPLT, pretty much just like you say. When I write that I’m “looking for the MM answer” that in no way contradicts that… I realize there’s a huge overlap between the MM view and other views on much of this stuff, but that’s my shorthand way of writing all that: especially when addressing someone like dannyb2b, whose views *may* not overlap with MM much at all.

8. March 2014 at 10:42

Mark, so I almost forgot to thank you for answering my question, which I think you did: the important quality I was looking for:

“Banks are contractually required to redeem their deposits at par value, but deposits in insolvent or illiquid banks have been known to trade at a discount (e.g. Cyprus)”

So what if the deposits of a nationalized bank were 100% guaranteed to always trade at par by the CB itself. Would that one step essentially CB-itize the national bank?

Rowe likes to talk about an asymmetry of redeemability between a CB and a commercial bank. So what if for a nationalized bank, this asymmetry were formerly abandoned and replaced, by law, with full symmetry? Maybe that’s what I was looking for.

http://worthwhile.typepad.com/worthwhile_canadian_initi/2009/10/what-makes-a-bank-a-central-bank/comments/page/2/

8. March 2014 at 11:11

Tom Brown,

“Mark, so I almost forgot to thank you for answering my question, which I think you did: the important quality I was looking for:…”

That’s good. I wasn’t sure because I wrote my comment on where the term “medium of account” comes from before I read your comment at “8. March 2014 at 08:38”, which is extraordinarily weird because I essentially answered the question before it was posed. (I guess I anticipated what was the core issue.)

“So what if the deposits of a nationalized bank were 100% guaranteed to always trade at par by the CB itself. Would that one step essentially CB-itize the national bank?

Rowe likes to talk about an asymmetry of redeemability between a CB and a commercial bank. So what if for a nationalized bank, this asymmetry were formerly abandoned and replaced, by law, with full symmetry?”

I think this would be sufficient to convert the deposits of the commercial bank to MOA, although technically they still would not be part of the monetary base. But keep in mind you’re asking about some very strange hypotheticals here, although I agree such questions are often highly useful when thinking about the nature of money.

8. March 2014 at 11:16

Danny, You said:

“Im pretty sure MM orthodoxy gets thrown off by a country like Australia that has no RR. For example since 1990 MB is up about 5-fold while CPI has less than doubled. P1 = P0*M1/M0 isn’t showing up in the empirical data. If V is stable in long run as I understand then I dont know how MM explains this. I could be missing something not sure where though.”

Given the equation of exchange is a tautology, isn’t the residual real GDP growth in Australia?

8. March 2014 at 11:17

Mark Sadowski,

Hat tip. Well put.

8. March 2014 at 16:30

Mark and Tom

“In a purely fiat system, as the US has had since 1971, currency is the medium of account. Moreover, since the central bank can issue currency at will, there is no constraint on the creation of reserve balances. That is why monetary economists typically consider both currency and reserve balances to be the medium of account. ”

Dollars are the medium of account right? If the commercial bank deposits and the MB have the same name “dollars” are they not both MOA? Both the fed and commercial banks have balance sheet restraints on issuance of their liabilities Im quite sure(respectively currency and deposits).

” Banks are contractually required to redeem their deposits at par value, but deposits in insolvent or illiquid banks have been known to trade at a discount (e.g. Cyprus). This cannot happen to the medium of account, as its price is fixed, and the central bank is the lender of last resort, by definition.

If Fed liabilities exceed assets or it goes bankrupt then I think it may not be able to redeem all its reserves at par either.

8. March 2014 at 17:25

Scott,

Off Topic.

JazzBumpa responded to my many responses. Here is my reply.

http://angrybearblog.com/2014/03/did-the-fed-cause-the-great-recession.html

JazzBumpa,

“This Atlantic article is relentlessly harsh in criticizing the Fed.”

Just to be clear, I would say that Matt O’Brien was very critical of many members of the 2008 FOMC, and in my opinion those members deserved such criticism. We often say “the Fed” did this or that but tend to forget the Fed is run by people. Monetary policy is in the power of the 7 Board of Governors plus 5 Fed Bank Presidents in rotation, and can only be as good as the people in those positions.

JazzBumpa,

“It points out in the graph under numbered item 1, that in July, ’08, 6 month forward expectations were for the FF rate to be higher by about 32 basis points. Directionally incorrect, sure, but can 32 basis points that have yet to materialize 5 years later bring down the entire economy? And this hard on the heels of a rate cut an order of magnitude larger? If David’s response to my comment had addressed my questions about Fed actions in 2007-8, I would have written a substantially different post, or, quite possibly, none at all. As far as I can tell, nobody else who is considering this issue has paid any attention – other than waving it away – to the fact that the FF rate was cut from over 5% to 2% in less than a year. Why do the non-actions of August and September render this irrelevant?”

As Marcus Nunes pointed out, by themselves nominal interest rates are an absolutely terrible indicator of monetary policy stance. The fact that the fed funds rate was reduced does not in and of itself make monetary policy expansionary. It needs to be compared to the neutral rate which unfortunately is not directly observable. Based on the fact that both NGDP growth and NGDP growth expectations were falling from early 2006 on through late 2008, it’s a safe bet that the neutral rate was below the fed funds rate throughout that entire time period and was itself falling.

If for example the neutral rate was 3%, dropping the fed funds rate from 5% to 4% no more made monetary policy expansionary than if it had been dropped from 50% to 40%. It was still too high causing the rate of nominal income growth to slow and bring down the neutral rate still further.

JazzBumpa,

“All your comments are very meaty, and it’s going to take some time to digest them. But I want to respond to your graph adding context to the one I borrowed from Williamson. Except for the spikes, which are brief to the point of being ephemeral, the effective FF rate was running 50 or more basis points BELOW the Fed target. As I said in the post, the Fed had lost control of the rate. And the fact that it was running low reinforces the notion that the Fed’s stance and actions were ineffective.”

The point of my version of that graph was to show that the Fed lost the ability to keep the fed funds rate at target after Lehman Brothers filed for bankruptcy precisely because the target was far too high, and after losing the ability to keep the fed funds rate at that too high target level it compounded matters by instituting interest on reserves in a bizarre counterproductive effort to hold short term interest rates up no matter what the consequences. We can be reasonably sure that these efforts were contractionary in part because every time the Fed took action to do so the stock market took another dive.

JazzBumpa,

“I don’y think aggregate demand can recover in a big way unless and until the middle and lower classes have money to spend. Fiscal policy can help, but it’s not at all forthcoming. Folks were living on borrowings for at least a decade, and that well is dry. The need for this resulted from incomes stagnating over 4 decades, while every increment of GDP growth and productivity gains went to the top. This is the sort of structural imbalance that is totally outside of the Fed’s sphere of influence.”

This sounds like you subscribe to some version of the underconsumption hypothesis, which I would suggest is a highly implausible theory. First, there’s no evidence that those with wealth or high incomes save any more out of the income that they derive from the production of new goods and services than anybody else. Second, there’s no significant correlation between national savings rates and the rate of growth of nominal incomes.

Wealth and income inequality, as undesirable as it may be for other reasons, is not an impediment to the ability of monetary policy to generate high levels of nominal income growth.In particular there are many examples of countries in the developing world where there is extraordinary wealth and income inequality and yet the growth rates of nominal income are sufficiently high to generate unhealthy levels of inflation.

8. March 2014 at 17:38

So even though deposits have the same name as currency (dollars), are used interchangeably in the economy with currency and more frequently than currency an assymetry of redeemability is what disqualifies them as MOA. Seems a bit off to me.

8. March 2014 at 18:28

dannyb2b,

“Dollars are the medium of account right? If the commercial bank deposits and the MB have the same name “dollars” are they not both MOA?”

“Dollars” are not the *medium* of account. “Dollars” are the *unit* of account. “Currency” and “reserve balances” are the *medium* of account.

dannyb2b,

“Both the fed and commercial banks have balance sheet restraints on issuance of their liabilities Im quite sure(respectively currency and deposits).”

By definition the central bank is the *lender of last resort*. The only limit on a central bank’s ability to issue liabilities are its institutional limits on which assets it may purchase.

In the case of the Federal reserve Section 14 of the Federal Reserve Act (FRA) sets out the rules governing Fed asset purchases.

According to Section 14.1 the Fed may purchase gold, Treasury debt, Agency debt and Agency guaranteed debt. The open market stipulation prevents the Fed from purchasing Treasury or Agency debt directly (that would be “monetizing the debt”) so it must buy Federal government debt (interestingly, this does not apply to any other asset the Fed may puchase) in the secondary markets. This of course has not proved to be much of an impediment.

The Fed is also permitted to purchase bankers acceptances and bills of exchange in the open market. These are privately issued assets but few American institutions use much of them anymore.

The Fed is also allowed to purchase state and municipal debt

and foreign government issued and guaranteed assets, as well as those of their agencies with a term not exceeding six months. The term constraint is important since about 99% of state and municipal bonds, and something like 88% of foreign bonds are of longer term.

So what’s eligible for purchase? Roughly…

Federal government Treasuries – $12.0 trillion

Agency bonds – $2.0 trillion

Agency guaranteed securities – $5.8 trillion

Bankers acceptances – zilch

Gold – $7.5 trillion

State and municipal bonds – zilch

Foreign bonds – $5 trillion

This comes to about $32.3 trillion dollars. Now, the Federal Reserve currently holds about $3.9 trillion in such assets so that leaves about $28.4 trillion in assets that they still haven’t bought.

(And I suppose they can buy up all the world’s foreign currency and overnight deposits which ought to be worth at least a few trillion dollars but let’s not get crazy!)

And I still haven’t touched on section 13.3 of the FRA yet.

Section 13.3 allows the Fed to lend to any individual, partnership, or corporation upon any collateral the Fed deems satisfactory. That’s the Section that allowed the Fed to create Maiden Lane I, II, and III, the Commercial Paper Funding Facility (CPFF), and the Term Auction Lending Facility (TALF) during the financial crisis. Approximately $2 billion is still currently lent out under Section 13.3 (through Maiden Lane and TALF).

In theory under Section 13.3 private label MBS, CDOs, stocks or corporate bonds are all eligible collateral so the sky is the limit. In practice section 13.3 only allows loans under “unusual and exigent circumstances.” But guess who gets to decide what consitutes “unusual and exigent circumstances?”

So yes, the Fed is legally prohibited from depositing money into the bank accounts of individuals with no strings attached, or, indeed, from buying up the global supply of cheese. But this accounting suggests there’s still ample room to issue more liabilities if the Fed so chooses.

dannyb2b,

“If Fed liabilities exceed assets or it goes bankrupt then I think it may not be able to redeem all its reserves at par either.”

How can an institution whose liabilities are the very medium of account their value is measured in go bankrupt? The very idea boggles the imagination.

Central banks cannot by definition default. The only support the Fed requires is the political support of the US that guarantees the legal medium of account nature of the dollars it issues. This political support does not require the financial support of the US Treasury, or of anyone else.

8. March 2014 at 18:35

dannyb2b,

“Dollars are the medium of account right?”

Remember, when Mark writes “currency” he means physical paper notes and coins. Regardless if those are at the bank (and thus vault cash, a component of a bank’s reserves) or in circulation, they are MOA. When he writes “reserves” this includes electronic Fed deposit liabilities owned by the banks. Those are MOA too. Bank deposit-liabilities owned by bank customers are not MOA because although they should be worth MOA dollars, they aren’t necessarily worth that much. The bank guarantees that your deposits can be swapped for MOA (currency is the only kind of MOA that non-bank private entities can own), but the CB does not guarantee they will exchange your MOA for bank deposits. And the bank may not be able to make good on it’s guarantee if it’s insolvent. That’s the asymmetric redeemability that Nick Rowe discusses in that link I provide above.

Technically, I think you might want to say that “dollars” are the unit of account (UOA). But practically CB dollars (currency and reserves) are what Scott considers to be the MOA. Things are a little more clear in a gold standard. Say $1 = 1 oz. Then “$” are the UOA, and gold is the MOA. Credit denominated in $ (i.e. bank deposits) are MOE only. The quantity of MOA as measured by the UOA can be changed by decree of the CB: they could redefine $1 = 0.5 oz for example, thus doubling the MOA by that measure (w/o any actual new gold being discovered). But UOA doesn’t really come up much here on Scott’s site, so I try to avoid using it. In fact things are really simple here, because goods which are MOE only (i.e. not MOA, like bank deposits), don’t really matter too much in Scott’s interpretation. So here on Scott’s site you can pretty much forget UOA and MOE and only think in terms of MOA. He’d probably prefer that you did.

“If the commercial bank deposits and the MB have the same name “dollars” are they not both MOA?”

By “MB” you mean monetary base, right? The answer is no. MOE can be denominated in the UOA (“$”) but it’s still not MOA.

“Both the fed and commercial banks have balance sheet restraints on issuance of their liabilities Im quite sure(respectively currency and deposits).”

Commercial banks, sure, they have to stay solvent. The Fed practically doesn’t have that problem. The Fed may have some legal restraints… I’m not sure, but practically it doesn’t: it’s not like it’s risking bankruptcy by adding more base money. A couple of fun facts to keep in mind also: paper notes stored at the Fed are not MOA any longer: they lose their face value there, since they are recorded as Fed liabilities once they are sold to banks. In that regard they are very much like personal IOUs: when your IOU comes back to you it loses it’s value. When they are sold back to the Fed, they are removed as liabilities from the Fed’s BS, and they become scraps of paper again. If they are resold to banks, they again are recorded as liabilities on the Fed BS and take on their face value again. Also, electronic Fed deposits NOT held by banks (for example, the Tsy Dept.’s TGA deposit) are also not considered to be part of the monetary base, and thus are not MOA. Coins are an oddity, in that they are assets to those entities which posses them, but liabilities to no entity. They are MOA though. The Fed buys paper notes for production cost from Tsy (the BEP), but they buy coins from Tsy (the Mint) at face value. So when coins are at the Fed, they are not in circulation, but they still retain their face value. Coins are an “obligation” of Tsy, in that Tsy must accept them back again at face value, say when they are worn out.

“If Fed liabilities exceed assets or it goes bankrupt then I think it may not be able to redeem all its reserves at par either.”

Ultimately the Fed is the responsibility of Tsy, even though it has a large degree of independence. So say some brain-dead congressmen got together and insisted on a Fed audit and determined that it had negative equity (this is possible, but not likely), they could force the Tsy to “bail out” the Fed as a political show. At least I think that could happen. I think the collective IQ of congress would have to take another 10 or 20 point or so hit before that happened though, plus they’d have to catch the Fed at a bad time, like if the bonds it owned took a big drop in value, because interest rates when up dramatically, for example. The Fed makes a lot of money generally, and though almost all of that is remitted back to Tsy, they generally don’t have any problem keeping equity at or above 0.

But it doesn’t really make sense to say that the Fed can’t redeem its reserves at par. Reserves are bank assets and Fed liabilities. In general a dollar of reserves “returned” to the Fed just means the Fed erases a dollar of liabilities from its BS. Coins excepted of course… those just become a dollar of Fed assets. Currency and reserves define what dollars are. That’s what being the MOA means. By definition a dollar of base money can’t have any other value other than a dollar. You can say MOA’s price is fixed at unity.

Now someone like Mike Sproul, a backing theory advocate, would disagree. Sumner completely rejects Mike’s backing theory though. When I put on my Mike Sproul hat, I have to think differently. To Sumner, MOA is “paper gold.” So to say the Fed can’t redeem its base money at par is like saying you can’t get an oz of gold for an oz of gold.

Some interesting alternative views to Sumner’s:

Mike Sproul:

http://www.csun.edu/~hceco008/realbills.htm

Mike Freimuth:

http://realfreeradical.com/2014/03/07/the-value-of-a-dollar/

JP Koning:

http://jpkoning.blogspot.com/2014/02/when-money-ceases-to-be-iou.html

I personally enjoy learning all those different ideas. Sumner’s view is particularly simple and easy to understand in this regard. I’m like an atheist interested in religious studies… I don’t subscribe to any of them, but I like to learn the internal logic of all. And I’ve come to believe that econ is almost more of a religion than religion itself!

8. March 2014 at 18:40

“there’s no evidence that those with wealth or high incomes save any more out of the income that they derive from the production of new goods and services than anybody else”

https://www.dartmouth.edu/~jskinner/documents/DynanKEDotheRich.pdf

Current monetary policy is imbalanced in that it confers greater benefits to those that hold more assets therefore realizing a lower MPS. Instead of creating money and evenly allocating it to people and realizing a higher MPS.

“there’s no significant correlation between national savings rates and the rate of growth of nominal incomes.”

I think that is because the fed offsets any contractionary force of higher saving.

8. March 2014 at 18:47

dannyb2b,

The Dynan, Skinner and Zeldes (DSZ) paper uses the CEX, SCF and PSID data which produce estimated aggregate savings rates in the range of 25%, 21% and 11-21% respectively over time periods (1980s) in which the savings rate measured by the BEA was approximately 8%-9% (see Table 2). The only data that even comes close to the correct aggregate measure is the PSID measure which uses an “active” measure of savings that effectively excludes capital gains income. This is not suprising because *capital gains are not, nor should they be, considered part of GDP*.

Other studies, ones that actually produce aggregate savings rates consistent with the NIPA accounts, have shown that savings rates at times have actually been inversely related to income:

http://www.federalreserve.gov/pubs/feds/2001/200121/200121pap.pdf

This study in particular showed that the savings rate of the top quintile was negative in 2000.

8. March 2014 at 18:52

dannyb2b,

“I think that is because the fed offsets any contractionary force of higher saving.”

There’s no need to. The US has one of the lowest national savings rates in the advanced world as evidenced by our persistently large current account deficit.

China on the other hand has a very high national savings rate as evidenced by its persistently large curent account surplus, and high rates of nominal income growth and inflation.

8. March 2014 at 19:02

Tom and Mark.

Im not trying to impose my ideology or antagonize for any reason just to be clear.

So what it comes down to is the definition on medium. Deposits although they are used more often as a medium for transactions than currency are not a medium.

Maybe because of the assymetry of backing? This seems to be an entirely separate issue?

Or does medium refer to something else? When I bought a car for $10000 the medium for the transaction was my deposit and the account was the number 10000 in my account. Thats how we accounted for the transaction based on the number of the deposit.

“Bank deposit-liabilities owned by bank customers are not MOA because although they should be worth MOA dollars, they aren’t necessarily worth that much. The bank guarantees that your deposits can be swapped for MOA (currency is the only kind of MOA that non-bank private entities can own), but the CB does not guarantee they will exchange your MOA for bank deposits. And the bank may not be able to make good on it’s guarantee if it’s insolvent. That’s the asymmetric redeemability that Nick Rowe discusses in that link I provide above.”

Bank deposits are worth the same. I buy a car with notes or transfer deposit, its the same. Deposits are higher risk than reserves but what about if my physical currency gets stolen?

My point is becuase my bank deposits are higher risk doesnt mean they cease to be MOA. Its a more risky medium sure.

8. March 2014 at 19:03

dannyb2b,

In the largest, and by most accounts, best study to date on the question of inequality and national savings, by Schmidt-Hebbel and Serven (2000), involving World Bank data on 82 countries over 1965-1994, they generally found no significant correlation between measures of income inequality and national savings.

The lone exception was in a regression that used the income share ratio of top 20% to bottom 40%. The correlation was significant at the 5% level, but was negative. In other words, it suggested that greater inequality resulted in lower national savings.

http://darp.lse.ac.uk/papersdb/Schmidt-Serven_(JDE2000).pdf

8. March 2014 at 19:07

Is there any circumstances where the MOE deposit is traded at a different price to the MOA currency for any goods or service? For example Is there any legitimate market where you have to pay more for an item if you pay in deposits as opposed to cash. If not Im pretty sure deposits are both MOE and MOA.

8. March 2014 at 19:11

… to be clear, Mike Sproul would not disagree that a dollar of base money is always defined to have a dollar’s worth of value. But he would argue that the value of the $ itself ultimately arises from the assets the CB holds. Even if it holds mostly Tsy bonds (i.e. promises to pay more $), as long as it holds some “anchor” assets this works out in his logic. He explains it here:

http://jpkoning.blogspot.com/2014/02/the-cost-of-manufacturing-liquidity.html?showComment=1392652641149#c2747714437021819015

Implicit in his view is that there’s some “reflux” channel through which holders of CB liabilities could ultimately redeem their notes. Like if the CB were to be liquidated for example.

It’s a simple view… but still it’s hard to beat the simplicity of Sumner’s “paper gold” view!