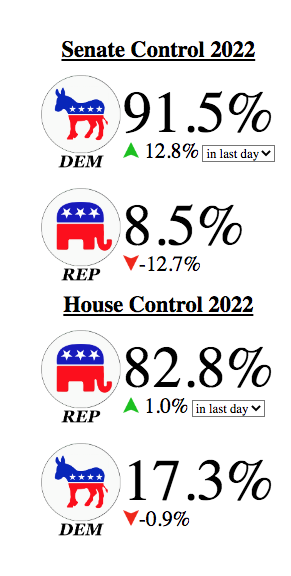

It seems like the conventional wisdom is that the GOP took the House by a narrow margin and the Senate is still up in the air. That’s what I hear in some media reports. But that’s not exactly the current view of the betting markets:

Can that be right? Are the Dems actually more likely to take the Senate than the GOP is to take the House? The 91.5% figure seems to be based on the fact that the Dems are strongly favored on all three outstanding Senate races (especially Nevada and Arizona), and they only need two of them. I’m not sure why the House GOP odds are not higher, perhaps because the Dems currently lead in most of the unresolved races. To be sure, an 83% chance of taking the House is still excellent, but I see absolutely no speculation on what would happen if the Dems ended up with 51 seats (not unlikely), and somehow also took the House. Senator Manchin would become much less influential.

Again, this is not likely, but I see at least a mild disconnect between pundit talk and actual election odds.

For the second time in a row, Trump (probably) handed the Senate to the Dems on a silver platter. Three months ago I explained what all the pundits missed:

I see some puzzlement in the media as to why Trump keeps endorsing such lousy candidates.

After losing the 2020 election, Trump immediately began planning his comeback (as I predicted.) The first step was to assure that the Dems took the Senate. Trump intervened in the two runoff races in Georgia, and at a minimum this cost Purdue his seat. With the Dems in total control of Congress and the Presidency, Biden soon became unpopular.

Now Trump’s trying to insure that the Dems hold at least the Senate in this fall’s midterms. Needless to say that is not an easy task, especially given all of the problems we face. But FiveThirtyEight claims the Dems are favored in the Senate. That’s an astounding indication of Trump’s ability to disrupt the natural course of events with some truly horrific endorsements. (Normally, the GOP would easily take the Senate in 2022.)

Politics is like a pendulum. When one party gets control of everything, it gives the out of power party the advantage in presidential races. The last thing Trump wants is a GOP Congress passing national abortion bans that get vetoed by Biden in the summer of 2024. That would force Trump to either come out as pro-choice (which he OBVIOUSLY is), or else take a public stand that would give swing voters a reason to vote for Biden.

Trump is an idiot, but he understands politics better than lots of very smart pundits. There’s a method to his madness.

As in 2020, Trump defied the oddsmakers. In the 2020 Georgia runoff, he sabotaged Purdue (who was on track to win) with his insane post-election nuttiness, which made the GOP seem toxic. This time, Trump worked his magic by promoting some of the most awful candidates you can imagine. Herschel Walker makes Caligula’s horse seem like Solon. (How motivated will GOP voters be in a runoff where Kemp is not on the ballot and Walker is the only guy they can vote for?)

At all costs, Trump wanted to avoid a highly unpopular GOP controlled Congress in 2024, just as he’s running for president. If that happened, swing voters would think, “We need Biden to veto their insane proposals—even Elon Musk says divided government is best.”

And it worked. Trump is an idiot savant. He doesn’t know if Finland is a part of Russia. But he knows politics better than our best pundits.

PS. Or maybe this post is just a spoof:

PPS. Go back and read the pundits at the National Review over the past month. LOL.

Over in Grand Rapids, Mich., the district elected its first Democrat to Congress, Hillary Scholten, in nearly fifty years over Republican John Gibbs. Gibbs won the party nomination on the strength of Trump’s endorsement over incumbent Peter Meijer, the only freshman House Republican to vote to impeach Trump for his role in the January 6 riot.

Meijer was one of the very few Republicans with an ounce of integrity, and like Liz Cheney he was “canceled” for telling the truth. Love to see that outcome.

PPPPS. The biggest loser on election night? Me!! it looks like we are a bit less banana republican than I had assumed.

Beckworth: But I want to read a quick excerpt here from what he wrote. He goes, “Africa was neither responsible for the pandemic nor the war in Ukraine. The first is undoing years of human development gains. The second has unleashed a wave of food and energy inflation. Now, the Fed is adding a potential debt servicing crisis to the cocktail.” He goes through examples like that, and I guess this raises the question, could this part of the perfect storm been avoided had the Fed raised rates sooner, say mid to late 2021? Now, again, this is hindsight and Monday morning quarterbacking, but let’s just say they could have seen all this coming. Would it have made enough difference to avoid some of these challenges today?

The Macroeconomic Hindsight of Earlier Fed Rate Hikes

Greene: I’m not sure it would’ve made a difference. When Chair Powell said, I think at the Jackson Hole Fed Conference, “Look, if we had hiked rates a few months earlier, it probably wouldn’t have made any difference at all,” I was pretty sympathetic to that view. I think it’s important to consider what the Fed is responding to in trying to figure out whether they’ve acted appropriately or not or if they had done something differently, if it might have helped. They were clearly responding to inflation, but the nature of inflation in the US is very different from the nature of inflation elsewhere, primarily because it’s got a big demand component to it. Whereas, in Europe in particular, inflation is mostly supply-driven. If the Fed had hiked earlier, maybe it could have headed off that demand spike a bit, but I’m pretty skeptical that it would’ve made a big difference and the Fed would’ve been the only major central bank in the developed world hiking at that point, so in terms of currency impacts, I still think the dollar would’ve been driven higher.

This is a good example of why I prefer not to discuss the stance of monetary policy in terms of interest rates. Monetary policy can affect interest rates in multiple ways, including the liquidity effect, the income effect and the Fisher effect. You might respond that in this discussion the implication is that higher rates are a tighter monetary policy. But in that case Greene is wrong, a significantly tighter monetary policy would have significantly slowed growth in aggregate demand.

So why is the economy still booming in late 2022? Because this particular increase in interest rates has not been associated with a significant tightening of monetary policy—NGDP growth continued at an extremely rapid rate in 2022. (Perhaps the Fed’s abandonment of FAIT has pushed the equilibrium interest rate higher.)

It’s OK to say that tighter money might involve higher interest rates.

It’s OK to say that higher interest rates might not slow AD.

It is not OK to say that tighter money might not slow AD.

Oddly (but not surprising to me), the questions asking about the effects of increasing and decreasing interest rates do not produce symmetrical answers.

Based on these responses, it seems as though roughly 3 in 10 Americans hold Keynesian views on monetary policy, a slightly larger number hold NeoFisherian views, and about one in 7 hold market monetarist views (interest rates don’t have any consistent impact on inflation.)

I wonder how economists would answer this survey question?

PS. Bonus election forecast: I predict a bad outcome when the votes are finally counted next month. My reasoning process is as follows. The US has become a banana republic (as even Trump now admits, and I’ve been saying for almost 7 years). Banana republics do not have good political outcomes. Hence the US will have a bad outcome.

PPS. Bonus global forecast: Authoritarian nationalism is on the rise almost everywhere. Thus (as in 1914-45), the world faces a bleak future.

In America, it’s not easy to figure out exactly what’s going on with monetary policy. Europe is even more opaque. Indeed we still don’t know the third quarter figures for Eurozone NGDP, and won’t find them out for months. Nonetheless, I’ll take a stab at the question, as well as a few observations on the UK.

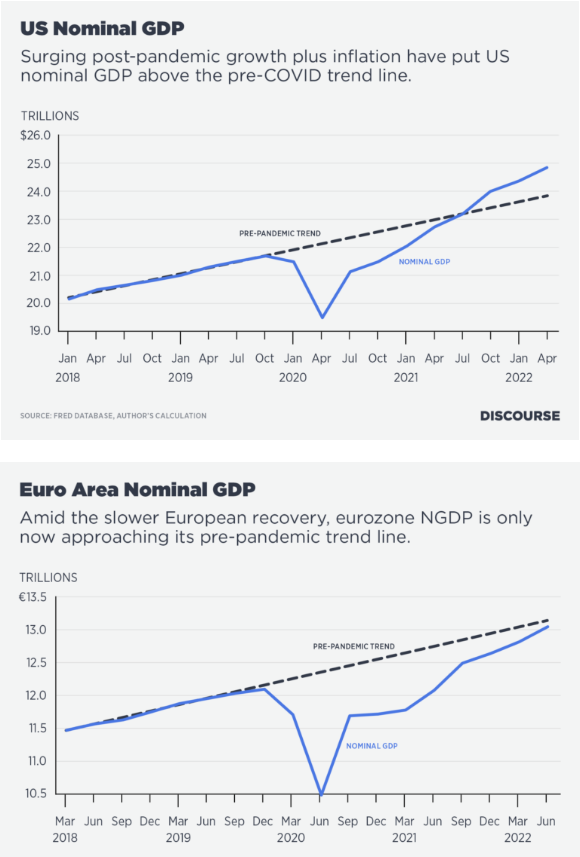

David Beckworth has an excellent Discourse article on inflation, which contains these graphs:

At first glance, it look like the US economy has overheated and the Eurozone economy is back on track. The US is quite overheated, but the Eurozone picture is a bit more complicated, for several reasons:

1. The Eurozone NGDP data is quite dated, and (AFAIK) recent NGDP growth has been quite high.

2. The pre-pandemic trend is not necessarily the optimal policy path. Suppose the Fed favored a NGDP growth target of 2% plus trend RGDP growth (a reasonable idea.) And suppose they noticed that America’s RGDP rose at an annual rate of 2.25% between 2009:Q4 and 2019:Q4. They then decided to target NGDP growth at 4.25%. Unfortunately, that policy would not succeed in the Fed’s objective of ensuring 2% long run inflation, as they’ve overestimated trend growth. The unemployment rate was 10% in late 2009, and fell to 3.5% in late 2019. They would have estimated trend growth over the expansion phase of the cycle, not the entire cycle. The actual trend RGDP growth rate in America is now about 1.5%, and lower still in Europe and Japan.

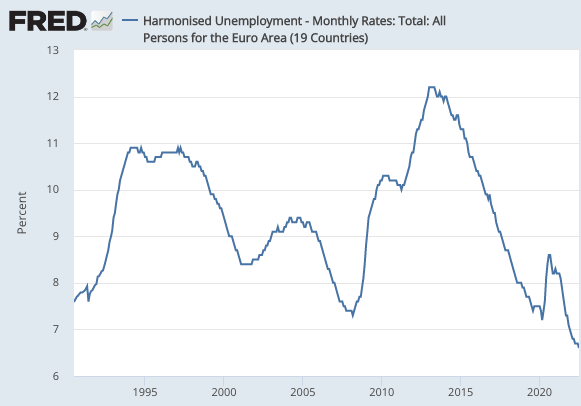

Notice that Eurozone unemployment had been falling rapidly prior to Covid, reaching a record low of 7.2% in March 2020. During the recent recovery, it’s fallen even lower:

So the Eurozone trend RGDP growth rate is also lower then its pre-Covid trend.

When people say something cannot go on forever, they are often wrong. The US trade account deficit can go on forever, or for at least as long as our multinationals earn big profits overseas. But a falling unemployment rate really cannot go on forever. So the trend rate of Eurozone NGDP growth might overstate the optimal rate by at least a little bit.

On the other hand, I see two pieces of evidence pointing the other way, against the view that the Eurozone is overheating:

1. Even if David’s graph incorporates a trend line for NGDP with slightly above average RGDP growth, the Eurozone has also been mostly undershooting its 2% inflation target. So perhaps that trend line is about right.

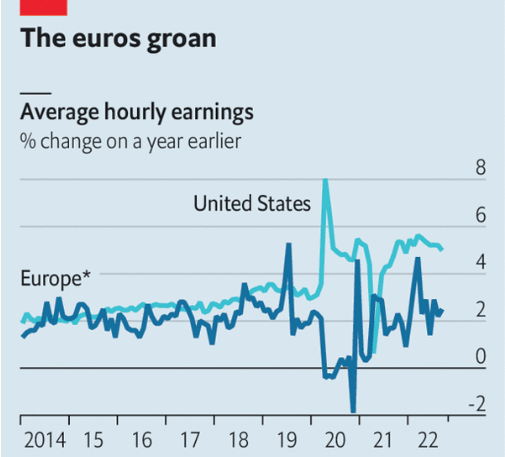

2. There’s little evidence thus far of demand-side overheating in the Eurozone wage date:

On the other, other hand, there are composition effects to consider, as well as lags. The Economist warns us that Eurozone wage inflation may be about to take off:

So far, European pay has increased little. Unlike in America, six in ten workers have collective-bargaining agreements, which tend to run for a year or more—meaning it takes time for economic conditions to influence their pay. Trade-union negotiators have limited demands, aware that a wage-price spiral would come back to haunt them. But negotiators’ patience is beginning to wear thin. Germany’s public-sector unions will enter forthcoming negotiations seeking a raise of 10.5%.

The problem for bosses is that the labour market remains exceptionally tight. The share of firms reporting that staff shortages are limiting their production is near record highs in both the manufacturing and service sectors. One reason is the enormous backlog of orders from the pandemic. Manufacturing firms have on average more than five months of work on their order books, according to a recent survey, up from four before covid struck. Add to that the cohort of workers retiring each year in ageing countries such as Italy and Germany, and a recipe is in place for a tight labour market throughout 2023.

All of this means the peak in inflation is probably some way off.

So I remain agnostic on the wage question. I’m quite willing to accept the view of Eurozone doves that the inflation problem has been almost entirely supply-side up through mid-2022. I’m less sure of the situation now and going forward, and indeed am puzzled as to why the Economist predicts tight Eurozone labor markets in late 2023. I thought all the experts were telling us that a Eurozone recession was inevitable in 2023? The situation remains confusing, at least to me.

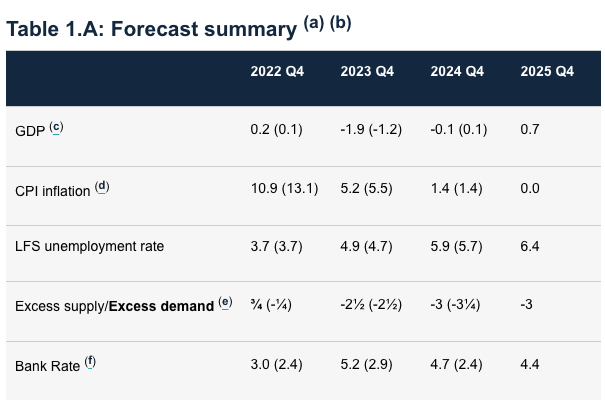

The situation in the UK is equally perplexing. Here’s a table from the BoE:

By adding GDP growth and CPI inflation, we get a very crude estimate of expected NGDP growth, which slows from 11.1% in 2022 to 0.7% in 2025. The average growth rate over that 4-year period (about 4.1%) is relatively high compared to the roughly 3% to 3.5% (post-Brexit) trend NGDP growth required in the long run for the BoE to hit its 2% inflation target. On the other hand, much of the fast growth in 2022 is a recovery from the Covid slump.

The British case raises a number of tricky questions. Is NGDP level targeting even appropriate? If so, where should we draw the trend line? If you look at RGDP growth and unemployment, 2023-24 looks like a recession. So why are forward markets forecasting a Bank Rate of 4.7% in late 2024? I’m genuinely puzzled.

I suspect that over the next few years I’ll revise some of my assumptions about how the macroeconomy works. One casualty might be Okun’s Law, which has performed very poorly in the US during 2022. Another might be my assumption about secular trends in interest rates, TIPS markets, and the Phillips Curve. Right now, US forward markets are forecasting high interest rates in 2023 and 2024. They are also forecasting PCE inflation falling back close to 2%. Larry Summers says that that sort of fall in inflation cannot happen without a recession. His claim seems plausible, but then why are fed futures so high in 2024? Wouldn’t interest rates fall sharply in a recession? And if the answer is that markets don’t trust the Fed to bring inflation down, then why don’t the TIPS spreads reflect this?

Over the next few years, at least one of our major assumptions about how the macroeconomy works is likely to need revision. A few years back, Tyler Cowen spoke of a Great Stagnation. I wonder if the world isn’t about to enter an even greater stagnation. Very low RGDP growth, and yet a surprisingly low unemployment rate. We will see.

Welcome to a new blog on the endlessly perplexing problem of monetary policy. You’ll quickly notice that I am not a natural blogger, yet I feel compelled by recent events to give it a shot. Read more...

My name is Scott Sumner and I have taught economics at Bentley University for the past 27 years. I earned a BA in economics at Wisconsin and a PhD at Chicago. My research has been in the field of monetary economics, particularly the role of the gold standard in the Great Depression. I had just begun research on the relationship between cultural values and neoliberal reforms, when I got pulled back into monetary economics by the current crisis.

"#5 seems like it is clearly a reflection of the stereotype of immigrant small local businesses: dry cleaners, restaurants, lawn services, etc. It may be that these small businesses really..."

"You are inching closer to admitting the gravity of digital deflation and unmeasured GDP. You aren't there yet, but I can smell it. To help get you there.... I have..."

"Can, I wonder if "flight to liquidity" is a better description than flight to safety. US TIPS are ultra safe, but fell sharply in price. I find the Russia trolls..."