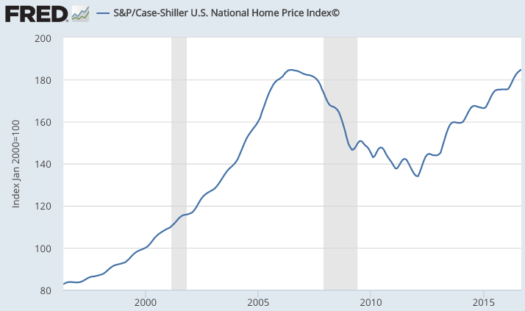

Real house prices are still well below the peak, but nominal prices hit a record high in September:

The 2006 period may have been a bubble, but as of today is seems far less irrational than it seemed in 2012. (This recovery also makes Kevin Erdmann’s arguments look even stronger.)

The world’s full of uncertainty and markets are volatile. Get used to it.

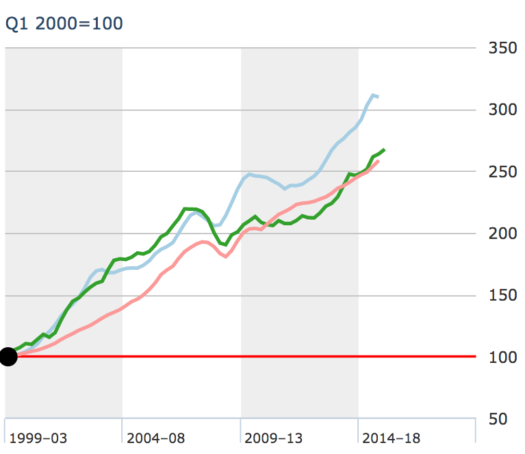

PS. UK house prices (green) took a dip after 2006, but are now well above 2006 levels (and equal to 2006 prices in real terms). Australia (blue) and Canada (pink) are much higher in both real and nominal terms.

What goes up must eventually . . . go up even more!

So the US is down in real terms, the UK is even, and Canada and Australia are up in real terms. Isn’t that sort of consistent with the EMH?

Sure, those prices will dip at some point in the future. That’s what efficient markets do, they go up and down.

If the British keep shooting themselves in the foot, before long they are going to run out of toes. Here’s the latest outrage:

“THEY are not, and never have been, immigrants.” So declared Enoch Powell of international students in an infamous speech against migration in 1968. Ending up to the right of Powell, who was as fierce a critic of immigration as they come, is an uncomfortable position. But that is where Theresa May’s government finds itself with respect to overseas students. As part of a plan to reduce the number of migrants, on October 4th Amber Rudd, the home secretary, announced new restrictions on foreign students, including tougher entry requirements for those going to lower-quality institutions. The proposal is merely the most recent attempt to deter foreigners from paying tens of thousands of pounds to study in Britain.

Since the turn of the century the number of foreign students in Britain has more than doubled (see chart). In contrast to Britain’s overall immigration trend, growth has come not from Europe but from the rest of the world. Chinese students are by far the biggest group, numbering 89,540 last year, up from 47,740 in 2004. The steep fees paid by non-EU citizens have made higher education an important British export. By one estimate foreign students contribute £7 billion ($8.6 billion) a year to the economy in fees and living expenses.

. . .

Other countries spy an opportunity. Australia and Canada, popular alternatives for Asian students seeking an English-language education, offer (limited) chances to stay and work, making them attractive destinations. Australia has simplified its student visa system to boost its appeal. Germany is offering more courses in English. And since 2014 public universities there have largely abolished tuition fees, including those for foreigners. This month the Irish government revealed plans to encourage more foreign students. “Everybody is doing the exact opposite to us,” laments Ms Owen Lewis. While the number of foreign students in Britain has stalled, in other countries it is zipping up. In Australia it increased by 11% last year.

Nor does the crackdown look politically necessary. A YouGov poll last year found that students were the most popular group of migrants among voters, three-quarters of whom thought their numbers were about right or should be higher. Even supporters of the right-populist UK Independence Party were keen on them. Reducing immigration in general will hurt Britain’s economy; barring fee-paying students is a particularly damaging way to do it.

Wow, Theresa May has ended up to the right of both Enoch Powell and the UK Independence Party. I opposed Brexit out of fear that it would open the door to right-wing nationalism, but even I never dreamed that it would end up being this bad.

Europe May Finally End Its Painful Embrace of Austerity

And here’s the claim:

As Europe has grappled with the trauma of a devastating financial and economic crisis, policy makers have consistently relied on one approach to managing the damage — budget austerity.

Shrink government spending by trimming pensions and cutting social programs, the logic runs, and the markets will gain confidence in the tough-minded people in charge. Confident markets make for happy markets. Money will pour in, and good times will roll.

Even as prosperity has remained painfully elusive across much of Europe, leaders have time and again renewed their faith in the virtues of this harsh medicine.

Until now.

Some policy makers are flashing tentative signs that they may be prepared to slacken their grip on public coffers to spur growth and improve the lot of ordinary people suffering joblessness and diminished wealth. In the clearest sign of this shift, the heavily indebted Italy is increasingly inclined to challenge Germany — the guardian of austerity — to loosen European purse strings.

Of course everything is relative, and European fiscal policy has not been particularly austere. But even so, can we assume that a slackening of “austerity” will boost growth? Veronique de Rugy of the National Review reports:

The Congressional Budget Office recently released its Monthly Budget Review for September 2016. It includes a revised estimate of the deficit for 2016. It isn’t much different than the one projected in August. The document makes it hard to ignore that in 2016 the deficit grew by $149 billion, from $439 billion in 2015 to $588 billion at the end of FY2016. This explains why we haven’t heard president Obama brag about how the deficit is shrinking in a while.

Normally the deficit falls during expansions. How did the economy respond to this loosening of “austerity”? RGDP growth slowed to less than 1.3% during the past four quarters, as the Fed tightened policy. As a result of our foolish fiscal policy, fiscal authorities will now have less room for “stimulus” during the next recession, as the deficit will be starting from a higher base. Of course this will come as no surprise to readers of this blog. The austerity of 2013 (when the deficit plunged from about $1,050 billion to about $550 billion between calendar year 2012 and 2013), coincided with an increase in GDP growth. But like Chicago Cubs fans, Keynesians never give up hope.

Now let’s look at the UK:

Before the June 23 vote for “Brexit,” the man in charge of the budget, the chancellor of the Exchequer, George Osborne, was publicly pursuing the aim of delivering a budget surplus by 2020. The target required cuts.

But as the political class absorbed the ballot result, interpreting it as a demand for redress from communities reeling from high unemployment and wage stagnation, Mr. Osborne acknowledged that his goal could no longer be achieved.

His successor, Philip Hammond, has raised the ante.

In a speech at an annual gathering of the governing Conservative Party on Monday, the new chancellor declared that the government would borrow more to finance new infrastructure projects — presumably creating construction and manufacturing jobs.

While reading this, I spied a link in the right column, to another NYT story, this one from May 25th:

‘Brexit’ Could Spell More Austerity for Britain, Study Warns

That’s pretty scary, but could the prediction be trusted? The NYT says yes:

LONDON — Prime Minister David Cameron’s campaign to keep Britain in the European Union was bolstered on Wednesday by a report from one of the country’s most authoritative economic research bodies, which concluded that a withdrawal from the bloc would lead to up to two more years of public spending cuts or tax increases.

A frequent critic of government economic plans, the research body, theInstitute for Fiscal Studies, this time delivered some welcome news for Mr. Cameron.

Of course it could be trusted (the NYT signals), it came from “one of the country’s most authoritative economic research bodies”, which is also “A frequent critic of government economic plans”. So we aren’t talking about one of those nutty right-wing outfits, like the Adam Smith Institute or the IEA.

NYT readers never need fear leaving their cosy intellectual cocoon, where fiscal stimulus produces growth miracles, and a continent where governments spend 50% of GDP is struggling because of “austerity.” Yes, the Trumpistas are even worse (and also oppose austerity), but then I don’t expect much from the “stupid party”. I do expect more from the Times.

In recent months, right wing nationalists such as Donald Trump and Theresa May have criticized the low interest rate policies of the major central banks. This may reflect the fact that a core part of their political support comes from grouchy old people, who are frustrated by the low interest rates earned on their savings accounts. Saturos sent me the following:

Mark Carney said on Friday that he would not “take instruction” from politicians after Theresa May warned that there had been “bad side effects” due to Bank of England policies.

In comments which risk an unprecedented clash between the Governor of the Bank of England and the Prime Minister, Mr Carney said that “it can be difficult sometimes if there are political comments on our policies”.

Carney explained the distinction between tactics and goals:

“The objectives are what are set by the politicians. The policies are done by technocrats. We are not going to take instruction on our policies from the political side.”

The UK government quite properly sets the objectives (such as the inflation target) and then leaves the tactics up to the BoE, which is independent of the government. A few hours later the May government retreated like a dog with its tail between its legs. Here’s the FT:

Theresa May’s allies have tried to cool speculation about tensions with Mark Carney, insisting the prime minister would be delighted if the Bank of England governor decided to serve his full eight-year term until 2021. . . .

Mrs May’s comments caused concern at the Treasury and the BoE because theyappeared to suggest the government wanted to set monetary policy, although Treasury insiders say this was a misunderstanding and stemmed from naive drafting of Mrs May’s speech.

Philip Hammond said he hoped the governor would remain in Threadneedle St until 2021 to act as a stabilising influence as Britain leaves the EU. One Treasury insider said: “Nobody inside Number 10 seemed to get how her words might be interpreted.” Mr Hammond wants to dampen pre-Brexit concern in the City of London and did not welcome Mrs May’s intervention.

But the prime minister is said by her aides to be fully supportive of the governor.

That’s more like it. (Her aides seem only slightly more competent than Trump’s. OK, I’m just kidding–May is 1000 times better than Trump.)

In these circumstances, it is hardly a surprise that investors are marking down the UK’s economic prospects by selling its currency. The government says it will not provide a running commentary on Brexit ahead of next year’s negotiations with the rest of the EU. But the faster that Mrs May’s government provides some clarity about exactly what it is aiming at the better.

Over at Econlog I’ve done a number of posts discussing whether this major “uncertainty shock” will cause a recession in the UK. In my initial post I suggested that the shock would hit RGDP harder than unemployment. I’m sticking with that prediction for now, but will keep an open mind. I believe that sharp increases in unemployment are usually due to demand (i.e. monetary) shocks, and that real shocks cause pain spread out over a longer period of time, affecting GDP more than employment (unless the real shock is specifically directed at the labor market, such as a higher minimum wage.) I believe the fall in the pound is signaling slower long-term British growth, but I still doubt whether we will see a sharp rise in the UK unemployment rate in the next 6 months.

PPS. I’m allowed to make bigoted statements about grouchy old people, because I am one.

Britain’s services sector, which accounts for more than 75% of the country’s GDP, continued its recovery from the initial shock of the Brexit vote in September, according to the latest PMI data from IHS Markit, released on Wednesday morning.

It completes a trilogy of much better than expected post-Brexit economic figures released this week, following strong growth in the manufacturing and construction sectors.

Every major constituent of UK economy has now staged a huge comeback following a massive drop in the immediate wake of Britain’s vote to leave the European Union.

Over the last couple of days, both the manufacturing and construction sectors came in substantially higher than had been expected, suggesting once again that the early uncertainty after the Brexit vote has now almost completely worn off.

This perfectly epitomizes the lack of accountability in economics. Let’s review:

1. After Brexit the media was full of breathless reports that “uncertainty” over Brexit was the biggest shock to hit the UK since WWII. We were told a recession was likely. The opinion makers fully understood that Brexit itself was at least two years away. The expectation was that Brexit uncertainty would be a massive confidence shock for the UK, causing investment to tank.

2. The early data is beginning to look increasingly positive, although in my view it’s still too soon to tell. We’ll know soon enough—maybe 4 to 8 months.

3. Almost none of the uncertainty regarding Brexit has been resolved. If anything, recent reports have been on the negative side—toward the sort of scary and uncertain “hard Brexit” that was expected to be especially devastating for investment. Yes, Theresa May did set a date to begin negotiations, but that was just a few days ago and had no impact on the recent macro data.

Notice that the article says that:

Over the last couple of days, both the manufacturing and construction sectors came in substantially higher than had been expected, suggesting once again that the early uncertainty after the Brexit vote has now almost completely worn off. (emphasis added)

My response:

You don’t get to say that. If the UK economy is doing well post-Brexit vote (and I’m still not 100% sure it is, but I think it’s plausible that it is) then it suggests that uncertainty doesn’t matter.

The policy uncertainty that the UK faced three months ago has absolutely not gone away, and that’s not even debatable. If the UK is doing fine, it means that something else drives the business cycle, not uncertainty. What could that something else be? Here are my top 6 prospects:

1. NGDP/monetary policy

2. NGDP/monetary policy

3. NGDP/monetary policy

4. NGDP/monetary policy

5. Labor market regulations

This lack of accountability is a much more general problem in macro and finance. People are not held accountable for their views. Just the other day a commenter gave me a hard time for making fun of Jim Chanos’ China predictions. Chanos has been predicting a Chinese real estate crash for a number of years. Instead, the Chinese real estate sector is booming. The commenter’s response was that Chanos had made some money shorting Australian mining stocks. Well that’s fine, but people need to be held to account for their actual predictions. If I make multiple predictions, then it’s likely at least some of them will come true. Chanos wasn’t famous for his views on mining stocks; he was famous for his forecast of a China crash.

This is a general problem. Nobody wants to be held accountable for their predictions. Over at Econlog, I admitted that the knee jerk reaction of the UK stock market to Brexit seems to have been wrong, and since I’m an EMH guy, that’s a loss for me. I’m on record predicting a 0.5% rise in the UK unemployment rate next year, and if that does not occur I’ll point it out next year and admit I was wrong. It’s important to learn from your mistakes.

In the end, I see the Brexit vote as being part of an epic global struggle of narrow-minded nationalism versus enlightened cosmopolitan neoliberalism. Elsewhere the issues are much starker, and the white hats and black hats are much easier to spot. But it’s the defining issue of our time, just as it was the defining issue of the first half of the 20th century. (This is not to imply that all Brexit fans are narrow-minded nationalists—I respect many supporters of Brexit—just that the issue has become tangled up in the global swing toward nationalism.)

I did not cite a fear of recession, rather that the UK would move away from neoliberalism. The FT is giving a lot of attention to Theresa May’s recent speech. If I had to sum up the speech in a single sentence, it would be that May is determined to move the UK sharply away from the neoliberal policies of Cameron/Osborne. She wants lots more nationalism and also some additional statism. Some British classical liberals seemed to feel that Brexit would allow the UK to become another Hong Kong. May’s vision is about as far from Hong Kong as it’s possible to be, and still be on the “conservative” side of the political spectrum.

Can nationalism ever be combined with libertarianism? I suppose it’s theoretically possible. But I’ve never seen it, and don’t expect I ever will. For some reason, nationalism and statism seem joined at the hip.

Welcome to a new blog on the endlessly perplexing problem of monetary policy. You’ll quickly notice that I am not a natural blogger, yet I feel compelled by recent events to give it a shot. Read more...

My name is Scott Sumner and I have taught economics at Bentley University for the past 27 years. I earned a BA in economics at Wisconsin and a PhD at Chicago. My research has been in the field of monetary economics, particularly the role of the gold standard in the Great Depression. I had just begun research on the relationship between cultural values and neoliberal reforms, when I got pulled back into monetary economics by the current crisis.

"Couldn't find the substack and if it's moderated just as well... Voted for Trump and he won. Sorry liberal Scott Sumner who believes in money non-neutrality, which is akin to..."

"Scott, Quick note of thanks. I've hugely enjoyed your blog and the intellectual stimulation I gotten from it. Also it was pleasure getting to know you and your wife. Hope..."