Still crazy after all these years?

Here’s Alexander Humboldt:

First they ignore it, then they laugh at it, then they say they knew it all along.

In late 2008, I wrote op eds saying that tight money was driving the US into recession. No newspaper was willing to publish them. Then in early 2009 I started a blog, and people laughed at my claim that money was very tight. “How can that be, with ultra low rates and all the QE.” It was difficult to find anyone who agreed with me—until today. Now it looks to me like Paul Krugman agrees with me. This is from a recent post entitled, “It’s Getting Tighter.”

When thinking about the market madness and its possible real effects, here’s something you “” where by “you” I mean the Fed in particular “” really, really need to keep in mind: the markets have already, in effect, tightened monetary conditions quite a lot.

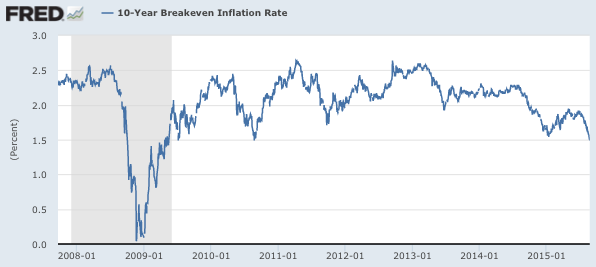

First of all, if break-evens (the difference between interest rates on ordinary bonds and inflation-protected bonds) are any guide, inflation expectations have fallen sharply:

Why only go back to 2011? Let’s see what monetary policy was like in late 2008:

Now that’s tight money!

Now that’s tight money!

Krugman continues:

Second, while interest rates on Treasuries are down, rates on private securities viewed as even moderately risky are up quite a lot:

Again, that makes me wonder what real borrowing costs looked like in 2008:

Now you might argue that this isn’t really tight money. Good borrowers could still borrow cheaply in 2008. It was default risk. Nope, good borrowers couldn’t borrow cheaply, as liquidity had dried up. How do we know? While yields on conventional Treasuries fell sharply, the real yield on TIPS soared higher during the second half of 2008. The 5-year TIPS yield soared from 0.57% to over 4%. There is no default risk with TIPS, it was purely a liquidity story. Because of the Fed’s tight money policy, liquidity had dried up:

Just to be clear, real interest rates are not a good indicator of whether money is easy or tight. But the spike in BBB yields was not just a default risk story; it was also a liquidity story.

Just to be clear, real interest rates are not a good indicator of whether money is easy or tight. But the spike in BBB yields was not just a default risk story; it was also a liquidity story.

Over at Econlog I have a post discussing a related issue, could a quarter point interest rate increase later this year do great harm?

I suppose we attach the label ‘crazy’ to people who believe things that are not socially acceptable and seem irrational. Now that a Nobel Prize winner is making similar claims, I guess I can’t claim to be crazy any longer.

Tags:

26. August 2015 at 11:45

Good post, looks like maybe the Fed is about to face another test…

26. August 2015 at 11:46

So TIPS yield rising, shouldn’t that indicate higher inflation concerns and thus “looser” money. (Sorry for such a novice question). Or is it that government is looking for liquidity and thus must offer more attractive yields to get it.

26. August 2015 at 11:51

I’m assuming that real yields = inflation + market rate…inflation is low, but market rate in an illiquid market is much higher.

26. August 2015 at 11:57

What did it look like back in say 1960s and 1970s when one main earner in a factory job in the US could make enough to support his family in a good lifestyle?

For me 2000 onwards was a sick joke. Graphs back to 2007 are like asking Brando about things after he went mad.

26. August 2015 at 12:39

Maybe you should have done it PK’s way. Rather than say (counterintuitively to the then-current mindset) that money was “tight” to say that is needed to be “more loose” or that the Fed should be lowering rates or buying LT assets or whatever or charging interest on reserves.

26. August 2015 at 12:39

When you are driving 100 mph into a wall, and slam on the brakes just before impact, you don’t claim the brakes caused the accident.

…

It’s the old story — was 2008 a liquidity issue or a solvency issue? If you believe the Fed can rescue everybody, then it’s always a liquidity issue and the answer is easy money always.

26. August 2015 at 12:57

Pras, No, the TIPS bonds are indexed, so it’s a real interest rate.

Thomas, You said:

“Maybe you should have done it PK’s way. Rather than say (counterintuitively to the then-current mindset) that money was “tight” to say that is needed to be “more loose” or that the Fed should be lowering rates or buying LT assets or whatever or charging interest on reserves.”

No, that’s not the way Krugman did it in 2008, that’s the way I did it, and a few other market monetarists. Krugman was saying there’s nothing the Fed could do, they were out of ammo. Who was the first person to publish a paper advocating negative interest on reserves?

Charlie, I see the loonies are out today. That comment is so far off base I won’t even try to set you straight. It would be pointless. If you are not interested in an intelligent conversation, then what’s the point of spending time commenting here?

26. August 2015 at 13:15

I stand by what I said.

Money was extremely loose leading up to the crash, loose money being defined that loans were easy to get and the volume of loans was steaily increasing, especially consumer credit, mortgages and mortgage derivatives.

Money began to get tight before the crash because lenders realized that many of those loans, especially in the MBS market, were in danger of defaulting and could not be traded. So money got extremely tight.

So the collapse in lending — tight money — was the *result* and not the *cause*.

Your argument is basically that the Fed should have intervened right then and there, and not waited, in order to keep the lending going. It’s hard to see how it could have done that, without buying MBS and other bad debt earlier and more aggressively.

26. August 2015 at 13:34

Charlie

I think you are new here. You need to take Scott’s course on Money first. Scroll down the right hand side for the link. And then submit an essay on: What is the difference between money and credit?

26. August 2015 at 13:37

It is amazing to see Krugman adopt the language of Market Monetarism. Better late than never. He might even start thinking fiscal policy might be done via tax cuts next. Or will hell freeze over first?

26. August 2015 at 13:38

Charlie Jamieson: Your mindset is also cast in bronze!

https://thefaintofheart.wordpress.com/2015/08/26/a-mindset-cast-in-bronze/

26. August 2015 at 13:39

James: money equals credit. Surely we don’t need another essay on that!

26. August 2015 at 13:56

Marcus, do people still believe in the Phillips curve, or do they pretend to believe in the Phillips curve because the Fed pretends to believe in the Phillips curve?

26. August 2015 at 14:59

Charlie Jamieson,

The Phillips curve should have been put out of its misery decades ago. It has been consistently wrong ever since it was discovered. In fact, I would put it as a the poster child of the “Lucas Critique.” As soon as policy makers started to use the Philips curve as a mechanism to guide policy, the relation between prices and unemployment broke down.

Yet we still talk about it.

I don’t believe that the Fed could have prevented the recession in 2008. There was clearly too much in the way of bad loans out there, and banks needed to readjust the books. That doesn’t mean that the Fed was late in realizing the magnitude of the problem. Or that money isn’t tight today.

26. August 2015 at 15:37

@scott

No. TIPS spread were not a liquidity story. As I have noted the embedded option in TIPS causes artifacts in pricing. These become particularly pronounced if inflation expectations have dropped and the remaining maturity of the bond is relatively short (in which case the embedded option has less impact on price). Because of the way the Fed constructed the TIPS index this finally became obvious even to the “genius” economists at the Fed when the TIPS index spiked in October of 2008. On December 1, 2008, the Fed changed the way it constructed the index. This resulted in a one day change in the TIPS index from over 4% to under 2%. The 2008 jump in the TIPS index had nothing to do with liquidity.

26. August 2015 at 15:42

Well, maybe I will become socially acceptable too.

I have been arguing for years that the world’s central banks need to shoot for Full Tilt Boogie Boom Times in Fat City, let the good times roll for a long while and then make a decision of what to do slowly.

Print more money baby, and a lot of it.

Or would you prefer the Fed keep the PCE at about 1.2% and talk about raising rates? And, by the way, suffocate the world economy as the monetary superpower.

26. August 2015 at 15:55

@Scott,

Also…the bid offer spread is the measure of liquidity. Yield is the measure of risk. You need to be careful not to confuse the two.

26. August 2015 at 16:38

No, liquidity has not dried up because money from the Fed has become too tight, it is because real coordination has become distorted in the present because of too much credit in the past.

More credit expansion will only make the problem worse. The Fed has already distorted the economy to such a degree that the needed corrections today significantly dwarf those from 2008.

Sumner is advocating for hurting more people.

26. August 2015 at 17:41

Scott, congrats. Maybe pressure from the academic community will encourage Yellen to postpone the rate hike.

To the MM haters: There’s no reason to allow deflation to set in. When the supply or demand of steaks change you see that reflected in the price of steaks. If the supply and demand of money changes, you see that reflected in all prices. If you want to avoid discoordination then you want to stabilze total spending so that individual prices convey as much information about supply and demand as possible.

26. August 2015 at 18:01

Sumner: “Now you might argue that this isn’t really tight money. Good borrowers could still borrow cheaply in 2008. It was default risk. Nope, good borrowers couldn’t borrow cheaply,…”

– flat out wrong by Sumner. Go to my ‘blog’ raylopez99.blogspot.com, click on the upper right graphic, entitled ‘Credit Default Spreads Peaked in early 2009 not 2008!’. This shows also btw that the bailout of fall 2008 was unnecessary, as it did not stop the default risk panic.

Sumner builds his logical structures on faulty foundations of sand. An economic Ozymandias… “Round the decay Of that colossal wreck,…The lone and level sands stretch far away”.

PS: MF and dtoh also pick up on Sumner’s sleight of hand I see.

26. August 2015 at 20:34

Scott, when I read that on Krugman’s blog I thought of you… I wondered why you didn’t jump on that one immediately. I guess a day later isn’t too bad.

Regarding Nobel laureates, however, if history is any guide, there’s no guarantee of avoiding craziness.

26. August 2015 at 23:01

O/T: Scott, what do you think of this self-proclaimed “center-right” group and their views on monetary policy, and their line up of speakers at Jackson Hole the next three days?

Do you suppose they really are any more “serious” than this guy who wants to enslave illegals?

BTW, I’m working on a way to heal the rift and sell that to the “serious” center right folks: a WSJ editorial. I’ve got the title worked out:

“A modest proposal: it’s time for we Americans to step up and take ownership of our illegal immigrant problem. Literally.”

Well, you gotta admit, it’d pretty much blow the bottom out of the “minimum wage” concept, so how hard a sell can it be??

26. August 2015 at 23:02

… H/T Brad Delong.

27. August 2015 at 02:11

‘The FED is out of ammo’ is not equivalent to ‘money was not tight’.

Paul Krugman always spoke and speak of the timidity/credibility trap. See his 98 paper on Japan. He believes in forward guidance but he also thinks that the FED cannot commit to do that (because of political pressures I guess). And as off now, he’s been right: the FED is expected to increase the rates soon whereas forward guidance would need the FED to keep the rates low for an extended period ‘of time even after the economy is out of the crisis.

27. August 2015 at 03:36

Why are you agreeing with Krugman’s reasoning from a price change?

27. August 2015 at 04:13

Charlie Jamieson @ 13:15 gets it right. What Sumner is saying is the Fed should have spotted the popping of the credit bubble and fixed it before it exploded. Of course that is impossible as the problems of the credit bubble were already baked into the economy.

And Ray @ 18:01 also gets it right. The worse of the financial pain was in 2009, not in 2008. The panic of 2008 was a well orchestrated political drama to empower the government to bail out Wall Street. Treasury Secretary Henry Paulson knew exactly what his job was and he nailed it. Pay no attention to the fact the guy got everything wrong. He got his clients the bailout they needed.

27. August 2015 at 04:34

@Tom Brown,

Please don’t bring up immigration. There are enough cranks commenting here already. Discussions about immigration will bring a whole nother level of craziness.

27. August 2015 at 04:45

I think everyone is panicking a little bit over the drop in inflation breakevens. The market has been a little wacky lately and also the inflation calculation includes oil prices, which are down by about 1/3 since June and are at their lows. IMO, this is just a typical market overreaction going from ‘we’re at peak oil and oil prices are never going down’ to ‘oil prices are never going up’. Time will tell and it’s hard to figure out exactly what’s going on, but it seems waaay too early to call this tight money that’s going to drive the economy into a recession. I think we all need to take a breather here.

27. August 2015 at 05:55

James, That’s the problem, he has commented here before.

dtoh, Then what were TIPS yields in late 2008? Can you show me the graph? I’m aware of the option feature, but remain skeptical of the claim that real interest rates did not rise.

Regarding liquidity, how do you explain the difference in yields between 29 and 30 year bonds? Surely it’s not default risk?

Tom, Given that I was invited to speak there, I think we can assume it’s a high quality group. As far as DeLong, he’s a brilliant blogger but when he gets into politics he becomes . . . Krugman-like.

M., Yes, I’m well aware of the many contradictions in Krugman over the years, and have blogged on it dozens of times. And yes, I’ve read his 1998 paper, and indeed in a 1993 paper I pointed out that temporary currency injections were ineffective.

Dan, No that is definitely not what I’m saying, and please stop lying about my views.

Charlie, you’ve been here before so I assume you know enough to ignore Dan.

27. August 2015 at 07:42

Dan W. … it might be argued that the Fed’s ‘loose money’ stance to the financial sector cause money to be very tight for the consumer (who faced bankruptcy and the loss of his home) and the worker (who lost his job or saw reduced wages).

Faced with the choice of saving the wealthy or the working class, the Fed only had the tools to save the wealthy (who have access to Fed bailouts).

Instead of talking about loose money or tight money in general, it would be better to take it a step further and measure where the money is going. Right now money is loose at the top and tight at the bottom.

Policy makers assumed that turning on the spigot at the top would cause the money to flow downward, but this has not happened. I suspect this is because it’s easier to make money in financial assets than it is to make real investments.

27. August 2015 at 07:43

Scott,

You can look at the data below. On December 1, 2008, the Fed changed the basis for calculating the index. On the day of the adjustment, the index fell from 4.17 to 2.03.

Data set is here: http://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=realyieldYear&year=2008

(You can find a brief description of the change in the footnotes.)

http://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=realyield

27. August 2015 at 08:00

“Tom, Given that I was invited to speak there, I think we can assume it’s a high quality group.”

Hahaha!… I didn’t know. Are you going? Is it a debate? Won’t the crowd feel a strong sense of cognitive dissonance hearing your thoughts on monetary policy after hearing the head-liners expound on the same subject? Oh, for example, say Peter Schiff?? Lol

27. August 2015 at 08:04

@Jeff, the genie’s not going back in the bottle this time. The WSJ crowd will have to find a way to accommodate “the base.” Lol… I’m merely suggesting a way forward: common ground so to speak. Lol.

27. August 2015 at 08:07

dtoh, You are beating a dead horse. I know all that, I’ve blogged on it. My request was that you provide the correct data, or at least the most accurate data we have for real interest rates in 2008. Please provide a link to the corrected data.

Tom, I was not able to make it this year, maybe next year.

27. August 2015 at 08:08

Tom, One other thing. I often present my views at “hard money” crowds and am always very well received. They are not the caricature that DeLong makes them out to be.

27. August 2015 at 08:38

With all the talk about the impending/possible fed funds rate increase next month, I hear lots of people say “its about time they raise rates, we cant have rates this low for this long” or “this low fed funds rate is causing distortions”. In your view, does it really matter what the fed funds rate is? Is it irresponsible to say “who cares if fed funds is 0.25 for the next 30 years”?

I read only periodically so forgive me if you’ve already covered this question.

27. August 2015 at 09:12

Scott,

Just to follow up:

1. Real rates probably did not start to rise until January of 2009.

2. You are correct in saying that “real interest rates are not a good indicator of whether money is easy or tight.” Borrowing costs are NOT what’s important. The amount that is actually borrowed is what’s important, and that depends not only on real borrowing costs but also on NGDP expectations. In fact rising real rates are probably more indicative of an accomodative monetary policy than falling rates.

3. As I have explained before, it’s probably more useful to think in the broader terms of marginal changes in the rate of exchange of financial assets for real goods and services by the non-banking sector rather than the imprecise Keynesian lexicon of borrowing and interest rates.

4. I don’t think liquidity was really a big consideration. (Effect rather than a cause. Certainly had nothing to do with TIPS spreads.) I want bore you now but it might be an interesting topic for you to post on in the future

5. IMHO, no question that monetary policy was extremely tight up until the very end of 2008/ early 2009.

Regarding 29 and 30 year bonds. Are you referring to the 1.5 bp difference in yields? Shorter maturity + higher coupon = shorter duration which means a lower yield in a positive yield curve environment. Same reason the 28 year bond with a lower coupon and longer duration is trading at a slightly higher yield than the 29 year bond. Liquidity, on the other hand, is the reason that the bid/offer spread on the 30 year bond is about half the spread on the 29 year bond.

27. August 2015 at 09:16

“I often present my views at “hard money” crowds and am always very well received.”

I’ll have take your word for it. I’m just having a real hard time imagining what you and Schiff could possibly agree about regarding monetary policy.

BTW, if you ever do run into Schiff again, please ask him this: What evidence would convince you that you’re wrong?

27. August 2015 at 09:18

Scott,

TIPS index corrected or not is still not going to give you a perfect read on the real (expected real) interest rates.

I don’t know where you can find the recalculated data for the September – November 2008 period.

You best bet is to compare the 5 year Treasury index to the actual 5 year TIPS which at that time had most recently been issued. (I’ll have a look and send you a link if I can find it.)

27. August 2015 at 09:19

…cultists, fundamentalists and hucksters always seem to have a difficult time with that question.

27. August 2015 at 09:22

Shows the 5 year index vs TIPS 5/8% of 2013

https://research.stlouisfed.org/fred2/graph/?chart_type=line&recession_bars=on&log_scales=&bgcolor=%23e1e9f0&graph_bgcolor=%23ffffff&fo=verdana&ts=12&tts=12&txtcolor=%23444444&show_legend=yes&show_axis_titles=yes&drp=0&cosd=2010-08-26%2C2010-08-26&coed=2015-08-25%2C2015-08-25&height=445&stacking=&range=Custom&mode=fred&id=DFII5%2CDGS5&transformation=lin%2C&nd=%2C&ost=-99999%2C&oet=99999%2C&lsv=%2C&lev=%2C&scale=left%2C&line_color=%234572a7%2C&line_style=solid%2C&lw=2%2C&mark_type=none&mw=2&mma=0%2C&fml=a%2C&fgst=lin%2C&fgsnd=2007-12-01%2C&fq=Daily%2C&fam=avg%2C&vintage_date=%2C&revision_date=%2C&width=670

27. August 2015 at 09:25

Shows the 5 year index (non-TIPS) and difference between that and the TIPS 5/8% of 2013.

https://research.stlouisfed.org/fred2/graph/?chart_type=line&recession_bars=on&log_scales=&bgcolor=%23e1e9f0&graph_bgcolor=%23ffffff&fo=verdana&ts=12&tts=12&txtcolor=%23444444&show_legend=yes&show_axis_titles=yes&drp=0&cosd=2010-08-26%2C2010-08-26&coed=2015-08-25%2C2015-08-25&height=445&stacking=&range=Custom&mode=fred&id=DFII5%2CDGS5&transformation=lin%2C&nd=%2C&ost=-99999%2C&oet=99999%2C&lsv=%2C&lev=%2C&scale=left%2C&line_color=%234572a7%2C&line_style=solid%2C&lw=2%2C&mark_type=none&mw=2&mma=0%2C&fml=a%2C&fgst=lin%2C&fgsnd=2007-12-01%2C&fq=Daily%2C&fam=avg%2C&vintage_date=%2C&revision_date=%2C&width=670

27. August 2015 at 09:28

Scott,

Sorry, I’m not much use with Fred. You’ll have to adjust the dates and do the subtraction of the two series on your own.

27. August 2015 at 11:11

Joe, Asking if it matters what the fed funds rate is is like asking whether it matters what the price of zinc is. If the Fed is not targeting the fed funds rate, it doesn’t much matter. If it is being targeted, it matters a lot. Ditto for the price of zinc. Not because the fed funds rate or zinc prices are intrinsically important, but because monetary policy is important.

dtoh, Thanks for the data, but until someone shows me some corrected data, I’ll continue to assume that real interest rates rose in late 2008.

27. August 2015 at 12:07

Thanks for the answer. That was what I was kinda getting at; since they do not currently target fed funds (like they target say inflation) its current level is really irrelevant. What truly matters is if money is getting tighter/looser.

I recently made the comment in a meeting that the Fed might tighten policy next month and someone replied with something to the effect “the Fed cant keep the rate low forever because its causing distortions in the market”. I wanted to reply but didn’t get a chance, to say “who cares what the fed funds rate is? we dont want tighter money”.

27. August 2015 at 15:28

Dr. Sumner,

If you are correct that the rising interest rates and the falling spread between 5 year and 10 year United States Treasury conventional and TIPS bonds are indicators of a loss of liquidity and a tightening credit market then the credit market is tightening but not because of any policy change by the Federal Reserve Bank (FRB). It is the market that has driven the tightening, not FRB policy.

So are you saying that the FRB policy be changed to counter the tightening of the market or that FRB policy has driven the tightening?

27. August 2015 at 17:15

Charlie, I like your explanation and this is a general criticism of loose money – it benefits the financiers first. Whether it benefits others depends on many other factors.

27. August 2015 at 19:29

This is the worst news of the day: I might have to start reading Krugman again, if he starts to say sensible things.

27. August 2015 at 20:24

dtoh, at Fred, go to the “Share” tab under the graph. There will be a url for the graph, just as you have it.

28. August 2015 at 13:11

– I agree with Krugman that markets already have tightened. That’s what I see when I look at the ……….. Rising USD !!!

28. August 2015 at 13:51

David, You said:

“If you are correct that the rising interest rates and the falling spread between 5 year and 10 year United States Treasury conventional and TIPS bonds are indicators of a loss of liquidity and a tightening credit market”

I never said anything about a tightening credit market. And the Fed controls monetary policy. Period. End of story.

I’m not saying it should be changed. It is changing, I’m saying it’s changing in the wrong direction.

3. September 2015 at 05:20

LOL I thought you hated Krugman.

Now you do a long post with graphs, “Look at me mom! I’m like Paul!!”