Why was the yield curve inverted before WWI?

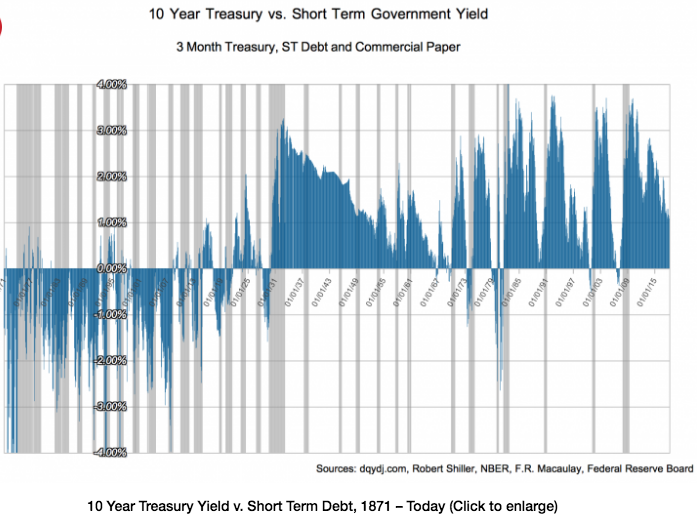

I recently came across a surprising graph:

It’s hard to read here, but if you go to the link and click on the graph, you’ll see a much bigger version.

There are some technical issues with its construction, which are discussed in the article. But when I looked at the raw data it seems plausible to me that the yield curve really was inverted during most of the 40 years before WWI.

Does anyone know why?

Tags:

21. August 2019 at 05:20

Just speculating: their graph starts at 1871. So perhaps it might have something to do with the US paying down their civil war debt in some weird way?

(It would be interesting to see the same yield curve measure for eg the UK.)

21. August 2019 at 05:26

Perhaps the demand for longer dated bonds from insurance companies was enough to keep it persistently inverted. Those investors would not be interested in trying to take advantage of an inverted curve by buying short and selling long if it meant that their asset duration meaningfully departed from their liability duration.

21. August 2019 at 05:27

Very cool chart!

Answering your question might require answering a different question first: Is the yield curve really providing an indication of the expectations for either disinflationary (falling inflation) or deflationary (negative inflation) conditions in the future?

Also note that you might really be asking a different question: Why was the yield curve inverted before the Fed came into existence? Since the Federal Reserve Act wasn’t passed into law until 23 December 1913, while World War I began on 28 July 1914, the timing of WWI is perhaps very coincidental, especially if you ask why didn’t disinflationary or deflationary conditions prevail in the period following the beginning of the Fed (or WWI).

21. August 2019 at 05:39

1880 through 1920 was the period with the lowest 10-year Treasury rates on record, until now and a brief fling in World War II, so short-term rates did not have to be that high to be higher than long-term rates.

My guess is that to issue bonds long-term, an issuer had to have a very high credit rating, such as a railroad bond or government. Lesser credits issued short-term debt.

To issue short-term debt, the government had to compete against other short-term issuers who were offering higher rates. Perhaps credit analysis was iffy in those days. Perhaps buyers of short-term debts faced some sort of transaction costs.

21. August 2019 at 05:47

Deflation.

21. August 2019 at 06:06

Perhaps it is because there was no inflation premium for longer-term bonds. E.g. the gold standard arrangement differed from that which followed WW1 and preceded the Great Depression and also there was probably greater price/wage flexibility in the short-run before unionization started to really take hold after WW1.

As a result, the variability of inflation in the short-term would cause short-term bond yields to be higher than long-term bond yields when the inflation rate was credibly pegged at nearly 0%.

21. August 2019 at 06:19

Good deflation?

21. August 2019 at 06:29

I think it may also be the case that short term rates were more stable then and long term rates were more volatile.

21. August 2019 at 06:49

Wow amazing to see an inverted yield curve preceded every recession even before WW1!

21. August 2019 at 09:02

Some evidence to back Mathias Georgens speculation. The Funding Act of 1866 authorized contraction of the currency. Then the Public Credit Act of 1869 pledged the government to repay all its debts in coin, settling the concerns about default or repayment in greenbacks. The next year the Treasury was authorized to issue $500 million in 10 year bonds at 5 percent, $300 million in 15 year bonds at 4.5 percent, and $1 billion in 30 year bonds at 4 percent.

These factors could explain the clear demarcation of a period of inversion. It could have then been sustained by the rapid growth in productivity of the late Industrial Revolution.

21. August 2019 at 09:21

The Satan worshiping central banksters and their puppets in DC definitely had an impact.

21. August 2019 at 11:58

https://twitter.com/realDonaldTrump/status/1164231651351617536

He’s right again you know

21. August 2019 at 13:07

The series is not comparing government debt to government debt in the earlier years. This is not a valid yield spread for those earlier years. It is the spread between short term apples and long term oranges — pretty much useless.

21. August 2019 at 13:28

Grumpy commented on this as being a natural state and provided support that it is really hard to get a model to produce an inverted curve.

If price expectations are well anchored then why would you have a positive real yield?

21. August 2019 at 13:29

Typo. Upward sloping curve.

21. August 2019 at 13:36

Matthias and Carl, I don’t see why that would cause an inversion.

Garrett, But I’d expect insurance company demand to be even higher today—assuming insurance is a luxury good.

Ironman, The 1920s are also an interesting period—flat, on average.

Brian, Why would deflation cause the yield curve to invert?

Kevin, I think long term rates were pretty stable. In the 3% to 4% range throughout the period.

Doug, I know that, but you’d get basically the same result using long term railroad bond yields.

21. August 2019 at 16:41

Scott,

I’m surprised I’m the first to mention the Long Depression. That might explain much of it.

21. August 2019 at 18:34

https://mailchi.mp/martingeddes/thestorm-how-to-prepare-for-a-global-corruption-purge

Educate yourselves

22. August 2019 at 03:56

Another reason POTUS brought attention to Greenland:

1 IN 3 CHILDREN ARE VICTIMS OF SEXUAL ABUSE.

https://www.japantimes.co.jp/news/2019/06/26/world/social-issues-world/greenland-seeks-break-silence-around-child-sexual-abuse/

22. August 2019 at 04:03

Leftists can’t manage ANY city or ANY country without rampant crime and evil.

Why is that?

22. August 2019 at 04:25

https://www.foxnews.com/politics/san-francisco-board-adopts-new-language-for-criminals-turning-convicted-felon-into-justice-involved-person

This is what communists do to control the minds of their sheep. They reword and reword until nothing means anything anymore.

Needles and human feces covering the streets wasn’t enough.

S#!thole state ruled by psychopaths

22. August 2019 at 06:53

I love that there’s a commenter here that calls central bankers Satan worshippers. Wrong blog, buddy.

22. August 2019 at 07:06

I haven’t meaningfully studied 19thC US financial history. But I did recently foray into the French Revolution and the late Ancien Regime had a permanently-inverted yield curve, the explanation was default risk. Rentes and other long-term bonds were perceived as untouchable but shorter-term debt was expected to be the first “adjusted” in any restructuring.

22. August 2019 at 07:08

Also, +1 to Doug Bates. I have to bet the 19thC US Commercial Paper market was a little wilder than the modern.

22. August 2019 at 07:53

I assume Brian was referring to expected deflation.

22. August 2019 at 09:33

Randomize:

You being triggered at an uncomfortable truth is only more evidence that I posted it in the RIGHT blog. “Buddy”.

https://i.imgur.com/CYTrlFD.jpg

Ancient Egyptians considered gold “the skin of the gods” — specifically the sun god Ra — and often used it to craft objects of spiritual significance.

Why is this relevant?

Vladimir Putin: “The New World Order Worships Satan”

You think this is a joke little sheep?

22. August 2019 at 09:36

What is a cult?

Epstein island.

What is a temple?

What occurs in a temple?

Worship?

Why is the temple on top of a mountain?

How many levels might exist below?

What is the significance of the colors, design and symbol above the dome?

Why is this relevant?

Who are the puppet masters?

Have the puppet masters traveled to this island?

When? How often? Why?

22. August 2019 at 10:37

Dr. Sumner,

Deflation could explain inversion but only if deflation expectations were greater in the long-term than they are in the short term, right?

With or without deflation, it sure looks like perpetually tight money during that period. Cut rates enough and that inversion should clear up. You’re FAR more knowledgeable of the prewar macro environment than I am; does tight money jive with reality?

22. August 2019 at 12:23

@ssumner

I was just reversing the logic that applies under the Fed monetary regime era where inflation is the norm. I figured that when there was a monetary regime under which the price level was dropping and productivity was increasing (good deflation), such as occurred from the end of the civil war to the first decade of the 20th Century, investors would be comfortable buying longer term bonds with lower nominal yields because of their high real yields.

It’s not a perfect match by any means since the price level started picking up around the turn of the century, https://fred.stlouisfed.org/series/M04051USM324NNBR, but in your graph, the regular inversions continued for another 7 years.

22. August 2019 at 12:42

So is an inverted yield curve actually more “natural” and “normal” than the other way round? Or at least not “unnatural”?

My bet is deflation as well.

22. August 2019 at 13:00

@George

I just want to say that you are really on your game today. Those are all excellent questions. I mean, really, what is a temple? And my favorite question of yours, “why is this relevant?” That one sure has me stumped. .

22. August 2019 at 13:26

Michael, The yield curve was not inverted during the depression of the 1930s.

Indeed yield curves are generally not inverted during recessions.

Randomize, I don’t think money was tight from 1898 to 1913.

22. August 2019 at 14:40

Could it be that the late stage of the industrial revolution coincided with an abundance of capital?

22. August 2019 at 15:31

Scott,

Yes, but just based on my reading, there were periods of deflation throughout most of the period you reference, the first in the US blamed on factors that caused the US to switch from a bimetallic standard to the gold standard, in an era in which gold was relatively scarce.

22. August 2019 at 15:50

tpeach is proof the blog author attracts Marxoid commies like flies on s#!t

22. August 2019 at 15:58

Carl,

I was asking those questions all the way back in Nov 2017 while you had no idea who pedophile Jeffrey Epstein was, nor that rapist Bill Clinton traveled to his pedo island 26 times.

“Let’s hope the Dems win in 2020” is my favorite blog author quote.

22. August 2019 at 20:12

@George

I’m embarrassed to admit that I did not know that Bill Clinton had gone to Pedophile Island 26 times. I keep ending up at boring blogs like this where people are absolutely clueless about pedophilia. Maybe you can share some of your favorite sites for keeping up on Pedophile Island next time you’re sharing your favorite quotes.

22. August 2019 at 23:42

Scott, after reading this interesting blog post, I decided to calculate the yield curve myself – once using Shiller’s data and once using the Jorda, Schularick and Taylor database (they use deposit rates for the hisotric short-term interest rate).

The results are actually quite different!

You can check it out here:

https://macrothoughts.weebly.com/blog/the-us-yield-curve-1870-to-1940

If you write me an email, I can also send you the graphs/data.

23. August 2019 at 01:26

Julius clearly has the best answer to the question.

23. August 2019 at 05:29

Michael, The period from 1898 to 1920 was a period of inflation.

Thanks Julius, That’s quite interesting. As they say, “further research is necessary”.

23. August 2019 at 07:55

Maybe investors feared a possibility of future new T-bill issues would be paid in greenbacks, but US still honored old bond commitments in gold?

Were there more transaction costs with rolling over T-bills? If investors had to go to the bank, redeem a bill, and then reinvest it, there are clear advantages of bonds for long-term investors.

23. August 2019 at 08:03

One theory: its the deflationary version of the Gibson paradox, arising from the workings of the gold standard.See Barsky and Sumners: https://www.researchgate.net/profile/Robert_Barsky/publication/24108581_Gibson%27s_Paradox_and_the_Gold_Standard/links/5567f1e108aeccd777378e91.pdf

23. August 2019 at 08:28

The Deep State – REVEALED

Elite child trafficking – EXPOSED

The Banking Cartel – SPOTLIGHTED

The Hollywood Illusion – SHATTERED

The Media Empire – CRUMBLING

We’re watching the death of The Control Matrix in real time.

And it’s glorious.

23. August 2019 at 08:44

The Gibson ‘Paradox’ was only called such only because most economic theorists at the time predicted that the correlation would be negative.

It makes total sense why slower money growth would depress interest rates.

With slower money growth, the aggregate rate of profit decreases (not necessarily temporally and visually as declining rates from one day to the next, only lower than it otherwise would have been).

By way of incentives and competition, lower rates of profit throughout the economic system in turn then put downward pressure on nominal interest rates, as lenders can’t consistently ask for rates that are more expensive than what borrowers can afford out of their lowered profits.

Costs always fall with a time lag, due to such things as depreciation charges being a function of past expenses. So it never was a ‘paradox’ that a lower rate of increase in aggregate nominal demand (which slower money growth brings about) would be positively correlated with lower interest rates.

Reality doesn’t have any paradoxes. Yet for some reason self-righteous economists love ‘identifying’ them because the truth of their own ignorance and mistakes was too much for them to have to admit. They’d rather call reality a problem instead of their own muddled and often politicized beliefs.

Speaking of Larry Summers, why was his name on the flight logs to the pedophile Jeffrey Epstein’s island of evil? What was he doing there?

Is this why he was obedient to the interests of Obama and had that cushy ‘advisor’ job?

23. August 2019 at 08:54

The Fed was created by international bankers in 1913 to enslave the worlds population via perpetual debt & to control presidents through threats of monetary policy changes. Hard to swallow, unfortunately that’s the real world. They extract wealth from the serfs, everyone here on this blog reading this right now. Same purpose of a parasite.

ROTHSCHILD OWNED & CONTROLLED BANKS:

Afghanistan: Bank of Afghanistan

Albania: Bank of Albania

Algeria: Bank of Algeria

Argentina: Central Bank of Argentina

Armenia: Central Bank of Armenia

Aruba: Central Bank of Aruba

Australia: Reserve Bank of Australia

Austria: Austrian National Bank

Azerbaijan: Central Bank of Azerbaijan Republic

Bahamas: Central Bank of The Bahamas

Bahrain: Central Bank of Bahrain

Bangladesh: Bangladesh Bank

Barbados: Central Bank of Barbados

Belarus: National Bank of the Republic of Belarus

Belgium: National Bank of Belgium

Belize: Central Bank of Belize

Benin: Central Bank of West African States (BCEAO)

Bermuda: Bermuda Monetary Authority

Bhutan: Royal Monetary Authority of Bhutan

Bolivia: Central Bank of Bolivia

Bosnia: Central Bank of Bosnia and Herzegovina

Botswana: Bank of Botswana

Brazil: Central Bank of Brazil

Bulgaria: Bulgarian National Bank

Burkina Faso: Central Bank of West African States (BCEAO)

Burundi: Bank of the Republic of Burundi

Cambodia: National Bank of Cambodia

Came Roon: Bank of Central African States

Canada: Bank of Canada – Banque du Canada

Cayman Islands: Cayman Islands Monetary Authority

Central African Republic: Bank of Central African States

Chad: Bank of Central African States

Chile: Central Bank of Chile

China: The People’s Bank of China

Colombia: Bank of the Republic

Comoros: Central Bank of Comoros

Congo: Bank of Central African States

Costa Rica: Central Bank of Costa Rica

Côte d’Ivoire: Central Bank of West African States (BCEAO)

Croatia: Croatian National Bank

Cuba: Central Bank of Cuba

Cyprus: Central Bank of Cyprus

Czech Republic: Czech National Bank

Denmark: National Bank of Denmark

Dominican Republic: Central Bank of the Dominican Republic

East Caribbean area: Eastern Caribbean Central Bank

Ecuador: Central Bank of Ecuador

Egypt: Central Bank of Egypt

El Salvador: Central Reserve Bank of El Salvador

Equatorial Guinea: Bank of Central African States

Estonia: Bank of Estonia

Ethiopia: National Bank of Ethiopia

European Union: European Central Bank

Fiji: Reserve Bank of Fiji

Finland: Bank of Finland

France: Bank of France

Gabon: Bank of Central African States

The Gambia: Central Bank of The Gambia

Georgia: National Bank of Georgia

Germany: Deutsche Bundesbank

Ghana: Bank of Ghana

Greece: Bank of Greece

Guatemala: Bank of Guatemala

Guinea Bissau: Central Bank of West African States (BCEAO)

Guyana: Bank of Guyana

Haiti: Central Bank of Haiti

Honduras: Central Bank of Honduras

Hong Kong: Hong Kong Monetary Authority

Hungary: Magyar Nemzeti Bank

Iceland: Central Bank of Iceland

India: Reserve Bank of India

Indonesia: Bank Indonesia

Iran: The Central Bank of the Islamic Republic of Iran

Iraq: Central Bank of Iraq

Ireland: Central Bank and Financial Services Authority of Ireland

Israel: Bank of Israel

Italy: Bank of Italy

Jamaica: Bank of Jamaica

Japan: Bank of Japan

Jordan: Central Bank of Jordan

Kazakhstan: National Bank of Kazakhstan

Kenya: Central Bank of Kenya

Korea: Bank of Korea

Kuwait: Central Bank of Kuwait

Kyrgyzstan: National Bank of the Kyrgyz Republic

Latvia: Bank of Latvia

Lebanon: Central Bank of Lebanon

Lesotho: Central Bank of Lesotho

Libya: Central Bank of Libya (Their most recent conquest)

Uruguay: Central Bank of Uruguay

Lithuania: Bank of Lithuania

Luxembourg: Central Bank of Luxembourg

Macao: Monetary Authority of Macao

Macedonia: National Bank of the Republic of Macedonia

Madagascar: Central Bank of Madagascar

Malawi: Reserve Bank of Malawi

Malaysia: Central Bank of Malaysia

Mali: Central Bank of West African States (BCEAO)

Malta: Central Bank of Malta

Mauritius: Bank of Mauritius

Mexico: Bank of Mexico

Moldova: National Bank of Moldova

Mongolia: Bank of Mongolia

Montenegro: Central Bank of Montenegro

Morocco: Bank of Morocco

Mozambique: Bank of Mozambique

Namibia: Bank of Namibia

Nepal: Central Bank of Nepal

Netherlands: Netherlands Bank

Netherlands Antilles: Bank of the Netherlands Antilles

New Zealand: Reserve Bank of New Zealand

Nicaragua: Central Bank of Nicaragua

Niger: Central Bank of West African States (BCEAO)

Nigeria: Central Bank of Nigeria

Norway: Central Bank of Norway

Oman: Central Bank of Oman

Pakistan: State Bank of Pakistan

Papua New Guinea: Bank of Papua New Guinea

Paraguay: Central Bank of Paraguay

Peru: Central Reserve Bank of Peru

Philip Pines: Bangko Sentral ng Pilipinas

Poland: National Bank of Poland

Portugal: Bank of Portugal

Qatar: Qatar Central Bank

Romania: National Bank of Romania

Russia: Central Bank of Russia

Rwanda: National Bank of Rwanda

San Marino: Central Bank of the Republic of San Marino

Samoa: Central Bank of Samoa

Saudi Arabia: Saudi Arabian Monetary Agency

Senegal: Central Bank of West African States (BCEAO)

Serbia: National Bank of Serbia

Seychelles: Central Bank of Seychelles

Sierra Leone: Bank of Sierra Leone

Singapore: Monetary Authority of Singapore

Slovakia: National Bank of Slovakia

Slovenia: Bank of Slovenia

Solomon Islands: Central Bank of Solomon Islands

South Africa: South African Reserve Bank

Spain: Bank of Spain

Sri Lanka: Central Bank of Sri Lanka

Sudan: Bank of Sudan

Surinam: Central Bank of Suriname

Swaziland: The Central Bank of Swaziland

Sweden: Sveriges Riksbank

Switzerland: Swiss National Bank

Tajikistan: National Bank of Tajikistan

Tanzania: Bank of Tanzania

Thailand: Bank of Thailand

Togo: Central Bank of West African States (BCEAO)

Tonga: National Reserve Bank of Tonga

Trinidad and Tobago: Central Bank of Trinidad and Tobago

Tunisia: Central Bank of Tunisia

Turkey: Central Bank of the Republic of Turkey

Uganda: Bank of Uganda

Ukraine: National Bank of Ukraine

United Arab Emirates: Central Bank of United Arab Emirates

United Kingdom: Bank of England

United States: Federal Reserve, Federal Reserve Bank of New York

Vanuatu: Reserve Bank of Vanuatu

Venezuela: Central Bank of Venezuela

Vietnam: The State Bank of Vietnam

Yemen: Central Bank of Yemen

Zambia: Bank of Zambia

Zimbabwe: Reserve Bank of Zimbabwe

The FED and the IRS

FACT: US Federal Reserve is a privately-owned company, sitting on its very own patch of land, immune to the US laws.

23. August 2019 at 08:57

Here comes the ‘conspiracy conspiracy conspiracy’ as the sheep were trained to believe by Operation Mockingbird MSM and Fakewood.

Facts matter!

23. August 2019 at 08:57

Of course Scott I didn’t mean that one can explain thse early yield curves, or anything else, by referring to a paradox itself lacking an explanation. I meant that one explanation for the supposed paradox also might explain the pre-1914 yield curve observations.

I don’t know what those flight logs signify, but I don’t suppose they bear on the merits of Barsky and Summers paper, which of course could be wrong nonetheless. I wonder what you make of that paper. (I know you’ve written on the Gibson Paradox but I don’t know whether you’ve referred to this particular account.

23. August 2019 at 08:58

Hard to swallow.

Important to progress.

Who are the puppet masters?

House of Saud (6+++) – $4 Trillion+

Rothschild (6++) – $2 Trillion+

Soros (6+) – $1 Trillion+

Focus on above (3).

Public wealth disclosures – False.

Many governments of the world feed the ‘Eye’.

Think slush funds (feeder).

Think war (feeder).

Think environmental pacts (feeder).

Triangle has (3) sides.

Eye of Providence.

Follow the bloodlines.

What is the keystone?

Does Satan exist?

Does the ‘thought’ of Satan exist?

Who worships Satan?

What is a cult?

Epstein island.

What is a temple?

What occurs in a temple?

Worship?

Why is the temple on top of a mountain?

How many levels might exist below?

What is the significance of the colors, design and symbol above the dome?

Why is this relevant?

Who are the puppet masters?

Have the puppet masters traveled to this island?

When? How often? Why?

Vladimir Putin: “The New World Order Worships Satan”

23. August 2019 at 13:30

Hi Scott,

One possible explanation that crossed my mind after seeing this would be that gold standard implied deflation over the (very) long term but there was sizeable variability in inflation rates in the short / medium term.

Under gold standard, one can reasonably assume that in 10 yrs purchasing power of one dollar will be more than now. But next year? Or the year after? It may as well be lower than now. Hence investors demanded positive inflation premium on the shorter end whilst demanding lower, negative indeed, inflation premium on the longer end of the yield curve. All due to inflation uncertainty over short/medium term.

Let me know what you think about this.

PS: I’m not sure what rates were used as proxies back in 19th century. I don’t think there were any 3mo bills back then.

23. August 2019 at 17:16

Reading the Barksy/Summers paper, it’s a good model for real interest rates and gold prices, and thus general price level. Yield inversion is not suggested by the model though.

Digging into the source, I believe there is an inherent issue with using New York Commercial Paper rates before the Fed. Before the Fed, CP ran the risk of not merely default but also suspended deposit withdrawals. The post-1920 differentials between CP and Treasury Bills may not reflect the pre-1913 risk of suspended withdrawals.

23. August 2019 at 19:53

Apologies for writing “Scott” when I meant “George” (the other George) in my previous comment.

23. August 2019 at 23:55

@Matthew Waters

That sounds more plausible, bad proxies for the short term risk free rate of interest would explain this perfectly.

24. August 2019 at 00:34

@ George J

You should check out my blog post.

I used two different data sets to plot the US yield curve from 1870 to 1940 and got vastly different results. Shiller seems to use a bad proxy for short-rates. I then use the Jorda, Schularick and Taylor Macrohistory data who take the deposit rate instead, which is probably a better but certainly not perfect proxy.

https://macrothoughts.weebly.com/blog/the-us-yield-curve-1870-to-1940

27. August 2019 at 01:54

Maybe change of international law had effect on future’s expectation?

https://en.wikipedia.org/wiki/Kellogg–Briand_Pact

13. September 2019 at 13:02

John Cochrane had a good post on the subject recently

https://johnhcochrane.blogspot.com/2019/09/more-on-low-long-term-interest-rates.html

13. September 2019 at 13:04

As a follow-up, his explanation is basically the same as Alex S.’s above. Stable long-run inflation expectations meant that the inflation risk premium was higher for the short-run than the long-run.