The real problem is a lack of nominal targeting

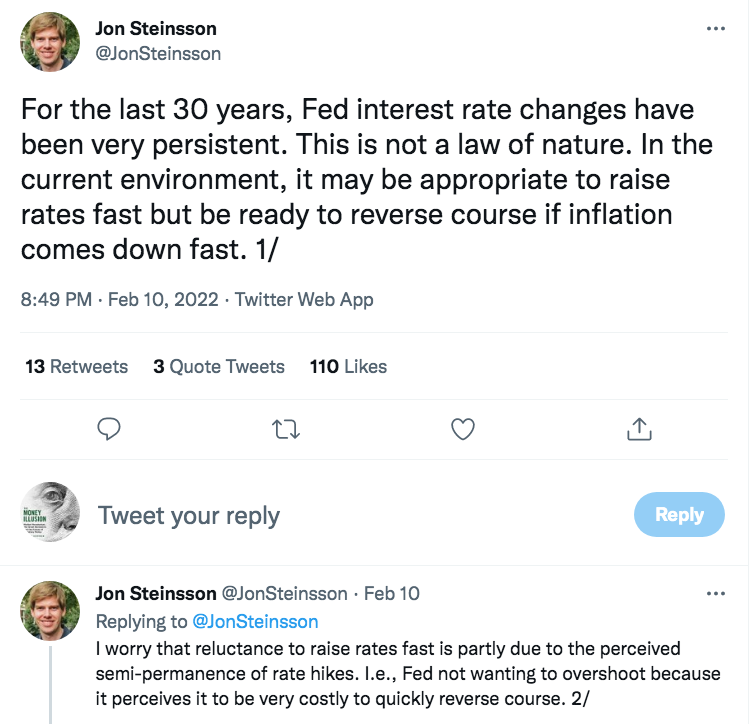

This tweet is correct, but tells only a part of the story:

I’ve made the same point many times. This is why I’ve been advocating treating the fed funds target more like a market price. I’ve argued that this rate should be adjusted daily to the nearest basis point at the median vote of the FOMC (voting by email if necessary). Under that system, policy “reversals” would occur frequently, and would be seen as normal, not embarrassing.

Nonetheless, the current debate about where the Fed should set interest rates mostly misses the point. The Fed needs to set a clear nominal target, and then stick to it. Where do they want the PCE price index to be in January 2025? Or better yet, where do they want NGDP to be in three years? That would do far more to stabilize the economy and prevent recession than any tweaking of interest rates. The economy is currently being destabilized by abysmal communication out of the Fed. No one seems to know if they are still committed to FAIT, and if so what that means. So tell us!!

PS. I have a new article at The Hill that provides three reasons why the Fed screwed up in the second half of 2021. Please read the whole thing.

Tags:

13. February 2022 at 10:16

Can the Fed credibly commit to meet any target of any kind? They didn’t do so during the end of the Bush years and the Great Recession, and they haven’t done so in the wake of the pandemic. I suspect that if they really wanted to, they could hit some kind of target. That they consistently miss their stated target I interpret as an indication that there is something that the Fed values more than meeting its target. Is there something structural wrong with the Fed that incentivizes voting members to choose policies that take them off target?

13. February 2022 at 10:56

“there something structural wrong”.

– You mean “structurally wrong”.

“I suspect that if they really wanted to, they could hit some kind of target”.

– Yes, el estupido, if you throw the ball in any direction you will hit “some kind” of target – just probably not the one you hoped for.

“something they value more than meeting their target”.

– It has nothing to do with “valuing something more”. There is no “hidden agenda”. They simply miss the target because planning the supply of money is not a science. It’s a pseudoscience where quacks include their emotions and hunches.

This country is totally fucked. We have idiots in academy, and idiots in government. My parents left the Soviet Union for these idiots. They should have gone to Poland or Lithuania.

13. February 2022 at 14:35

Lizard, That’s what my Hill article is about.

13. February 2022 at 14:42

View on this article Scott?

https://economicsfromthetopdown.com/2021/11/24/the-truth-about-inflation/

13. February 2022 at 15:13

Kester,

That’s a really long article, but I can’t sample a section of it that isn’t ill-informed, rambling, pretentious, or some combination of the three. Not recommended reading.

13. February 2022 at 15:42

Yglesias linked to that Steinsson post in his twitter feed. I sense a conspiracy–even Dean Baker is expressing concern about the CPI numbers and suggesting that QE isn’t necessary–the conspiracy is deep!

I really like your suggestion that the Fed vote daily on rate changes. Their meeting schedule seems embedded in prehistoric notions of transportation and information gathering. The March meeting will probably feature a 25 basis point hike and some mushy platitudes about organic returns to historical trends. You and Yglesias will be justifiably upset about this because unstable monetary policy will lead to bad political outcomes.

Will Trump appoint hawks to the Fed in 2025?

14. February 2022 at 04:18

Wow, reading those comments on the Hill article was definitely a mistake. Half the people seem to think inflation is caused by greedy corporations price gouging, and the other half think its caused by fiscal policy….

Regardless, do you think part of the Feds reluctance to tightening monetary policy is because their tools for fighting inflation are weak and causes unintended side effects?

Or is it that they’re just being overly cautious here?

14. February 2022 at 06:17

Using a price mechanism, pegging policy rates, to ration Fed credit is non-sense (“a price mechanism is a system by which the allocation of resources and distribution of goods and services are made on the basis of relative market price”).

The effect of current open market operations on interest rates is indirect, varies widely over time, and in magnitude. What the net expansion of money will be, as a consequence of a given change in policy rates, nobody knows until long after the fact. The consequence is a delayed, remote, and approximate control over the lending and money-creating capacity of the banking system.

14. February 2022 at 06:31

Is it just in the nature of people who rise to the top of the Federal Reserve to want more discretion than is allowed by slavish obedience to something like an NGDPLT rule?

14. February 2022 at 07:34

Kester, A waste of time. Stop sending me that sort of garbage.

Mike, No, their tools are very powerful.

Carl, They are well intentioned, but in some cases I don’t think they fully understand the implications of monetary theory. I can’t see Bernanke or Yellen making this mistake (although they might make other mistakes.)

14. February 2022 at 07:48

The Fed isn’t raising interest rates because they know, deep down, that it will simply make the problem worse.

If you have a step-by step mechanism by which handing out vast sums of government money to banks reduces the amount of spending, then I’m all ears. But there isn’t one. Not with the current structure of our economies.

If the argument holds that if wages go up, prices will go up, then when interest rate costs go up, prices will go up similarly – for the same reason. And that just fuels inflation – because interest rate rises is just a private sector transfer. Those receiving the transfer will spend their earned interest on the higher prices – confirming them.

Raising interest rates doesn’t work. What actually does the work is taxation drag. Hence why monetary policy allegedly takes a year or more to work.

What mainstream expects interest rates to do is reduce the amount of spending. What you’ll hear is that “Monetary policy works with a lag – typically 12 months or more – so decisions today set our fate next year”. What that tells you is that it isn’t interest rates that are doing the work. It is something else.

That something else is taxation. Specifically increased tax take without offsetting additional government expenditure. That causes fiscal drag and will remove money from the economy relative to the level of activity within the economy. The more active it is, the more tax is raised because that’s how percentages work.

Therefore if government holds station, and preferably refuses to buy anything except at last year’s price, then demand will be quashed down to the level of supply we have. And that will take the same time as ‘interest rate rises’ to work, because it was always taxation drag doing the work.

It will involve job losses and an increase in unemployment. Unemployment is the current buffer stock that stops people asking for higher wages – because they are scared they will be replaced by somebody on the unemployment queue.

MMT would replace that with a Job Guarantee, so that nobody loses their job. They just transition to one with a lower wage when the unsustainable excess private sector operations are eliminated by the fiscal squeeze.

As it stands though, unemployment, a higher tax take and constrained government spending is the cure – as it always has been, and always has to be. Except Government likes to pretend the central bank does the dirty work.

Central Banks raising interest rates has always been a Wizard of Oz routine. MMT prefers to look behind the curtain.

14. February 2022 at 07:49

The MMT analysis is that there is always a buffer stock that provides the counterbalance, and it is that which offsets ultimately offsets inflation, not anything else. Certainly not messing with interest rates.

The analysis shows that an employed buffer stock is a superior price anchor to the existing unemployed buffer stock.

Similarly MMT shows that interest rate rises are the cause of inflation (the academic inflate bit, not the price changes because of lack of supply bit), and that the natural rate of interest is zero. Therefore interest rate setting is an artificial market intervention that doesn’t work and should be abandoned.

Similarly the view that banks should be regulated on the asset side – via the quality of their loan book, rather than the liability side – via the Basel nonsense is a policy that arises from understanding how banks work.

14. February 2022 at 07:49

In which case we would just see a Job Guarantee in place, and rather than PAY-FOR we have a principle of PAY-NO-MORE-FOR – a blanket refusal of government to accept price rises on the things it buys and a suspension of any programme where suppliers try to raise prices.

Then the elimination of federal taxes down to perhaps a couple – a property tax and a progressive tax on employment borne by employers.

Beyond that legislators need to understand that they can’t buy anything unless they’ve made it unemployed with taxes first.

What MMT people have failed to do is ask the question – who gets to have less stuff now the supply side has been hit. Messing around with interest rates won’t help that process. Somebody has to take the loss though.

14. February 2022 at 07:52

Scott, what is your view on georgism and the land/location value tax. Do you agree with the Georgists that the surroundings/whole of society give locations their value – none of it landowner’s effort?

Why should landowners collect or enjoy all that land rental value (excluding buildings), when the whole of society creates land rental values? Local taxes replaced by greater central government grants. If due to inaccurate valuations rate goes over 100%, starts to tax the buildings.

Increases in government spending (and cutting other taxes) increases the rental value of the land, so is self-financing with a 100% land value tax in place. This was proven by Joseph Stiglitz in his ‘Henry George theorem.’ The initial revenues will substantially improve the deficit.

14. February 2022 at 07:53

https://en.wikipedia.org/wiki/Henry_George_theorem

14. February 2022 at 08:09

As Dr. Philip George says: “When interest rates go up, flows into savings and time deposits increase.” I.e., transaction deposits are shifted into savings’ deposits — even as the volume of bank deposits remains unchanged.

The expansion of time/savings deposits in the payment’s system adds nothing to GDP period. Banks pay for their earning assets with new money, not existing deposits. The DFIs’ savings deposits have a zero payment’s velocity.

The lending capacity of the payment’s system is determined by monetary policy, not by the savings practices of the nonbank public. The commercial banks could continue to lend even if the nonbank public ceased to save altogether. The lending capacity of the payment’s system is a function of the velocity of its deposits, it is not a function of its volume of deposits.

14. February 2022 at 08:20

The demarcation of increased velocity, due to increased interest rates, peaked in the 1st qtr. of 1981.

Thus, the saturation of DD Vt (end game) according to Corwin D. Edwards, professor of economics. [Edwards attended Oxford University in England on a Rhodes scholarship and earned a doctorate in economics at Cornell University. He spent a year teaching at Cambridge University in England in 1932. He taught at New York University in 1954, the Chicago School from 1955-1963, the University of Virginia, and the University of Oregon from 1963-1971.]

Edwards: “It seems to be quite obvious that over time the “demand for money” cannot continue to shift to the left as people buildup their savings deposits; if it did, the time would come when there would be no demand for money at all”

14. February 2022 at 09:01

Kester,

Interest rates can rise for multiple reasons. If it’s due to a tightening of monetary policy, then it does work, and there is usually little-to-no lag of effect, though there is usually a relatively gradual effect on inflation itself. We saw this in the US during the Volcker years: RGDP growth/contraction fluctuated wildly and quickly with changes in monetary policy. In contrast, inflation followed a relatively steady decline from mid-1980 to mid-1983.

In the (market) monetarist view, interest rates are not where the action is happening. They change in response to the same policy decisions and exogenous forces that cause changes in NGDP, short-run RGDP, and inflation.

14. February 2022 at 09:24

The FOMC has no idea what they are doing. re: “zero net purchases by March 2022”. How does that translate into pegging interest rates?

14. February 2022 at 09:24

Will Sumner apologize for five years of propogating the DNC’s Russia hoax, now that Durham has filed charges against the Clinton Campaign for hiring hackers to spy on Trump, then funding a frivilous study in an effort to make it appear like she was connected to the big bad Russians?

All you have to do is whisper “russian” and the American people freak out.

Just ask Sumner. He’s probably writing his blog from a panic room.

14. February 2022 at 09:40

I don’t doubt their intentions. I just wonder how Bernanke can make the following statement

without fearing a seemingly obvious follow-on question of why he didn’t just focus on a simple metric of price stability, unless he knew that his listeners and he believed they knew things that could not be expressed in such a metric.

https://www.federalreserve.gov/boarddocs/Speeches/2003/20030203/default.htm

14. February 2022 at 10:05

What is the level of R * associated with 4% or 5% N-gDp?

15. February 2022 at 06:31

Goldman Sachs just slashed their GDP growth rates for 2022.

“Specifically, the bank slashed its Q1 GDP forecast from 2.0% to just 0.5%,”

What level of interest rates will keep it from falling?

15. February 2022 at 07:09

GDPNOW is at .7 growth for this quarter (Feb8). Do we really want to tighten? Maybe, as wholesale inflation rose 1% in January. This used to be called stagflation. It is as if the Fed has no ability to get what it wants. What is going on?

15. February 2022 at 07:19

PS—although job creation is high—so not really stagflation. I really don’t understand what is happening——not why—but what.

15. February 2022 at 09:54

We’ve once again got FOMC schizophrenia: Do I stop because inflation is increasing? Or do I go because R-gDp is falling?). If it pursues a rather restrictive monetary policy, e.g., QT, interest rates tend to rise.

This places a damper on the creation of new money but, paradoxically drives existing money (savings) out of circulation into frozen deposits (un-used and un-spent, lost to both consumption and investment). In a twinkling, the economy begins to suffer. 2018 is prima facie evidence.

15. February 2022 at 10:09

All monetary savings originate within the payment’s system. The source of interest-bearing deposits is non-interest-bearing deposits, directly or indirectly via the currency route (never more than a short-term seasonal situation), or through the bank’s undivided profits accounts.

I.e., transaction deposits have been shifted into savings deposits, savings deposits with a zero payment’s velocity. The solution to FOMC schizophrenia is to drive the banks out of the savings business, which doesn’t reduce the size of the payment’s system. Savers never transfer their savings outside the banks unless they hoard currency.

There is just an exchange in the ownership of pre-existing deposit liabilities in the banking system, a velocity relationship. Where do you think velocity has gone since 1981? Savings have become increasingly impounded and ensconced in the payment’s system (a global problem, reflecting Alvin Hansen’s secular stagnation).

There has increasingly become a larger proportion, and or a larger volume of savings, being continually held in payment systems. An increase in bank CDs adds nothing to N-gDp.

In the context of their lending operations it is only possible to reduce bank assets, and deposits, by retiring bank-held loans, e.g., for the saver-holder to use his funds for the payment of a bank loan, interest on a bank loan for the payment of a bank service, or for the purchase from their banks of any type of commercial bank security obligation, e.g., banks stocks, debentures, etc.

The NBFIs, e.g., hedge funds, insurance companies, pension funds and shadow banks are the DFI’s (regulated member banks), customers. The DFIs process all of the NBFI’s underlying payment transactions, both clearings, and settlements. The prosperity of the DFIs is dependent upon the prosperity of the NBFIs. Negative interbank demand deposits won’t get the banks to lend without an increase in bankable opportunities.

15. February 2022 at 12:35

https://twitter.com/jordanbpeterson/status/1493681085858951174?cxt=HHwWjMC9pZTCz7opAAAA

And finally, the Danish government breaks from Sumner and his band of civil liberty violaters.

It’s time to stop your misinformation campaign Scott.

15. February 2022 at 14:25

@Michael R and others:

The reason this particular cycle is so hard to figure out is it’s really unique compared to the past. This isn’t a normal cycle, it’s the first time ever we literally shut down the economy on purpose. So now it’s trying to restart and the process for how that happens is pretty difficult to figure out, as we’ve never done this before.

16. February 2022 at 07:22

When there are rising prices people are going to spend what they earn because they need it to buy things they need. And that’s why interest rates don’t work when you have cost push inflation on items with inelastic demand – as we have now with gas. Nobody is going to be doing the increased saving you are relying upon.

The opposite is the case. Interest rate increases government sector spending, via interest rate payments on reserves, which puts more money in the system and *causes* inflation – both by direct injection and by making the future price of money more expensive, which then feeds into the cost of goods and services. Turkey being the current poster child for that problem.

As usual with mainstream theory fans, you have it entirely backwards.

16. February 2022 at 11:25

I think the “original sin” happened at the point when they decided to abuse the English language rather than be upfront about their goals and orientation.

The plain language meaning of “stable prices” means that they don’t have the authority to pursue inflation for its own sake, even though they clearly want to. But instead of saying something honest, like “we’re not going to seek complete price stability because we think it’s bad for employment long-term,” they chose to start speaking as if “price stability” means 2% (or *at least* 2%) annual price increases.

This abuse of language led to further abuses of language and the steady stream of illogical and/or incomprehensible statements we’ve heard over the past year, namely: the conveniently vagueness of the word “transitory”, Powell’s “what we really mean by inflation is a continuing process”, his apparent failure to understand the meaning of “average”, the constant incantations of how “nimble” and “data-dependent” they are as they passively ignore data month after month, and Mary Daly’s prizeworthy “We didn’t have price stability in the 2010s because there wasn’t enough inflation, but by any measure we’ve had price stability during the pandemic”.

It’d be like a cult that redefines monogamy to mean “two affairs per year” and a cult leader who tells followers “You broke your marriage vows because you didn’t have any extramarital liaisons this year.”

It’s a fundamental truth of human nature that nothing good comes from abusing language in that manner.

17. February 2022 at 11:40

– The FED does have a “target”. They follow the 3 month T-bill rate.

17. February 2022 at 14:03

The 4,300+ banks, as a system, act like one bank. One bank that pays for the deposits it already possesses. It thereby compensates for these higher unnecessary costs with higher risks. The perverse competition causes consolidation, forces economies of scale, and results in discrimination against smaller loans from lower income borrowers.

Banks can’t attract more deposits by paying interest to saver-holders, as deposit growth is dependent entirely on monetary policy. Deposits grow as the Central Bank expands the loan pie.

It’s stock vs. flow. The system operating under the deregulation of interest rates, destroys the velocity of circulation. As interest rates rise, more deposits are shifted into stagnant savings, bottling up savings, reducing money velocity. Bank-held savings have a zero payment’s velocity. Banks don’t lend deposits, deposits are the result of lending (the exact opposite of an intermediary).

17. February 2022 at 14:23

Jeff, Congress gave the Fed a dual mandate, and the Fed believes that requires positive inflation. I suspect that Congress feels the same way.

That may or may not be true, but it’s hardly dishonest. If Congress wanted a zero percent inflation rate for the CPI, they should have said so.

17. February 2022 at 19:22

While this is from Sumner’s Greatest Hits collection, it is very good, nonetheless. This is part of the direction of future monetary policy.

18. February 2022 at 09:06

I understand the dual mandate—given that there is likely some trade-off between unemployment and inflation, the Fed is supposed to sacrifice some price stability for growth and jobs. That seems fairly straightforward. My interpretation of the 2012 and subsequent statements buntil recently was that they viewed the optimal trade-off as generally lying at around 2%.

What seems to be new in the past few years is that they are talking as if positive inflation is required by the stable prices mandate itself. I don’t know the reason for this change—maybe they are trying to provide some cover for single-mandate banks who are also trying to stoke inflation? In any case, Powell and some others often seem to speak as if the stable prices mandate is essentially equivalent to AIT at 2%. This seems to me a clear erosion of the mandate and a slippery slope, since it gives the impression that the 2% is table stakes, if you will, and they are required to seek even more inflation when there is any employment concern. And because the “averaging” in AIT is so poorly defined, it opens the door for more dovish members to pursue a near-total evisceration of the stable prices mandate. Mary Daly is on record with Reuters last month saying “You could pretty much use any averaging period you could consider, and you would find that we have achieved our two-percent averaging.” Complete nonsense, but hardly unexpected once the majority has conceded that “0=2”.

20. February 2022 at 11:48

I just saw this interview from Charles Evans last Fall: https://bcf.princeton.edu/events/charles-evans/

At the 34 minute mark, he starts describing what he thinks “FAIT” means. It sounds like the algorithm is:

1) if inflation is ever 1.9% or less, do whatever it takes to generate a significant upward shift in the price level

2) there is no obligation to compensate even for large inflation overshoots. Only if inflation expectations are persistently above 2.5% should you tighten to bring them down

3) additionally, disregard any positive inflationary contribution from “supply shocks” (the interview is unclear on how disinflationary or deflationary supply shocks should be handled)

This has nothing in common with the mathematical concept of “average” and if implemented could reasonably be expected to generate average inflation much higher than 2%, so I think it is fair to say that describing this as “FAIT” was an abuse of language. If this is what they have in mind by “average inflation targeting” then their earlier official statements were quite misleading and I’m surprised a lawyer like Powell would have allowed them to be issued.

25. February 2022 at 15:35

Scott, in the Hill piece you ask “why wait so long? Why set a target interest rate of zero and continue quantitative easing when the economy is booming and inflation is running near 6 percent?” You don’t mention the December 2020 forward guidance, specifically the “maximum employment” language. Genuine question: Do you think that

(1) tighter policy in 2021 would have been consistent with the Dec 20 guidance,

(2) FOMC should have tightened more in 2021 although this was inconsistent with the Dec 20 guidance, or

(3) policy was appropriate *given* the Dec 20 guidance, but this guidance itself was poorly designed/unnecessary/should be unnecessary under a well-designed targeting regime?

Thanks.