Currency demand at Christmas

My dissertation looked at currency demand at Christmas. Here’s what I discovered:

1. Between December and January of each year real currency demand falls.

2. The Fed accommodates that drop by decreasing the supply of currency by a roughly equal amount.

3. Hence prices change very little between December and January

4. The seasonal decline in percentage terms was much larger in the 1920s and 1970s than the 1940s.

5. The seasonal decline as a share of GDP is fairy stable. That’s because the cash/GDP ratio was far higher during the 1940s.

6. The seasonal decline was concentrated in coins and small bills.

Here’s what I concluded.

1. The seasonal variation in currency demand is due to transactions balances, not hoarding balances.

2. Hoarding demand (and thus total cash demand) rose sharply between the 1920s and 1940s due to falling interest rates (op. cost of holding currency) and rising tax rates (benefit of hiding wealth from government in the form of currency.) Between the 1940s and 1970s the ratio fell back to 1920s levels due to rising interest rates. The transactions demand for cash as a share of GDP varies relatively little over time.

3. In the 1920s people shopped with coins and small bills. By the 1970s coins could no longer be used to make significant purchases and were merely used for change in non-seasonal transactions (parking meters, phone booths, Coke machines, etc.) I seem to recall that coin seasonality dropped due to inflation, but am not certain. But big bill seasonality did not rise as much due to inflation as you’d expect, as consumers switched to credit cards and checks for big transactions.

4. Because the total cash ratio to GDP was high during the 1940s, but transactions use of cash was not particularly high, the seasonal drop-off was much lower in percentage terms. But still about the same in absolute terms, as a share of GDP.

5. Because large bills are hoarded they wear out much more slowly than small bills.

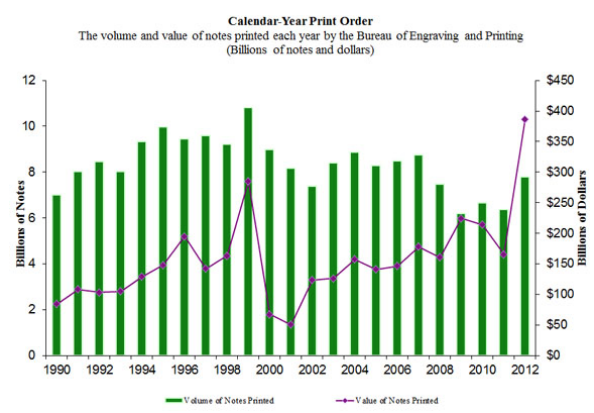

There was one policy implication that I did not discuss (or indeed realize until much later.) If we were going to go the “old monetarist” route of targeting the money supply, the optimal policy would not have been to target the quantity of money in value terms (which is distorted by hoarding), but rather the quantity of money by volume. I.e., the actual the number of green pieces of paper in circulation. Dollar bills and $100 bills each count as “one bill.” In the graph below you’ll notice that the value of currency produced by the government (purple line) actually rises in 2009. So money was not “tight” in that sense. But the volume of new currency notes issued (green bars) falls between 2000 and 2002, and also between 2007 and 2009. (Ignore the 1999 build-up for Y2k.) So money was tight in volume terms but not value terms. Why the difference?

Between 2007 and 2009 the interest rate fell to zero, making it much more attractive to hoard $100 bills as a way of avoiding taxes. In contrast, transactions fell during the recession; so fewer small bills were “needed.” I used the scare quotes because of course in a macro sense more small bills were “needed.” More precisely, a monetary policy regime was needed which would have produced a steady production level of bills by volume. That production is endogenous given the monetary regime, but responds to changes in goods and services transactions produced by changes in the policy regime. This post explains the idea in more detail, using coin production.

Have a Merry Christmas and Happy New Year. Or to my readers who do not celebrate Christmas, just a Happy New Year.

PS. Dylan pointed me to this funny satire by John Carney, which includes this blog.

Tags:

25. December 2013 at 09:06

Two Money Illusion posts on Christmas — what a nice present! Thank you, Scott.

25. December 2013 at 10:58

Thanks Philo.

25. December 2013 at 11:33

Well, I’m an atheist who doesn’t celebrate Christmas, so to me it’s just another Wednesday.

“1. Between December and January of each year real currency demand falls.

2. The Fed accommodates that drop by decreasing the supply of currency by a roughly equal amount.

3. Hence prices change very little between December and January”

Real currency demand is a rather oxymoronic concept.

What I know: If I want to hold more (less) money, then I accomplish this by seeking another individual (or individuals) to hold less (more) money.

The less (more) cash I want to hold, requires another individual to hold more (less) cash.

In the aggregate, the demand to hold cash is always a constant, ceteris paribus. The only way this ceteris paribus does not hold, is if there is an increase or decrease in the aggregate money supply. For then it is not necessarily the case that one individual holding less (more) cash implies another individual (or individuals) to hold more (less) cash. Money could be added or subtracted to the total.

The Fed is not actually “offsetting” any aggregate rise or fall in the demand for cash holding. It is only changing a constant demand to become higher or lower constant by inflating or deflating the money supply. If it did not increase or decrease the money supply, then the demand to hold cash would remain constant. The more “people” wanted to hold more cash, the more other people would have to be present to hold less cash. If everyone wanted to hold more (less) cash, then what would actually change is spending over a given period of time. For example, instead of 1000 units being spent per month on average, 800 units would be spent.

This fall in spending would have the benevolent outcome of shifting the productive structure of the economy to be more in line with the new preferences: Prices would be lower relative to cash balances, i.e. a rise in purchasing power of money. This is incredibly important and should not be interfered with by political force. If it is so interfered, and the money supply is forced upwards, then individuals would not be able to acquire the increased purchasing power they desire. An increase in the supply of money would, in an environment of people wanting a higher purchasing power, lead to further desires to hold more money, which is what we see happen when the Fed inflates. The additional money the Fed creates is typically not destroyed by the people. It is held, and then exchanged via the same offsetting desires to hold less and more money among the populace.

The central bank is not doing the totality of individuals any good by increasing the money supply in a context of some individuals wanting to hold money for less time and other individuals wanting to hold money for longer time, nor is it doing the totality of individuals any good by increasing the money supply if everyone wanted to hold money for longer, such that total spending (and, eventually, prices) declined. Do people want unemployment and declines in output? That is not for any single individual to decide on behalf of everyone else. If individuals behave in such a way in the market that there are some individuals who lose their jobs, then that is in fact what should occur. Each individual gets what they want GIVEN the wants of everyone else. No individual exploits another.

This is the best outcome, because it maximally encourages saving and planning for an uncertain future. The more the individual is faced with the consequences of his own actions and everyone else’s actions in a voluntary market, the more sensitive the individual will be to the desires of other individuals in the market. Demand could evaporate overnight. To protect against it, individuals would seek higher savings to consumption, which can provide insurance against other individuals choosing to reduce their spending because they don’t want to trade the same this month, as they did last month.

This will not cause fascism.

This will not cause depressions.

This will cause the most safe, the most secure, the strongest insurance against the seeming whims of a laissez-faire market.

Most relevantly, it will eliminate the need for the sudden increases in the demand to hold money we see today with political force constrained (as opposed to the more conservative market constrained), irrational central bank.

Fears of another Nazi Germany in the US are unfounded. The dramatic deflation in the early 1930s there would not have occurred if the previous dramatic inflation didn’t occur. There would have been no reason for such deflation, just like there is no reason for massive deflation today (the Fed did not inflate in the recent decades like the Weimar bank did in the 1920s).

Massive deflation simply does not occur without previous massive inflation. Consumers do not capriciously stop consuming for no reason. If we want a stable monetary order, then let us make money the way computers and clothes are made. The last time I checked, we don’t have massive volatility problems in those industries. Why? Because they’re decentralized. It’s easier to plan around a decentralized industry than a centralized one subject to the whims of small groups of individuals (with political power to boot!).

NGDPLT will not solve the problems that NGDPLT is presented as needed to solve. The very fact that Dr. Sumner is here advocating for a different way of central banking, is actually a consequence of the existence of central banking, and not, as he believes, merely a correction or improvement to central bank laws.

Price targeting monetary theorists thought they finally cracked the code, before price targeting was tried, until it was finally accepted as problem causing. Spending targeting theorists are suffering from the same hubris and misguided faith as the price targeting theorists. Do we have to go through another failed rule, or can we let our knowledge of economic laws grounded on transhistorical principles prevent another disaster?

Socialism has never worked. It cannot work. Socialism only in money can’t work. It’s “unnatural.” The market will eventually expunge it as white blood cells expunge viruses. It might take a while, and during that period of time, the false self-professed messiahs will believe that the lack of dramatic and sudden expunging will mean “it’s working.” But the problems will build up over time, and those problems will, like price targeting, seem like the number targeted is “too low.”

If NGDP is adopted, at some point it will be revealed that 4.5% is far too low to accomplish solving the problems that NGDP 4.5% itself has caused. So we will see a new generation of monetarists castigating the “orthodox” market monetarists for “allowing the market to crumble” instead of getting on board for a MORE inflationary rule, which is the new end all and be all of monetary policy: a slowly accelerating NGDP growth rate.

Everyone, please, I implore you. If you know in your hearts that NGDPLT is not capable of being permanent, that it will almost certainly be exposed at some point as being insufficient, that it can only be a temporary stage in the “development of sound monetary policy”, then why go through the unnecessary steps of pain and suffering, and why advocate for a step in the process of steps that lead to a sudden collapse in money?

We should work towards a free market in everything, step by step. To do that, we should advocate for abolishing just the central bank as a start, and to do it in stages. First, to vehemently declare central banking as unjust as a first principle. Then, all the while communicating that central banking must end, to reduce its inflation of the money supply over time down to the rate of the most likely free market money, precious metals. Bring the market monetarists kicking and screaming, until they wise up.

25. December 2013 at 11:48

Massive deflation simply does not occur without previous massive inflation.

We already know you’re an idiot, you don’t have to remind us constantly.

25. December 2013 at 12:47

Geoff: Always a pleasure to read your rantings. A clever mix of vaguely rational paragraphs, tied together with unexamined rationalizations. Can you even tell the difference? I wonder.

You know, I assume, that you’re being very rude. The large number of readers that come here, are attracted by Sumner’s insights. You’re like an econ vampire, trying to steal Sumner’s audience in order to shout your message too. I presume you know that what you really ought to do is start your own blog, to present your point of view. But of course you probably already know that nobody would come. Nobody would care to read it. Must be frustrating for you. But in your own mind, is that enough to excuse your constant, too-long, never changing, never learning, off-topic essays, posted as comments on someone else’s blog?

Well, in any case, Seasons Greetings. Happy Festivus. I wish you well in your Airing of Grievances, and I hope that you someday get the help you so desperately need.

25. December 2013 at 15:31

Best line in that whole satire:

“A lot of people look at the amount of presents under the tree and attempt to derive the stance of Santa. But this is wrong. You need to examine the demand for presents as well as the supply. In general, a large pile of presents is a sign that Christmas policy has been too tight, while coal in the stocking is a sign that it has been too loose.”

25. December 2013 at 19:01

Daniel:

Again, the lack of rebuttals from you, and the childish ad hominem, is only more evidence that you have no rebuttal to my arguments.

You are only reinforcing my convictions when you talk like that.

Don Geddis:

“Geoff: Always a pleasure to read your rantings. A clever mix of vaguely rational paragraphs, tied together with unexamined rationalizations. Can you even tell the difference? I wonder.”

I see you are interpreting your own lack of understanding the rationalizations (which is not surprising of course, considering how you don’t read texts that espouse theories contrary to your own, whereas that is pretty much all I read), to be a sign that I myself have not “examined” my rationalizations.

“You know, I assume, that you’re being very rude.”

Yes, I know that advocating for actions contrary to your preferences is something a sensitive and hubristic intellectual would find offensive or “rude.” I get it. It is like people in church hearing an atheistic rant. Rude. Offensive. Etc. It makes sense.

But I hope you can realize that it is I who receives rude comments. Just look at Daniel’s comment. He called me an idiot. I don’t see you telling him that he’s being rude. Why? Because you enjoy reading it. I deserve it don’t I?

“The large number of readers that come here, are attracted by Sumner’s insights. You’re like an econ vampire, trying to steal Sumner’s audience in order to shout your message too.”

I feel honored that you put me on such a high pedestal.

“I presume you know that what you really ought to do is start your own blog, to present your point of view. But of course you probably already know that nobody would come. Nobody would care to read it. Must be frustrating for you. But in your own mind, is that enough to excuse your constant, too-long, never changing, never learning, off-topic essays, posted as comments on someone else’s blog?”

I am pretty sure that those who start blogs open to public commenting, are not doing so because they want to be in an echo chamber.

I do run a few blogs, I am just not telling you what they are, because I prefer to remain anonymous. Ideas are more important to me than cult of personality worship that you seem to prefer.

“Well, in any case, Seasons Greetings. Happy Festivus. I wish you well in your Airing of Grievances, and I hope that you someday get the help you so desperately need.”

What did I say that would warrant this churlish comment? All I did was post a comment saying we should work towards a free market, and the problems with central banking. Oh how horrible of a person am I, huh?

I need to be insulted, because then my arguments would be refuted, right?

Can’t you see how ignoring me and/or insulting me, is you communicating to me that you can’t refute my arguments, that is, they are correct, or at least more correct, than your theories and convictions? You just gave me a Christmas present with your insults.

25. December 2013 at 19:01

Daniel:

Again, the lack of rebuttals from you, and the childish ad hominem, is only more evidence that you have no rebuttal to my arguments..

You are only reinforcing my convictions when you talk like that.

Don Geddis:

“Geoff: Always a pleasure to read your rantings. A clever mix of vaguely rational paragraphs, tied together with unexamined rationalizations. Can you even tell the difference? I wonder.”

I see you are interpreting your own lack of understanding the rationalizations (which is not surprising of course, considering how you don’t read texts that espouse theories contrary to your own, whereas that is pretty much all I read), to be a sign that I myself have not “examined” my rationalizations.

“You know, I assume, that you’re being very rude.”

Yes, I know that advocating for actions contrary to your preferences is something a sensitive and hubristic intellectual would find offensive or “rude.” I get it. It is like people in church hearing an atheistic rant. Rude. Offensive. Etc. It makes sense.

But I hope you can realize that it is I who receives rude comments. Just look at Daniel’s comment. He called me an idiot. I don’t see you telling him that he’s being rude. Why? Because you enjoy reading it. I deserve it don’t I?

“The large number of readers that come here, are attracted by Sumner’s insights. You’re like an econ vampire, trying to steal Sumner’s audience in order to shout your message too.”

I feel honored that you put me on such a high pedestal.

“I presume you know that what you really ought to do is start your own blog, to present your point of view. But of course you probably already know that nobody would come. Nobody would care to read it. Must be frustrating for you. But in your own mind, is that enough to excuse your constant, too-long, never changing, never learning, off-topic essays, posted as comments on someone else’s blog?”

I am pretty sure that those who start blogs open to public commenting, are not doing so because they want to be in an echo chamber.

I do run a few blogs, I am just not telling you what they are, because I prefer to remain anonymous. Ideas are more important to me than cult of personality worship that you seem to prefer.

“Well, in any case, Seasons Greetings. Happy Festivus. I wish you well in your Airing of Grievances, and I hope that you someday get the help you so desperately need.”

What did I say that would warrant this churlish comment? All I did was post a comment saying we should work towards a free market, and the problems with central banking. Oh how horrible of a person am I, huh?

I need to be insulted, because then my arguments would be refuted, right?

Can’t you see how ignoring me and/or insulting me, is you communicating to me that you can’t refute my arguments, that is, they are correct, or at least more correct, than your theories and convictions? You just gave me a Christmas present with your insults.

25. December 2013 at 22:18

#2 seems like a good response to Bryan Caplan’s doubts about the money demand function: http://econlog.econlib.org/archives/2006/06/what_responds_t.html

On the other hand targeting cash by volume irrespective of denomination seems like an immensely stupid idea. As if there is a stable demand function for money in terms of its volume, growing at a steady rate irrespective of what the money is worth.

26. December 2013 at 08:43

Geoff,

Well, either you’re a moron – and there’s no point in trying to reason with you.

Or it could be your intelligence causes envy in lesser people.

Take your pick.

26. December 2013 at 09:18

Geoff,

“What I know: If I want to hold more (less) money, then I accomplish this by seeking another individual (or individuals) to hold less (more) money.

The less (more) cash I want to hold, requires another individual to hold more (less) cash.”

What if I simply wish to diversify my existing assets into real cash? I could hold my savings account in Benjamins under my mattress instead of the local bank. Who then, am I “seeking” or negotiating with?

26. December 2013 at 10:08

Daniel:

Still lacking a rebuttal to my arguments, and still insulting like a child. How surprising. Maybe one more round of insults will finally do it.

Chuck E:

“What if I simply wish to diversify my existing assets into real cash?”

“I could hold my savings account in Benjamins under my mattress instead of the local bank. Who then, am I “seeking” or negotiating with?”

Your bank.

There is money and there is that which is exchanged for money. If you want to diversify your assets, and you want to hold more (less) cash as a part of your assets, then you’re still in a position of requiring someone else to hold less (more) cash as a part of their assets.

If you want to hold more Benjamins under your mattress, instead of at your bank, then in this case, in order for you to hold more Benjamins under your mattress, the bank must hold fewer Benjamins in their vault.

Money is a scarce good. You can’t multiply a dollar by having it change hands. In the aggregate, the sum total of money does not change when an individual holds less or more money, ceteris paribus.

26. December 2013 at 10:10

Currency demand is a one of those concepts that makes Marco economics seem more like quantum mechanics.

If a whole lot of people decide that they want to spend $100 to $1000 over the next 3 weeks, and they go to their respecive banks and take out money and more people are walking around with more money currency in their pockets than at any other time of year, that is a decrease in currency demand!

And this is because the same people are also spending more currency, and people are hoarding less currency.

It goes against everything that is taught about the concept of demand. If something is in demand, it is because lots of people want to use that resource. But with currency, we say demand is low, when people want to use it.

26. December 2013 at 10:13

Chuck E:

I do enjoy reading you write that cash is “real” money in order to describe the events taking place in your thought experiment. I am not being coy here. I think it’s a significant revelation of how people think about money.

26. December 2013 at 10:34

Geoff,

“Rebutting” austro-sadists is like “rebutting” creationists. A total waste of time, since they’re too stupid to understand the issue – and they’ll claim victory anyway.

And thank you for proving my point.

26. December 2013 at 11:47

Daniel:

Another swing and a miss. “I don’t have to provide a rebuttal because you wouldn’t understand it anyway.” Really? Are you really Daniel, or are you my rather spoiled 12 year old niece Danielle? She talks like that to her mother.

Back the grown up talk though: My argument is still there unchallenged. Continuing to act like a child won’t enable you to acquire the requisite knowledge to provide a response, let alone a rebuttal. Continuing to insult me is only going to add to the evidence that you are wrong.

26. December 2013 at 12:04

I take great pleasure insulting morons.

How do I know I’m dealing with a moron ? They tend to use phrases like “monetary socialism”.

26. December 2013 at 13:41

Daniel:

Thank you for at least attempting to put together a coherent argument.

OK. You feel discomforted by being advised that what you advocate is socialistic money. I get it. I mean, who else but Marxists, Proudhonists, and other radical left wingers enjoy having their ideas and/or worldviews characterized as “socialist”? Obviously I am just trying to get a rise out of you at the expense of the truth.

But is getting a rise out of you and truth mutually incompatible? Not in this case. I don’t throw around the phrase “socialism” as an insult without substance. I use it to describe a particular economic and political situation.

The meaning of socialism, if you have ever actually bothered to look it up, is government ownership and/or control over the means of production.

A society can be understood as falling between two extremes. At the one end of the spectrum, there is 100% socialism (totalitarianism). At the other end, there is 0% socialism (private property anarchy). A society with a central bank but otherwise private ownership of the means of production (which is not, by the way, even an accurate description of this country), is “socialist” to the extent of money. It is not wrong to identify it as socialist.

Why is this? It is because it is indeed the case that the government controls the means of producing money (the Federal Reserve System) in our society. Money production is not open to competition. It is not controlled 100% privately, for profit, in competition, where anyone can enter the market to compete, where the best money wins. The state enforces a monopoly of its own currency as the medium of exchange/account. As such, yes, it is monetary socialism.

You can call me a “moron” all you want, but what I am arguing is factual, and you have yet to even come close to providing a response that I would characterise as a refutation or challenge or rebuttal.

All you have is name calling an childish antagonism. Perhaps it would do you some good to actually educate yourself on the meaning of socialism, and capitalism.

You don’t take please in insulting morons, in my case, for I am smarter than you. You take pleasure in insulting me because I make you feel stupid and immoral.

26. December 2013 at 19:25

From your other post,

John Cochrane:

“Some economists tell me, “Yes, all our models, data, and analysis and experience for the last 40 years say fiscal stimulus doesn’t work, but don’t you really believe it anyway?”

http://www.themoneyillusion.com/?p=2219

I find it extremely difficult to believe that any economist ever said such a thing to John Cochrane. As such my impression is that this is probably some sort of flippant lie.

27. December 2013 at 01:59

That was probably more of a summary of the conversation.

27. December 2013 at 07:23

Geoff,

Let’s say you were feeling ill and decided to go to a doctor.

And the doctor looks at you and says – “yes, you are indeed ill. But it is mostly because you’ve been living a sedentary and unhealthy lifestyle. And yes, I could cure you – but that would prevent you from learning your lesson about healthy living – and you’d only get ill again at some point in the future. And if you die – well, it only proves how unfit you were.”

That would be the awesomest doctor evar, right ? Right ? RIGHT ?

Now, back to you long-winded rant – it can be boiled down to

“M must be kept constant, and if V decreases – and causes a recession – then so be it, for that is the will of Jeebus and the penance for our sins – as communicated unto us by his prophet Mises. Any attempt to compensate by increasing M will only enrage the True Gods further. Repent, ye sinners, before it is too late !!111one”

(In case it’s not clear, I’m talking about M * V = P * Y)

Yeah, dude, that’s some really tight logic there.

Moron.

27. December 2013 at 09:41

Daniel,

As a counterpoint to your doctor….

Suppose your doctor says…You are reasonably healthy for a person of your age, but the latest research says that statins will lower your risk of heart attack even if you have no family history of heart disease, and show no particular elevated risk factors. So, I am going to proscribe generic Lipitor. But, we have seen elevated liver enzymes in Lipitor patients, so I am also going to proscribe something for your liver.

Is that the best doctor ever? Most of what was said sounds reasonable taken each in its part, but as an overall strategy sounds a touch ridiculous. Sometimes treatment is worse than the illness.

When you hand over to an economist control of all of the levers, you should be just a touch skeptical? What is the chance that his proscription will while logical on its face, will not result in side effects (unintended consequences)that are just as bad as the illness?

27. December 2013 at 10:22

Doug M

http://media.tumblr.com/tumblr_m59jwiaz481qa0tls.jpg

27. December 2013 at 10:49

Daniel,

Do you actually have a point? It is impossible to miss it if there was nothing to be aiming for.

27. December 2013 at 11:36

My point is that austrian economics is a pseudo-science relying mainly on circular logic and ipse dixit.

27. December 2013 at 11:46

Funny, it is the usually the Austrians who say that mainstream economics is a pseudo-science, relying upon circular logic, flawed assumptions, and unnecessarily and unrealistic quantification.

They want to consider economics a subset of philosophy.

27. December 2013 at 12:12

Austrian economics certainly is a subset of philosophy. And, as we know, philosophy is to reality as masturbation is to sex.

27. December 2013 at 12:24

Ah, but the Austrian is more likely to realize that this is all just mental masturbation. There is nothing wrong with masturbation. In fact, I recommend that everyone should give it a try. It just isn’t particularly productive.

27. December 2013 at 12:43

Considering are fond of claiming that millions of people going unemployed is somehow a good thing (among others), I’d say there’s such a thing as TOO MUCH masturbation.

27. December 2013 at 12:44

*they (the austrians) are fond of

27. December 2013 at 20:09

Daniel:

“Let’s say you were feeling ill and decided to go to a doctor.”

I wouldn’t ask for the doctor to give me more of what caused me illness in the first place. In other words, I wouldn’t ask for more inflation.

“And the doctor looks at you and says – “yes, you are indeed ill. But it is mostly because you’ve been living a sedentary and unhealthy lifestyle. And yes, I could cure you – but that would prevent you from learning your lesson about healthy living – and you’d only get ill again at some point in the future. And if you die – well, it only proves how unfit you were.”

You’re forgetting that this doctor has been my doctor since 1913, and yet I am continually ill, and he keeps trying to convince me that “this time” he figured it out.

Meanwhile, all I want is for this psychopathic doctor to stop pretending he knows how to control people better than they can control themselves.

“Now, back to you long-winded rant – it can be boiled down to”

“M must be kept constant, and if V decreases – and causes a recession – then so be it, for that is the will of Jeebus and the penance for our sins – as communicated unto us by his prophet Mises. Any attempt to compensate by increasing M will only enrage the True Gods further. Repent, ye sinners, before it is too late !!111one””

It’s clear you don’t read free market economics. You have your conception of it, and that it enough for you. Praise Jeebus!

In actuality, my theory “can be boiled down” to this:

Laissez-faire in money production.

When money is guided by market forces, there is no reason for a sudden massive drop in aggregate spending. But even if there were, then this is a signal that the capital structure and labor allocation SHOULD change, to be more in line with individual preferences, you know, those preferences you want overruled by the preferences of statesmen, because they’re more important.

In a free market of money, M would likely rise over time. But, unlike our credit/debt house of cards monetary system, free market money is not eradicated upon debt default or repayment of debt. In a free market, once money comes into existence, it tends to stay in existence. Massive deflation would be highly unlikely.

“(In case it’s not clear, I’m talking about M * V = P * Y)”

Ah yes, the fallacy ridden equation of exchange. Of course you would resurrect that monstrosity. I mean, it’s not like you challenge conventional wisdom.

“Yeah, dude, that’s some really tight logic there.”

Is that it? You tell me “You want a recession…and…and the equation of exchange!”

That’s some incredibly powerful reasoning you have going on there.

“Moron.”

That’s Mr. Moron to you bub.

“My point is that austrian economics is a pseudo-science relying mainly on circular logic and ipse dixit.”

You don’t even understand Austrian economics, I am puzzled at how you can even convince yourself that your opinion is informed.

“Austrian economics certainly is a subset of philosophy. And, as we know, philosophy is to reality as masturbation is to sex.”

Your immaturity knows no bounds.

“Considering are fond of claiming that millions of people going unemployed is somehow a good thing…”

It’s not a bad thing to conclude that not all jobs are net productive jobs, and that not all jobs are capable of being sustained.

You seem to believe that jobs are the end. The goal. The finish line. In actuality, jobs are but means to ends. It is those ends that jobs should be constrained. Thus, if millions of people go into lines of work that are not conducive to the ends of consumers, then yes, they should change jobs, which of course means temporary unemployment.

You’re arguing from emotions, not economic science. You’re essentially just trying to guilt trip economists into abandoning economic science, on the basis of feeling bad for people who lose their jobs.

Can’t you see how you are displaying for the world to see that you are not interested in economic science, but how to feel better about yourself and everyone regardless of whether or not they are being productive?

28. December 2013 at 04:12

Yet another wall of text full of circular logic and arguments based on thought experiments in which cows are assumed to be perfectly spherical.

Typically austrian, I might say.

28. December 2013 at 11:45

Daniel:

Once again yet another post from you devoid of any substantive argument.

28. December 2013 at 12:03

Not sure how one can argue against a moron who claims deflationary recessions are caused by previous inflation.

28. December 2013 at 12:41

Daniel:

If you’re not sure, and if you want to intellectually demolish those who do argue that recessions are caused by previous inflation, then usually what people do is they read the source material of those they want to intellectually demolish.

This is so they have an actual understanding of what it is they are claiming is “moronic”. That way, they can separate themselves from those who don’t think but make conclusions based on how they feel about something.

Yes, this is much more difficult than acting like a creationist in the face of reason and evidence, and hand waving and dismissing any and all arguments that challenge one’s views. But engaging those arguments is how we grow and become more intelligent. For me, I am not afraid of engaging counter-arguments to my fundamental convictions. In fact, it’s where I spend most of my efforts. I do this because I am more concerned about finding truth, than being surrounded by those who share my beliefs and give me encouragement and validation simply because they agree (but who themselves are wrong).

For example, instead of just focusing on how the Fed could “save the economy” 2008-2009, ask yourself why, during 2007-2009, did the Fed find itself in a world of having to expand the money supply more than it did in the recent past, in order to reverse the consequences of rising money holding times, such as falling spending and falling prices?

Do you take periods of rising money holding times as unexplainable, “exogenous” or “shock” events that the Fed is supposed to deal with in order to save us all? Or do you ever analyse and research the reasons for why so many millions of people across the country would suddenly desire to hold their money incomes for longer than investors and capitalists expected? In other words, why did so many investors not expect the increased money holding times, such that the Fed found itself have to “step in” and inflate the money supply to reverse the consequence of falling spending and prices?

These are the types of fundamental questions that I don’t see you addressing. You have lots of insults, but do you really want to be that kind of a person? An unthinking thug?

28. December 2013 at 12:55

One of the best lessons in economics is that you can’t understand how to “fix” the market unless you first learn how the market works. A doctor has to know how a healthy body works without need for any medical help, before he can know how to help an unhealthy body with medical help.

Do you know how a free market works, i.e. one without a central bank? How capital and labor are allocated? How the productive structure is determined? The function of interest rates? How they are determined?

28. December 2013 at 14:04

Not sure how one can argue against a moron who claims wage/debt stickiness is either a fiction, or a problem to be fixed by throwing millions of people out of work.

28. December 2013 at 14:28

“Not sure how one can argue against a moron who claims wage/debt stickiness is either a fiction, or a problem to be fixed by throwing millions of people out of work.”

The same way as you would if you’re unsure “how to argue against a moron who claims deflationary recessions are caused by previous inflation.”

You do research. You ask questions. You don’t just accept without question what you’re being told by those who are themselves responsible for the problems you observe.

For wage stickiness, you could ask why it is that workers would be willing to forgo any wage income at all, and why employers would be willing forgo any profit at all, such that unemployment rises from the recent past.

You could ask how is it possible for a worker to choose no wages rather than lower wages, and yet still be sustained over time.

You could ask why virtually all workers and employers have come to the conclusion that rising standards of living are synonymous with rising nominal incomes, despite the fact that economics teaches us that rising standards of living are in fact synonymous with rising real incomes, and possibly falling or stagnant nominal income per capita?

You could ask yourself what would people’s willingness to accept a lower price would be, if they were born into a world where money was produced in a free market, such that production in general exceeded money production, such that prices and wage rates fell over time, instead of rose over time? In this scenario, would workers and employers be more or less willing to accept lower prices as compared to the recent past?

I am not claiming wage rates adjust instantaneously to changes in nominal demand for labor.

What I am claiming is that printing more money in order to prevent unemployment ignores the causes of why there is unemployment in the first place, and as a result, ignores the possibility that the solution you espoused in the past to reduce unemployment in the past, is precisely the cause for why there is unemployment now in the present. If you won’t even entertain this as a possibility, then that isn’t scientific of you. You’d be behaving like a dogmatist.

Reason and evidence should reign supreme, not your emotions regarding people losing their jobs. Jobs are not the goal. They are not the end. They are a MEANS to ends. The ends are individual consumer/saver preferences. Jobs should be made and unmade based on those ends. It’s why we produce and work in the first place. We don’t work for work’s sake. If work never had any payoff, none of us would work.

28. December 2013 at 14:35

Not sure how one can argue against a moron who blames people for not acting according to his/her ideology.

28. December 2013 at 14:42

Daniel:

“Not sure how one can argue against a moron who blames people for not acting according to his/her ideology.”

The same way as you would if you’re unsure “how one can argue against a moron who claims wage/debt stickiness is either a fiction, or a problem to be fixed by throwing millions of people out of work.”

Notice a pattern yet?

In this case however, a little self-reflective analysis might help you. You say you’re unsure how to argue against one who blames others for not acting according to his ideology. Well, ask yourself why you blame people for exactly that very thing. You blame the last recession on the Fed not acting in accordance with your set of ideas (ideology is defined as a set of ideas) about how money production “should be” run.

You blame the millions of people losing their jobs on the Fed not acting in accordance with your particular ideology regarding money.

Now, we’re already way past your bedtime, so I don’t expect you to be able to grasp, let alone be convinced, of anything I has said above, but what I do request is for you to please accept the truth that you will continue to be “unsure” of how to respond to certain arguments, if you never research those arguments in various papers, books, and articles.

28. December 2013 at 14:54

I think I get it now Daniel. You don’t even understand what you yourself are saying and believing.

You believe it is wrong to put the blame on incorrect means to achieve desired ends, as the reason for why those ends were not achieved.

You say those who do say such a thing are “morons.”

Well, as I showed you, that kind of makes you a moron, Sumner a moron, basically everyone a moron. For everyone puts the onus for why the economy went into recession on people not acting in accordance with certain ideas, i.e. an ideology. You blame others for not acting in accordance with your anti-austerity ideology.

You’re quite the hypocrite. Flawed character all over the place. No wonder you have trouble dealing with my posts. You need a psychological boost derived from hatred against those who disagree with your ideology you want imposed on them by force.

28. December 2013 at 14:55

Yes, I tend to be unimpressed/unconvinced by circular logic and ipse dixit.

Must be why I’m not partial to the austrian worldview. Unlike certain brainiacs around here.

28. December 2013 at 15:34

Daniel:

“Yes, I tend to be unimpressed/unconvinced by circular logic and ipse dixit.”

How is your comment right here something other than ipse dixit?

“Must be why I’m not partial to the austrian worldview.”

You’re not partial because you’re afraid of even reading it.

You have to actually read the literature you claim is wrong, before your claim is to be convincing and/or informed.

What I said above is not limited to “Austrian worldview.” Papers out of the Federal Reserve have shown that there are non-Austrians who are saying the same thing. But even if there weren’t, it wouldn’t mean the theory is false.

28. December 2013 at 15:36

Daniel:

And where is anything I said “circular logic”? You haven’t shown that either.

28. December 2013 at 16:06

Its statements and propositions are not derived from experience. They are, like those of logic and mathematics, a priori. They are not subject to verification or falsification on the ground of experience and facts.

It’s true because we say it’s true.

28. December 2013 at 16:30

Daniel:

“It’s true because we say it’s true.”

No, they’re true because of painstaking reflection and consideration. They aren’t just assumed without any consideration, the way it is blindly assumed by self-professed empiricists that the laws of nature do not change over the course of time, such that empiricist methodology is structured in accordance with that assumption (hypothesis tested, then some time later data is collected, then some time later analysis is carried out, then some time later the hypothesis proposed in the past is now, in the present, considered falsified or confirmed by experience.

A priori argumentation does not imply ANY argument is permitted. Those that “pass” are those that are consistent with logic constrained to human action, whereas all those arguments not so constrained, are rejected as not applicable to human life and thus rejected as not economically valid.

They’re not true simply because they’re stated as true, or psychologically believed to be true. They are true because they are logically deduced from the incontrovertible axiom of action. It has been discovered as incontrovertibly true, because any attempt to refute it, would itself be an action. Refutation is an action, and action cannot of course refute action. It seems trivial to us today, but I can assure you that it took many thinkers many centuries to make this simple truth explicit, because it cannot be observed the way pears and trees and birds can be observed. It doesn’t take much mental stamina to know one is looking at an object. It takes a lot more mental stamina to think about what it means to observe, and how we come to know what observation really is.

It’s not very helpful to yourself to mischaracterize single passages.

28. December 2013 at 16:34

blablabla, I’m right because I say so, yadda yadda yadda

Try changing the tune.

28. December 2013 at 16:55

Daniel:

“blablabla, I’m right because I say so, yadda yadda yadda”

I just said it’s not true simply because someone says so.

How can repeating the falsehood that I believe it’s true simply because I say so, make it something else?

“Try changing the tune.”

But you’re obviously tone deaf. The tune is there, an A in C major is being played, but you claim it’s an F.

What WOULD I have to say in order for a particular proposition I am claiming is true, such as “the law of marginal utility”, which cannot be observed, to in fact be true?

28. December 2013 at 17:00

Daniel:

I hope you realize that you are really just communicating your own beliefs for how truths are established when you insist, despite my protestations, that I believe X is true “simply because I say so.”

28. December 2013 at 17:02

they’re true because of painstaking reflection and consideration.

Those that “pass” are those that are consistent with logic constrained to human action

They are true because they are logically deduced from the incontrovertible axiom of action

http://www.youtube.com/watch?v=oVOZPlqrRcQ

28. December 2013 at 17:11

Daniel:

I would love to see you refute the axiom of action, without presenting nor intending your refutation to itself be an action.

Because I’m generous, I’ll give you a thousand attempts to do it.

Now’s your opportunity to disprove the premises of Austrianism!

28. December 2013 at 17:17

Sure, right after I disprove the existence of invisible gnomes.

28. December 2013 at 17:19

Daniel:

“Sure, right after I disprove the existence of invisible gnomes.”

Why do you have to disprove that first? Are you afraid of trying to disprove action?

28. December 2013 at 17:21

First, I need to apologize to any readers that have made it this far down the comments. I was one of the first to respond to our resident troll, far above — even though I know better, and that trolls only seek attention, and a better community is made by starving them, not feeding them. My bad.

That said, this comment thread (like many before) has once again been taken over, by a discussion that never was relevant to the original blog post. It’s too late, now.

Geoff, you keep asserting that you’re the good guy here. That you’re trying to have a rational argument, but nobody will engage you on the issues. Please understand that we have lots and lots of counters, but long experience with you has shown that you are not an honest debater. And, despite your claims, you are not seeking truth. I myself have had long comment debates with you in the past. It isn’t that I’m right and you’re wrong, on the issues. It’s that your behavior never changes, even when it is explained to you why your arguments gain so little traction here. It’s clear that you don’t care that nobody is convinced by you; you love thinking of yourself as a martyr.

But now that this thread is already ruined, I’ll bite. Let me respond (just this once) in detail, to some of your claims. Let me be completely clear: I am not going to try to argue substance, try to argue that you are “wrong” and Sumner is “right”, on economics. I’m just going to explain to you why your long posts are so useless and unconvincing here, and try to guide you as to what you would need to do, in order to make some progress convincing people. Perhaps Sumner is wrong, and you are right! But you haven’t presented anything convincing yet.

Of course, I don’t believe that you are actually seeking truth. I believe you are a dishonest debater. So I expect no change in your behavior at all, and on some future post you will repeat much the same useless essays as you’ve posted here. But what the hell. Let’s pretend that you’re actually just ignorant (not understanding why your essays are not convincing), rather than evil (understanding that you aren’t constructive, but not caring).

Geoff, you write: “Laissez-faire in money production.”

That only addresses money as the Medium of Exchange. Surely you’ve read this blog long enough to realize that the whole concern is about a change in value of the Medium of Account. So it is completely beside the point to rant on about a free market in production of the Medium of Exchange.

Now, I know in the past that you’ve talked about a gold standard, or perhaps an Account of a basket of precious metals. You need to realize that all the action on the blog, is about the Medium of Account. Stop wasting our time with free market “exchange” production. If you want to make a proposal, make a Medium of Account proposal. That’s the one that matters, for the ideas on this blog.

“When money is guided by market forces, there is no reason for a sudden massive drop in aggregate spending.”

We completely disagree. So you can’t just express this as an axiom. You need to support it, to defend it. Our historical evidence over the centuries, is that even when there was a gold standard, aggregate spending was highly volatile. So nobody believes your pure statement of this claim as an axiom. Surely you know, if you and your audience disagree about your “axioms”, then constructive communication is not possible. To be constructive, you need to back up to general principles that we all agree with, and being your argument from there. We don’t agree with this claim.

“In a free market, once money comes into existence, it tends to stay in existence. Massive deflation would be highly unlikely.”

And here, like most Austrians, you only think about supply. But any market has both a supply side, and a demand side. And floating prices (or, in the case of money, “value”). You’ve read this blog long enough. Surely it cannot escape your notice that Sumner’s big emphasis is the demand side.

You’re arguing that, in your design, that supply will be stable. That’s super. But the whole concern in this blog, is that money demand is not stable. And thus money value is not stable. Sumner’s NGDPLT is an attempt to stabilize money value over time, and thus avoid the negative consequences of volatile money value.

If you want to make a serious proposal, you must at least address the question of unstable money demand (and thus value). Going on and on about stable supply is completely irrelevant.

“if millions of people go into lines of work that are not conducive to the ends of consumers, then yes, they should change jobs, which of course means temporary unemployment.”

You’ve brought this up many times in the past, and already received the response (from me, among others): if your theory was true, then we would expect greater unemployment in some industries (the “lines of work that are not conducive…”), but simultaneously, increasing employment in other industries.

But that’s not the pattern we saw, in 2008. Instead, we saw increasing unemployment in every industry, at the same time. That doesn’t match your story, of “misallocation” of investment. But it does match the story of depressed NGDP and a sharp rise in the value of a dollar.

You can’t keep claiming your theory of misallocation, so in contrary to observed history, without at least acknowledging that we’re unable to find any of the jobs that these people should “change” into, you just sound completely out of touch and irrelevant.

“You could ask how is it possible for a worker to choose no wages rather than lower wages”

That’s not how the theory of sticky wages works. Instead, the scenario is: a company employs 10 workers at a given salary. Suddenly revenues drop by 10%. One choice is to give all workers a 10% pay cut. Instead, the choice selected (by both firms and employees) — for possibly complex reasons — is generally to maintain even wages for 9 employees, and to fire/layoff one employee. Who then cannot find a job at any wage.

Well, this comment has already gone on far too long. (Polite blog protocol is to keep comments short, on topic, and relevant to the original post. This very comment is an example of bad behavior.) So I’ll stop with my responses to your writing. But know that essentially every other sentence you write, is broken in a way very much like the ones that I’ve outlined. This is why you are unconvincing to this audience: because you’ve put so little effort into trying to construct a convincing argument. You just like to lecture, but not to convince.

Now, I assume that you actually aren’t a constructive, honest debater. But if by some miracle I’m wrong, then I expect your future posts to: (1) talk about the Medium of Account, rather than (just) the Medium of Exchange; (2) focus on the (shifting) demand for money (even if you think it will be stable) rather than just the supply of money; (3) explain why “malinvestment” causes unemployment throughout the whole economy, rather than just in the “wrong” industries; (4) show that you understand the details of the sticky wages (& prices) theories.

Note that none of this is about whether you are right, or Sumner is. It’s only about whether you’re honest enough in debate, to actually listen to the other side, and respond to their concerns. Are you actually trying to be constructive? Or are you just a troll?

Perhaps your writing will change, in the future. I won’t hold my breath.

28. December 2013 at 17:42

Don Geddis,

First of all, it’s not like there was some high-level debate going on. It’s a web-page, a bit of trolling won’t change anything.

Second of all – like I said above – you do not debate the austrians, just like you don’t debate creationist. Or pigeons (they’re in the same ballpark). They do not play by the same rules. They already have the answers, facts are irrelevant – I believe they call it “praxeology”.

And third of all – this Geoff fella is clearly missing (more than) a few nuts and bolts. Notice how he responds with a wall of text to a every single insulting sentence you throw at him.

Might as well have a little fun with him.

Wanna bet he’ll respond with another wall of text ?

28. December 2013 at 18:21

Don Geddis:

Your apology is accepted.

“Geoff, you write: “Laissez-faire in money production.””

“That only addresses money as the Medium of Exchange. Surely you’ve read this blog long enough to realize that the whole concern is about a change in value of the Medium of Account.”

Surely you’ve seen my countless posts explaining how medium of account is derived from medium of exchange. Money is that commodity which is exchanged indirectly for other goods, which has the consequence of people using it to tally their gains and losses in terms of that commodity, i.e. medium of account.

We do not require a central plan on what is to be the medium of account. A free market in money is the same thing as a free market in medium of account. People are not so stupid that they will use Bitcoins or gold as medium of exchange, but be totally clueless as to what commodity to use as a medium of account.

“So it is completely beside the point to rant on about a free market in production of the Medium of Exchange.”

No it isn’t. It is not besides the point at all. We don’t have to design a medium of account. A free market in money IS a free market in medium of account.

“Now, I know in the past that you’ve talked about a gold standard, or perhaps an Account of a basket of precious metals. You need to realize that all the action on the blog, is about the Medium of Account. Stop wasting our time with free market “exchange” production. If you want to make a proposal, make a Medium of Account proposal. That’s the one that matters, for the ideas on this blog.”

Do you even know what money is? Money is not the commodity that people track on their balance sheets that differs from the commodity they use as a medium of exchange. If some European companies are using US dollars as a medium of account, then this requires US dollars to be used as a medium of exchange.

People don’t use potatoes as a medium of account because they’re not a medium of exchange anywhere.

Your rebuttal is 100%, completely and totally irrelevant to the argument I am making. When I advocate for a free market in money, I am not claiming that any and all free market mediums of account are excluded. Let individuals decide how they want to calculate their gains and losses no less than allowing them to choose their own medium of exchange.

You are being misled by Sumner regarding this alleged dichotomy between medium of account and medium of exchange.

“When money is guided by market forces, there is no reason for a sudden massive drop in aggregate spending.”

“We completely disagree. So you can’t just express this as an axiom. You need to support it, to defend it. Our historical evidence over the centuries, is that even when there was a gold standard, aggregate spending was highly volatile.”

What historical evidence are you talking about? The historical evidence that has been conducted has shown that precious metal monetary systems do not undergo sudden massive drops in supply or spending. But even if it did, which it didn’t, then that would not in itself constitute justification to point weapons at innocent people preventing them from continuing to use such a commodity for money.

The evidence actually shows that when states interfere in money, by drastically increasing the supply of non-free market money, such as Greenbacks, or Continentals, or gold-backed pyramid scheme paper, that’s when we get those large deflationary periods.

“So nobody believes your pure statement of this claim as an axiom.”

That wasn’t an “axiom.” That was a historical argument subject to falsification by evidence, which doesn’t exist.

The only “axioms” that exist in economics are very modest. Action, costs, profits, losses, etc.

“Surely you know, if you and your audience disagree about your “axioms”, then constructive communication is not possible. To be constructive, you need to back up to general principles that we all agree with, and being your argument from there. We don’t agree with this claim.”

You don’t agree with action?

“In a free market, once money comes into existence, it tends to stay in existence. Massive deflation would be highly unlikely.”

“And here, like most Austrians, you only think about supply. But any market has both a supply side, and a demand side.”

And here, like most anti-Austrians, you conflate demand for quantity. Any individual who demands more money, requires another to demand less money. I can’t hold more money unless you agree to hold less money, and vice versa.

If both of us wanted to hold more money, then what we both want can be accomplished by falling prices. We don’t want more money to eat, we want more purchasing power.

If you wanted more money, but prices and spending rose all around you to the exact same extent, then your desires would be frustrated. You would have exactly the same purchasing power as before.

“And floating prices (or, in the case of money, “value”). You’ve read this blog long enough. Surely it cannot escape your notice that Sumner’s big emphasis is the demand side.”

It is precisely the lack of respect for the demand side that Sumner wants the central bank to reverse the effects of changes on the demand side. He wants money printing to be unlimited, to counteract ANY rise in demand for money holding no matter how large it is.

In this respect, he is willing to ignore the causes for why people would want to hold more money, by risking his solution to be more of what caused the sudden rise in the first place.

“You’re arguing that, in your design, that supply will be stable. That’s super. But the whole concern in this blog, is that money demand is not stable. And thus money value is not stable. Sumner’s NGDPLT is an attempt to stabilize money value over time, and thus avoid the negative consequences of volatile money value.”

That’s precisely why it is so destructive. Free market valuations of money are good. They are beneficial. They are needed. They should be allowed to run freely. Valuing money is an integral part of the function of money. If market actors are not free to value money, then market coordination is seriously hampered, and the desired outcome of “stability” is actually compromised. It is counter-productive.

The reason why the state “stabilizing” the exchange value of flour, or penicillin, would be so destructive, is the same reason it is destructive in money.

Stabilizing money is just an ex post rationalization that people have GIVEN that naked aggression has taken place in regards to money for the benefit of the aggressors. Sumner is intellectually compelled to come up with some intellectual reason, any intellectual reason, to justify the existence of the Fed, because if he didn’t, then his intellectual investment would be exposed as nothing but an apologia for aggression.

It’s why he is so relentless in getting people to believe in the gobbledygook of “stabilization.” Free association is not stable. Trying to force it as stable will only make it more unstable.

“If you want to make a serious proposal, you must at least address the question of unstable money demand (and thus value).”

Address it HOW exactly? Am I supposed to treat fluctuations in demand as an inherent evil the way you do before I am “approved” here?

Fluctuating money demand coordinates the economy in beneficial ways. I don’t see how violence is justified to stop people from peacefully making changes in their valuations in exchange.

“Going on and on about stable supply is completely irrelevant.”

No it isn’t. It is completely relevant. You just don’t want to hear it. That’s the difference.

“if millions of people go into lines of work that are not conducive to the ends of consumers, then yes, they should change jobs, which of course means temporary unemployment.”

“You’ve brought this up many times in the past, and already received the response (from me, among others): if your theory was true, then we would expect greater unemployment in some industries (the “lines of work that are not conducive…”), but simultaneously, increasing employment in other industries.”

And as I have repeatedly pointed out to you in response, many times in fact, no, that is NOT what is implied at all. When I say temporary unemployment, I mean it. I don’t argue that when someone loses their job, they will instantly and without any delay whatsoever, find work in another project.

It takes time for not only workers, but employers, to find the best uses for resources and labor, given that errors have been revealed.

When you assert that my theory requires zero drops in employment, that is, like I have argued before, a straw man.

It is a good thing when corrections are made to existing errors. I find it baffling how you can disagree with that. I also find it baffling that you expect no dips in employment before you call for the guns to be taken out of their holsters.

Seriously, what is so incredibly evil about someone temporarily losing their job due to consumers finding better products elsewhere, but living in a maximally free market in everything, such that they have maximal opportunity to find new employment as quickly as possible? What is so evil if more than one individual goes through this at the same time?

You’re not convincing me why guns are justified to keep people in jobs they should not be in.

“But that’s not the pattern we saw, in 2008. Instead, we saw increasing unemployment in every industry, at the same time. That doesn’t match your story, of “misallocation” of investment.”

Actually it does. You can’t expect misallocation of resources to take place alongside a counter-factual world that really exists, that enables those misallocated resources to instantly find new deployments.

Your counter-argument is untenable. Misallocation is fully consistent, indeed requires, “aggregate” idle resources and “aggregate” unemployment.

“But it does match the story of depressed NGDP and a sharp rise in the value of a dollar.”

It matches that story AS WELL.

“You can’t keep claiming your theory of misallocation, so in contrary to observed history, without at least acknowledging that we’re unable to find any of the jobs that these people should “change” into, you just sound completely out of touch and irrelevant.”

Misallocation is not “contrary to observed history.” The evidence is fully consistent with it.

You just have the mistaken notion that because there is a correlation between NGDP and employment, that falling NGDP causes falling employment. How do you know that falling employment doesn’t cause falling NGDP? Because the Fed can always reverse NGDP? NGDP contains consumer spending. NGDP can rise by increases in inflation induced addition to consumer spending, and no additional wage payment is made. That is possible. NGDP is not the finance source of wages. Wage payments precede that which those who receive wages spend their money on after. NGDP is a function of wage payments, not the other way around.

But even if unemployment did arise by virtue of a decline in aggregate spending, this is not sufficient justification to point guns at innocent people. If spending falls, then this means what is being produced, should not be produced in the way it is being produced. People hold money for longer because they’re waiting for better alternatives. Those alternatives are hampered when spending is forced back upwards.

“You could ask how is it possible for a worker to choose no wages rather than lower wages”

“That’s not how the theory of sticky wages works.”

That’s not how to answer questions. You don’t answer questions about economic theory by refusing to answer on account of it not fitting into your existing understanding.

“Instead, the scenario is: a company employs 10 workers at a given salary. Suddenly revenues drop by 10%. One choice is to give all workers a 10% pay cut. Instead, the choice selected (by both firms and employees) “” for possibly complex reasons “” is generally to maintain even wages for 9 employees, and to fire/layoff one employee. Who then cannot find a job at any wage.”

Why would the employer and/or employee agree to cease trading for any wage, instead of a lower one? Again, you’re not even asking the why that I said to Daniel he should be asking.

“Well, this comment has already gone on far too long.”

Too bad. Your points are still as flawed now, as they were back when you said them the first time.

Maybe you’ll eventually do some more research.

“Now, I assume that you actually aren’t a constructive, honest debater.”

False. I am honest and constructive.

“But if by some miracle I’m wrong, then I expect your future posts to: (1) talk about the Medium of Account, rather than (just) the Medium of Exchange; (2) focus on the (shifting) demand for money (even if you think it will be stable) rather than just the supply of money; (3) explain why “malinvestment” causes unemployment throughout the whole economy, rather than just in the “wrong” industries; (4) show that you understand the details of the sticky wages (& prices) theories.”

I am still waiting for you to show you understand how a free market in money works.

“Note that none of this is about whether you are right, or Sumner is. It’s only about whether you’re honest enough in debate, to actually listen to the other side, and respond to their concerns. Are you actually trying to be constructive? Or are you just a troll?”

Are you someone who will continue to refuse to engage the ideas, and instead demand that I accept your ideas?

Time will tell.

Perhaps your writing will change, in the future. I won’t hold my breath.”

28. December 2013 at 18:22

Daniel:

Another post, another absence of rebuttals.

29. December 2013 at 10:01

Re: Medium of Account. OK, so you also want a free market in MOA. So some currency will use gold, some a basket of metals, some fiat, etc. It is my intuition that a lack of standardization will cause friction in transactions, much like the arbitrary difference between English and metric measurements. So I don’t yet support this change, but I’m open to being convinced. You should start your own blog and try to present your case.

In any case, this doesn’t need to be a source of disagreement, right? Why can’t you consider Sumner’s NGDPLT with fiat money, merely as one possible competing form of “money” among all the ones that might be created? There’s a whole separate question of your “guns” and “force” complaints, but you can easily imagine that the government merely offers dollars, but doesn’t force a monopoly. (Except perhaps for taxes, but then, even in your world, everybody is allowed to choose the kind of money they want to use for transactions. The US government will choose fiat dollars. Surely that is still allowable, even in your free market money world.)

“The historical evidence that has been conducted has shown that precious metal monetary systems do not undergo sudden massive drops in supply or spending.”

Demonstrably false. I see a huge number of historical recessions, just in the US, just in the last couple centuries, despite being on a gold standard or free banking. Now, you may believe some crazy ABCT explanation for the “sudden massive drops” in output (and spending), but the fact that the drops happen is not at all controversial.

People here believe that carefully managed fiat money can greatly reduce these business cycles and thus improve the welfare of society. Your claim that a steady money supply would have the same effect, is disproved by historical evidence. To be taken seriously, you need to at least address this evidence.

“Any individual who demands more money, requires another to demand less money.”

Not at all. Do you know simple MICROeconomics? A demand curve is just an individual’s preferences, about how much quantity they would want, at various possible prices. And individual’s demand curve can change on its own, without affecting anyone else.

The point is that money itself has demand as well, and you never seem to consider that in your writings, but it’s the primary concern here.

And it’s easily possible for everyone’s demand for money to rise at the same time. (Velocity goes down.)

“Free market valuations of money are good.”

Nobody believes you. You can’t just assume this. If you want to make progress in communication, you need to present convincing arguments for those areas where there is not yet agreement.

In this case, taking out a 30-year mortgage, the homeowner and the bank agreeing on a nominal repayment three decades from now … and then making the value of that repayment highly volatile and unpredictable … I can see no benefit, only harm, from money value volatility. Perhaps your idea of unpredictable value is better, but you can’t just assume this; you need to explain and convince.

“The reason why the state “stabilizing” the exchange value of flour, or penicillin, would be so destructive, is the same reason it is destructive in money.”

I wonder if you’ve really thought this through. One obvious difference, is that there is no separate market for money value, so if the value of the MOA changes, this can only happen by the hassle of millions of individual prices changing. (There is tremendous wage and price stickiness in the money value market, unlike the liquid markets in commodity trading.)

Secondly, flour and penicillin supply is constrained by real-world limited resources. But the nominal quantity of money is arbitrary. The Fed can produce any amount we choose, at no cost.

It is precisely because there are important differences between money, vs. flour and penicillin, that the best approach to managing them is so different.

“Am I supposed to treat fluctuations in demand as an inherent evil”

All this time you’ve spent on this blog, and you still don’t understand the basic problem that is being solved?

Total spending is MV. Velocity is unstable. When spending drops, the value each dollar rises. To bring every market back into equilibrium, all posted prices must fall, in order to return to the same real value being exchanged. But some prices (esp. wages, but also others) are “sticky”, and slow to change. The obvious, natural result of wages being too high in value, is a significant drop in labor purchases (i.e., massive unemployment). And thus also a drop in productive output.

We can see no benefit, to people being forced to be idle instead of productive, due solely to the value of money rising, but wages having too much inertia to quickly adjust to equilibrium.

This problem appears to be easily solved, merely by keeping the value of money more stable. (By adjusting M, to match any changes in V.)

None of your proposals address the unnecessary unemployment and fall in output. You make proposals that don’t solve this problem, and so of course everybody ignores you as irrelevant.

“Fluctuating money demand coordinates the economy in beneficial ways.”

This assertion just isn’t believed. We see the pain of forcibly unemployed people. We see the drop in productive output of valuable goods. We know that is suffering. We don’t see any benefits, much less sufficient benefits to overcome the obvious costs.

You can’t just assume these things. If you want to be constructive, when your perspective is so different from that of your readers, you need to explain and convince about these underlying assumptions.

“I don’t argue that when someone loses their job, they will instantly and without any delay whatsoever, find work in another project. … When you assert that my theory requires zero drops in employment”

It seems that you didn’t read very carefully. I never said that unemployment should have zero delay, nor that there should be zero unemployment. You completely missed the criticism. Let me highly the important part again: “we would expect greater unemployment in some industries, but simultaneously, increasing employment in other industries”

The problem with your malinvestment theory, is not the unemployment in some industries. It is the LACK of extra employment in ANY industry. There is no industry that people were moving “in to”. EVERY industry suffered increasing unemployment. THAT is what you need to address and explain.

Unemployment is fine. Economy-wide unemployment is not a prediction of your theory, yet is what we observed historically. But you constantly repeat your claims, never even acknowledging or addressing the obvious contradiction.

“People hold money for longer because they’re waiting for better alternatives.”

Another unsupported assertion that we don’t believe. Velocity changes, yes … but for complex reasons. Your simple sentence doesn’t capture it.

“I am still waiting for you to show you understand how a free market in money works.”

I’m not an expert on a money free market. But that isn’t the topic of this blog. This blog compares possibly structures for the Fed, e.g. discretion, or inflation targeting, or a Taylor rule, or NGDPLT. Look at the pros and cons of each choice, and try to figure out what would be best for the US economy and its citizens.

You are rudely hijacking this space for your own pet interests. If you have an off-topic passion, you should start your own blog space to argue and discuss, not disrupt the space here, which is trying to be productive and constructive on a much more narrow and focused topic.

“Are you someone who will continue to refuse to engage the ideas, and instead demand that I accept your ideas?”

This is not the place, to engage your ideas. I also don’t demand that you accept my ideas. All I’m suggesting, is that if you really intend to be polite and constructive, you need to take efforts to meet the readers here halfway, instead of just repeating off-topic lectures based on assumptions that nobody here shares.

29. December 2013 at 13:17

Don Geddis:

“Re: Medium of Account. OK, so you also want a free market in MOA. So some currency will use gold, some a basket of metals, some fiat, etc.”

Put it this way. I want you, Don Geddis, to be able to use whatever commodity you own to make exchanges, and, as a corollary, what commodity you use to track your gains and losses. I would find it terribly uncivilized for me to impose my preferred money commodity on you by force, by threatening you with violence if you don’t comply. That includes demanding that you pay me a percentage of your income to me, in the form of the commodity I prefer, say gold or Bitcoins, at the punishment of your ultimate death if you should defend yourself from my aggression.