Build the NGDP and businesses will come with the goods and services

This recession may well end up being worse that the Great Recession. But it probably doesn’t have to be:

1. The recession will certainly be deeper than the Great Recession, indeed it probably already is. But deeper doesn’t mean worse.

2. The recession may have to be worse than the Great Recession, if the medical situation turns out to be far worse than I expect.

3. However, if the medical situation turns out to be about as I expect, then we could have economic growth in the second half of 2020, and full employment in 2022.

I say, “could have” because it will also depend on monetary policy.

In my view, the most likely medical outcome is a sharp reduction in new caseloads in May. There will also be improvements in PPE for workers and lifestyle changes will persist. This will allow some (but not all) businesses to begin reopening, starting in May. Then, sometime in 2021, we will likely have a vaccine or drug treatment or vastly improved PPE, or some combination that allows for a more normal economy. I’m not certain this optimistic scenario will be correct, but I suspect something will turn up, given the enormous pressure to solve the problem. So I believe it’s more than 50% likely.

The point of this post is not to give you my worthless predictions on the coronavirus, rather to point to some misconceptions I see in the media. One theme is that it may be difficult for the economy to recover once the medical crisis is over, because firms have gone bankrupt. Nonsense.

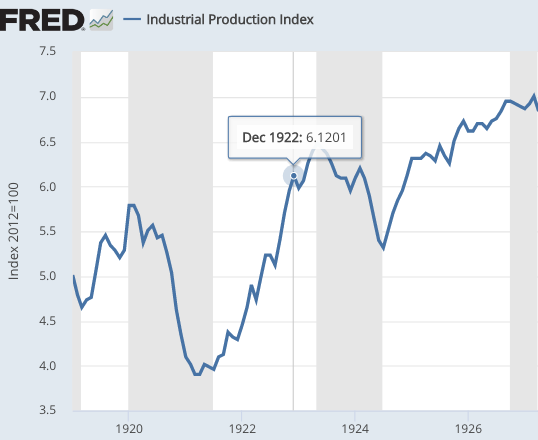

US economic history is full of examples of explosively fast recoveries when the initial problem is no longer impacting the economy, and even when it is (as in March-July 1933, a period when much of the banking system was shut down.) A good example is the extremely fast 1921-22 recovery. In July 1921, we were at the bottom of a very deep recession, and by December 1922 we were booming—“the Roaring 20s”. How about having an extremely fast 2021-22 recovery!

The 1921-22 recovery was aided by a great deal of wage flexibility, more than we have today. But we have the advantage of a fiat money system and hence can print enough money to get NGDP back up to the trend line by 2022. We don’t need wage flexibility. And we certainly don’t want a repeat of the needlessly anemic recovery from then 2008-09 slump.

I cannot emphasize enough that in the absence of a shutdown for medical reasons, our economy is capable of rapidly returning to full unemployment if the Fed provides adequate NGDP. Recall the movie line, “build it and they will come”. I’d say, “Build the NGDP and businesses will come with the goods and services.”

Don’t believe the pessimism; we should expect and indeed demand that the Fed provides adequate NGDP once the epidemic is over. If the economy is not at full employment in early 2022, it will likely be because NGDP is not 8% above 2020:Q1 levels, not because of mythical “hysteresis”.

Jay Powell seems to have his heart in the right place:

Jay Powell said the Federal Reserve would use its powers “forcefully, proactively and aggressively” until the economy recovers from the coronavirus shock, as the US central bank moved to offer an extra $2.3tn in credit and support the market for high-yield corporate debt.

But good intentions are not enough; we need level targeting, announced ASAP.

PS. Bonus prediction: This summer the media will begin dividing countries up into safe and infected categories. The safe category will include Australia and New Zealand, China, Taiwan, Vietnam, Iceland and a few others. Soon South Korea, Hong Kong and Norway will join the list, and then gradually more and more countries. By “safe” I mean community transmission of less than 2 cases per week. There will be a lot of chatter in the media about how to move from the infected to the safe category, and a lot of political disagreement on the topic.

PPS. In the US, the epidemic began in western states. Today, the epidemic is dramatically worse in states east of the Texas/Louisiana border, even accounting for population.

Update: Just as France was hit much harder than Northern Europe, Quebec is being hit much harder than the rest of Canada. Then there’s Louisiana . . .

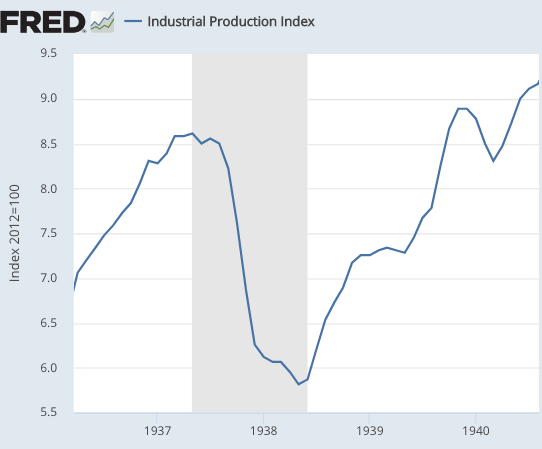

PPPS. The recovery from mid-1938 to late-1939 was also very rapid, despite a pause after minimum wages were enacted in the fall of 1938:

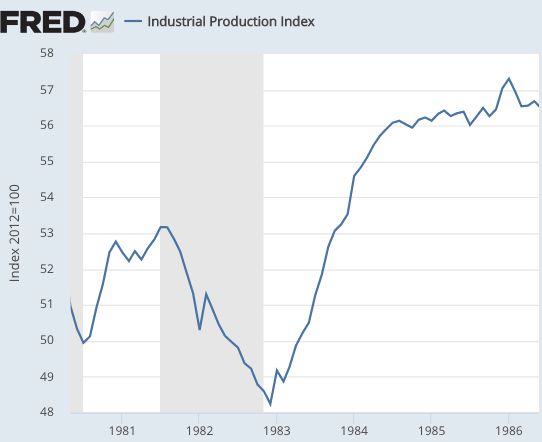

Or how about the rapid recovery during 1983:

Or how about the rapid recovery during 1983:

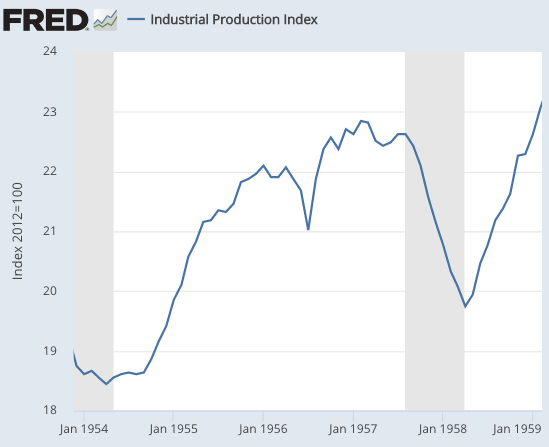

Or how about 1958:

Tags:

9. April 2020 at 11:03

Scott, to what degree does price level targeting contradict NGDP level targeting in this situation? Price level targeting is compatible with both high and low NGDP.

9. April 2020 at 12:26

Doesn’t the Singapore situation suggest periodic lockdowns might be necessary until a vaccine? If I’m reading that right then how could we possibly have a quick economic recovery pre-vaccine?

9. April 2020 at 12:56

“If the economy is not at full employment in early 2022, it will likely be because NGDP is not 8% above 2020:Q1 levels” how can there be any expectation of make up policy when the fed still has an inflation target? On the off chance they do change their targeting regime they’d probably switch to average inflation; PLT probably is unlikely, and NGDPLT doesn’t even seem to be in the cards. Seems as if the outlook going forward can’t be anything but pessimistic with the best case scenario (adopting average inflation targeting) still being suboptimal.

9. April 2020 at 13:17

JJ, I’d say PLT is about 80% as good as NGDPLT, at least right now.

myb6, I agree that we can’t have a complete recovery until a vaccine or cure.

Tristan, I agree.

9. April 2020 at 13:17

@myb6:

Because future precautions can be much more localized and targeted. We’ve learned a lot these past weeks. At risk populations (elderly, diabetics, respiratory problems) will have to be very careful for a while, but the rest of us can start to get back to working and living.

9. April 2020 at 14:27

First off, we won’t have fracking to get us out of this recession like we had in 2009. So obviously in the long term cheap energy is great for America but thanks to fracking low oil prices are bad in the short term which is why 2016 featured superficially low GDP growth.

Second, the issue these last 20 years has been automation and (especially since 2009) not China. This outbreak shows how we need more automation and more robots. I think this outbreak might make us accept a little more risk with things like autonomous trucks and cars. So we need a supply chain that doesn’t get sick.

Third, cheap oil is great for airlines AND advances in aircraft technology. So Concorde was shut down in part because everyone knew where the price of oil was going in 2003. All of the helicopter airlines shut down in the 1970s because of oil price concerns. So these low oil prices are good for advances in supersonic and VTOL aircraft with the huge caveat of how air travel will rebound once the outbreak is contained.

9. April 2020 at 14:56

@Gene Frenkle – seems you are obsessed with petroleum, what is it, talking your book since you’re from Texas? How trite. Tell us your views on hydrogen as a carrier fuel? Hydrogen cars (they have some). Electric cars? Solar space heating? Nuclear energy? Renewables? Or is your daddy in oil and you are afraid to lose your inheritance? (I can relate to that btw, real estate in DC is my thing).

Notice how ruthless Sumner is about bankruptcy: he doesn’t care since technically a bankruptcy is neutral, society neither wins nor loses: somebody loses (shareholders, unsecured creditors) while somebody else gains (competitors, secured creditors made whole) and society, if the bankruptcy is painless (i.e., lawyers don’t pick over the carcass for years but per Chap. 11 allow the bankrupt business to quickly get back into business) while society is at a net zero level (no gain, no loss). In practice I feel certain essential industries never fully recover from bankruptcy, i.e. discount airlines that are highly leveraged, so as a whole society may suffer a bit (a wave of bankruptcies would favor bigger, established companies, which is the modern trend in business anyway).

9. April 2020 at 15:06

Scott,

I agree with your medical prognosis.

I pretty much agree with your aggregate economic prognosis subject to the same caveats that you mention.

I think though what is very different from past recessions is that rather than having the output decline spread broadly throughout the economy, the current recession is concentrated in a few industries and businesses (restaurants, bricks and mortar retail, etc.) where the output drop is close to 100%.

The potential problem I see is how you reallocate that loss. Part of it is of course absorbed just through reduced consumption by everyone of restaurant dining, etc. Workers in the affected industries will be 100% protected. Affected farmers will certainly also get aid.

But…the loan programs implemented so far will be totally ineffective in protecting business owners, and I wonder what happens when you totally wipe out the capital of a very large number of mostly small and independent entrepreneurs.

And BTW – PLT won’t work because they will set the level way to low (given the amount of OMP that has and will take place) and therefore PLT would end up depressing real output. I don’t see any mathematical way you can grow real output without high single digit inflation unless velocity miraculously drops.

9. April 2020 at 15:12

@Ray Lopez

I agree with your comments about bankruptcy, and I think Scott will say himself that he mostly cares about maximizing aggregate utility.

9. April 2020 at 15:37

Ray, oil was very important from a macroeconomics perspective the last 20 years. The reason Trump was even in striking distance to Hillary in 2016 was because low oil prices negatively impacted fracking equipment suppliers in WI, PA, and MI. So I have pointed out several times Moody’s Analytics election prediction model was wrong because it characterized low oil prices as a positive when in fact in 2016 low oil price was a negative.

Going forward energy is a non issue especially if, like me, you think climate change is a dumb issue. So from a transportation perspective all of those things you mentioned will win out based on if they can be converted to kinetic energy cheaper than oil.

9. April 2020 at 17:18

China just cut IOER from 0.72% to 0.35%. First cut since 2008.

Reserve requirement back below 10% for the first time since 2007. MLF and LPR and deposit rates set to follow? Gearing up for a monster stimulus package? CNY 4 trillion+? Would certainly help support a rapid global recovery

9. April 2020 at 18:48

I agree about level targeting, but level of what and what level? Is there any alternative to a price level target?

But if it targets a PL 8 quarters from now at 2%/year and real GDP is 2%/year greater than now but with a big dip and smart recovery and NGDP is to increase at 4%/year, the quarterly price levels will be in for a roller coaster. Operationally how will the Fed know from day to day or quarter to quarter what to do.

9. April 2020 at 20:48

I think that makes a lot of sense from a business cycle and employment perspective, which I realise is the focus of macroeconomics and your focus. What about real output? John Cochrane has suggested it may take years or decades for the economy to restructure to people’s changed preferences:

“Ask yourself, if you are lucky enough as I am to work from home and still have a paycheck, just when and under what conditions are you ready to go back to the office, to have people breathing the air in the seat next to you in the seminar room, to go touch the salad bar tongs, to go give a talk, shake a lot of hands and meet a lot of people, to get on a plane, to stand in a line? The virus may be contained, with aggressive testing and public health playing whack-a-mole, but authorities relenting and allowing business to open, in a highly regulated way. But will you just go back to normal? Likely not.

“Yes, people forget, as our government forgot centuries of pandemics and paid no attention to its own many reports. But forgetting takes years. And if corona comes back slightly mutated every year, or every time one person gets on a plane from a part of the world where it’s raging, if it remains considerably more frightening than the flu, we will be living like this for a long time.”

https://johnhcochrane.blogspot.com/2020/04/whack-mole-long-run-virus.html

9. April 2020 at 20:59

BTW, I’m sure many like me are awaiting your take on the UK Government’s decision to sell bonds directly to the BoE. Markets haven’t reacted much, but do you think it could be the start of the end of central bank independence? Here’s a tweet thread from Tony Yates you might like to comment on: https://threadreaderapp.com/thread/1248163798957142016.html

9. April 2020 at 21:36

I do not think pondering precious price level target is what the Fed should be doing,

Rip off the lockdowns, and shoot for Full Tilt Boogie Boom Times in Fat City, send in the helicopters on Main Street in fleets.

Even so I think inflation will be tame. But that is not a concern for the next two years.

9. April 2020 at 22:33

Rajat

I suppose the fact that markets more or less ignored it means the U.K. Treasury move was no big deal. And thus not monetary financing.

https://uk.investing.com/news/economy/uk-government-expands-overdraft-with-bank-of-england-2092847

10. April 2020 at 03:56

@Gene Frenkle – thanks but I doubt energy is the reason Trump got ahead, more like his dumb base, though at the margin maybe oil was the reason some liked him (anyway Texas is not a swing state so probably that doesn’t matter, anymore than it did for Bush I). But your points are otherwise good, indeed, energy is the prime mover for an economy, not unlike freshwater. But it tends to be forgotten more or less in GDP. Freshwater is vital for life but is typically underpriced and wasted. I’m buying energy stocks btw, and Trump today helped negotiate a oil price war truce (it is said, though probably both Saudi and Russia wanted a truce anyway).

10. April 2020 at 05:01

Hi Scott,

This may be slightly off topic, but this post got me thinking. What types of industries/asset markets do you think would benefit most from a regime change in monetary policy toward nGDP or Price Level targeting? Especially in a post-COVID19 environment.

I know it’s an extremely broad question, just looking to get your thoughts.

10. April 2020 at 06:19

Great article. Help is on the way!

Total Checkable Deposits (WTCDNS)

https://fred.stlouisfed.org/series/WTCDNS

Currency Component of M1 (WCURRNS)

https://fred.stlouisfed.org/series/WCURRNS

10. April 2020 at 07:36

Transactions velocity, Vt, is an independent exogenous factor acting on prices and production.

10. April 2020 at 07:42

“Build the NGDP and businesses will come with the goods and services.”

If, by ‘build the NGDP’, you mean provide money in adequate amount, this is correct. Because goods and services are ‘the demand for money,’ which Milton Friedman pointed out, is unique in being infinite.

Think wheelbarrows full of money in Weimar Germany still being absorbed by whatever goods and services Weimar could produce. The Fed needs to recognize that the least damaging thing they can do right now (but only temporarily) is to produce moderate inflation of prices of goods and services.

That, looking through the opposite end of the telescope, is a declining ‘price of [buying] money’ (which, btw, will have the side effect of increasing, ceteris paribus, the price of renting money, i.e., interest rates).

The incentives created will be to induce more production, or economic recovery. One thing Donald Trump could do to help this along, would be to issue an Executive Order making all ‘price gouging’ laws inoperative. Since ‘price gouging’ is exactly what we need.

Another Executive Order could abolish the FDA’s authority to legalize drugs and medical devices, and all occupational licensing of medical professionals. That would free up Yankee ingenuity to help solve the medical care problem, and even lead to a cure, or a vaccine that would prevent future outbreaks.

10. April 2020 at 09:01

Say’s law doesn’t apply to fiscal policy:

In his early works, Karl Marx juxtaposed the terms “rentier” and “capitalist” to show that a rentier tends to exhaust his profits, whereas a capitalist must perforce re-invest most of the surplus value in order to survive competition. He wrote, “Therefore, the means of the extravagant rentier diminish daily in inverse proportion to the growing possibilities and temptations of pleasure. He must, therefore, either consume his capital himself, and in so doing bring about his own ruin, or become an industrial capitalist….”[4]

However, Marx believed that capitalism was inherently built upon practices of usury and thus inevitably leading to the separation of society into two classes: one composed of those who produce value and the other, which feeds upon the first one.

Says Law:

…”a product is no sooner created than it, from that instant, affords a market for other products to the full extent of its own value.” –Jean Baptiste Say, ”Of the Vent or Demand for Products” A Treatise On Political Economy (4th ed.), translated from the French by C.R. Prinsep (Philadelphia, 1830), Ch. 15.

“There is a plethora of such statements by economists early and late to the effect that a “general glut of the market is impossible.” And “production creates its own demand.” These statements incorporate numerous assumptions that are not in accord with the facts of modern economic behavior, viz., that “asked prices” correspond to costs of production, that the velocity of money is a constant, that money is neutral, that money and purchasing power cannot be created and destroyed out of the orbit of production processes, that prices are flexible both upward and downward, etc. L.J.P. pg. 566

10. April 2020 at 09:06

What’s needed is a recovery plan:

https://www.cnn.com/2019/09/14/politics/bernie-sanders-teases-housing-plan/index.html

Bernie Sanders teases $2.5 trillion housing plan

10. April 2020 at 09:09

Everything Sumner has said for the past 40 years is wrong.

1. Sumner advocated for trade agreements in the 90s, that led to outsourcing millions of jobs.

2. His response to those who were concerned was that service sector jobs would replace manufacturing jobs, and we would all live happily ever after in the long run.

3. Now service sector jobs are being outsourced – including high salaried programming, designing, consulting, medical, and marketing jobs – and the economy is nearing bankruptcy.

4. Sumner’s response in 2020: “sorry but trade is good, Ricardo said it was, and of course he has to be right because I read it in a text-book”.

This is what happens when you regurgitate information from a text-book without questioning what you are reading.

He follows this atrocious record with more meaningless predictions using troughs and peaks. He is shameless…and academics like this are a cancer to our economy…

10. April 2020 at 09:25

dtoh, The physical capital stock won’t go away in 12 months. The skilled entrepreneurs and skilled workers won’t go away either. The bounce back should be very quick (but probably won’t be.)

PLT would be far, far better than what we’ll actually get.

Rajat, That Cochrane post fits in with my Econlog post claiming the free market may do too much social distancing.

The BOE move seems like merely an accounting issue, nothing substantive. Can someone explain to me why it’s important? It’s long been believed by academics that it makes no difference as to whether the Fed buys T-bonds in the primary or secondary market.

James, I agree.

Tom, I’d guess it would be cyclical industries like oil and autos.

Patrick, Yes, deregulation is the way governments can help most effectively. Just get out of the way.

10. April 2020 at 09:40

Ray, the strong economy started in Q2 2014 and then the election year of 2016 we had superficially weak economic growth because of low oil prices. Those low oil prices negatively impacted fracking suppliers in the Rust Belt just enough that Trump was able to convince them the bad economy was back. So Texas had .3% GDP growth in 2016 which made the overall GDP numbers look bad and gave Trump something to attack—the weak economy is back. Everyone in Texas was amazed with .3% GDP growth because it showed how diversified and resilient the Texas economy had become since the 1980s.

10. April 2020 at 09:47

@ BC

“I do not think pondering precious price level target is what the Fed should be doing”

With no NGDP futures market, how else will the fed know how much to load onto the helicopters each week? And how will we know that they are in fact targeting something?

10. April 2020 at 11:55

If I assume real GDP remains depressed until we get a vaccine then keeping NGDP level implies greater inflation until Victory over Coronavirus Day (VC Day). If that is the case, and there has been neither a drop in prices nor an increase in investment, where will the boom come from?

If I assume that real GDP increases between now and VC Day, then I assume that the change in GDP will be due to an increase in remote services (e.g. take-out services, online meetings…) that makes up for the losses in in-person services(e.g. restaurants, commercial flights…) or I assume that there will be an increase in long term investment to offset the short term loss in consumption. But since the ones accumulating capital during this period will probably be the ones providing remote services, I would assume they would continue to invest in remote services. Either way, with my crude model, it is hard to see such a major change coming without major job dislocations even after VC Day.

10. April 2020 at 15:38

@Gene Frenkle – go here: https://www.270towin.com/states/Texas

Note the last time Texas voted for a Democratic Party president was Jimmy Carter. Texas = solid Republican state for federal presidential elections, not a swing state, hence does not matter, regardless of the oil market. You might have a point however for Pennsylvania and Ohio (see: https://www.270towin.com/states/Pennsylvania ) which voted for Obama but switched to Trump in 2016, possibly due to ‘blue collar’ issues like industry (steel, cars) and energy (coal).

10. April 2020 at 16:57

The US recovery after 2008 was anemic, and after about 10 years might have been considered complete, in terms of employment.

Some monetary economists are still jibber-jabbering that the Fed should target inflation, even coming out of the 2020 economic depression. But that is a replay of the 2008 playbook.

If the Fed is allowed to follow its inclinations, that suggests we have another 10 years to recover from the 2020 depression. So by 2030 everything will be back to normal, with luck.

Dudes, put on your thinking caps. Now is the time to employ tens of millions of people as quickly as possible. It is not a time to to tweetybird around price level targets.

10. April 2020 at 17:09

myb6, could you explain what you mean?

We are having our first proper lockdown in Singapore now. Our caseload per million inhabitants is still rather low by international comparison. Even when compared with big countries, but even more when compared with other big infected cities.

10. April 2020 at 17:12

I won’t speak for the Brits, but is the risk with primary market purchases that the value & timing of purchases then gets determined by the fiscal authority rather than the central bank? I think that’s what Yates is referring to in saying “The issue of substance at the root of this is not the temporariness of the operation, but whether it represents a subordination of monetary policy objectives in favour of fiscal objectives; or even if not whether it portends one in the future.” As he says, who can say and the markets are not worried yet. But central bank independence has been around long enough that it is unlikely to be lost in one day or with one move.

10. April 2020 at 17:33

Scott, I saw ba interesting suggestion to have a lockdown for 5 or 6 six days a week, and let people back to work the other 1 or 2 days.

The main non-obvious idea was that even if someone gets infected in the open days, there are likely to be no longer infectious themselves by next cycle.

The economy can run with 40% open days (2/5) pretty much indefinitely compared to shutting down everything completely.

I think I saw the article via a link from slatestarcodex. The authors of the article ran lots of simulations under different models, and the results were quite robust.

Another thing, Scott, do you think the Fed getting good at inflation targeting since the late 20th century made them bad at rapid recoveries?

10. April 2020 at 18:03

Scott,

“The physical capital stock won’t go away in 12 months. The skilled entrepreneurs and skilled workers won’t go away either.”

It’s not like instant oatmeal where you can just throw the physical capital and workers in a room and you get instant output. The people who know how to actually allocate and use the capital and how to organize and manage the workers are all going to be bankrupt, sidelined and dispossessed of their assets.

10. April 2020 at 18:55

Fellow Friends of The Money Illusion, including Dr. Ray Lopez:

Okay, lockdowns are a reality and Tyler Cowen is predicting perhaps multiple lockdowns.

We are 17 million unemployed now, and I hope we are through the first inning of this. I will no longer debate lockdowns, as they are a fact of life.

I hereby coin the term “The 2020 Depression.”

Okay, so say somewhere in towards the end of the year, and when lockdowns policies are exhausted if not victorious , we have 40 million unemployed in the US, and a sluggish global economy, plausibly a global economy in the 2020 Depression too.

Should macroeconomic policy be about hitting inflation targets, or even NGDPLT? (I am a supporter usually of robust NGDPLT.)

Or, as I contend, should macroeconomic policy become, “How do we get 40 million people re-employed in the next year?” Remember these people were kicked out of jobs, effectively by government ukase.

Remember also, if Fed follows its 2008 playbook, the 2020 Depression could have consequences for the next 10 years.

We are not talking about losing 25% of GDP for 2020 only, if the Fed, and possibly other policymakers, persist in the 2008 playbook policies. And as Marcus Nunes has pointed out, even if GDP re-assumes former trajectory, it will be on lower level on the X-line of the graph (the vertical).

So…how to you get 40 million people re-employed in 2021? I am hopeful lockdowns will have been abandoned by then. If not, the question becomes, “How do we get 50 million people re-employed in 2022?”

If we do not get 40-50 million people re-employed quickly, I suggest shopping for boots, jodhpurs, epaulettes and a high hats. They may come in handy when seeking promotions.

10. April 2020 at 19:50

Ray, Trump is president because he picked off MI, PA, and WI. He picked off those states because Hillary had high disapproval but also because fracking equipment suppliers in those states were negatively impacted by the low oil prices. So Texas doesn’t make the equipment to supply frackers it is made in the states that have the factories. But the thing is even with high oil prices after the Great Recession and then frackers making lower prices work from 2017-2019 the manufacturing job boom never happened in the Rust Belt because of automation.

Btw, the cheapest business jet has a button that the pilot can press that lands the plane autonomously and drones have been the skies for years. Those facts mean we could get rid of pilots sooner rather than later and with cheap oil we could have Uber for small planes and small airports by 2030 at the latest.

10. April 2020 at 21:04

“Bay Area coronavirus job losses will top 800,000: report

California faces nearly 4 million in job losses by May, study says’

Sone Jose Mercury News

California is about 11% of nation…call it 40 million unemployed US by end of May….

11. April 2020 at 02:21

@Gene Frenkle – I think we can agree Trump won due to swing states where Rust Belt issues, including oil production, were important.

@Benjamin Cole – “Or, as I contend, should macroeconomic policy become, “How do we get 40 million people re-employed in the next year?” – you are very traditional, as you care about workers. In this sense you are like Sumner. But in fact, modern GDP is not about workers anymore: union membership (and sticky wages) peaked in the 1950s at 30%; today it’s 10% and dropping. Thought experiment: imagine an economy where machines do all the work and the labor force is unemployed. Wouldn’t we have record GDP? We would. Of course you’d have to redistribute this GDP so workers can have their Keynesian paradise (i.e., lots of leisure as Keynes predicted). Bye.

11. April 2020 at 05:20

What may have been a week ago, but feels like a few months ago, I remember Scott saying (and me agreeing) something like “this will not change everything” and we will rather quickly forget as we always do. He may have had some qualifiers, but that is not my point.

What have we likely “learned” (learn means to know something we did not know before) in the past 5 weeks?

We have learned that the world can act as one unit—-at least more than before——by preventing behavior rather than permitting it—-quite an accomplishment (sarcasm).

We have learned, as Scott also mentioned a month or so ago (or was it years?) and I also agreed, to be more risk adverse, or more colloquially “to be scaredy cats”—-which I thought may have been true but not that relevant.

We have learned that those who are not the least bit harmed by this shutdown as they still get paid—e.g., -like all government workers, TV heads and other “journalists”, alcohol and pot distributors, teachers, all politicians, online businesses, and wealthy influencers (e,g., Bill Gates) also on average favor more shutdown time.

We have learned we will “obey” based on extremely incomplete information as to the danger of some exotic illness—-which so far at least seems to be a rounding error of the amount of new deaths added—-(counting and testing errors, would have died anyway errors, the shocking estimate by some who have “counted” that less than 800 people in US younger than 50 have died—-and the estimate of the average death age being in the vicinity of 78-83—-what kind of crazy “pandemic” is that?)

We have learned this has been a boon for some businesses and for government itself.

What I HOPE we also have learned, is the need to discover just how damaging this shutdown has been, how dangerous Declared “states of emergency powers are” , how critical the need to know a true danger—-not a “feared danger” —which should have been predicated on real data and a willingness to accept some danger—-as we already unquestionably do. The current group of pols will never admit error—-they already hide or ignore all anomalies—.

Will Cochrane’s prediction be correct? Or will Scott’s previous dictum of “we always forget’ (for all practical purposes) be correct and move on as before.

I believe our actions have been a terrible error—-and not for dollars versus lives reasons —-but for some lives versus some other lives reasons. I don’t care if we declare victory or what the hell we say—-but this cannot have been close to the correct response—and a “never again” (except for a Black Plague style event) mindset needs to be established—-or we will “go out, not with a bang, but a whimper”. We must learn this was a terrible mistake. Lockdowns are disasters——look what we have done. Could we do this again in 6 or 12 months and survive? No.

(In Stephen King’s apocalyptic novel of good and evil written when he was 27, a virus named Captain Trips killed “99.4%” (humor about scientific precision) of all humans. The main character quoted the last four lines from The Hollow Men to describe his dark sense of the utter irony of the virus being created by science).

——-

11. April 2020 at 05:41

PS—-The novel, of course, was The Stand.

11. April 2020 at 05:46

Dr. Ray Lopez:

You have struck on the solution! Machines don’t get sick.

However, I think your solution will take too long to implement, just like the vaccines we are promised…in 2022.

I think there is a great deal of validity to Michael Rulle’s comments above. People in sinecures have a different point of view from those harmed by the lockdowns.

11. April 2020 at 06:10

After 4 months (!) we get results from the first published randomized test in a small German town. Interestingly, it almost matches the Diamond Princess. An estimated 15% have or had the disease (90% of the 15% or so “had” the disease and were unaware) and the death rate was .37% (for those multiplying need to use the number .0037). One test, one town——-need many more—-clearly but those who “had” it were most likely exposed before lockdowns—-like the DP ship.

This would translate into 185K deaths in US. More work to be done. If true——how optimal was what we did to prevent some percent of this—-recognizing both economic and “other lives” opportunity costs exist?

11. April 2020 at 07:06

Today’s WSJ has a piece by Salena Zito,that nicely demonstrates why government needs to get out of the way’

https://www.wsj.com/articles/they-developed-their-coronavirus-vaccine-in-salks-shadow-11586557454?mod=hp_opin_pos_1

—————quote———–

Thanks to their previous collaborations on vaccine-platform development, the twin teams of Dr. Falo and Dr. Gambotto were able to generate their new potential vaccine, which they call PittCoVac, in a mere seven days. As they wait for the FDA’s green light, Dr. Falo says they’re tackling two issues. “One is the clinical testing and regulatory process. The other one is the scalability. So can you make a lot of these—millions, billions—to distribute across the world?”

It helps that the vaccine doesn’t require refrigeration. “That means that we can actually put these in boxes just like Band-Aids,” Dr. Falo says, “store them, ship them, distribute them globally, which is really important for underdeveloped countries who don’t have the means of keeping vaccines cold the entire time.”

The regulatory issue is out of their hands. Dr. Falo says the FDA is working as fast as it can while maintaining safety. “We’ve started that process. We’re exchanging data with them, describing what we have, how we make the vaccine, and their experts are evaluating that data to determine whether this vaccine is safe to put into patients.”

————–endquote————-

11. April 2020 at 07:12

My “office” is a “we-work” style large building which remains open. I have gone in twice the last month simply to turn on my computer which inexplicably turns off 1-2 times a month—I access it normally by remote access software from home.(the building is 20 minutes from my house)

I did that yesterday—-in and out in 2 minutes. There were 2 other people in a 20,000 square foot space. Plus I went to the men’s room for the sole purpose of washing my hands like a good citizen. Lots of cleaning supplies. I noticed a sign suggesting we wash our hands!. The surprise was——there was statistical info about the benefits of washing hands.

WASHING YOUR HANDS SEVERAL TIMES A DAY DECREASES YOUR CHANCE OF CATCHING FLU BY 20%.

I had never even thought of that before—-I.e., putting a probability number on the benefit. But once I saw the number I thought—-“how can they possibly know that?” Also, we are doing this now for COVID-19, not the flu—-although I assume the reasons are the same. Only 20%? Better than zero—-but doesn’t the Virus hang around more?

Anyway—in 2017-2018, 45 million people got the flu, 810,000 were hospitalized and 61,000 died and deaths and flu fairly evenly distributed in ALL age groups. Hmm. This year we estimate between 29000 and 50000. The flu season is estimated to last 13 weeks but it’s peak and length changes.

So far, using the high number of 50k and the estimate of Covid of 60k that is 110k. I guess that means when that total is higher than 60 we go on Lockdown. Currently it is 18-20 not 60—but whatever.

Yes, being sarcastic. But isn’t that what

11. April 2020 at 07:14

……what it de facto implies?

11. April 2020 at 08:13

Oxford believes there is an 80% chance that a Covid Vaccine will be ready for the public by September. Let’s do a bit of forecasting reactions to this.

We have had flu vaccines forever—-and we still have 10s of thousands of deaths per year. The CDC rates it’s effectiveness which changes every year at between 37-45% a year. Effectiveness is an interesting concept. The CDC sight is very vague on what it really means statistically, except people still get the flu who take the shot but at a lower rate one does not takes the shot—-and best if everyone gets it (why isn’t it required ?!)

What will happen is the vaccine will be as effective as the flu vaccine and it will be declared by too many this is not good enough. It will be pointed out that it’s the same with flu. And then we will incorporate the flu into our counting obsession. And use the combo for lockdown reforms

Politics will drive it all.

11. April 2020 at 08:25

Shouldn’t lockdown decrease the flu? In fact, our Covid theory says this is a certainty. Why are we not tracking this?

I compare what we are doing with how trading firms control risk. Most, not all, most of the time, are extremely detailed and specific. What we are doing with this pandemic is absurdly amateurish. Yes the logistics are much harder, but the concepts are the same—-and we are failing miserably

What if Flu deaths are not decreasing?

11. April 2020 at 08:41

It is amazing that no entity has stats for flu as we do for Covid. This is the last week that CDC will publish its weekly flu review. It’s the end of fu season. They do say that flu is still “elevated”—whatever that means

11. April 2020 at 18:19

@ B Cole

“Some monetary economists are still jibber-jabbering that the Fed should target inflation, even coming out of the 2020 economic depression. But that is a replay of the 2008 playbook.”

Target the price level is exactly what the Fed did not do 2008-2020.

What would be wrong with targeting, say 3% growth in the price level over the next couple of years.

I can understand neither what you favor nor oppose.

12. April 2020 at 06:21

Scott, what are your thoughts on the Fed buying non-treasuries in their latest round of QE? It’s supposed to be investment grade and high yield corporates and ETFs. It seems like a good way of lowering the borrowing costs of the smaller businesses that really need it but a lot of people are screeching about “the fed buying up (worthless) junk bonds”. But surely if they’re buying a hugely diversified basket of these assets they’re not exactly exposing themselves to a huge amount of market risk?

12. April 2020 at 16:36

Thaomas–

I understand what you are saying that the Federal Reserve failed to hit a 2% inflation target after 2008

But, egads man, we are talking about 50 million to 60 million unemployed Americans by the end of June or into July.

If the Fed engaged in policies that somehow helped sopping up that 50 million to 60 million unemployed within a year, I do not care if the price level target is breached and we have, say, 8% inflation for two years.

It might be heretical to posit such, but I believe there are some things even more important than the rate of inflation.

12. April 2020 at 16:40

I suspect that many people will still avoid restaurants and mass events until a vaccine or very effective treatment are available. And even then I suspect that people will have learned to go without restaurant meals and will be habituated to doing more meals at home, so the industry won’t bounce back all that quickly. Same for a lot of other industries. Also, I think that you should keep in mind the psychological effect of this. Are millennials really going to go out and splurge so soon after a recession, given that there only experience of the labor market was the financial crisis and the recovery that was so slow that it never really felt like a recovery? I think that millennials will need to see the economy actually get strong before they spend again, and that puts the economy in a paradox of thrift situation. There has to be on the ground evidence that this time is different before people update their priors.

13. April 2020 at 09:43

Matthias, Regarding rebooting the economy, I’ve been talking about the fact that there is no silver bullet, there are a million small steps that must be taken one at a time. Your suggestion is a good example.

You asked:

“Another thing, Scott, do you think the Fed getting good at inflation targeting since the late 20th century made them bad at rapid recoveries?”

I think the problem is more the reliance on interest rate targeting during a period of falling equilibrium rates.

dtoh, You said:

“The people who know how to actually allocate and use the capital and how to organize and manage the workers are all going to be bankrupt, sidelined and dispossessed of their assets.”

Then the new owners will hire them back. (And I doubt your premise.) History shows that economies can quickly bounce back even after very severe recessions.

sramsay, I’d prefer the Fed first buy all the safe assets available, and only then turn to riskier assets. Even buying lots of safe assets will have a spillover effect on riskier markets, boosting their prices as well, as investors who formerly held T-bonds re-allocate.

But if necessary to stabilize NGDP, they should absolutely buy risky assets. Just not yet.

Burgos, It all depends on monetary policy (NGDP).

17. April 2020 at 18:44

Thanks for the reply Scott, Why dyou think they skipped a step in this way? Has it just become (incorrect) conventional wisdom that buying treasuries doesn’t have much effect? Also, what do you say to those people angry about credit risk? Is buying high yield corporates really *that* risky for the Fed?