Zero fiscal multiplier, Ed Balls edition

Here’s Britmouse:

. . . here’s a quote from a Bloomberg interview with Ed Balls from yesterday, hat tip to Richard Williamson:

Guy Johnson: Ed Balls, you do have your economics GCSE, we all know that. Do you think the change in the [BoE] mandate will lead to higher inflation?

Balls: No, because I think the Bank of England will do its job, and it’s got a very clear remit to meet a symmetric target of 2% and that’s not changed.

My emphasis. Yes, I omitted transcribing the previous question in the interview where Balls talked about a liquidity trap and how monetary policy was “pushing on a string”… so shoot me.

And Dan S left this comment in my previous post:

Along the same lines, a character named “Economist Hulk” has popped up on Twitter in the past couple days. My favorite so far: “HULK CONFUSED BY @EDBALLSMP. WANTS FISCAL STIMULUS BUT TO KEEP 2% INFLATION TARGET. HULK NOT AWARE OF MACRO MODEL WHERE THIS MAKES SENSE.”

Perhaps supply-side models. The world of Keynesian economics continues to entertain and amuse.

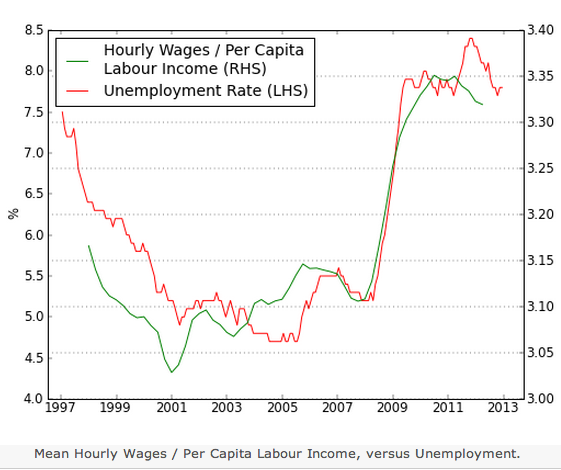

BTW, Britmouse also produced this excellent graph, illustrating the “musical chairs” problem in Britain:

Tags:

28. March 2013 at 10:15

Stop this “unemployment” nonsense – British employment-to-population ratios recovered over half of their losses by now, and net job growth is very strong.

“unemployment” is the most meaningful concept of all concepts in economy.

28. March 2013 at 15:40

So this is unrelated but you might find this link interesting. It reminded me of why you think the current account for the US is largely irrelevant and that the capital account should be taken into account(pun).

http://www.bloomberg.com/news/2013-03-28/proving-greenspan-wrong-shows-why-rey-became-worthy-to-bernanke.html

28. March 2013 at 16:52

http://media.bloomberg.com/bb/avfile/Economics/On_Economy/vxQUQaB5duvE.mp3

The Hays Advantage Podcast

Kathleen Hays with co-host Vonnie Quinn covers business stories with top-tier guests

Bentley’s Jackson, Larsson, Moore Discuss Fed Challenge (Audio)

Mar 28, 2013

Aaron Jackson, associate professor of economics at Bentley University, and Erik Larsson and Tom Moore, two students who were on the university’s 2012 Fed Challenge team, discuss how they placed first in the regional competition and won second place in the national round. They spoke with Bloomberg’s Kathleen Hays and Vonnie Quinn on March 27 on Bloomberg Radio’s “The Hays Advantage.”

29. March 2013 at 00:23

HULK ASTONISHED TO TURN UP ON MONEY ILLUSION. HULK VERY INFLUENCED BY SCOTT SUMNER. HULK CONVINCED BY YOUR CRITIQUE OF HOW MOST PEOPLE THINK ABOUT MACRO, HOWEVER HULK NOT YET WILLING TO GO FULL MARKET MONETARIST. BUT HULK HOPE YOU KEEP UP THE GOOD WORK.

29. March 2013 at 00:24

The magic 2 percent ceiling on inflation.

That is the divine number, unless it be 0 percent. Major central banks everywhere genuflect now to this exalted wisdom (except the People’s Bank of China, which will tolerate a 4 percent ceiling. How is their economy doing? Rip-roaring, why do you ask?)

No one ever says where this sanctified 2 percent comes from.

Let me pose a fact: Real per capita income rose by more than 30 percent in the 1960s. In the 1950s, you might see a kid with rickets in the USA. By 1970, no.

Structurally, the USA economy was a mess in the 1960s. The private labor force was 50 percent unionized, the top tax rate was 90 percent. The banks, Wall Street, phones, airlines, trucks, trains and cars were heavily regulated. Little foreign competition.

The Fed stimulated, and got results anyway. Huge results. Real incomes up about one-third in one decade. The sense of better material well-being in the 1960s was nearly palpable. Fat City baby.

So now what do we hear from economists about the 1960s?

Only “waa-waa.”

You see, inflation popped its head above 5 percent in 1969. Horrors. The decade was a failure.

Give unto me such failures every decade.

So now we will have a decade with inflation under 2 percent. Who is happy now?

Central bankers and inflation-obsessed economists.

29. March 2013 at 01:28

As I am sure I have explained to you before, Benjamin, the 2% comes from the idea, eg as expressed by Greenspan in the early 90s, that central banks should aim to reduce inflation to a level at which it does not need to be factored into the decisions of households and businesses. That level is considered to be about 2%. Higher than that and households and businesses begin to introduce indexing mechanisms that make inflation more volatile. Lower than that and you get too close to deflation for comfort (I suspect that fears of deflation are overdone, as Japan’s experience suggests, but never mind). In short, far from inflation-obsession, the whole point of the 2% target is that it allows inflation to be forgotten for practical purposes.

29. March 2013 at 03:25

Daniel, Yes, but I’m surprised they present that as a new idea. I’ve been hearing that argument since at least the 1990s.

Steve, Thanks, I should provide a link.

Hulk, Now I know what I miss by not doing twitter.

29. March 2013 at 15:59

Isn’t the 2 % target justified by reference to hedonic assessments of the reliability of price indices? – Boskin etc.http://www.stanford.edu/~boskin/Publications/CPI.pdf

29. March 2013 at 20:25

Rebel–

Inflation, schmaflation.

There are times when the nation needs Fat City. Like now.

Households and business introduce indexing? Yes, and with unions dead, how do workers index? And with foreign competition, can the Big 3 raise prices in concert anymore?

Huge pools of capital are waiting to be invested, if only there is a hint of boom times ahead. We could have a great boom, and you know what? When businesses add capacity that holds down inflation. And when production goes up, that holds down unit costs. The overhead gets spread over more units.

Bernanke should put the lever on “High” on the printing presses, and take a long vacation in the Caribbean.

And why does a 4 percent ceiling seem to work in China, while a 2 percent ceiling in the USA/Europe has been asphyxiating?

Egads, man. Real incomes up more than 30 percent in the 1960s. And you contend that well, since inflation was above 2 percent it was tainted?

30. March 2013 at 02:39

China is still a rapidly growing economy, Benjamin. Higher inflation is part of the way in which China’s growing prosperity spreads to, eg, service producers like haircutters (ie the Balassa-Samuelson effect). Also, China’s consumption basket gives a heavier weight to food and energy, which tend to have more volatile prices, so a higher ceiling would be appropriate anyway.

As you know, I would attribute the present economic weakness despite corporate cash piles to excessively easy monetary policy. Businesses suspect that the reckoning is not complete, and are therefore reluctant to commit to major projects. Note how the US, where some assets, notably houses, were allowed to fall in price, has lower inflation and higher growth than the UK, where such asset prices have been propped up.

30. March 2013 at 07:44

By the way, Benjamin, from Scott’s money and inflation part 3 panel data: US 1950-90 inflation 4.2% RGDP growth 3.1%, W.Germany 1953-90 inflation 3.0% RGDP growth 4.1%.

30. March 2013 at 10:51

Pyrmonter, No, because there is no good theoretical reason why zero “true” inflation would be optimal. I’d add that those estimates are mostly just wild guesses. There’s no good theory underlying the method.

Rebeleconomist, Do you recall that Germany was recovering from WWII in the 1950s and 1960s, and the US wasn’t?