Chinese house price bleg

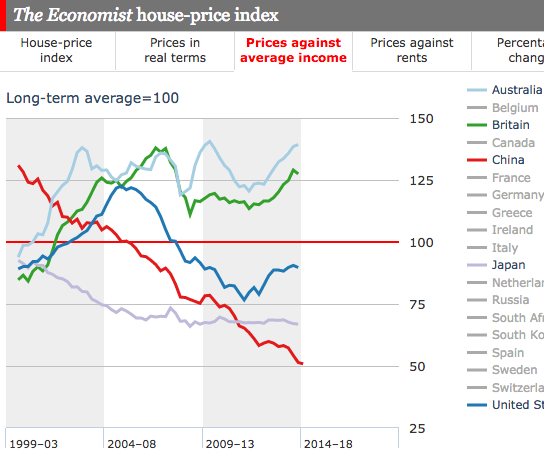

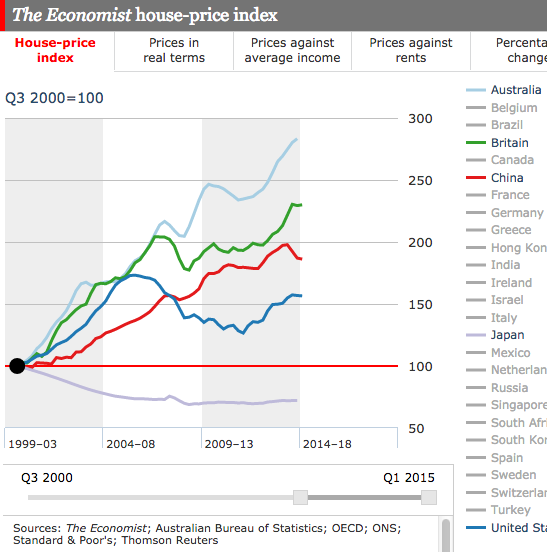

People are always talking about the Chinese house price bubble. And I have to admit that it was also my impression that Chinese house prices had risen dramatically in recent years. I was curious to see just how much and checked The Economist’s handy interactive graph. And I was completely shocked by what I found:

Yes, this is house prices adjusted for changes in income, but still . . . The ratio of Chinese house prices to income has fallen from 130 in 2000 to 50 today?

I showed 4 other countries for comparison purposes, and they all seemed to be about what I’d expect. But China?

Questions:

1. Is the data in The Economist wrong? And if so, where can I get the correct data?

2. If it’s accurate, does this mean China never had the house price bubble that everyone is talking about?

What am I missing here?

PS. In nominal terms the Chinese prices look more impressive, but considering how much China’s boomed since 2000, I even find the nominal increase to be quite underwhelming—somewhere between the US and the UK. And don’t mention specific cities, I only care about the overall Chinese housing market, not individual cities.

PS I have a new post at Econlog.

PS I have a new post at Econlog.

Tags:

27. August 2015 at 08:22

According to this working working paper, the house price to income ration should be around 8-9 times

http://www.nber.org/papers/w21112

27. August 2015 at 08:26

Cloud, China’s probably too high. But on the other hand it seems to have declined sharply, so perhaps it’s less out of line? Or is my data wrong?

27. August 2015 at 08:28

If this data is legit, the obvious explanations are

1. Rapidly rising income.

2. Alleviation of Mao-era housing shortages (i.e., building skyscrapers everywhere).

27. August 2015 at 08:31

E. Harding, I can confirm both of those. Incomes have soared since 2000. So either both graphs are right, or both are wrong. The fall in the ratio is consistent with the rise in nominal prices, given the huge surge in incomes.

27. August 2015 at 08:39

However, from the graphs, the Chinese house price-to-rent ratio seems to have continuously risen.

27. August 2015 at 08:46

E. Harding, Wow, that implies Chinese rents have fallen since 2000, even in nominal terms. I’m beginning to think the data in the Economist really is bogus.

27. August 2015 at 09:29

The US data seems a little strange to me too. They show home price/income in 2005 pretty close to the late 1970s but price/rent is much higher. But, rent has been a pretty stable portion of nominal income over that period, so I think there must be some sort of creep in the denominator of one of their ratios.

I wonder if they are using per capita income as the denominator in the price/income measure. This would miss changes in household size, I think, because home prices would be a per household measure and income would be a per capita measure. Falling household size in China would cause a distortion there, if that is what they are doing. Although, the basic trends are probably still the same, if this is a problem and you account for it, just not as pronounced.

27. August 2015 at 09:32

You have to wonder about the data as I thought the housing market in China was really hot 2009 – 2012 with mixed results since then. Could be a lot of China averages represent so much many realities it is hard to see it in the averages. For example, you have a house price in Bejing averaged out with small poor farmer ownership. Secondly, home ownership is increasing higher percentage of the population so the data is effected by a lot of starter homes.

It is reasonable to understand what is driving this.

27. August 2015 at 10:16

https://www.evernote.com/shard/s76/sh/aa107da3-2666-4a4c-bb8e-56f541b7625f/9312091d2c23b758cb74ed5a49d1f7e0

If we refer to the figure in the link above,we would see it is only possible when tier 3 cities in China dominate the index. But then, it would be a bit misleading to the main picture of the China situation, as tier 3 are much less developed regions.

I mean , when we talk about housing price bubble in US, we won’t focus on Alaska, I guess 🙂

27. August 2015 at 10:23

On China, I think you can do worse than read Wang Tao at UBS and Jonathan Anderson of Emerging Advisors. Both would corroborate the idea that affordability in China has been falling for the past TWO decades.

27. August 2015 at 10:24

Eek. By falling, I meant improving…

27. August 2015 at 10:27

Kevin and Collin, Good points. But clearly the mystery remains.

Cloud, Thanks, but those figures don’t really solve the problem:

1. First of all, the difference between tier 2 and 3 is nowhere near large enough to explain what The Economist shows, it would just change the result slightly.

2. But the level of prices is very different from The Economist, showing a much more rapid increase in even tier 3 than for in all of China (from the Economist.) The Economist shows only about a 80% increase over 15 years.

3. Tier three cities (and Alaska) should absolutely be included in any nationwide index.

Thanks Robert.

27. August 2015 at 10:29

If true, then Chinese are making more money, but haven’t splurged on housing. This kind of makes sense as it seems most of the new housing has been ugly lego block high rises. Not exactly fancy. In fact, most of those buildings would look right at home in an American 70s era urban ghetto.

27. August 2015 at 10:32

I know you want to avoid talking about individual cities, but real estate is necessarily a local market. The (almost) nationwide housing boom and bust in the US in the 2000’s was rare. The main drivers of housing prices are 1) labor and capital inflows and outflows, 2) supply restrictions, and 3) momentum. While overall macroeconomic variables are a useful second order effect (e.g. reducing the employed labor force even without net migration), to lump together the Beijing and Guangzhou housing markets into one market called “China” is about as useful as also throwing in Vancouver, Canada and Sydney, Australia into this hypothetical “Chinese real estate market” index.

27. August 2015 at 10:34

Chuck, You could say that, but by Chinese standards the new housing is palatial. It’s a vast improvement over what they had before. Just ask my wife!

(Also you don’t have the crime, graffiti, etc of American urban slums.)

27. August 2015 at 10:35

Njnnja, You were warned. I’m going to ignore your comment. 🙂

27. August 2015 at 11:04

Suspect it mostly means the data from China is wacky. I remember reading at one point that according to state inflation measures, the median apartment price was reported not to have changed since 2001.

That might mean is that China has more inflation and less real growth than reported, but judgment should probably be deferred until better information becomes available.

The uncertainty would help explain the stock market volatility.

27. August 2015 at 11:11

Yeah, this is odd…

“According to the NBSC, from 2000 to 2011 private housing CPI rose by 8%. Let me emphasize very strongly that is not 8% annually but 8% total in twelve years. In a period when official real GDP growth was averaging around 10% annually, official housing price inflation was a mere 8% total. To provide some perspective, research covering a similar time period found total real estate asset price inflation of 200-300%. ”

http://www.baldingsworld.com/2015/07/15/considering-the-veracity-of-chinese-gdp/

Lots more detail at the link, including some evidence even NSBC doesn’t really believe its own numbers — they reweighted ousing higher even as they found the cost was increasing more slowly than components.

27. August 2015 at 11:22

Talldave, I regard claims that China’s real growth is much less than reported as being right up there with those who claim the actual rate of inflation in the US is 8%, and the government is lying. Anyone who travels to China frequently can see the effects of double digit growth, but I’m completely open to the idea that house price inflation numbers may be wrong. But then where are the accurate figures for the ratio of Chinese house prices to income?

People describe a house price bubble, but where are they getting their data?

27. August 2015 at 11:34

Scott — The NBER says about 10% housing price inflation a year. Do you believe them or NSBC? 🙂

http://www.nber.org/papers/w21346

OECD countries make substantial revisions all the time, I wouldn’t be shocked if China was exaggerating its growth by 2-3% — the housing numbers by themselves appear to account for about 1%. Clearly Chinese growth has been strong, but just as clearly those numbers make no sense.

27. August 2015 at 11:41

New post by Yglesias on monetary policy:

http://www.vox.com/2015/8/27/9215629/september-fed-interest-rates

27. August 2015 at 11:41

Also, NSBC itself seems not to have any confidence at all that its numbers are even comparable across years, and they often flatly contradict proxies like PMI readings. I’m not sure we can say anything useful about the ratio of income to housing given the uncertainties in those numbers.

27. August 2015 at 12:41

@TravisV, That was an excellent link. Thanks!

27. August 2015 at 13:13

Of course, the Australian housing price results are not completely independent of Chinese conditions … (Speaking as someone living in a house in Melbourne with a mainland Chinese landlady.)

27. August 2015 at 13:16

Yglesias makes the argument that lower rates will boost unemployment — again, people who know that the Phillips curve is a myth still make that argument.

He specifically says that lower rates will help lower-skill, black workers. However.

a) real borrowing rates for lower-skill, lower-income workers are still high, and to the extent that you lower them you just trap them into loans they can’t repay.

b) it’s not like business are borrowing money so they can hire workers; more likely they are borrowing to buy assets and probably downsize workers in the process.

27. August 2015 at 14:11

Australia’s house prices are also buoyed by extremely favourable policies. I can take a mortgage, buy a house, rent it out, and any shortfall between the rent and the mortgage payment is a loss set against taxable income. Also explains why household debt is so high in OZ. When I looked at buying a house there I was offered a mortgage seven times larger than I needed and advised to put the excess in a deposit account…. Not for me. But there must be many who do this.

27. August 2015 at 15:34

If you see pictures of Chingdao (spelling? major inland city) you can believe this. Huge apartment blocks—no elevators btw.

Perhaps the figures are adjusted for square footage or quality. A larger flat with indoor plumbing and electricity is worth more than a small house with neither.

Manhattan is not the USA and Beijing not China.

27. August 2015 at 18:12

Normally this blog thinks the UK is doing great – is this blog wrong or is the Economist’s data wrong?

27. August 2015 at 21:19

Bubbles are not bubbles because of what trends look like absolutely.

Bubbles are bubbles because of what is relative to what would have been.

If China’s real growth rate is 10% per year where prices would have fallen 8% each year, then even a horizontal, flat trend would not be inconsistent with a bubble.

28. August 2015 at 03:28

It’d be interesting to compare China to S. Korea, especially from 1985 thru maybe 2005. Over that period I believe (from what I saw) they built new housing (mostly high-rise) for a large fraction of their population that was still living on the land (as they made the switch to industrial farming, which took a while because family farms and the associated guilds had some of the same stickiness they had in the U.S. And the condos in the high-rises were considerably nicer than my friend’s family’s rural home. They didn’t want to move or sell to the agribusiness biggies but after the disappointment of having to change, getting older, with children not wanting to stay on the farm, they loved it. And I think this was all private investment, encouraged by government policy and slashing of land use regulations. Where not only was the new housing higher quality in a more dynamic environment, but it was lower cost.

The ghost cities I’ve seen in China remind me of what I saw happen in Korea, both infrastructure (cleaving mountains for new highways, electrical generation, …) and homes. Especially since it appears not only is the quality of life inversely proportional to the number of people living on the land, but so is political stability. i.e. this transformation diminished the power of the (traditionalist, “why should we change?”) rural voters. It was striking how the big cities, esp. Seoul cleaned up. Local pollution is way down, save for what still blows in from China, but that is improving as well. Appears to track individual wealth more than any regulatory dicta. i.e. dicta without wealth is ignored.

28. August 2015 at 05:40

James Bullard says volatility won’t change economic outlook

http://www.bloomberg.com/news/articles/2015-08-28/fed-s-bullard-says-volatility-isn-t-changing-economic-outlook

28. August 2015 at 10:32

Talldave, I don’t believe either number. I’ll use the official Chinese GDP data until someone comes up with something better, or until the data doesn’t match what I see on the ground. Right now no one has come up with anything better, and it does match what I see on the ground.

Suppose you were right. Then by now China would be less than half as rich as they claim. But they claim to be much poorer than Mexico? Just how poor do you think China is? Try spending two weeks in India, then 2 weeks in China. Tell me what you see. India’s growing at 7%.

Robert, You should read Lorenzo, who’s the expert. The main issue is controls on new construction.

Benjamin, Qingdao is actually a coastal city, and the tall apartment buildings do have elevators. (Do they work? Well that’s a different issue . . . )

Ben, Doesn’t the UK data show exactly what I claimed it showed? A big rise then mostly sideways.

Ari, Excellent comment.

28. August 2015 at 11:31

Scott — The difference isn’t very big, maybe three or four years of growth. So I’m basically just saying I wouldn’t be surprised if China in 2015 is only as rich as China claimed to be in 2012 or 2011. India just isn’t even close, even in 2001.

The 9.3% claimed average growth rate (for PPP) since 2001 gives us a multiplier of about 3.2 (1.093^13), if the true rate was only 7% the multiplier is 2.4, which would mean they exaggerated gains in PPP GDP per capita by 2-3K, or about what they’ve probably achieved since 2012 or 2011. All very rough estimates, of course.

Ari Tai — Yeah, we all hoped the model for China was South Korea, but it may look more like Venezuela (where China just invested $20B).

29. August 2015 at 07:10

Talldave, China’s been growing at 9% to 10% for 35 years, not 15 years.

It’s just idiotic to compare China to Venezuela, just idiotic. Why not compare it to Iceland, or Burundi? Or Fiji Islands? Or the planet Mars? Are you just picking countries at random?

30. August 2015 at 04:15

On a macro level, I agree with you that the hubbub over the veracity of China’s GDP numbers is exaggerated. The country clearly has seen sustained massive growth across all sectors of the economy for a lengthy period. That said, I think you are swinging a bit far in your suspicion of suspicion, e.g. the following comment:

“Suppose you were right. Then by now China would be less than half as rich as they claim. But they claim to be much poorer than Mexico? Just how poor do you think China is?”

Given that China still has hundreds of millions of people living in rural areas where the standard of living is not too different from Chiapas or Oaxaca that doesn’t seem at all outlandish to me.

30. August 2015 at 05:08

Jonathan, I agree about Chiapas for western China, but recall that not all rural areas in China are that poor. Rural areas in places like the Pearl River delta are surprisingly rich. And urban China seems if anything to be richer than Mexico. Just take one metric, car sales, about 1 million/year in Mexico and over 20 million/year in China. And China has about 12 times the population.

The official figures (PPP) have China about 60% or 70% as rich as Mexico, which seems about right or a bit low. But 30% or 35%, with that level of cars sales? I just don’t buy it.

30. August 2015 at 05:13

Update, I just checked and the World Bank has China at 72.7% of Mexico. India’s at 33%. Obviously China is nothing like India, easily twice as rich.