In a recent post, I said the following about Iowa’s sudden shift to the political right:

It’s weird when you move away from a place for several decades. You still believe that you understand the place from when you lived in the area. But you really don’t. Unless you live somewhere, you cannot understand it. And maybe it’s impossible to truly understand a place even if you do live there.

Today, I’d like to focus on economics, not politics.

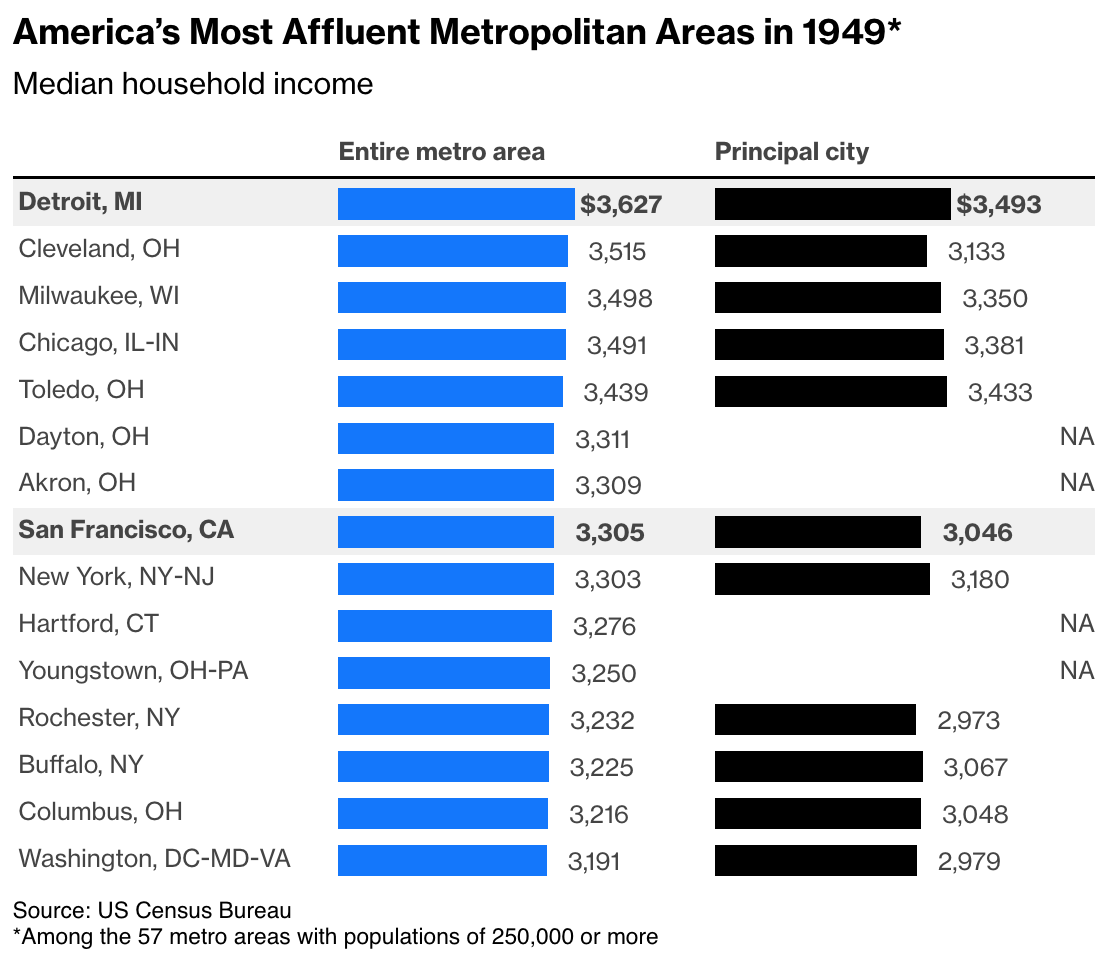

I was born in Michigan (in 1955) and grew up in Wisconsin. I went to grad school in Chicago. According to a recent article in Bloomberg, this was the richest part of America in the period after WWII:

As a child, I never gave much thought to economic disparities. I recall a general view that “hillbilly” areas like West Virginia were backward, as was the deep south. Other than that, I thought we were pretty normal. West Coast, Midwest, East Coast, Texas, Florida, it was all pretty much the same in my mind. Was I wrong? (BTW, the people on TV news shows mostly had midwestern accents.)

When I moved to Boston in 1982, I certainly did not have any sort of feeling that I was moving to a more advanced part of America. But by the time I left in 2017, Boston did seem much more advanced, as does Orange County, California, where I live now.

I’m sort of getting used to the way the media now portrays the Midwest as backward, but at a deeper level I don’t think that view will ever cease to feel a bit strange. I wasn’t living there when the transition occurred. I don’t remember it as being backward. Commenters tell me that Iowans have become Trumpistas because they are uneducated. I’m skeptical. The Midwest never seemed uneducated to me back then—indeed I recall midwestern states often scored high on various test rankings.

When I saw the Milwaukee Bucks win the title in 1971, it was America’s 12th largest city. Now it feels weird when I hear commentators refer to Milwaukee as a “small market”, and indeed when they again won the title in 2021 it was America’s 31st largest city. (There are only 30 NBA teams.)

Is it possible that all this will flip again by 2070? Might Mississippi become richer than Massachusetts? Or does the past 50 years represent a once and for all change due to population sorting—taking a (mostly) geographically homogeneous nation and doing radical sorting by education level? Are we now “locked in” to this pattern? I have no idea.

Notice how this blog has gone downhill as its become infected with politics.

2. The FT has an excellent interview with Adam Posen. This caught my eye:

Adam Posen, president of the Peterson Institute for International Economics, has been a rare vocal critic of what he dubs the rise of “zero-sum economics”.

As I keep saying, we are in a new dark age of economics. Opponents of zero sum thinking are not now viewed as “rare” contrarians. What a sad state of affairs.

Though public debt is at historic highs — more than 100 per cent of GDP across the developed world — it is stabilising in Europe but rising relentlessly in the US. With interest rates rising rapidly at the same time, the interest paid on public debt is increasing — and doing so much faster in the US.

In future years, people will regard the Trump/Biden period as a fiscal train wreck.

4. The NYT has a good piece on how we are shooting ourselve sin the foot when it come sto trade with China:

Mr. Manchin and Mr. Rubio may find ways to discourage this kind of partnership. Under the Inflation Reduction Act, electric vehicle batteries produced by a “foreign entity of concern” are ineligible for the $7,500 electric vehicle tax credit. Although the meaning of that phrase remains unclear, one possible interpretation suggests that virtually any firm subject to Chinese law might be forbidden — meaning that even if Ford produced every part of a car in the United States, the Chinese company’s involvement might still disqualify the car’s buyer from receiving the $7,500 tax credit.

But rejecting Chinese know-how would make us, ironically, more dependent on China in any future security-related rupture — because we will simply have to import from China what we never learned to make ourselves.

This is the kind of dilemma that Treasury Secretary Janet Yellen had to navigate during her recent trip to China — and that federal officials must negotiate for years to come. If American firms can’t open factories with Chinese firms in the United States, then the country’s workers will miss out on jobs, its consumers won’t get new technology and its engineers will fall behind the world’s best. Competing with China is a good idea. Being so suspicious of it that you trip over your own feet isn’t.

5. As usual, Janan Ganesh hits the nail on the head:

At some point, demagogues will have to choose which they hate more: free trade or the blob. Curbing the one tends to empower the other. Notice that, though Trump started the move to industrial protection, it has achieved real substance under a centre-left government. The right could never follow its antitrade logic to its natural conclusion, which is the aggrandisement of officialdom. Trump managed to fall out with the national security state, of all things. The idea that he could abide a US version of Japan’s former, and lordly, Ministry of International Trade and Industry, is fanciful. Yet that kind of technocratic power is what, via the hand of his successor Joe Biden, populism has inadvertently created.

I fear, though cannot know, that we are living through the biggest wrong turn in government policy of my lifetime. A decade into this protectionist age, we might regret the waste, the pork, the higher consumer prices (do “workers” not pay those?) and the fragmentation of the west into squabbling trade zones. But the wrongness of this trend is another column. For now, what stands out is the improbable winner of it. Imagine being told in 2016 that elites would have more clout, not less, and owe it to their own tormentors.

6. Tucker Carlson and I have almost identical views of Trump. Here’s Reason:

Based on his private statements to colleagues, we know that former Fox News personality Tucker Carlson did not believe Trump lawyer Sidney Powell’s wild claims about systematic fraud in the 2020 presidential election. “Sidney Powell is lying,” Carlson flatly stated in a November 16, 2020, text message to fellow Fox News host Laura Ingraham that came to light as a result of the defamation lawsuit that Dominion Voting Systems filed against the channel. . . .

We also know, again thanks to discovery in the Dominion lawsuit, that Carlson had a low opinion of Donald Trump. In a November 10, 2020, text message, he called Trump’s decision not to attend Biden’s inauguration “hard to believe,” “so destructive,” and “disgusting.” He was more broadly critical in a January 4, 2021, text message to his staff. “There isn’t really an upside to Trump,” he said, describing “the last four years” as “a disaster.” Carlson was eager for a change: “We are very, very close to being able to ignore Trump most nights. I truly can’t wait. I hate him passionately.” The day after the January 6 Capitol riot by Trump supporters, Carlson privately called him “a demonic force” and “a destroyer.”

The only difference is that I am not afraid to say this in public.

7. Joe McCarthy was a Wisconsin senator, so I guess it’s no surprise that the new McCarthyism is being spearheaded by another Wisconsin politician:

A US congressional committee is investigating a handful of venture capital firms for their investment in Chinese technology companies, the latest sign of Washington’s increasing scrutiny of American funds suspected of helping develop sensitive industries in China.

Investments by GGV Capital, GSR Ventures, Walden International and Qualcomm Ventures are being probed by the House select committee on China, led by Wisconsin Republican Michael Gallagher. The firms didn’t immediately respond to requests for comment.

Remember when they said we don’t hate the Chinese people, just their government? Now all 1.4 billion Chinese are suspect:

“There’s no such thing as a truly private entity in China,” Gallagher told reporters Wednesday. “Democrats and Republicans agree that we don’t want to be fueling our own destruction, helping the Chinese perfect systems designed to kill Americans in future conflicts or helping to perfect an Orwellian techno-totalitarian surveillance state that’s being used to commit genocide.”

8. The Economist has a good article on scientific fraud:

For example, critically ill patients undergoing surgery were once sometimes given starch infusions to boost their blood pressure. This was based in part on seven now discredited studies by Joachim Boldt, a German anaesthesiologist. A revised round-up of the evidence published in the Journal of the American Medical Association, in 2013, after his fabrications were discovered, concluded that giving starch infusions in these circumstances caused kidney damage and sometimes killed people.

Likewise, for more than a decade cardiac patients in Europe were given beta-blockers before surgery, with the intention of reducing heart attacks and strokes—a practice that rested on a study from 2009 which was eventually determined to have been based, at least in part, on fabricated data. By one estimate, this approach may have caused 10,000 deaths a year in Britain alone. And a systematic review showing that infusion of a high-dose sugar solution reduces mortality after head injury was retracted after an investigation failed to find evidence that any of the trials included in it, which were all ascribed to the same researcher, had actually taken place.

9. I opposed Brexit. It seems the British public is coming around to the same opinion. Here’s The Economist:

Politics is routinely dominated by the short run: in-party scraps; looming by-elections. But quietly shifting and longer-term trends risk being neglected. One such is the rise of disillusion with Brexit. Polls from YouGov, Ipsos and NatCen Social Research all find that sizeable majorities of Britons now regret the decision to leave the European Union. The latest numbers show a margin as wide as 60-40% for those wishing that Britain had remained in the eu, compared with the 52-48% vote to leave in June 2016.

10. It’s always amusing to see people try to promote their candidate using fascist iconography.

“COVID-19. There is an argument that it is ethnically targeted. COVID-19 attacks certain races disproportionately,” Kennedy said. “COVID-19 is targeted to attack Caucasians and black people. The people who are most immune are Ashkenazi Jews and Chinese.”

“We don’t know whether it was deliberately targeted or not but there are papers out there that show the racial or ethnic differential and impact,” Kennedy hedged.

I suppose one could also say “there is an argument” that Kennedy is secretly being financed by Donald Trump and Vladimir Putin.

Heck, there is an argument that I was created on one of Saturn’s moons and my consciousness was inserted into the corpse of a human killed in an auto accident back in 1955.

PS. Kennedy just passed DeSantis as third most likely to be our next president.

I was sad to see that James Bullard is retiring from his position as president of the St. Louis Fed. He was a fan of NGDP level targeting, and as David Andolfatto points out he was willing to dissent in both dovish and hawkish directions. He will be missed.

I don’t like monetary policy hawks and doves. Policy should be expansionary at some times (e.g., when I started blogging) and contractionary at others (right now.) Bullard understood this.

I’ve always been skeptical of the economic slack theory of inflation. There’s no way FDR could have generated high inflation in 1933 if the slack theory were true. I see inflation as being driven by changes in NGDP growth (monetary policy), and slack is something that happens if NGDP decelerates too rapidly.

But so far, NGDP growth has not decelerated too rapidly, indeed I’ve argued it’s decelerated too slowly. Even so, far worse things could have happened, and in the past often did happen. Fed policy during late 2021 and early 2022 was really bad (after being good in 2020 and early 2021)—since then it’s been average. It’s decelerated, which is appropriate—but a bit too slowly. Let’s see what Q2 looks like.

Matt Yglesias is correct that the recent strength of the economy supports the NGDP view over the slack view:

I think that’s right. But we need to be careful here, as most of the hard part still lies ahead. The Fed needs to bring down wage inflation, and before it’s all over Krugman may end up being correct. Slack doesn’t cause lower inflation, but it’s usually a side effect of wage disinflation.

Victory would be getting back to 2% with only a small increase in slack. I discuss this in a recent post on the difficulty of achieving a soft landing.

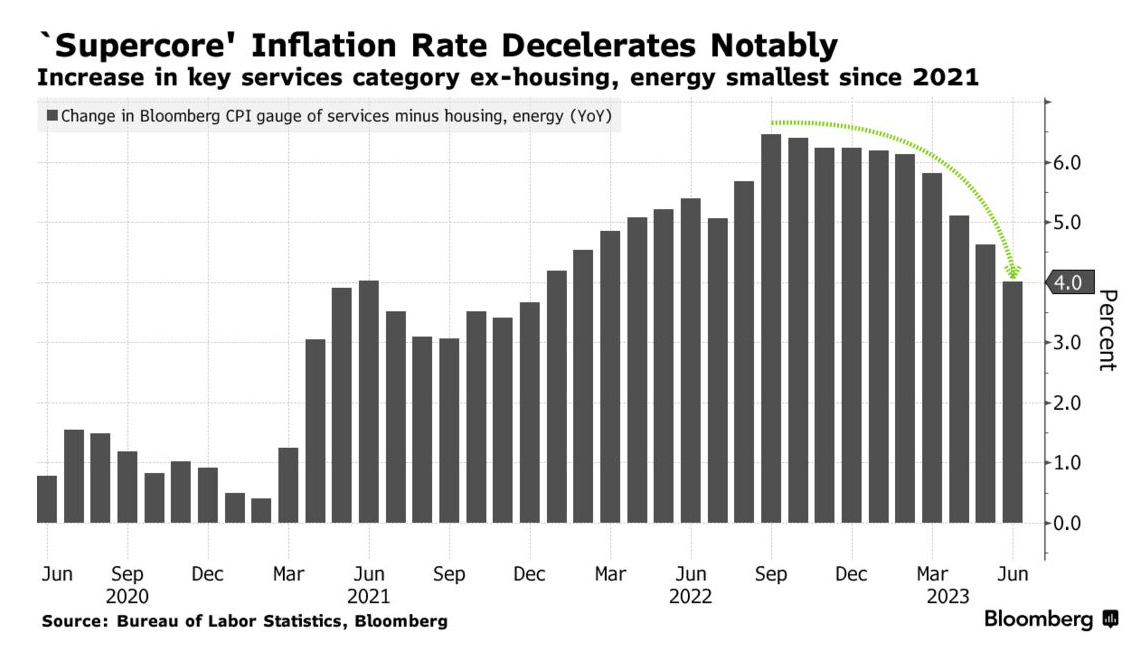

We still have a loooong way to go, but today’s report contains good news. Not so much the fall in annual headline inflation to 3% (which was due to base effects), rather the fall in non-housing services inflation:

The inflation that really matters is wage inflation. Unfortunately, it’s hard to get good data on wage inflation. The Atlanta Fed says it’s running 6.1%, and the BLS says 4.4%. “Supercore” inflation is the part of inflation that is most closely tied to wages, so its recent decline is a good sign.

But don’t become too optimistic; the next few reports may be worse.

Welcome to a new blog on the endlessly perplexing problem of monetary policy. You’ll quickly notice that I am not a natural blogger, yet I feel compelled by recent events to give it a shot. Read more...

My name is Scott Sumner and I have taught economics at Bentley University for the past 27 years. I earned a BA in economics at Wisconsin and a PhD at Chicago. My research has been in the field of monetary economics, particularly the role of the gold standard in the Great Depression. I had just begun research on the relationship between cultural values and neoliberal reforms, when I got pulled back into monetary economics by the current crisis.

"This man is the devil. Look at his eyes. Same as Soros. All baggy and nasty. Good people dont age like that. Its the sign of a madman. A negativity..."

"I watched Satantango on video over 3 days. I found it absolutely gripping, but one must surrender for a time one's idea of what a movie should be. Instead, you..."