Rogue nation

Most foreign policy experts in the US, and the overwhelming majority of foreign countries, believe the Iran nuclear deal was a good thing, and that Trump made a mistake in walking away from the agreement. But it’s worse than that. Not only does the US no longer wish to participate in this agreement, but we insist that the rest of the world follow our wishes.

And now the US has arrested a top Chinese business executive for violating our misguided Iran sanctions policy. News of the arrest caused stock prices to plunge all over the world, as investors expected the US-China trade war to get worse. And the war may not be confined to China, as there is talk of putting tariffs on cars made in Europe and Japan. Let’s hope the administration comes to its senses, before things get out of control. Everyone loses from trade wars.

I still expect neoliberalism to win out in the long run (see my previous post), as the alternative is too dangerous. But right now the Trump administration is playing with fire.

In recent posts here and at Econlog I’ve been discussing how the US should respond to Chinese misbehavior. How should the rest of the world respond when the US becomes a rogue nation? That’s a difficult question.

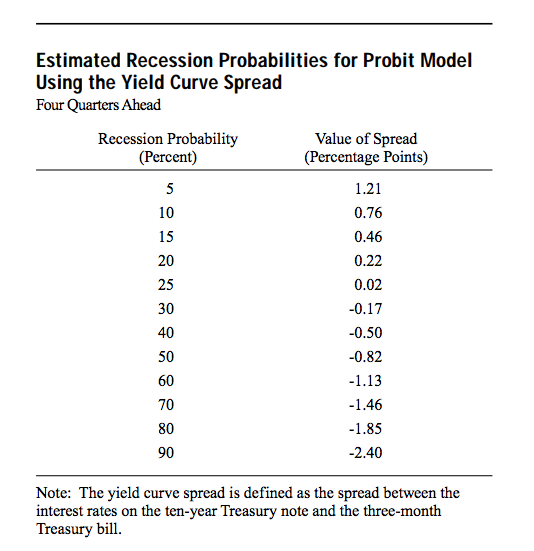

PS. The 10-year yield still exceeds the 3-month yield by 45 basis points. Based on an empirical study by Arturo Estrella and Frederic Mishkin, the probability of recession within 12 months is now about 15%:

Fed funds futures also point to a slowdown but no recession. A slowdown doesn’t concern me because recent growth has been unsustainable—partly a sugar high from fast NGDP growth, and partly a one-time response to the corporate tax cut.

BTW, fed funds futures markets are currently predicting a fed funds rate of 2.55% in July 2020. If that outcome occurs, the yield curve will still likely have a positive slope, and we probably won’t be in recession.

Nonetheless, the probability of recession is certainly a bit higher than last week. There is reason to be concerned.

If I were the Fed, I’d probably raise rates this month (by 20 basis points), but also announce that no further rate increases are expected, unless the economy moves in an unanticipated direction. But then if I were the Fed, I wouldn’t even have this policy regime in the first place. I’d end IOR and use the monetary base (which would then be 98% currency) as my policy instrument. I’d use 3.5% and 4.5% futures contract “guardrails”, to help steer the base.

Monetary policy should be about money and NGDP expectations, not about banking and finance and interest rates and inflation. K.I.S.S.

Tags:

6. December 2018 at 10:04

Here’s another paper outlining a different recession probability model developed by Jonathan Wright that factors in the level of the Federal Funds Rate in addition to the spread between the 10-Year and 3-Month Treasury yields.

Here’s a chart showing where that math said we were just three weeks ago.

Finally, here’s the tool we built to do his math, so you can estimate the probability based on these factors today without having to wait for us to update the chart (note: the chart takes the 90-day average of the data before estimating the probability, which is the method Wright uses in his paper).

Hope this helps!

6. December 2018 at 10:27

Trump’s only sense that he trusts is his gut. It’s understandable why he’d rule out trusting his own brain, but his gut has a spotty track record.

6. December 2018 at 10:37

Thanks Ironman.

Tom, Maybe he’ll be frightened by the stock market—but then there’s the circularity problem to worry about.

6. December 2018 at 10:43

It seems Huawei licensed certain US tech. But you only get the license if you sign that you don’t export the technology to certain countries. It seems Huawei didn’t really care about that part. So it’s not unreasonable for the US to punish Huawei for flouting US law. I thought you are a man of the law, Scott, now aren’t you?

6. December 2018 at 12:08

I’ve been thinking a bunch about the situation the Fed is putting Trump in…

REMEMBER WARSTLERIAN ECON: The fed has moral obligation as “bankers” to favor private sector and reward con fiscal policies.

So let’s look at tariffs Scott.

The Fed is basically convincing Trump that they will not go along with his 4% GDP and let him dance around on Obama’s grave.

So if you are Trump would you rather get the slow down to 2% done by:

1) MASSIVE TRADE WAR that benefits Trump Voters and screws Blue Urban markets.

2) No trade war and fed just raises rates.

—–

My point Scott is that when the Fed DEVIATES from its moral obligations as described in Warstlerian Econ when it wrongly pretends it is neutral on fiscal policy…

IT PUSHES US TOWARDS TRADE WARS, NOT AWAY.

The Fed then has to choose:

1) ADMIT that it prefers Trump Econ to Obama Econ and as such will let Trump’s Econ run hotter, let him good and hot for 2020.

2) Continue the bullh*t lie that it isn’t MORALLY OBLIGATED to offset bad fiscal and reward good fiscal.

It’s not Trump playing with fire Scott… it’s the Fed.

6. December 2018 at 12:12

Ironman:

I propose that the sign is wrong on that model concerning the effect of the short term rate on recession probabilities. In your tool, if 10 year rates are 0%, short term rates have to be 2% or higher to get to a 50%+ probability. In truth, the probability of recession correlating with an inverted curve is probably higher when yields are low than when they are high.

6. December 2018 at 12:16

Taken to its conclusion, this turns the fed into a five and dime candy store… which is good, they become AUTOMATED in a way because the discretion flows to fiscal / politics.

New fed stance: “We’ll drop rates .5% for a year if US and China get Trade War worked out!”

One way or the other trump is going to run Econ to favor his voters… if Fed pretends it can’t or won’t help out… the own whatever Trump does.

Bankers are NOT neutral and no real Economist works for the govt.

6. December 2018 at 14:16

Morgan Warstler nails it…

What is the point of electing someone on a platform of tax cuts and deregulation if the Fed is going to operate GDP-growth capping policy?

Answer: none.

We VOTED to experiment with expanding the economy’s potential via these policies. If Powell doesn’t let that experiment unfold then Trump has every right to ask him to step aside.

P.S. the U.S. has long suspected Huawei of breaching PRE-DEAL Iran sanctions – as far back as 2011. Remember those?

6. December 2018 at 14:40

What’s sauce for Iran is sauce for Russia and Venezuela.

Monetary policy is being conducted surprisingly competently over the past two-four years.

6. December 2018 at 15:09

Christian, When have I ever advocated enforcing bad laws? Have I called for Jeff Sessions to lock up more pot smokers? Do you even pay attention?

Morgan, Not sure what you are talking about. Try speaking English.

Brian, You have a rather primitive understanding of monetary policy. The Fed doesn’t “limit” the economy’s potential.

6. December 2018 at 15:32

hmmm, I don’t think I implied that the Fed can “limit” the economy’s potential.

What I was implying (I thought pretty clearly) is that the Fed is operating under some misguided output gap assumptions that lead it to believe it needs to counter any growth rate above their estimate of “potential.” Whereas the electorate chose a candidate who ran on a platform of challenging those assumptions. Hence the political friction.

6. December 2018 at 15:55

@ Christian List

Thanks for explaining why the US has grounds to prosecute the Huawei executive.

I think that there is a good, simple, and in a sense dumb way forward on this. Basically, the US commits to enforcing its own laws. If Chinese executives enter into deals that make them subject to US criminal law and then are prosecuted for violating the law, then that is their own damn fault. I also hope that China does the same to US executives.

6. December 2018 at 16:08

This should have been said eight years ago.

6. December 2018 at 16:34

Wall Street traders are more concerned with the 2 year/10 year spread than 3 month/10 year. That’s why the markets are so spooked, that spread is almost flat.

6. December 2018 at 17:33

I am no fan of arresting women at airports who are not US citizens, or trying to arrest Julian Assange, a non-US citizen, on espionage charges. Imagine if Russia arrested a US citizen on espionage charges, for receiving an online dump of information.

The charges against Meng Wanzhou were filed by the Attorney General of the Eastern District of New York. The attorney generals are generally considered to be apolitical. We will see.

The Communist Party of China generally has an overt contempt for Western economic and democratic principles, such as intellectual property, moral hazard, civil rights, or sanctions against nations that violate international norms.

Arresting a citizen of China for playing by the rules enforced by her own nation strikes me as a difficult decision to justify.

6. December 2018 at 17:39

Scott,

I paid very close attention, but it doesn’t make much sense. You are either in favor of the rule of law or you are not. The rule of law is not about cherry picking.

I’m just teasing you, Scott. But to be honest I really don’t like your cherry picking based on political ideology. I would have found it more credible if you had also argued for people who are diametrically opposed to your political agenda.

To your defense I have to say that your piece “How should we think about Russian meddling in the 2016 election?” was some kind of progress, and I appreciated it.

@P Burgos

I suppose you can argue like that. I just doubt that the Chinese executives knew in every detail what they were doing. US law looks like a kafkaesque nightmare to me. From an outside view, it appears to me that anyone can get caught up in this grotesque spider’s web, no matter what you do.

The list of questionable US laws is long. And I do not mean obscure laws here that no one needs anymore, I mean very basic laws that are used all the time.

The power of US law enforcement seems immense to me. And rogue states like China must be asking themselves: Who’s really in charge in the US? I don’t really get it, and they won’t get it either.

6. December 2018 at 18:28

Here:

http://www.themoneyillusion.com/why-im-not-impressed-by-conservative-judges/

It was no kind of progress at all; don’t fool yourself.

6. December 2018 at 18:55

Scott, just read it again, it makes perfect sense, but you gotta mentally prepare to find your own side wrong…

I’ve been thinking a bunch about the situation the Fed is putting Trump in…

REMEMBER WARSTLERIAN ECON: The fed has moral obligation as “bankers” to favor private sector and reward con fiscal policies.

So let’s look at tariffs Scott.

The Fed is basically convincing Trump that they will not go along with his 4% GDP and let him dance around on Obama’s grave.

So if you are Trump would you rather get the slow down to 2% done by:

1) MASSIVE TRADE WAR that benefits Trump Voters and screws Blue Urban markets.

2) No trade war and fed just raises rates.

—–

My point Scott is that when the Fed DEVIATES from its moral obligations as described in Warstlerian Econ when it wrongly pretends it is neutral on fiscal policy…

IT PUSHES US TOWARDS TRADE WARS, NOT AWAY.

The Fed then has to choose:

1) ADMIT that it prefers Trump Econ to Obama Econ and as such will let Trump’s Econ run hotter, let him good and hot for 2020.

2) Continue the bullh*t lie that it isn’t MORALLY OBLIGATED to offset bad fiscal and reward good fiscal.

It’s not Trump playing with fire Scott… it’s the Fed.

—–

Ok Scott, now you’ve re-read and it sinks in!

The Fed is ASSURING that even if Trade War is bad for the Economy, Trump does it anyway.

Trump does tons of great dereg and tax cuts and Fed raises rates (IMMORAL).

So Trump will go gangbusters slowing Economy down to improve the lives of Trump Belt / Trump Voters, smaller pie, more go to his people.

The Fed is GUARANTEEING the Trade War you claim to fear.

6. December 2018 at 19:45

What amuses me about the weirder trolls here like E Harding and M Warstler is that they think they are delivering deep knowledge to Sumner, like he’s a peer and they are hashing out high-level debates. When actually they are clowns that no one, least of all Sumner, takes seriously.

6. December 2018 at 20:06

I agree that arresting Chinese CFOs in Canada for violating US sanctions which shouldn’t exist in the first place is sort of inherently offensive. Why should I care about Iran at all? What did they ever do to me?

This is the Deep State at work. (Or more like Fifth Columnists at work.)

6. December 2018 at 20:13

Kevin Erdmann:

The chart accurately reflects what Wright’s recession model would predict for the given yield spreads and Federal Funds Rates.

That said, I think you have a valid point. Since Wright’s probit model is based on historic data, where recessions have occurred at much higher FFRs and yields, the model is being extended (or stretched) to cover the low FFR condition, which falls outside the range of observations where recessions have previously occurred.

We know that low FFRs do not prevent microrecessions from occurring within the U.S. economy (such as oil producing states experienced from mid-2014 to 2016), so it’s not much of a stretch to consider that the recession probabilities given by Wright’s method understate the actual probability of a national recession when FFRs are at low levels. Or as George Box put it, “all models are wrong, but some are useful”, where the question yet to be answered is how useful is it at these levels?

P.S. Congratulations on the new book – I’m looking forward to reading it in the near future!

6. December 2018 at 20:44

OT but in the ballpark.

Richard Clarida seems to be a breath of fresh air at the always-stale Federal Reserve. (He is new Vice Chair).

Clarida has pondered aloud the 2% IT “ceiling” and asymmetry.

At the PIMCO blog there is a post that may give some insights into Clarida’s thinking.

https://blog.pimco.com/en/2018/12/engineering-inflation-for-the-fed-the-time-is-now

No, the author is not Clarida, but maybe is an acolyte. (Clarida comes to the Fed from PIMCO).

Yes, i wish someone at the Fed would flat out say they want NGDPLT, and a robust target at that, by any means necessary, and we are taking the weapons we need, including money-financed fiscal programs.

But… Clarida is what we got, and he looks better than some others.

6. December 2018 at 21:42

Thanks Ironman. Always a pleasure to trade notes with you.

7. December 2018 at 01:56

OT but interesting. I genuflect to the QE totem. But unless I chant incessantly enough to drive out thoughts, doubts persist. John Cochrane says QE does nothing, and today hoots about Canada.

In economic news, Japan household spending in October unexpectedly declined 0.3% year-over-year, again raising concerns that the Bank of Japan’s monetary stimulus is either too small or ineffective. Household spending and also real wages slipped for a third straight month.

Also, Bank of Japan Governor Haruhiko Kuroda said the central bank’s purchases of equity exchange-traded funds was necessary, and shrugged off criticism its growing presence is distorting the stock market. Kuroda said the need to debate central bank ETF buying was not yet on the table. The Bank of Japan owns 77.5% of Japan’s ETF market, having bought nearly 23 trillion yen of ETFs since 2013, a senior central bank official said.

In other news, the business confidence of large manufacturers in Japan likely fell for a fourth straight quarter, in the three months to December, Reuters reported citing it own poll. Trade tensions were blamed.

7. December 2018 at 05:59

Ben, I’d say that Cochrane has discovered that the interest rate channel is highly overrated (both as cause and effect) but that QE was effective anyway.

7. December 2018 at 09:03

“But then if I were the Fed, I wouldn’t even have this policy regime in the first place. I’d end IOR and use the monetary base”

I’d go the other direction. Have IOR be the main instrument. When IOR, make bids for $X amount of Treasuries at zero yield. Lowest maturity offered wins the new money first.

Also have a helicopter money failover instrument to these monetary injections. End the FDIC and discount window. Have non-full-reserve bank accounts register as Securities Act offerings to non-accredidated investors.

7. December 2018 at 09:12

That should say “When IOR is at zero.”

I still don’t know how the guardrail could concretely work on the lower-bound. The Fed could nominally lose a lot of money on futures for undershooting NGDP, but that wouldn’t be the governors’ money.

For me, the lower guardrail needs a concrete secondary action. The upper guardrail itself takes money out of the market with pledged margin. The governors could have sole judgment and bonuses set on an NGDP level target, but that wouldn’t require the guardrails.

7. December 2018 at 10:32

Brian, And exactly how does the Fed cap the economy’s growth? The traditional argument is that they do so by reducing inflation which raises the unemployment rate? Is that your argument?

Christian, You said:

“I’m just teasing you, Scott.”

Teasing requires a bit of skill. Thinking that belief in the rule of law implies support for vigorously enforcing pot laws is evidence of a lack of such skill. But then I’m just teasing you.

“was some kind of progress”

When you see “progress” I see evidence that you are beginning to ever so slightly understand views I’ve held all along. But I’m just teasing you.

Harding, I want prosecutors to decide which laws are worth enforcing, not judges.

Matthew, You said:

“The Fed could nominally lose a lot of money on futures for undershooting NGDP”

As long as you and I get rich, why does it matter?

7. December 2018 at 11:43

“Most foreign policy experts in the US, and the overwhelming majority of foreign countries, believe the Iran nuclear deal was a good thing, and that Trump made a mistake in walking away from the agreement. ”

You may have missed the news that Iran this past Saturday tested another medium-range ballistic missile. Once again, in noncompliance with UNSCR 2231 (2015 Iran Nuclear Deal). I believe the UK, France, Netherlands and Germany held a closed door meeting to decide what to do next.

This agreement was a joke from the beginning, done purely for political purposes. Israel already showed Iran had no intention of honoring any part of the agreement. It’s ridiculous to think they would have- with threats all around them and a radical population, nuclear weapons are a logical pursuit for the current regime.

I think your hatred for Trump creates some blind spots when it comes to foreign policy.

PS. The treaty was never approved by the Senate so it should be unconstitutional to begin with.

7. December 2018 at 15:06

“As long as you and I get rich, why does it matter?”

I just haven’t understood the lower guardrail and the explanations have not made sense to me.

Let’s say lower guardrails work by $10 margin for the Q4-18 contract. Reserves/currency are reduced by $10. Every 1 percentage point off of 3.5% level target is $1. I also consider the completely isolated effect, with no secondary policy.

If the market expects NGDP to come in at 2.5%, then the market expects the $10 to yield 46% with settlement in three months (1.1^4).

So the isolated effect of the lower guardrail is 1) the monetary base is reduced by $10 for 3 months and 2) the market sees a very high yielding, government-backed asset. The direct effect decreases NGDP.

For efficient markets, a Rube Goldberg series of concrete events could increase long-term NGDP expectations.

1. The market sees that if NGDP goes down by a significant percentage, the people with currency will get very rich.

2. These people will eventually spend the money.

3. So the market will expect much higher NGDP down the line.

Sorry, this is too many steps for me. The guardrails on Bretton Woods had a direct, concrete step of raising or lowering dollars per oz of gold. The higher guardrail has concrete step of reducing monetary base, but lower guardrail also reduces the monetary base in the short-term.

The monetary base will increase substantially three months later, but the recipients of that money are unlikely to spend it. The recipients had the $10 saved to begin with.

An interesting idea is to instead post the $10 margin with *bonds* for lower guardrail.

8. December 2018 at 09:54

Tom, You said:

“You may have missed the news that Iran this past Saturday tested another medium-range ballistic missile.”

So this is evidence that Trump’s new policy is working?

Matthew, At the lower guardrail the Fed does enough stimulus (open market purchases) to keep NGDP expectations within the range, to avoid big losses.

8. December 2018 at 13:35

I would like the lower guardrail itself to somehow concretely increase NGDP, without any secondary measures. Friedman said once he would like a computer to do monetary policy. I’m trying to program that thing.

The higher guardrail, by itself, does automatically constrain NGDP. The lower guardrail is tough.

8. December 2018 at 21:36

Scott,

I never talked about pot. I couldn’t care less about pot. I talked about this case, and similar cases.

But I find your approach problematic. It sounds like arbitrariness.

My approach is a bit different.

1) I want transparency. I want to know who is calling the shots and why.

2) I want solid clues / evidence BEFORE US law enforcement begins its terrorizing “investigations”. There needs to be a good reason and a well-defined limited scope.

9. December 2018 at 11:51

Christian, You said (responding to me):

“Scott,

When have I ever advocated enforcing bad laws? Have I called for Jeff Sessions to lock up more pot smokers? Do you even pay attention?

I paid very close attention, but it doesn’t make much sense. You are either in favor of the rule of law or you are not. The rule of law is not about cherry picking.”

And now you say:

“I never talked about pot.”

I give up.

10. December 2018 at 13:05

Scott,

I’m sorry. You talked about pot and I made a general statement about the rule of law. It was not about pot. I don’t care about pot.

Pot laws aren’t really witch hunts. They are transparent, for example in the sense that close to every pot-smoker knows if his behavior is legal or not – and how high the punishment can be if he gets caught.

I’m worried about kafkaesque laws and investigations with unlimited scope, that can trap you no matter what you do, similar to witch trials in the past.