I’d put a weight of 0% on A and 0% on B. I’d put a 100% weight on monetary policy. In 2021, the Fed should have set their fed funds target at a level that would return NGDP to the pre-recession trend line. In fact, they set rates well below their equilibrium level, and hence NGDP rose about 8% above trend. Thus 100% of the excess demand was caused by the Fed not doing its job.

BTW, I’m not sure what “consumption/aggregate demand” means. Consumption and aggregate demand are very different concepts.

PS. I’m almost ready to take a victory lap on this post from late 2022, where I expressed skepticism about the Fed’s forecast that the unemployment rate would rise to 4.6% by the end of 2023, despite positive RGDP growth of 0.5%. I suggested that conditional on positive GDP growth, the unemployment rate would not rise very much.

Fed officials see inflation finishing the year close to 4% now, compared with 3.6% prior. Unemployment is only seen rising to 4.1% from 4.5% previously. Officials now see stronger economic growth this year of 1% verses 0.4% previously.

Twitter’s acquiescence to autocratic or non-liberal regimes is not an exaggeration by critics of the social network. The data, which the public audit receives automatically, speaks for itself. Since Musk’s takeover, the company has received 971 requests from governments (compared to only 338 in the six-month period from October 2021 to April 2022), fully acceding to 808 of them and partially acceding to 154. In the year prior to Musk taking control, Twitter agreed to 50% of such requests, in line with the compliance rate indicated in the company’s last transparency report (none have been published since October 2022). Following the change of ownership, that figure has risen to 83%, according to the analysis of the data by the technology information portal Rest of World.

And this:

NEW: Twitter blocked promotion of a Democrat’s campaign video because it expressed support for abortion rights.

“The mention of abortion advocacy is the issue here,” a Twitter employee told North Carolina candidate Rachel Hunt. https://t.co/cc0bsV1gkX

For example, if you hit 21 on your first two cards in blackjack, it used to pay $15 on a $10 bet. Now it pays only $12. Roulette wheels used to have two green slots, zero and double-zero, that paid out nothing. Now they have a third slot, triple-zero, that also pays out nothing.

In the delicately balanced world of big-time gambling these are huge changes—and they’re obviously right out in the open. How can casinos get away with fleecing regular customers like this?

The answer appears to be simple: they don’t care.

Isn’t this sort of like how companies are extracting more tips and bigger tips in all sorts of ways? We just went to a restaurant that added a 4% service charge, and still wanted the normal 20% tip. And now you have retailers asked for tips. I assume this is because Americans are no so rich we can afford to act like rich people, just throwing money away. Or am I missing something?

3. Really good FT article on how the free market wing of the British Conservatives lost their party:

To borrow Oscar Wilde’s quip about the death of Little Nell, it would take a heart of stone to hear the wails of free-market Brexiters without laughing. Recent weeks have seen a flurry of laments, fury and blame-shifting by leading Leavers, from Nigel Farage to Lord Frost. But perhaps the most striking was an article by Daniel Hannan, a central figure in the Brexit movement, which appeared under the headline, “The liberal Brexit dream is dying” — though naturally he blamed the “Europhile establishment”.

The UK leads the US by a few years, and so I expect this to also happen in the US:

But even when Truss used her only party conference speech as leader to rail against the “anti-growth coalition”, she failed to notice it was sitting in front of her, in the rows of Nimbys, immigration hawks and urbanite-hating culture warriors. The party is locked into a low growth economic model and a belief in spending cuts which struggles to be specific.

The pro-growth wing of the GOP will eventually notice that they’ve lost their party.

4. The Economist is very pessimistic about the future of banking:

[T]he world is moving towards a bigger role for the government and a smaller one for private actors—a fact that should alarm anyone who values the role of the private sector in judging risk. . . . It is getting harder to spot the differences between the Chinese system of explicit direction of lending and the “social contract” of the Western system, in which there is massive state underwriting of risks and a mass of regulation foisted on banks in return, so that they do not abuse the insurance they have been granted.

What is more, the seeds of many banking crises have been laid by misguided government intervention in banking, particularly by those moves that skew incentives or the pricing of risk, warns Gary Cohn, formerly second-in-command at Goldman Sachs, a bank. It might be easier to sleep at night knowing that, at present, the government has all but promised to protect all deposits, has lent generously to banks clinging on and has infused the system with funds through its wind-up operations. But this is precisely the kind of action that will cause sleepless nights in future.

5. Now that Trump is going against their favorite candidate, conservatives are getting annoyed. The National Review has a piece trashing Trump for his juvenile insults against “Rob” DeSantimonious. (Do you remember 8th grade?)

It’s quite funny, and well worth reading. This is especially good:

In case you missed it yesterday, the Trump campaign attacked Ron DeSantis for issuing a statement in 2017 in support of Trump’s nomination of FBI director Christopher Wray. Hey, if issuing a statement of support for Wray is somehow disqualifying . . . what should Republicans think of the guy who picked Wray in the first place?

It wasn’t Trump’s fault, the DEEP STATE forced Trump to pick Wray.

In another National Review piece they interview Republican voters:

She said she used to like DeSantis because of how he handled Covid in Florida but now has questions about “other things coming out about him,” though she did not elaborate.

I’m guessing these are similar to the “other things” that have come out about me in the comment section of this blog. Every time I read these stories I think about how the GOP establishment created this clown. Then I just grab another bag of popcorn and enjoy the spectacle.

6. Bloomberg has an interesting article on the newest trillion dollar company:

The US doesn’t want China to achieve parity in chipmaking; Huang argues that President Joe Biden’s restrictions will do the opposite. They incentivize China to foster a homegrown industry, and it already has more than 50 GPU companies, he says. Huang sets the stakes even higher and suggests the restrictions could trigger an international incident—specifically, an invasion of a nearby island where much of the world’s semiconductors, including Nvidia’s, are manufactured. “China is not going to sit back and be regulated,” Huang says. “You got to ask yourself, at what point do they just say, ‘F— it. Let’s go to Taiwan. We’ve got nothing to lose.’ At some point they will have nothing to lose.”

7. Henry Kissinger celebrated his 100th birthday by calling for the US and China to start acting like mature adults:

Kissinger said it was up to both Washington and Beijing to step back from their standoff, which he said was at “the top of a precipice.”

I recently discussed the current German recession, which is accompanied by a very strong labor market. In a recent post, Tyler Cowen provides a summary of Czechia’s recent recession, which shows the same pattern. In another post, he links to a Jason Furman tweet on the puzzling pattern of US growth in income/output:

Unlike many other countries, the official (NBER) definition of recession does not involve two negative quarters, but lots of people wrongly believe it does.

I’m interested in another question—why do we care about recessions?

I cannot be certain, but I suspect that many people fall for the following logical fallacy:

A implies X

A is strongly correlated with B

B implies X

I think I know why we care about recessions. Recession are generally associated with lousy labor markets. The high unemployment of the 1930s was such a severe social problem that it put macroeconomics on the map as an important field of inquiry, and as an area of interest to government policymakers.

In the US, recessions are highly correlated with two declining quarters of GDP. But the correlation is not perfect. There was clearly a recession in 2001, but we did not experience two consecutive negative quarters. There was clearly a boom in early 2022, but we did experience two negative quarters.

I suspect that many people are making the following logical fallacy:

We all know that recessions are traditionally associated with really bad labor markets (true). Thus past recessions have been important events (true). Recessions are almost always correlated with two negative quarters (true). Thus future cases of two negative quarters will be important events (false).

Here I’m dodging the question of whether two negative quarters are “actually a recession”, which is about as uninteresting a question as one could imagine. Who cares?

[Actually, I can think of an even dumber question: Is economics a science? Watch me move right along at the cocktail party when I hear that one.]

I’ll tell you who cares about recessions—dumb people who believe that words have magical powers. “If only I could convince you that this is a recession!” Yawn.

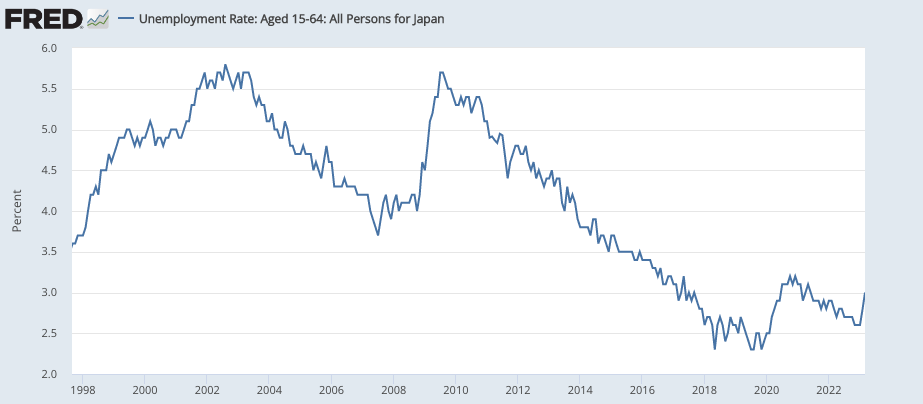

It’s not that I think you are wrong; it’s that I don’t care. Japan had a bunch of recessions in the 2010s. Do I care? No, none of them showed up in the labor market:

It’s incredibly uninteresting to see a slow growth economy alternate between slightly positive quarters and slightly negative quarters.

The entire world is now becoming more like Japan, with ever slower trend GDP growth rates. In the future, there’ll be lots more of these “recessions” with booming labor markets.

This is why the “Will there be a recession?” debate is so dumb. I don’t care whether the US experiences a recession; I’m simply not interested. The interesting question is whether the US will experience the sort of recession that we experienced in the past, where the unemployment rate always rose by at least 2 percentage points.

Now that’s an interesting question.

The German and Czechia recessions are so boring that the news media should not have wasted any ink reporting on these two events. No one cares.

PS. Another really dumb topic is “greedflation”. I’ve stopped even reading the articles. Josh Hendrickson brilliantly nails the underlying problem here:

This brings me inevitably back to so-called “greedflation.” This story is an attempt by people to treat every bout of inflation like isolated cases that require the fresh eyes of a new detective.

It’s even worse. Lots of economists also think we need to treat every recession like isolated cases requiring detective work. It’s (almost always) the falling NGDP, stupid. (Covid in 2020 was the exception that proves the rule.)

PPS. BTW, US productivity and output growth was overstated in 2020 and is now being understated. The longer run figures are more accurate.

In the old days, the threat of bonds being defaulted on made the bonds less attractive to investors. Now we live in the land of Oz, and default threats make investors rush to buy the bonds. Here’s Bloomberg:

The currency’s outperformance — steamrolling even the traditional safe-haven yen, which fell to six-month lows past 140 per dollar last week — reflects the US’s unique position at the center of the global financial system. Even when the nation is flirting with default, investors have little choice but to flock to dollar-denominated assets like Treasuries for protection.

An MLIV Pulse survey earlier this month showed US debt was second only to gold as the most popular asset to buy in the event of a default.

In the old days, if a candidate was enmeshed in a scandal his rivals would rush to take advantage of the situation—criticizing his behavior. Now we live in the land of Oz, where rivals rush to defend the person they are running against when it is discovered that he committed sexual assault. Here’s Time magazine:

But when the time came to actually stand up to him, Trump’s primary rivals and political enablers were too cowardly or calculating to throw much of a punch. Nikki Haley, Trump’s major declared opponent and former U.N. Ambassador, dismissed the potential indictment on Fox News as “more about revenge than it is about justice.” Another active candidate, businessman Vivek Ramaswamy, went further, blasting the “disastrously politicized prosecution” and calling on other Republicans to condemn it. Former Vice President Mike Pence, who is openly considering a run, told an interviewer the probe “reeks of the kind of political prosecution we endured in the days of the Russia hoax.”

PS. This quote from Tyler Cowen explains why I completely ignored the debt ceiling “drama”:

There may yet be a final round of drama, but the people who treated this event as the nothing burger it is were on the right track the whole way through.

In Turkey, the liberals win both the prosperous coastal cities and the oppressed minority groups (the Kurds in the southeast.)

The authoritarian nationalist right wins the rest. That’s politics in the 21st century. Long gone are the days when non-minority working class voters supported the left.

(Within a few more election cycles, the Democrats are going to lose the Hispanic working class.)

Welcome to a new blog on the endlessly perplexing problem of monetary policy. You’ll quickly notice that I am not a natural blogger, yet I feel compelled by recent events to give it a shot. Read more...

My name is Scott Sumner and I have taught economics at Bentley University for the past 27 years. I earned a BA in economics at Wisconsin and a PhD at Chicago. My research has been in the field of monetary economics, particularly the role of the gold standard in the Great Depression. I had just begun research on the relationship between cultural values and neoliberal reforms, when I got pulled back into monetary economics by the current crisis.

"Camden, I have no doubt that if you put some thoughtful Israelis and Palestinians in a room they could come up with a solution. But that's not because of their..."

"Come to think of it, there is some value in engaging with your generic Palestianian, or Israeli for that matter, to get a sense of the shared experience of a..."