Why no China crash? Wrong question

Tyler Cowen recently did a post with this title:

Why has it taken so long for a China crash to arrive?

Wrong question! Here are some good questions:

1. Why hasn’t China had a deep slump? (i.e. a depression, or at least Great Recession)

2. Why hasn’t China had a financial crisis?

3. Why hasn’t China had an asset price collapse?

I hope this doesn’t sound too pedantic, but I’m honestly not sure what “crash” means (except when I hit another car.)

The US had a huge stock market crash in 1987, but no economic slump and no financial crisis. The 1980s S&L crisis was a sort of financial crisis, but no deep slump or asset price crash accompanied that fiasco. And of course there have been deep slumps without financial crises or asset price collapses, say in 1921, or 1982. So asset price collapses, financial crises, and deep slumps are three distinct problems.

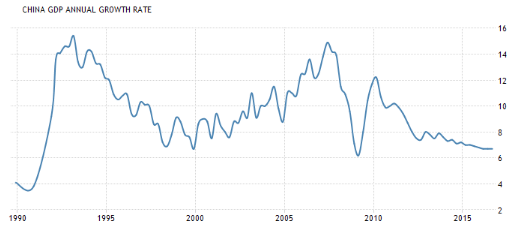

In 2009 we had all three, and I suppose the same could be said for the East Asia crisis of 1997-98, so I’d guess that’s sort of what Tyler had in mind. Nonetheless, I’d like to take them one at a time. Let’s start with deep slumps. Here’s China’s reported RGDP growth rate since 1990:

China has a reputation for having a very smooth RGDP time series, but that’s a bit misleading. One issue is the high average growth rate. Thus when growth slows from 14% to 6% during the Global Financial Crisis, China seems to have dodged a bullet, even though that’s a bigger growth slowdown than occurred in the US. And the second factor is that growth really has been very smooth for the past three or four years, gradually slowing from 8% to 6.7%. That might be partly because big countries are more diversified, so you see more volatility in say Latvia or Iceland than in the US, or perhaps China is smoothing the data for political purposes. But that smoothness is quite recent. (The growth dip in the late 1990s and early 2000s probably reflects the strong dollar, to which the Chinese yuan was pegged at the time.)

China has a reputation for having a very smooth RGDP time series, but that’s a bit misleading. One issue is the high average growth rate. Thus when growth slows from 14% to 6% during the Global Financial Crisis, China seems to have dodged a bullet, even though that’s a bigger growth slowdown than occurred in the US. And the second factor is that growth really has been very smooth for the past three or four years, gradually slowing from 8% to 6.7%. That might be partly because big countries are more diversified, so you see more volatility in say Latvia or Iceland than in the US, or perhaps China is smoothing the data for political purposes. But that smoothness is quite recent. (The growth dip in the late 1990s and early 2000s probably reflects the strong dollar, to which the Chinese yuan was pegged at the time.)

So China already has normal business cycles, just around a higher trend rate of growth. No deep slumps (with the possible exception of the post-Tiananmen slowdown) but that’s partly because deep slumps are pretty rate, especially for countries engaged in rapid catch-up growth. AFAIK, South Korea had only one deep slump in 50 years, for instance. The main cause of deep slumps is tight money that produces dramatically slower NGDP growth, not “malinvestment”.

2. Why no Chinese financial crises? I suppose because the big banks are publicly owned. They were bailed out in the late 1990s, and will probably be bailed out at some point in the future. Rapid NGDP growth also helps.

3. Why no bursting bubbles? Because bubbles do not exist, the EMH is true. Yes, the US housing “bubble” burst, but not the similar “bubbles” in the UK, Canada, Australia and New Zealand. In all those cases prices are at “bubble” levels or even higher. There is simply no reason to expect asset prices to crash.

Now of course asset prices are volatile–recall the Chinese stock market fell in half a few years back. But that’s not something you can predict. If Shenzhen housing prices are up 50% in the past 18 months (or something like that) then there will probably be future periods when housing prices fall in that dynamic city. That’s how an efficient market behaves. Just as housing in New York and San Francisco have had their ups and downs, without there ever being a crash that exposed pre-crash prices as a “bubble”.

If I’d had to guess, I’d estimate that China will have one Korea-1998 type disaster in the next 30 years, but I have no idea when. It will be impossible to predict. That’s because if it could be predicted three years ahead, then the date of the crash would immediately move up by three years!

So don’t hold your breath for a China crash. It will probably happen at some point, but no one will be able to predict it. Nonetheless, you can be sure that Jim Chanos and other China bears will take credit for predicting it, even though they were wrong many times before being right.

P.S. In a 30 year window, I think the second most likely number of 1998-type disasters for China is zero. Two is third most likely.

Tags:

5. November 2016 at 05:23

Sumner: “China has a reputation for having a very smooth RGDP time series, but that’s a bit misleading” – yeah, misleading is the word: look at the GDP growth since 2007 and notice how smooth it looks compared to what was before. It’s fake.

Sumner also repeats his false definition of a crash. If we believe Sumner’s definition, a freak wave that capsizes a ship is not harmful since, long after the wave passes, the sea is calm again. Keynes is rolling in his grave (but Keynes would never read this crummy blog…I wonder why I do).

5. November 2016 at 05:26

Not a rethorical question, the very smooth growth statistic is not a bit suspicious ? Do other large economies show the same lack of volatility ?

5. November 2016 at 07:22

Agreed with all this post, except for

“The main cause of deep slumps is tight money that produces dramatically slower NGDP growth, not “malinvestment”.”

-Would you have said the same thing in 2006, when the worldwide 1974 recession, 1980s Latin American debt crisis, OPEC collapse, African economic crises, post-Soviet collapse, and 1997 crisis would have been fresher in your head?

I mean, we’re talking about China here, not the US.

5. November 2016 at 11:20

Re this: “…but no one will be able to predict it.”

You are 100% right.

But sadly, dozens will “predict” it because they are always predicting it. And they will all (mostly) honestly forget that they’ve predicted 20 of the last 3 bubbles.

5. November 2016 at 12:36

That assumes the knowledge is widely known such that all or most stock prices are affected. Yet that isn’t necessarily the case.

While I agree that future prices cannot be predicted using the tools of the natural sciences, I know that the argument “if it could be predicted then it would happen today” is a flawed argument. One person knowing or predicting future stock indexes, and then acting on it, would have little if any affect on prices.

That something can be known is not synonymous with everyone knowing it.

So “tight money” is not itself a rate of NGDP growth? Sumner you keep changing your definitions. If tight money causes NGDP growth changes, then tight and loose money must be something other than changes in NGDP. So…money supply? Interest rates?

The truth is that the main cause of the business cycle per se is malinvestment caused by socialist money. These twisted and distorted caveats and couched phrases such as “deep” are intentionally misleading in order to divert attention away from that which you support for your own self-serving reasons.

5. November 2016 at 13:44

Ray, Look again, only since 2013. But then you never could read graphs.

Jose, The US has been pretty smooth since 2009. Remember that these are year over year figures.

Harding, Good point. I mean for large diversified economies. Small developing economies are more susceptible to real shocks.

5. November 2016 at 16:50

Excellent blogging.

The role of the People’s Bank of China is foggy. Remember, they can print money and buy bad loans thus unburdening their banking system.

The PBOC is below inflation target so they have plenty of room to do this.

In Western economies, a raft of bad loans tanks the banking system, undercutting the economy. Especially since bank loans are one form of monetary expansion.

China may have “malinvestment.”

Of course, the US “malinvests” $1 trillion annually into “national security” and who knows how much into Kardashian jewellery.

I prefer free markets, but the China system could be better than the present US system.

Interestingly, high house prices is some Sino cities are due to zoning. Sound familiar?

When is the next US recession? Next year? Maybe.

It is very possible the US hits another recession while the China doomsters wait…and wait…waiting