If you look hard enough for a reason to tighten…

Now that eurozone inflation has fallen far below the ECB’s 1.9% target and seems likely to stay lower, the Germans are in an embarrassing position. They can no longer oppose monetary stimulus by their usual arguments—that the ECB should focus like a laser on inflation targeting and ignore growth.

So now they are looking for a housing bubble in Germany to justify my their hawkishness. JN sent me the following article:

It still enjoys a reputation as a renter’s paradise, but on Monday the Bundesbank issued a warning about the rise in house prices in Germany. In its monthly report published on Monday, the central bank said that properties in German cities “may currently be overvalued by between 5% and 10%”.

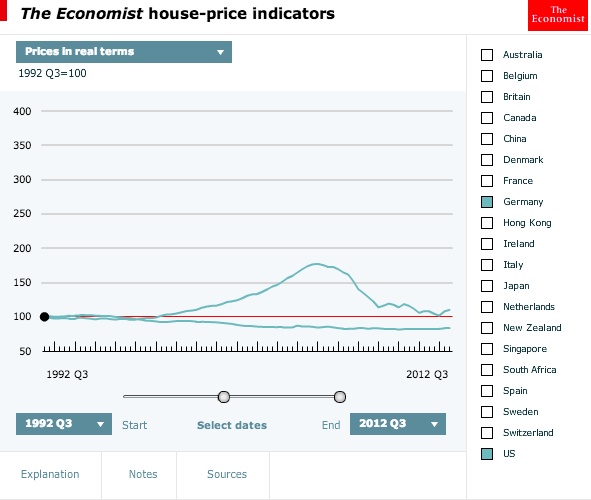

So I went to The Economist’s great interactive housing guide and plugged in real housing prices for the past 20 years:

The top line is the US, with the famous up and down pattern. The bottom line is Germany, where real housing prices seem remarkable stable, although they look like they have fallen about 20% in the past 20 years.

Now admittedly the 2012 endpoint is out of date, so I went to the most recent data I could find, August 31, 2013, where The Economist reported that nominal German house prices are up 5.1% in the past 12 months. So maybe real housing prices have only fallen about 15% in the past 20 years.

Having trouble seeing a bubble? That’s why you don’t work at the Bundesbank. You just aren’t squinting at the data in the right way. There’s definitely a bubble brewing in Germany. After all, there is no fundamental reason why German house prices would rise 5% after falling 20% in real terms. It’s not like Germany is the shining star of Europe, with amazing low 5.2% unemployment. And it’s not like long term interest rates are at a record low level. So it must be a bubble.

The article JN sent me concludes with the following paragraph:

Not all German economists are convinced by the Bundesbank’s gloomy analysis. The Institute for the German Economy in Cologne looked into the subject last year and concluded that the rise in property prices was healthy and no bubble was in sight. “In Germany we’ve seen roughly a 10% rise in credit,” said Michael Schier of the institute’s real estate team. “That simply doesn’t compare to the 150% bubbles we saw in some of the countries that were hit by the credit crunch.”

OK, 10% is not as much as 150%. But it’s still clearly a bubble. How could it not be?

Tags:

24. December 2013 at 15:13

According to the European Commission’s House Price Index (HPI), house prices are rising in Belgium, Germany, Estonia, Luxembourg, Malta, Slovakia and Finland. The most recent data for Germany (2012Q4) shows it is up 5.0% year on year:

http://appsso.eurostat.ec.europa.eu/nui/show.do?query=BOOKMARK_DS-304230_QID_-4AFF5667_UID_-3F171EB0&layout=TIME,C,X,0;GEO,L,Y,0;TYPPURCH,L,Z,0;INFOTYPE,L,Z,1;INDICATORS,C,Z,2;&zSelection=DS-304230INDICATORS,OBS_FLAG;DS-304230INFOTYPE,INDEX_Q;DS-304230TYPPURCH,TOTAL;&rankName1=INFOTYPE_1_2_-1_2&rankName2=TYPPURCH_1_2_-1_2&rankName3=INDICATORS_1_2_-1_2&rankName4=TIME_1_0_0_0&rankName5=GEO_1_2_0_1&sortC=ASC_-1_FIRST&rStp=&cStp=&rDCh=&cDCh=&rDM=true&cDM=true&footnes=false&empty=false&wai=false&time_mode=NONE&time_most_recent=false&lang=EN&cfo=%23%23%23%2C%23%23%23.%23%23%23

But in the Euro Area as a whole, house prices are down by 2.2% year on year. House prices are falling in France and are in an accelerating free fall in the Netherlands. And don’t even bother asking how they are doing in the Euro Area periphery (shhh).

But as everybody knows, the ECB runs a one size fits Germany only monetary policy, and the rest of you miscreants just have to suck it up with supply side reforms or whatnot.

And of course the question remains, what the heck does monetary policy have to do with house price bubbles anyway, and the answer is, quite frankly, not a damned thing. But it does make a convenient excuse for money so tight that the Euro Area squeaks when it walks.

24. December 2013 at 16:03

It could also be that, after 20 years, the dreadful East German housing stock has been sufficiently replaced to upwardly affect prices. (The reunification affects German housing price data since the East German housing was way less valuable than the West German housing when priced in an open market.)

Though, given Mark Sadowski’s data (pausing here to mention how much folk reading this blog appreciate Mark S’s rampant statistical empiricism), perhaps not.

The German constitution has a “right to build” provision (basically, you cannot stop folk building on their land except by explicit legislation–none of that “you need some official’s permission” nonsense) and its local government financing is significantly on a per-person basis. So government land use regulation does not significantly restrict supply and, guess what, house prices are really stable.

Read a post–which I now can’t find, dammit–where someone pointed out that Germany restructuring was aiding by strong income growth in the Mediterranean and down the PIIGS countries need to restructure, Germany is not returning the favour.

But creating non-existent housing bubbles while unemployment soars and Greece is experiencing Great Depression scale income collapses is getting to the really vicious stage.

24. December 2013 at 18:40

Given that the Bundesbank mishandled German reunification (which was also German Monetary Union) in much the same way as the Bundesbank-dominated ECB has mishandled the Euro, we are clearly dealing with an entrenched mindset.

On the Bundesbank’s reunification track record, see this post by Lars Christensen:

http://marketmonetarist.com/2012/08/18/the-bundesbank-demonstrated-the-sumner-critique-in-1991-92/

and the 2003 paper by Jorg Bibow he links to.

24. December 2013 at 20:20

This ‘bubble-phobia” appears to be the fallback position of the anti-QE’ers and Chicken Inflation Littles. They cannot say we are facing inflation; indeed inflation is at the lowest rates since the Great Depression. The USA inflation trend-lines are sinking towards deflation, at this point.

Some inflation-hysterics have shifted from saying 2 percent inflation is okay to saying we should shoot for zero inflation (how that is measured…oh, forget it). Plosser rhapsodizes about deflation.

Others are ranting about bubbles, despite the fact that equities and housing better but hardly frothy.

The inflation-hysterics can’t talk about gold, as gold is sinking, and will probably sink for a long time.

We need a psychiatrist, or sociologist, to explain this blood-lust, this strident, strained peevish zeal to fight inflation, even when there isn’t any to speak of. Or is this some sort of (misguided) creepy class warfare thing—keep money tight, tight, tight and teach those freeloaders a thing or two. The oddity is, at this point tight money will keep interest rates at zero, meaning creditors will hardly gain.

Is there is basic urge in humans to “control” something? As in “controlling” communism, or sexism, or minute traces of carcinogens, so now we have a population that wants to “control” inflation.

This is no longer about economics. No sensible person is worried about inflation under 4 percent as much as they should worry about real economic growth. That is just nuttiness.

A nominal index is not as important as real output.

Or, at least I thought….

24. December 2013 at 21:41

Prof. Sumner,

Really, you actually think there is no real estate bubble in China? You think Lars Christensen was wrong when he wrote the following in October last year?

“since 2010 the PBoC obviously has become fearful that it had created a bubble – which is probably did.”

http://marketmonetarist.com/2013/06/21/chinese-monetary-policy-failure

http://marketmonetarist.com/2012/10/22/dangerous-bubble-fears

25. December 2013 at 05:44

Mark, Thanks for the data—love your “one size fits Germany” comment.

Lorenzo, Good point about German zoning.

Travis, I don’t believe “bubbles” are a useful concept. Will Chinese house prices fall at some point in the future? Of course, markets go up and down. That’s what they do. Is there malinvestment in Chinese housing? Yes, especially in smaller cities. But I don’t believe the concept of bubbles is useful. What good is it? It doesn’t help us to predict future Chinese housing prices. People were crying bubble 10 years ago, when Chinese houses were very cheap by today’s standard. If you could go back in a time machine and buy Chinese houses at the prices of 10 years ago, would you?

25. December 2013 at 06:53

Merry Christmas, from CNBC.com, http://www.cnbc.com/id/101295601/page/2

“Nominal Christmas Present Targeting

By Scott Sumner, TheMoneyIllusion.com

If the Fed would simply announce a nominal target for presents, we’d all receive more presents on Christmas day. There are many ways to do NCPT but I prefer that the Fed create a presents futures market.

A lot of people look at the amount of presents under the tree and attempt to derive the stance of Santa. But this is wrong. You need to examine the demand for presents as well as the supply. In general, a large pile of presents is a sign that Christmas policy has been too tight, while coal in the stocking is a sign that it has been too loose.

P.S. As Mark Sadowksi points out in comments, naughty boys and girls would get hot potatoes rather than coal.

P.P.S Nick Rowe responds. Obviously I agree but I want to make something clear…”

25. December 2013 at 14:06

That should be “and now the PIIGS countries”.

26. December 2013 at 20:02

My guess is that the German data is distorted by the extreme difference between wealthy parts of west germany and poor parts of east germany. You can buy whole blocks of flats in east germany for silly prices like 10,000 euros.

31. December 2013 at 11:16

Philippe. That should not distort rates of change data.