Yes, there’s a third wave now (for all you people who insist we are technically still in the first wave.) But will it affect the election?

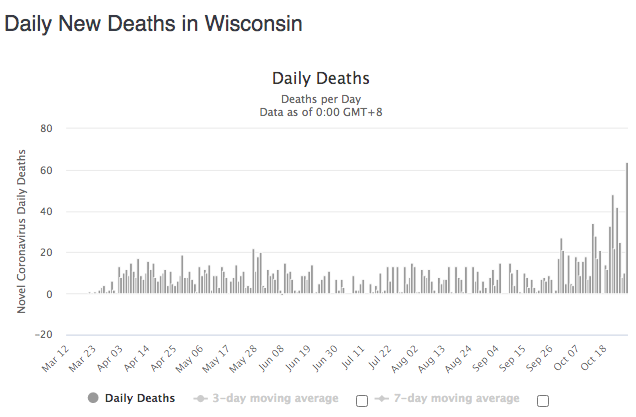

Wisconsin has recently been hit harder than any other electorally important state. Until September 30th, it had never seen more that 22 deaths in one day. Yesterday my home state had 64 deaths.

Is this affecting the race? A week ago, Biden had a 6.3% lead in the Wisconsin poll average (using 538). Now it’s 8.4%. Biden’s lead is also widening slightly in nearby Minnesota, Michigan and Iowa.

Wisconsin is just one state, but if you believe the third wave is hurting Trump, the most dramatic effects should be in states where it’s only recently become a big problem. But in that case, the smaller Covid surges in other states might be having a smaller but still meaningful impact on their races.

On the other hand, and this is important, the national polls are tightening somewhat as we approach election day, just as I expected. Pennsylvania is also getting tighter. So there presumably are other factors pushing in Trump’s favor. Nonetheless, if Trump were to lose a close race, the Covid third wave could be decisive, at the margin.

PS. After reading Kavanaugh’s disgraceful comments on whether late votes might “flip” the election, I am so done with conservative claims that, “At least Trump put good people on the Supreme Court”. No, he put immature GOP party hacks on the Supreme Court. I wish Merrick Garland were there instead.

Hypermind has two new NGDP prediction markets up and running, one covering 2020:Q4 to 2021:Q4, and one covering 2021:Q4 to 2022:Q4.

It’s early, and I don’t believe there’s been much trading, but so far the predicted growth rates are rather low (below 4%.)

I hope to get the new markets embedded here soon, but feel free to start picking up some of the $100 bills on the sidewalk (actually Amazon coupons.)

And once again, people with more money and power than me should be working hard on getting a highly liquid NGDP prediction market up and running. A high quality NGDP prediction market is like a billion dollar bill that’s lying on the sidewalk. So why has the federal government been too lazy to pick it up?

Bush was president when we plunged into the Great Recession, and Trump presided over the recent slump. Should they be blamed? I’m not sure, although I suspect that in both cases the president played only a very modest role in causing the recession.

On the other hand, I believe that voters were much more likely to blame Bush than Trump, and that’s one reason why the GOP lost so badly in 2008.

You might argue that polls show Trump losing just as badly as McCain, but those same polls show that Trump gets fairly high marks for the economy. Voters blame him for other things—mostly the lackadaisical response to Covid-19.

Let’s start with a few obvious points. Both recessions were global, and both were considerably worse in Europe. That doesn’t exactly point to a scenario where the US president is to blame. I suppose that Europe’s recessions could be the ripple effect of a US instigated shock, but ripples are almost always smaller than the original shock, not bigger.

The most likely explanation for the recent recession is that almost all countries were hit by the global Covid shock. You can say Trump didn’t do his part, didn’t encourage testing, masks, social distancing, etc., and I’d agree. But there’s not much evidence that a better president would have prevented a severe recession in 2020. I do blame Trump for not doing his part; I just don’t believe it would have been decisive.

The most likely explanation of the Great Recession is that a real estate slump lowered the natural rate of interest, and central banks such as the Fed and ECB did not lower the policy rate fast enough, effectively tightening policy. You could argue that Bush should have appointed someone better to lead the Fed, but his appointee did far better that Trichet at the ECB. (I favored Bush appointing Bernanke.) So it’s simply not realistic to presume that Bush played a major role in the recession.

Others point to “deregulation” such as the repeal of Glass-Steagall, but banking was never deregulated and the Glass-Steagall repeal had little impact.

Others (on the right) point to government efforts to put as many people into houses as possible, and Bush does share some of the blame here, but lots of others were involved in that effort. And that played only a minor role in the recession.

Given the fact that the public votes with limited information, it’s reasonable for them to blame leaders when things go bad, even if leaders only are responsible for 3% of outcomes. How else can voters encourage leaders to do their best?

I’d say it’s rational for voters to view Trump positively on economics (a view I don’t fully share–I’m more neutral) and negatively on Covid. And it was rational for voters to blame the GOP for the recession in 2008, despite the fact that it was mostly bad luck. And that’s despite the fact that I happen to view these two presidents as equally responsible for the two recessions. The point is that the public needs to hold presidents accountable for the modest role they play, or the democratic system cannot work. And the public works with limited information.

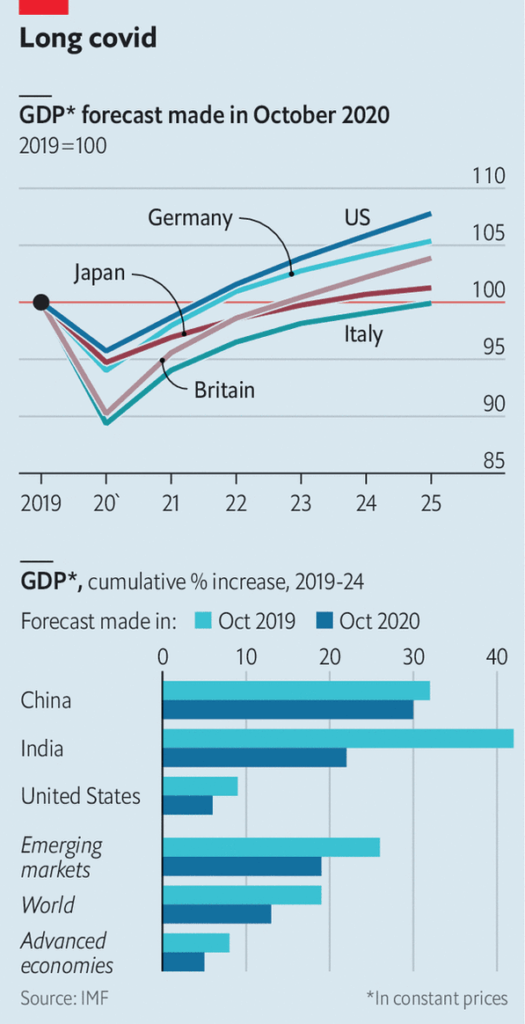

1. What’s up with India? And another lost decade for Italy?

2. Less immigration might slow growth in the US, but the slowdown is a global phenomenon. Immigration is a zero sum game for the world, and yet world growth is expected to slow.

[Update: I meant zero sum for the global labor force. Several commenters pointed out that it’s not zero sum for global GDP, because labor moves to where it’s more productive. I should have said, “and yet growth is slowing in each region.”]

3. It seems likely that Covid-19 will be over long before 2025, so there seem to be some semi-permanent effects. Why? It looks like a loss of roughly 3 percentage points in the US (or 0.6% per year for 5 years).

4. Perhaps the Fed won’t allow enough NGDP growth, and some of the lost growth will be employment related.

5. Or maybe productivity growth will slow. That could be due to less capital accumulation resulting from less investment during Covid, or slower technological progress.

6. The IMF forecasts may be wrong; maybe growth will not slow. Or maybe it will slow for reasons unrelated to the IMF model, such as Biden policies. (I doubt Biden would have a big impact, but who knows?)

7. But growth is expected to also slow outside the US, and the Great Recession also led to sharp reductions in long run RGDP forecasts for many countries, including the US. Why aren’t we expected to bounce back to trend?

I’d like to end up with a slightly different hypothesis, which I’ve been discussing on and off for almost a decade. Maybe trend growth is slower than we assume. Growth during 2009-2019 was in the 2% to 2.5% range, but that was entirely during the expansion phase of the business cycle. During that period, unemployment fell from 10% to 3.5%. That’s unsustainable.

The correct way to measure trend growth is to compare two widely separated years with similar unemployment rates. That approach often yields trend growth estimates that are lower than the consensus. If the IMF is correct, then total growth between 2019 and 2025 will be roughly 7.8%, or 1.3% per year. Maybe that’s the new normal. After all, population growth is gradually slowing, and productivity growth is also slow, although poorly measured.

I’ve recently been saying the new normal is 1.5% measured trend growth, and I’m sticking with that. FWIW, if the IMF is correct about the 7.8% growth from 2019-25, then RGDP growth from 2007:Q4 to 2025:Q4 will average 1.54%. If unemployment is around 4.5% in 2025 (as in 2007), then that will likely be the new long run trend. That’s relatively bad, and may help to explain why we see such low real interest rates.

PS. I say “relatively” bad; it still means the richest big country the world has ever seen will keep getting richer and richer and richer. It beats living in a disease-ridden London slum in 1831. Or a rural French village in 1324. Those people did not have pet psychologists to address depression in dogs and cats. We are bursting with happiness; I see it on twitter every single day. 🙂

There has also been a surge of early voting, with almost 53m Americans having already cast their ballot either by mail or in-person, according to the US Elections Project.

In Texas, almost 6.4m voters have cast their ballots, equivalent to more than 70 per cent of the total number of votes cast in 2016.

And there’s still 10 days until the election! So can we assume that 80% or 90% of Texans will have already voted before November 3rd? What does that mean?

I used to focus on the polls released the day before the election. Do we now need to take the integral of the poll gap for the entire month preceding an election?

Even that’s not enough, as the undecided voters might be more inclined to wait to the last minute. Or maybe not. The debates are all over; why not just decide now, and get it over with? I already voted.

And we need to figure out which party is helped by mail-in votes. It seems that more Dems vote by mail, but who does that help? Does it help the Dems because it boosts turnout? Or hurt them because a few percent of ballots are declared void due to some problem? (Such as not being signed.) I have no idea.

Usually, when people say, “Be realistic, it’s over”, they mean it figuratively but not literally. I.e., it’s not literally over, but we know who will win. In Texas you might say, “It’s over” and mean it literally but not figuratively. The votes have been cast, but we don’t know who has already won.

Maybe I’m getting old, but I have trouble wrapping my mind around this new reality. I can’t shake the notion that “Election day” on November 3rd is an important day, even though apparently it is not. It’s a day when we’ll discover something important that happened weeks ago.

PS. Two months ago, we knew with 100% certainty that the Trump people would release a sketchy Biden “scandal” a week or two before the election. When it actually happens, Bayesians will not update their view of Biden at all, as it’s not “new information.” It’s not that Bayesians ignore the information—they already knew about it.

Bayesians knew that if Trump supporters actually had something, they’d release it two months early and hammer Biden relentless over the two months before Election day. If it were a phony story, they’d release it two weeks early and hope there wasn’t enough time to discredit the story before Election day.

Welcome to a new blog on the endlessly perplexing problem of monetary policy. You’ll quickly notice that I am not a natural blogger, yet I feel compelled by recent events to give it a shot. Read more...

My name is Scott Sumner and I have taught economics at Bentley University for the past 27 years. I earned a BA in economics at Wisconsin and a PhD at Chicago. My research has been in the field of monetary economics, particularly the role of the gold standard in the Great Depression. I had just begun research on the relationship between cultural values and neoliberal reforms, when I got pulled back into monetary economics by the current crisis.

"Couldn't find the substack and if it's moderated just as well... Voted for Trump and he won. Sorry liberal Scott Sumner who believes in money non-neutrality, which is akin to..."

"Scott, Quick note of thanks. I've hugely enjoyed your blog and the intellectual stimulation I gotten from it. Also it was pleasure getting to know you and your wife. Hope..."