In 2015, the UK Conservatives did better than predicted by the polls. In 2016, Brexit did better than expected. At the time, I did a post pointing out that the surprise Brexit vote was bad news for Dems (although I later botched the election itself.)

Yesterday, (conservative) Liberals won a surprise victory in Australia. This is also bad news for Dems. It’s becoming increasingly clear that polls consistently underreport support for the more “politically incorrect” political party in Anglo-Saxon countries.

One glimmer of good news is that Democratic voters seem to be leaning toward more “electable” candidates such as Biden. Even though Biden is not particularly popular among progressives on the two coasts, all that matters is the “Obama/Trump” voters in the Rust Belt. NOTHING ELSE MATTERS. The Dems must win Wisconsin, Michigan and Pennsylvania.

On balance, I think the Aussie election is more important and points to a likely Trump win in 2020.

PS. The Aussie economy is doing fine, but they have the same political polarization that we do:

Even by Australian standards, the leadership coups at public broadcaster ABC last week, which led to the sacking of managing director Michelle Guthrie and the resignation of chairman Justin Milne, have been brutal.

They have also highlighted the hyper-partisan nature of the country’s politics and the wider “culture wars” between conservatives and progressives, which are polarising debate and risk undermining confidence in public institutions.

Tariffs are generally assumed to have an inflationary effect on the economy. I imagine that’s true in most cases, say a developing country with a newly elected populist government. But is it always true?

In my (still underrated) book on the Great Depression, I explained how the Smoot-Hawley tariff had a deflationary impact on the US economy. Stock and commodity prices fell sharply in April-June 1930, as the bill moved toward passage. The biggest stock market crash of 1930 occurred right after Hoover announced that he would sign the bill.

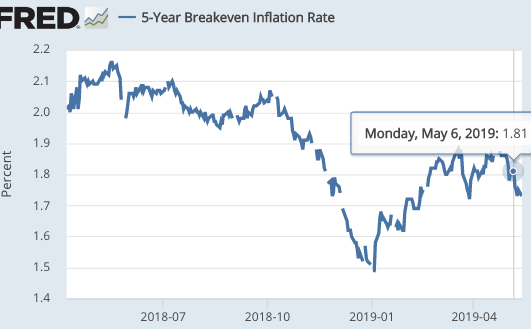

The same appears to be true of the recent trade war with China, which triggered a narrowing of the 5-year TIPS spread, down .08% to 1.73%:

In both 1930 and today, the Fed could have prevented a contractionary impact by an aggressive easing of policy. But in both cases they were reluctant to ease too rapidly, as that would make their previous rate increases look mistaken. (I’ve discussed this problem in previous posts, which is why I prefer daily rate adjustments, to the nearest basis point.)

I suppose that one could also point to the Fed being reluctant to look like they were being bullied by Trump, although that’s highly speculative.

The Fed funds futures now show one rate cut by year end, and another by mid-2020. That does not mean that money is currently too tight, as rates should move up and down with changes in economic growth. A better argument for money being too tight is that the newest Philly Fed forecast for 2020 inflation has dropped to 1.9%, and I suspect even that’s a bit too high, as market indicators suggest even lower inflation.

That doesn’t mean that everything is gloom and doom; the economy will probably do fine if inflation runs at 1.7% over the next 5 years. But if the Fed is going to have a 2% inflation target, it is better that they actually hit their target—if only to put them further from the zero bound.

Trump is arguing that the Fed needs to cut rates because of the trade war with China. Is Trump correct? The 5-year TIPS spread suggests that a rate cut would indeed be appropriate. But given my severe case of TDS, I’m reluctant to give him any credit. I hope readers won’t be offended if I point out that his argument makes no sense. Trump insists tariffs have an expansionary impact on the US economy. If that actually were the case (it isn’t), then Trump would be wrong in arguing that the trade war provides a rationale for the Fed to cut rates.

Trump is probably of two minds. His primitive understanding of trade theory leads him to view tariffs as expansionary, whereas the strongly negative view of stock investors toward tariff news triggers fear in the reptilian part of his brain. (And really, is there any other part?) And that fear leads him to call for the Fed to assist him in the trade war.

PS. Slightly off topic, but this David Beckworth tweet gets to the heart of the problem with monetary policy:

Here is my real critique: the Fed can get all the new tools in the world–neg rates, yield curve control, auto QE, etc.–but with a low inflation target regime they probably won’t matter much. IMHO, the past decade has shown us it is the monetary regime not the tools that is key.

I worry that the profession is focused too heavily on technical gimmicks, and is missing the bigger picture.

Oh, I know that Trump wants the Fed to cut its target rate ASAP. But that’s not my question. My question is whether Trump actually wants lower interest rates over an extended period of time.

Well, President Donald Trump got his interest rate cut… sorta.

Trump warned on Twitter over the weekend that tariffs on $200 billion in Chinese goods could rise to 25% on Friday. He added that a 25% tariff will soon be assigned to a selection of $325 billion in presently untaxed goods.

The proclamation uprooted the latest push higher in stocks globally, with the bellwether Dow Jones Industrial Average losing more than 400 points early on in Monday’s session. But, the yield on the 10-year Treasury note dropped to 2.48% as investors flocked to the government-backed safe-haven. . . .

So, in effect, with a series of tweets the president managed to make it cheaper — at least for the short-term — to take out a mortgage or buy stuff on variable rate credit cards. . . .

“He got what he wanted on rates,” AGF Investments Chief U.S. Policy Strategist Greg Valliere told Yahoo Finance Monday.

Trump has made his views on Federal Reserve Chair Jerome Powell no secret.

Actually, Trump has made his preferences a secret. Trump has never told anyone how he would like the rate cut to be accomplished. He hasn’t told us whether he’d prefer a brief rate cut, followed with considerably higher interest rates over time, or whether he’d prefer a policy that cut interest rates over an extended period of time. The former involves easy money and the latter involves tight money.

In other words, Trump hasn’t told us whether he’s a low rate guy who favors slow NGDP growth, or whether he’s a high rates guy who favors fast NGDP growth.

You may think you know what he wants, but he’s never told us.

In any case, Yahoo is right. Trump’s recent actions did result in an interest rate cut. All of you who insisted that “Trump was right about the need to cut rates” can now bask in your “success”.

I hate flying. There’s driving to the airport, then looking for a parking space, then airport security, (some tickets even require you to get a boarding pass at the airport), then waiting in a slow moving line to board the plane, then sitting in a tiny seat for 20 minutes before the plane actually takes off, then a bumpy ride, then waiting a long time to get off the plane. You might even have been forced to put your carry on bag in the luggage section at the last minute, requiring you to wait at baggage claim.

I love trains. They are smooth and spacious and comfortable, at least if you live outside the US. So will someone explain the following to me:

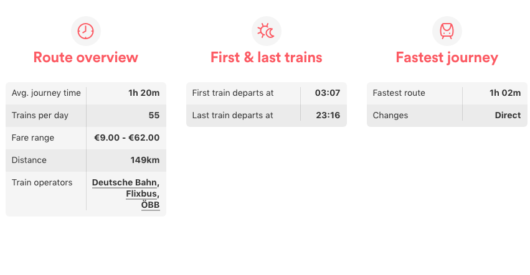

Moritz Leiner, a representative of the Association of Ethical Shareholders Germany, urged Lufthansa to reconsider its climate-change policy, pointing out that the company operates four daily flights from Munich to Nuremberg, two cities that are only a two-hour drive apart.

The driving time seems like an odd comparison, so I goggled some train data for Munich to Nuremberg:

So there are 55 trains a day, with an average time of 1:20 and the fastest at 1:02. I understand why people fly when the cities are far apart. But why do people take short flights? Can someone explain what I’m missing? It seems like low hanging fruit for the fight against global warming. And I’m not even a fan of high speed rail boondoggles in places like California. But what about where you already have decent train service? Why fly?

PS. I’m usually sitting around row 37. Sometimes I wonder what would happen if every passenger in front of me was a Navy Seal. How long would it take them to stand up, grab their carry-on and walk off the &$#*@&$ plane. The actual humanity in front of me takes forever, exhibiting an especially annoying mix of selfishness and clumsiness.

[Before starting, let me recommend a new Sebastian Edwards paperdiscussing the effectiveness of MMT-style policies in Latin America. I have a new post at Econlog.]

Last year, I did a post over at Econlog speculating that cycles in the price of oil led to cycles in fracking activity, which led to cycles in manufacturing employment growth.

Seven months later, the fracking/manufacturing part of the hypothesis is looking increasingly plausible. For various reasons, fracking activity has slowed in recent months. In this case, however, the slowdown is not due to weak oil prices, and experts predict a pickup later in the year:

Schlumberger CEO Paul Kibsgaard told analysts and investors last week that his company is seeing a slowing-down of activity in the U.S. shale plays over the first four months of 2019. “North America land activity is set for lower investments with a likely downward adjustment to the current production growth outlook,” Kibsgaard said, “the higher cost of capital, lower borrowing capacity and investors looking for increased returns suggest that future E&P investments will likely be at levels dictated by free cash flow. We, therefore, see land E&P investment in North America down 10% in 2019. ”

Overall, employment growth in 2019 continues to be strong, running at 205,000/month, only slightly below 2018 boom levels. But manufacturing job growth is slowing more rapidly, with growth especially anemic over the past three months. Year-over-year data shows the rate of manufacturing job growth slowing from a peak of 2.3% in July 2018 to 1.6%, and I expect a further decline.

Notice that there was also a manufacturing jobs boom during the 2014 fracking boom.

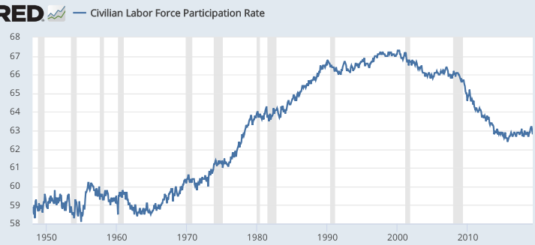

Labor force participation in April was 62.8%, exactly the same as 5 years ago. But that’s actually good news, as the retirement of boomers was expected to lead to further declines. On the other hand, I doubt we’ll get back to the levels of the late 1990s; there are too many demographic headwinds:

The 3.6% unemployment rate is consistent with what we are seeing in other similar developed economies. Relatively “neoliberal” economies are seeing unemployment fall to rates not seen since the 1960s. What makes the US stand out is that productivity numbers have also been pretty good (unlike places like the UK.)

Job growth in the US is also helped by a recent surge in immigration. Overall, a very good jobs report. It shows that manufacturing is not the key to strong employment gains, but fracking is the key to strong manufacturing jobs gains.

PS. Speaking of the UK, I predict their next election will feature Trump vs. Sanders, err, I mean Boris Johnson vs. Jeremy Corbyn. If the Liberal Democrats can’t do well against those two clowns, it’s time to close up shop. If the Brits had any sense, they’d make Rory Stewart their PM. But only after Brexit is resolved—that’s one of those problems that would destroy any leader.

Welcome to a new blog on the endlessly perplexing problem of monetary policy. You’ll quickly notice that I am not a natural blogger, yet I feel compelled by recent events to give it a shot. Read more...

My name is Scott Sumner and I have taught economics at Bentley University for the past 27 years. I earned a BA in economics at Wisconsin and a PhD at Chicago. My research has been in the field of monetary economics, particularly the role of the gold standard in the Great Depression. I had just begun research on the relationship between cultural values and neoliberal reforms, when I got pulled back into monetary economics by the current crisis.

"No. 2 But then again, an entirely pious US foreign policy would probably result in the US having been zero allies. Bharat appear ascendant and more democratic than any other..."