Don’t look now, but monetary policy is tightening dramatically

While most of the economics profession seems to assume that a Fed cut in interest rates means money is getting easier, policy has dramatically tightened in recent weeks.

Perhaps the most startling data point is the expected level of interest rates in the fed funds futures market, which has plunged to barely over 1% in 2021. Consider that figure to be a prediction that NGDP growth in 2021 will be weak enough to justify such a low policy rate. Sorry, no more “one and done”.

Yes, it’s likely that the low expected rate partly reflects some factors unrelated to US NGDP growth, say global weakness, but I wouldn’t count on that explaining all of the drop. Lots of other indicators also point to slowing growth in NGDP. Five year TIPS spreads are down to 1.41%, consistent with roughly 1.15% PCE inflation. Again, TIPS spreads are somewhat biased, but do contain at least some information about inflation expectations. Stocks are also selling off, albeit from a fairly high level. While no single indicator is definitive, the overall picture is of a decline in aggregate demand (and aggregate supply as well.) We are seeing the income and Fisher effects in action.

It’s now pretty clear that the Fed should have cut rates by 0.5% last week. In fairness, the latest demand shock came from the renewed trade war, which occurred after the meeting.

The lesson here is that the Fed should adopt my proposal to adjust its fed funds target daily, to the closest basis point. Time to join the 21st century.

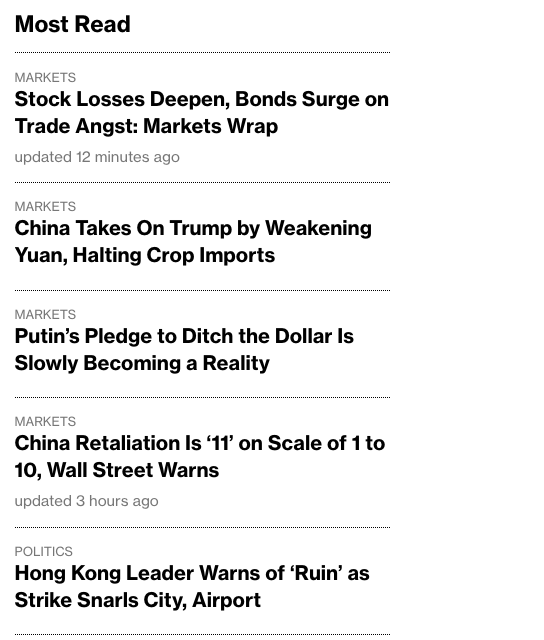

Update: When the news starts to look like this:

Update: When the news starts to look like this:

It’s not a good sign. Oh, and Boris Johnson seems determined to drive the UK into a hard Brexit, while the Eurozone continues to be dysfunctional.

Have a nice day!

Tags:

5. August 2019 at 09:03

Very good, timely, and important post. Powell can’t wait until next meeting, he needs to issue reassurances to the markets that the Fed is aware of recent developments and poised to act as aggressively as needed.

5. August 2019 at 09:20

Yes, the dramatic fall in the yield curve is also a signal of much tighter money. I disagree about stock prices having been at a high level. High level for earnings expectations versus interest rates?

The Fed needs to signal more rate cuts are coming soon, but they are never timely, as you point out.

I’m curious, do you think this rather stiff slap from China makes it less likely Trump can find what he considers a face-saving deal?

And it won’t matter if China decides they no longer want one. They may decide it’s in their interests to try to make sure Trump is defeated.

5. August 2019 at 09:30

By the way, it’s looking increasingly like you were right about China being in a better position to “win” this trade war. It seems its easier for them, for example, to find alternative sellers of agricultural products/substitutes, than for the US to find a market large enough to replace theirs. There are other facets of this fight, but this prediction is looking good.

5. August 2019 at 10:14

If there is a plunge in asset prices, what can the Fed do to stop it, what can the Fed do to re-inflate asset prices, what can the Fed do to help banks rebuild their balance sheets? This is the dilemma one can face when one relies on rising asset prices (and low interest rates to maintain rising asset prices) as the path to prosperity. Quantitative easing may take on a whole new meaning if asset prices plunge. How so? By the Fed buying not only bonds, but equities too. But which equities to buy (my criticism of Farmer’s idea)? Ask Trump. These are interesting times.

5. August 2019 at 10:27

Rayward, Do even read my previous replies?

5. August 2019 at 10:37

Recession odds are sharply rising. What a mess.

5. August 2019 at 10:41

So, you think this is another “passive tightening” just like the summer of ’08 when the Fed left the FFR at 2% despite a drop in the equilibrium rate? We’ll have to see what the results will be.

5. August 2019 at 10:44

Cameron, I agree.

Paul, The past week is definitely passive tightening.

5. August 2019 at 10:49

So what is your interpretation of the large stock market drop today? Is it an anticipated escalation of the trade war in response to the Chinese currency “devaluation”? Because it doesn’t seem like the currency devaluation should have such a negative impact on stocks in and of itself.

5. August 2019 at 10:55

Well, can more aggressive (easier) monetary policy avert the disaster? I hope so. But if disaster hits, and the perfect storm seems to be building, I’m not confident the Fed has the tools to deal with it nor am I confident in Mnuchin (and his boss). And yes, I do read your replies. And yes, I (almost always) agree with your policy prescriptions. And yes, I would have greater confidence if you were on the Fed. My view about reliance on rising asset prices isn’t meant as a call for tighter monetary policy, it’s a call for doing something else to achieve prosperity (something else to increase investment in productive capital). We’ve dug ourselves into a hole, a futures market that screams monetary easing but in a time of very low interest rates. Again, my concern is a plunge in asset prices. I don’t see how to recover from the plunge. Sure, quantitative easing, including purchases of equities even, but the political fallout would be enormous. With the buffoon in the White House, every action would be seen by him as his Waterloo. Disaster looms.

5. August 2019 at 11:09

Scott, but we don’t see most of the other indicators of tight financial conditions. Inflation expectations, measured by Treasury prices, have fallen, but not very sharply, and not by amounts so as to be worrisome. Stock prices have fallen, but that’s been the story of the last 2.5 years every time Trump announces a new idiotic round of tariffs. Economic activity is slowing, but that’s a reversion to trend only broken by market jitters in 2018 following a big Republican-backed tax cut.

5. August 2019 at 14:08

Does the Fed have the legal authority to change rates on a daily basis? Does it have the technical ability (and I don’t mean technology wise, but institutionally, can they agree on a process to set the rates on a daily basis, and then let management set the rates)? What does the Board of Governers and FOMC do after such a switch? How often do they meet? How markets react to (and game) the new regime?

The main thrust of the questions are to point out that the Fed is essentially a government bureaucracy, and changes to a government bureaucracy are difficult to do, not only because they often require changes in law, but also for the mundane reason that change in any large organization is difficult to accomplish, and especially so if top managers aren’t unanimous in their desire to implement the change and consistent in their vision.

5. August 2019 at 16:47

Policy wank, You said:

“Because it doesn’t seem like the currency devaluation should have such a negative impact on stocks in and of itself.”

Yes, that’s pretty clear. It looks like risk of escalation.

Rayward, If you read my replies and then ignore them, that’s even worse.

Paul, Five year TIPS spreads are down to 1.41%, implying 1.15% PCE. I don’t expect inflation to be that low, but it fits the general picture. You are right that the LEVEL of stocks does not imply a recession, but market moves in the last week are signaling increased risk.

Burgos, The Fed can change rates whenever they wish. I’ve suggested that each FOMC member email in their preferred target daily to the nearest basis point, and the policy rate be set at the median vote.

Yes, Bureaucracies change slowly, but the Fed did a number of innovations in 2008, and could do so again.

6. August 2019 at 08:30

The Fed should cut to a range between 1.75%-2.00%. That should raise the rest of the yield curve such that it would be more or less flat. Barring trying to clamp down on excessive inflation, the Fed should never cause the yield curve to invert. Aside from that, I maintain that if they’re going to do inflation targeting, they shouldn’t allow market based inflation expectations to drift very far from 2%.

I worry that there might be a rational expectations effect on demand via the yield curve shape. We might see a reduction in aggregate demand if enough people expect a recession and act accordingly.

6. August 2019 at 08:35

Justin, I’d favor an even bigger cut.

6. August 2019 at 17:44

@SSumner

If the fed has the legal authority to set rates on a daily basis, then why do the Fed governors prefer to do so on something more like a quarterly basis? If they can set the rate at just the median preferred rate of the voting governors, then why had the Fed proffered to hew closer to setting rates only after reaching consensus? If what you write makes so much sense, and the Fed has the legal authority to implement your ideas, why does the Fed take 10 years or more to even come part way around to your (market monetarist) views? Is there value to understanding the Fed from a more political economy, behaviorist, or public choice point of view. Because either the governors have very different beliefs about monetary policy and macroeconomics than market monetarists, or the governors are thinking about things in addition to monetary policy and macroeconomics when they make decisions, or they are simply making irrational decisions.

6. August 2019 at 21:23

Burgos, Those who accept the status quo as a given never have any impact on policy . I hope to have an impact on policy.

The Fed has occasionally changed its policy approach in the past, why should I assume that they would not do so in the future?

7. August 2019 at 00:31

@ SSumner

Thanks for the response. That strategy probably makes more sense than trying to change opinions at the Fed; it is probably easier (and less frustrating) to explain a better way of doing things so that it is available when the Fed is ready to change.

7. August 2019 at 07:08

“Lots of other indicators also point to slowing growth in NGDP.”

Is there a website that charts the NGDP?

thank you

7. August 2019 at 12:16

AP, FRED shows recent NGDP data, and Hypermind plans to create a NGDP futures market later this year.

8. August 2019 at 05:02

It’s sad to say, but it never even occurred to me it was not a lie.