My vision of macro

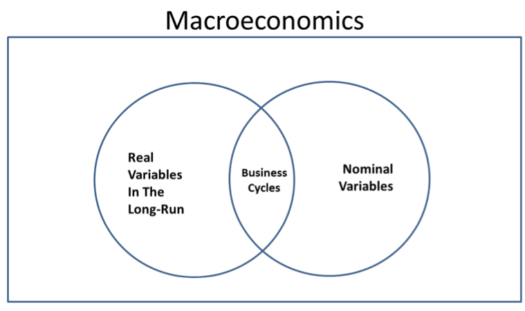

The following Venn diagram helps to explain how I visualize macro:

There are three basic fields within macro:

There are three basic fields within macro:

1. Equilibrium nominal

2. Equilibrium real

3. Disequilibrium sticky wage/price (interaction)

I’ll take these one at a time.

1. Within equilibrium nominal there are important concepts:

A. The quantity theory of money

B. The Fisher effect

C. Purchasing power parity

The first suggests that a change in M will cause a proportionate change in P. The second suggests that a change in inflation will cause an equal change in nominal interest rates. The third suggests that a change in the inflation differential between two countries will cause an equal change in the rate of appreciation of the nominal exchange rate.

All three concepts implicitly hold something constant; either the real demand for money, the real interest rate, or the real exchange rate. In all three cases the concept is most useful when the money supply and price level are changing very rapidly, especially if those changes persist for long periods of time.

2. Equilibrium real macro can be thought of as looking at economic shocks that do not rely on wage/price stickiness. These include changes in population, technology, capital, preferences, government policies, weather conditions, taxes, etc. These can cause changes in the real demand for money, the real interest rate, the real exchange rate, the unemployment rate, real GDP, and many other real variables.

3. Disequilibrium macro looks at nominal shocks that cause changes in real variables, but only because of wage/price stickiness. Thus because prices are sticky, an increase in the money supply will temporarily cause higher real money demand, a lower real interest rate, and a lower real exchange rate. These changes occur even if there is no fundamental real shock hitting the economy. The effects are temporary, and go away once wages and prices have adjusted.

If wages and prices are sticky then an increase in the money supply will also cause a temporary rise in employment and real output.

And that’s basically all of macro. (This is how I’d try to explain macro to a really bright person, if I were given only 15 minutes.)

I also believe that understanding the implications of this three part schema makes one a better macroeconomist. Talented macroeconomists like Paul Krugman tend to have good instincts as to which real world issues belong in each category. Here’s my own view on a few examples. For simplicity, I’ll denote these three areas: nominal, real, and interaction:

1. Most business cycles in ancient times were real, with some interaction. The 1500 to 1650 inflation was nominal.

2. Recessions such as 1893, 1908, 1921 and 1982 were mostly interaction.

3. The Great Depression was all three.

4. The Great Inflation was mostly nominal, especially in high inflation countries.

5. The 1974 recession was more “real” than usual. Ditto for the WWII output boom.

6. The real approach works best for short run shocks to specific industries such as housing and oil, plus long run growth. The nominal approach works best for high inflation rates and long run inflation. The interaction approach works best for real GDP fluctuations in large diversified economies.

7. If one set of economists say the Japanese yen is too strong, and another set say it’s too weak, they are probably using different frameworks. Those who say its too strong are using a nominal framework, and are likely worried about deflation. A weaker yen would boost inflation. Those who think the yen is too weak are using a real framework. Rather than worry about deflation, they worry that Japan has a current account surplus. These views seem to contradict, but it’s theoretically possible for both to be right. Perhaps the nominal exchange rate for the yen is too strong, and the real exchange rate is too weak. You would then weaken the nominal exchange rate by printing money, and strengthen the real exchange rate by reducing Japanese saving rates. (I don’t favor the latter, just saying that’s the proper implication of the misguided worry about Japanese CA surpluses.)

8. Don’t let your policy preferences drive your analysis. Throughout all of my life, it’s been assumed that monetary shocks drive real output by causing changes in the unemployment rate. Not changes in trend productivity growth or population growth or labor force participation or any number of other variables. Money matters because it affects unemployment. If the unemployment rate is telling you that monetary policy is no longer holding back growth, the proper response is not to double down on your belief that we need easier money and then look for new theories to justify it, but rather to conclude that whatever problems we still have are now “real”, not “interaction.”

A good macroeconomist knows that all three fields of macro are very important, and which models apply to each of the three fields, and which field is most applicable to each real world macro issue.

Tags:

26. March 2017 at 12:43

Would the 2008/2009 recession be due to interactions too?

26. March 2017 at 12:49

Great post, I will spend some time reading around this. I pretty much completely ignored macro from BA Econ to DPhil Econ. The disagreement between credible macroeconomists put me off. I was too lazy to wrestle with the ambiguity and understand the core differences.

Do you distinguish between equilibrium real and microeconomics? If so, how?

26. March 2017 at 13:34

Bill, Yes, with a bit of a real shock thrown in.

Matthew, Real macro is really just a form of micro.

26. March 2017 at 14:21

So what you are saying is that the circle representing the real variables is the range of production outcomes that would be possible (given best policy management of the existing real variables) if there were not sticky prices and wages?

Given that there are business cycles that interfere with real production, the nominal circle can be tweaked by policy to minimize this interference by the business cycle, which is in turn caused by the sticky prices phenomena?

This may be a bad interpretation on my part, but it seems to leave no room for the idea that good management of the nominal variables could lead to an increase in the real production possibilities. Nor does it leave open the possibility that the real production possibilities could shrink over time because of bad management of the nominal variables. And it doesn’t admit the possibility that fully flexible prices and wages might lead to negative outcomes in the face of nominally fixed payment obligations. Or that an economy might get stuck in a lower production equilibrium even when prices were fully flexible unless all contracts were continually renegotiated.

I hope I am not too badly mischaracterizing your views. Actually, I hope I am, because otherwise economics truly is a dismal science. And I really think you should give yourself more credit to affect things than my interpretation does.

26. March 2017 at 14:54

In the Great Depression, what were the important “real” elements? Is there particular telltale evidence for the “real” component?

I see the “nominal” and “interaction” components of the Great Depression. But I’m not clear why we should believe there was also a major “real” component.

26. March 2017 at 16:16

I also thought this was a great post, if only because most macroeconomic education is just not presented in this manner, and should be.

26. March 2017 at 17:16

Great post.

I do hope a few pages in new macro texts are devoted to property zoning.

Property, like wages and employment, is ubiquitous. Also, about 50% of commercial bank lending is on property.

Like taxes and employment, property figures into nearly every business.

26. March 2017 at 17:50

Could the nominal losses of the Great Recession be playing a role in long run (real economy) productivity losses, just the same? Here’s why I ask, re Andrew Haldane’s recent speech, page 11:

“Pre crisis, the strongest rises in measured productivity were in manufacturing, information and communication and financial services, all of which experienced annual growth of over 4%. But growth was not confined to these sectors, with virtually all sectors making a positive contribution to productivity growth.”

“In the period since the crisis, those pre crisis trends have changed dramatically. Virtually every sector has seen productivity flat-line. The contributions of all sectors to productivity growth have fallen and most are tightly bunched around zero. Whatever has caused UK productivity growth to fall, it has done so on a generalized, cross-sector basis.”

26. March 2017 at 18:49

Becky, though it seems to me pretty obvious the Great Recession caused the post-2008 productivity stagnation, countries with high nominal GDP growth (Brazil, Belarus’, Russia, etc.) failed to get out of that trap. I’m not sure when the world will get out of the post-Great-Recession real weakness.

26. March 2017 at 20:29

Sumner has a perfect record, ex post, explaining the economy using monetary theory. In reality, from Coleman, “Applied Finance” (2017), an excellent textbook: “expert forecasts of macroeconomic factors are no better than random numbers (Chan et al. 1998), and analysts’ year-ahead forecasts have crippling errors (e.g. Espahbodi et al. 2015). Not surprisingly, models proposed to predict returns do not outperform naïve estimates (e.g. Simin 2008). A practitioner valuation primer gave a précis of the difficulties by saying that the process is so challenging that a fund manager “who is right 60 to 70 percent of the time is considered exceptional” (Hooke 2010: 9)”

But I like our host. He lets me post here, most people would have banned me by now, hehe.

26. March 2017 at 21:07

In defense of Sumner, he will argue Knightian Uncertainty, after his hero Frank Knight, see: “Knightian uncertainty” What this says is that only after the fact do you know about things like the Wicksellian Natural Rate of Interest, and that’s why prediction is hard, but the fact that you only know these variables ex post does not make the theory wrong. That’s all very well and good, except you cannot test anything Sumner says as false. Sumner is always right, something his fawning ace students no doubt knew and were quick to point out (so to get a passing grade).

27. March 2017 at 00:34

Do you consider issues like inequality and politics as the “real” variables? Or do you think that those are not Macro?

27. March 2017 at 02:15

@ Ray:

“models proposed to predict returns do not outperform naïve estimates”

—–

DOW futures are down 147 this a.m. Just batting 100 percent.

27. March 2017 at 02:31

You don’t have to watch MZM Vi. You already know that Vt will fall. It is axiomatic. The more savings which are increasingly impounded and ensconced within the confines of the commercial banking system, the lower money (savings) turnover. This will be accelerated every time the Fed now raises its regressive remuneration rate, RRR. Thus, there will be a decline in consumer durable goods, followed by a decline in business’s capital goods, i.e., a deceleration in overall incomes, viz., R-gDp.

27. March 2017 at 04:29

Nice framework, simple, direct, but complete enough to help make fairly sophisticated analysis.

27. March 2017 at 12:37

Jerry, The diagram is a framework for thinking about macro issues. There are many possible assumptions about what monetary policy can or cannot do. In this post I’ve explained what I think it can do, and what I think it cannot do.

Daniel, I wrote a whole book on that called “The Midas Paradox”. The short answer is that the federal wage policies were a massive (and negative) real shock. Those occurred in July 1933, May 1934, late 1936, late 1938 and late 1939.

In addition, you have Hoover’s high wage, high tariff and high tax policy regime, although I don’t think those real shocks were as important as the New Deal shocks.

Thanks John.

Becky, It’s possible that the after effects of the Great Recession could still be reducing the level of productivity. But in that case you’d expect a higher than normal growth rate of productivity. But we have lower than normal productivity growth.

Ray, You said:

“after his hero Frank Knight”

Very funny.

Cloud, Yes, I view them as real factors. They seem more micro than macro to me, but I suppose that’s debatable.

Thanks Jose.

27. March 2017 at 15:25

Sumner once again overlooks the crucial area of economic calculation, as it relates to economic coordination in a division of labor, and how it is adversely affected by socialist monetary systems such as the Federal Reserve System that prevent investors from observing and knowing relative market prices, interest rates and spending.

To the socialist minded, the production of pencils requires no market based coordination among the myriad industries such as lumber, copper, oils and synthetics, and graphite mining. They just get produced the way they are supposed to get produced if enough state money is printed. The non-existent free market does the rest, and woe unto anyone who citicizes the non-existent free market from doing its job in the existing world.

Yes, business cycles can roughly be thought of in terms of the interaction between “real” and “nominal” variables, but unlike the Venn diagram presented here, they are not distinct when the universal category is calculation. Here, BOTH are subject to valuation and calculation, the problem of course is that there is no market in money, so it is impossible for investors IN A DIVISION OF LABOR, not subject to some singular, centralized mind, to coordinate in a sustainable manner.

27. March 2017 at 16:00

If the unemployment rate is telling you that monetary policy is no longer holding back growth, the proper response is not to double down on your belief that we need easier money and then look for new theories to justify it, but rather to conclude that whatever problems we still have are now “real”, not “interaction.”

Interesting. The Federal Reserve created a new index, the labor market conditions index, a couple of years back to get a better grip on employment markets, which they still believe affect inflation.

The Phillips curve has been prone for a couple generations, nevertheless if we want to look at employment markets the labor markets conditions index has been softening since 2010.

It is interesting to ponder who determines when macro economic management is appropriate.

Would the voting public regard. “labor shortages” as a feature or a bug of good monetary management?

27. March 2017 at 20:16

@flow5:

Yeah that was quite a crash in the Dow today LOL

28. March 2017 at 00:38

“There has never been any empirical evidence that money and credit markets are predominantly in equilibrium. It is a theoretical supposition.

On the planet we live, there is no perfect information

In our world, information, time and money are rationed.

Neoclassical economics has demonstrated that therefore markets cannot be expected to be in equilibrium.

What happens when markets do not clear (i.e. always)?

Demand does not equal supply. Markets are rationed.

Rationed markets are determined by quantities, not prices”

https://www.postkeynesian.net/downloads/Werner/RW301012PPT.pdf

28. March 2017 at 08:54

If an individual firm run by people can make lack coordination with other firms about WHEN their individual market is ready to use up resources in order to acquire that firm’s output, why can’t more than one firm run by people lack such coordination?

Is it not FAITH to believe that coordination just happens even with socialist money and thus without market determined interest rates and relative prices?

28. March 2017 at 09:18

@msking

and we just recovered and are 150 points up for the week in Dow, SP500 and Nasdaq even more up. But flow5, The Denigrated, will keep saying he got it right because there was a brief dip on Monday.

28. March 2017 at 10:08

Ben, You said:

“It is interesting to ponder who determines when macro economic management is appropriate.”

Janet Yellen and her staff.

28. March 2017 at 10:50

Scott, totally off topic, but I recall you did research a few years ago on the civic virtues of Scandanavian societies and how they contributed to economic growth. Raj Chetty has published another paper showing that Utah (yes Utah) apparently has the highest income mobility in the US, at a level comparable to Denmark or Sweden. The theory is that the Mormon Church is responsible for a socially inclusive civic minded society. Furthermore, a geographic breakdown shows that income mobility is highest in the great plains states and parts of the mountain west, which are racially homogeneous areas settled mostly by people of Germanic ancestry. The worst areas are confined to the deep south, which have deep lingering problems with racism. Perhaps you should write an extension of your paper/blog post about this.

http://www.rajchetty.com/chettyfiles/mobility_geo.pdf

28. March 2017 at 14:11

That does not appear to be a Venn diagram unless a) there are real variables that are also nominal variables, b) inflation = 0 in the long run, c) the set descriptions for the rings are differ from the words (and the words describe elements in those sets), or d) the intersection is supposed to be the empty set (there are no business cycles).

I think what you really mean is more of an interaction between real variables in the long run and nominal variables (and that interaction is called the business cycle). That would be illustrated by e.g. two nodes (real, nominal) and a link (business cycles) between them.

28. March 2017 at 15:02

@ George:

“But flow5, The Denigrated, will keep saying he got it right because there was a brief dip on Monday”

I’m not that stupid George. You should read my posts. I’m the best trader in history.

28. March 2017 at 15:03

Scott Sumner:

Why is it politically correct to discuss nominal and real values by saying that we have negative real rates of interest but not politically correct to say that we have negative real rates of income?

28. March 2017 at 18:19

Comments (7867) |+ Follow

Exactly, that’s the 3rd seasonal inflection point of every year (c. May 5th). Stocks could easily reverse to the upside until that juncture (as is typical). Short-sellers beware (use stops).

At that point CPI inflation will be re-accelerating relative to real-output. Instead of interest rates falling, interest rates will be rising. Then we’ll get coterminous subpar readings on R-gDp (& downward revisions from economic forecasts).

27 Mar 2017, 02:05 PM

28. March 2017 at 18:20

Sumner, never mind. You answered my question in a prior post.

28. March 2017 at 20:47

Scott Sumner:

“Ben, You said:

“It is interesting to ponder who determines when macro economic management is appropriate.”

Janet Yellen and her staff.”

—30—

Maybe, though is it generals who decide when and how to fight a war?

Also, there are other members of the FOMC, as you surely know.

Even Volcker was once outvoted by Reaganauts on the FOMC. Yellen cannot get too far from consensus—and the likes of Ester and Mester. (Yes, sadly, Richard Fisher has departed).

Then, there are always legitimate concerns that regulatory agencies are “captured” by the industries they are supposed to regulate. This is hardly a novel observation.

Is the financial class and industry influential on monetary policy and rule-making? More so than, say, the real estate construction industry or agriculture or manufacturing? Seems like it.

There is no labor seat on the FOMC, that is for sure.

28. March 2017 at 21:07

I liked this, because I have such a hard time parsing the language of mainstream macro-economists. This is a great starting point. I have personally spent the most of my effort learning chartalism/mmt/postkeynesianism. I expect that your assessments are good for the most part, but I haven’t yet made clear connection between our social and cultural practices– legal, political, and financial processes, and the principles and concepts you use in analysis.

I would suggest that the cultural assumptions required to make your analysis valid are more narrow and rigid than your certainty in presenting these ideas suggests. I’m generally not satisfied with the usual critiques of standard economic frameworks: ie people aren’t really rational, etc.

The only comment I want to make on inflation is I can conceive of a phenomenon I would call “price drift”, where people keep adjusting prices merely because that is expected. In such a scenario, there are no underlying inflationary causes.

We live in a world where computation is no longer expensive, prices can be computed algorithmically, so long as people have the proper tools. How do our technical limitations affect real and nominal price phenomena? Could technology negate tools like monetary policy or interest rates, etc? I find the idea of “menu costs” to be merely the most basic starting point to think about the social language of value scorekeeping, accounting, and resource governance.

I have a lot to think about with the way you present the distinction between real and nominal. Thanks for giving me so much to think about.

28. March 2017 at 23:23

If the Fed can do damage by poor management of money demand (aka nominal spending plans/NGDP growth expectations) in 2008 it can do it over the medium term too. If it can fail in short, sharp, bursts, it can fail over longer periods. Stop talking about unemployment. Talk about managing money demand/nominal spending/NGDP growth expectations.

http://ngdp-advisers.com/2017/03/28/stop-talking-unemployment/

29. March 2017 at 05:40

@ msgkings

“quite a crash in the Dow today LOL”

———-

He who laughs last, laughs best. The DJIA is down 300 points from its March high. Real selling won’t happen until later.

29. March 2017 at 05:53

Rates are falling because economic activity was choked off. It fell off because when the Fed hiked rates, it doesn’t just restrict the growth of new money & money velocity, it impedes savings velocity (a subset of money and credit velocity). Savings velocity is responsible for real economic growth. Thus in a twinkling R-gDp is swallowed up.

All economists are ignorant.

29. March 2017 at 09:00

[…] Alexander | Scott Sumner wrote an interesting blog post on his vision of macro. It is a useful way of seeing where Scott stands today. However, we were […]

30. March 2017 at 08:53

Risk-on. Everything is copacetic. Stagflation (a supply and demand imbalance), was just the result of high oil prices in the 70’s. Since R-gDp is still *real*, there’s no need to worry about the impending transitory, indeed intertemporal, acceleration in other folk’s inflation.

31. March 2017 at 18:37

John, I have a new post on that.

Jason, You said:

“I think what you really mean is more of an interaction between real variables in the long run and nominal variables (and that interaction is called the business cycle).”

No, I mean business cycles have both real and nominal aspects.

Derek, You said:

“In such a scenario, there are no underlying inflationary causes.”

Is that also true of changes in the price of apples and oranges? No underlying causes?