Why are stocks doing well?

This post is not about forecasting the stock market, something I doubt that anyone can do with a high level of consistency. Rather I’d like to consider some possible reasons why stocks have rallied to relatively high levels by historical standards, despite an economy that appears headed for 20% unemployment.

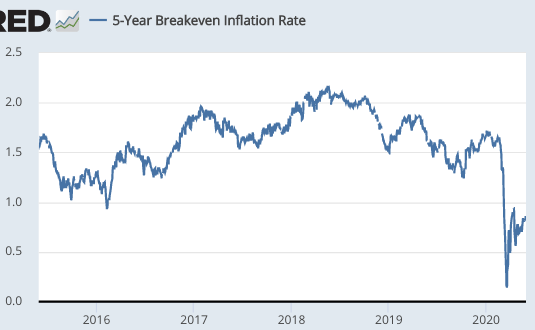

1.Perhaps the economy will recover quickly, as Lars Christensen predicts. I certainly think this is possible, but note that TIPS spreads remain quite depressed:

Overall, I’m a bit skeptical of the claim that the unemployment rate will fall below 6% by November. I hope I’m wrong.

2. Another possibility is that we’ll see a shift of national income from labor to capital. The NASDAQ index is especially strong, reflecting the profitability of (capital intensive) internet companies that benefit from social distancing. But how long with the pandemic last?

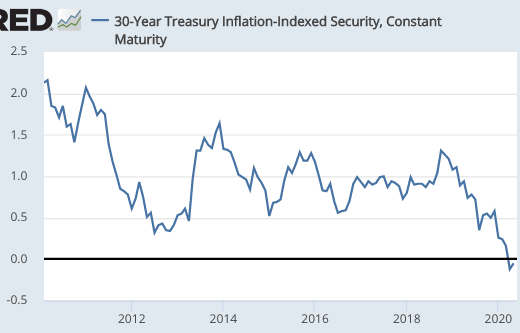

3. Another possibility is that the now almost 40-year downward trend in real interest rates is still underway, with no sign of a reversal. Look at 30-year real interest rates on Treasury debt:

If future cash flows are being discounted at a much lower real interest rate, then you’d expect stocks to be doing better than what one would expect during a period of high unemployment. The counterargument is that real interest rates often fall during slumps.

Bloomberg has a new article on the bull case for stocks:

The Really Big Stock Bull Case Says Fed Stimulus Doesn’t Go Away

You and I know that monetary policy is not currently stimulative, indeed it’s disinflationary. But recall that average people ascertain the stance of monetary policy by looking at interest rates. If the markets are signaling near-zero rates for as far as the eye can see, most people (including Bloomberg reporters) would consider that “easy money”.

Thus Bloomberg is saying that the “bull case” for stocks is due to easy money, which I translate as the bull case is due to a relatively permanent fall in the equilibrium real interest rate.

I’d put at least a little bit of weight on all three of the factors above. But in my view the fall in real interest rates is the biggest factor.

If the S&P500 can reach 3000 at a time of 15% (more likely 20%) unemployment, then it seems increasingly likely that the Robert Shiller model of the stock market is simply wrong. It’s dead as that parrot in the Monty Python sketch.

Was it ever true? Probably not, at least not in the sense of being useful. But hey, he’s got a Nobel Prize and I don’t, so what do I know?

Tags:

30. May 2020 at 11:32

The Fed has signaled that it will do “whatever it takes” for stock prices to rise. Duh.

30. May 2020 at 11:51

Link?

30. May 2020 at 11:53

Scott,

The best explanation I’ve heard for why the stock market seems to be getting back to normal despite the unemployment is that public companies especially large ones with better access to financial markets will be better able to weather the storm than their smaller competition and better handle the transition to work-from-home so they’ll be better positioned in market share after the pandemic than they were before. Also the fed is pumping money and Congress is cutting checks.

30. May 2020 at 11:56

I’m a regular reader of this blog who rarely comments, but a big thanks for your tip about TIPs you wrote at the very bottom. Did not have the bravery to invest in stocks then, but put a lot into TIPs before they jumped around 10% because of what I read on here, and having faith in your view of monetary policy and market monetarism.

Maybe you should take up a second job as an investment advisor?

30. May 2020 at 12:17

In what sense does this disprove the Shiller model of the stock market? Certainly predictions of future dividends are very unstable due to the pandemic.

30. May 2020 at 14:03

Interesting. But how would this theory explain the performance of the Nikkei index in the late 90’s and 2000s as Japanese real interest rates plummeted?

30. May 2020 at 14:48

Maybe stocks aren’t as volatile because leverage at US corps is historically low.

30. May 2020 at 15:17

Phil, I agree that big firms are currently favored, but I wonder for how long.

Ben, Glad to be of service! (I should charge the 30% that hedge funds get.)

Shyam, I meant that Shiller seems to think that there is some sort of normal valuation to which stocks return, whereas I suspect the 21st century will have permanently higher valuations—on average.

sd0000, Good point. I don’t know, other than perhaps weaker cash flow expectations.

Kevin, Yes, but the level of stocks prices also seems quite high, given the economy.

30. May 2020 at 15:28

Kevin please provide a reference for corporate leverage.

30. May 2020 at 15:45

Stocks are 10% down since Feb. 19. (Arithmetic 3044/3386.) The 30 year nominal Treasury is yielding about 50 bp less than it was on Feb. 19. The 10 year nominal Treasury is about 85 bp less than on Feb. 19. I think stocks trade on the nominal yield.

Grumpy Economist says he hasn’t found proof that airplanes are a big virus problem. Some researcher wrote in the WaPo that a study showed it wasn’t a big problem. Some celebrity flew from HK to Bangkok to see kickboxing and then a bunch of people got sick. It was the sports arena were people caught the virus but the airport is considered to be the place to stop the spread. Somebody hugs and shares alcohol with another in a sports arena and the virus travels 20 centimeters and the disease is spread. Earlier the same person traveled 1000 kilometers on a plane without coughing on anybody. It’s ironic.

30. May 2020 at 16:00

I think I agree with this post. But then, in macroeconomics, no one is ever wrong.

Lars C. made a brave forecast.

BTW, PCE core at 1% yoy April. If ever a central bank should overshoot an inflation target….one that is too low anyway….

30. May 2020 at 16:33

Exposure assessment professor on virus on airplanes.

https://www.washingtonpost.com/opinions/2020/05/18/airplanes-dont-make-you-sick-really/

30. May 2020 at 16:57

“permanently higher”?

herodatus wrote:

Go, tell the Spartans, passerby, that here by Spartan law we lie. Go, tell the Spartans stranger passing by, that here, obedient to Spartan law, we dead of Sparta lie.

maybe he meant fisher

30. May 2020 at 18:47

Brian:

https://fred.stlouisfed.org/graph/?g=r74t

30. May 2020 at 19:09

A common explanation given by Austrians is that fed has created a huge amount of new money by buying up stuff and this new money has led to inflation in stock prices (but not other prices that the fed is targeting).

How would you respond to this claim ?

30. May 2020 at 19:51

Kevin – Thanks for the chart. I see lots of articles about record corporate debt. Like everything else, “record” doesn’t always mean much. Everyday I see articles about how “total covid deaths” broke a new record. If I saw a total deaths went down that would be truly apocalyptic.

30. May 2020 at 20:02

Kevin,

I prefer the following ratio for corporate leverage. It’s a composite so I cannot link a graph. It is interest expense divided by revenue.

Take this:

Board of Governors of the Federal Reserve System (US), Nonfinancial Corporate Business; Interest Paid, Flow [BOGZ1FA106130001Q], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/BOGZ1FA106130001Q, May 30, 2020.

Divide by this:

Board of Governors of the Federal Reserve System (US), Nonfinancial Corporate Business; Revenue From Sales of Goods and Services, Excluding Indirect Sales Taxes (FSIs), Flow [BOGZ1FA106030005Q], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/BOGZ1FA106030005Q, May 30, 2020.

It was 11% in 1989 and decreased to 5% in 2013 and continued to be at 5% since then but the most recent datum was 2019.

30. May 2020 at 21:03

You can see what the market is pricing in for future earnings by taking dividend futures and assuming something between a 25-40% payout ratio.

https://www.cmegroup.com/trading/equity-index/us-index/sp-500-annual-dividend-index.html

You just need to take a zero rate curve to gross up those prices a bit to get the actual implied dividends. With those you can do a DCF to get what the expected return is on stocks. The r should be somewhere between 4 and 5%, which you can compare to long corporates around 3.5%

30. May 2020 at 21:15

Kevin, it appears your most recent datum for that leverage graph is also from 2019. So neither your graph nor mine inform about what happened since Feb 19, 2020. However, it is interesting to see these things since as Ken pointed out, there are many articles about high corporate debt. No doubt there has been plenty of borrowing the past 13 weeks but it is good to know interest expense over revenue is starting at 5% going into a recession (and not 11% as in 1989 going into the early 1990’s recession).

30. May 2020 at 21:20

This reminds me about how the media were panicking about China corporate debt in 2015. I was mocked because I said Bloomberg was not reporting any China aggregate corporate debt level worth worrying about at the time.

31. May 2020 at 03:03

Shiller makes a classic ‘ought-is’ mistake. Because equity P/E ratios have ‘historically’ (in his survey) been in a certain range, any prices outside that range are ‘bubbles’ or ‘overvalued.’

Not only have real interest rates been declining for 40 years, but they’ve been declining for 700 years. Current levels are perfectly in line with the ‘long term’ picture. (And it’s difficult to imagine them increasing dramatically short of some catastrophe or serious changes.) Of course this will lead to changing discount rates and ‘appropriate’ prices.

31. May 2020 at 06:30

[…] Original Post […]

31. May 2020 at 07:57

Market, I have no idea what these people are talking about. How did monetary policy cause high stock prices? By magic? Policy does affect stocks, but only because it affects the broader economy. The Fed doesn’t directly buy stocks. Because NGDP growth has been slow, there is no excessive inflation of stock prices via monetary policy.

Garrett, Interesting. What does this say about recent stock prices?

Tacitus, Good point.

31. May 2020 at 14:20

Scott,

A common story might be that central banks around the world create money, buy a lot of bonds, and thereby keep bond interest rates low, which then leads many investors to invest the money in stocks and real estate, which then leads to price increases there.

The value of the S&P 500 has about tripled since 2009, is this true for NGDP as well? Unfortunately I can’t find any good data on this. I could find GDP, which only increased by 25%?! What???

I don’t know the truth, but the current stock prices seem strange to me too. Of course, you can always come up with great explanations using hindsight 20/20. Isn’t it funny that we would do the same thing when the stock prices were completely down? So how rational and sustainable are the explanations really?

31. May 2020 at 18:04

I think it means that the expected return on stocks isn’t much higher than it was in February, but the “spread” on risk-free returns is higher. This is similar to long corporates, where yields are back to where they were pre-crisis but spreads remain elevated

31. May 2020 at 20:35

Scott, Christian, Market Fiscalist,

Isn’t that just that old story that (Internet-) Austrians expect some kind of Cantillon effect that starts in bonds and slowly through the economy with stocks being earlier than eg groceries?

Mostly for that kind of effect to work, market participants have to be idiots who only ever look back, but never act on their expectations of the future.

Long and variable lags as opposite to efficient markets anticipating widely expected events.

1. June 2020 at 07:46

Matthias,

I am not saying that the theory is correct. For one thing, they leave out the part where monetary policy has to act in some way. These people seem to want to print way less money or even no money at all and pretend that this is the normal “zero state”.

But their theory is articulated in a simple, plausible sounding way so that non-experts understand and believe it. It is also very much oriented towards the common-sense feelings of the people. I think that’s why they are relatively successful. It appeals to common sense, even if it is not true.

Or they just know that the money stream will be endless?

Your argument is good argument per se, but not necessarily at the moment. The S&P500 is close to its all-time high, so one can cautiously ask where are all these rosy expectations coming from???

There’s always a lot of talk about “uncertainty”, which is supposed to be so important. Every scenario is supposedly priced into stocks, because the market is so smart. The situation currently reminds me more of mid/end February, when quite a few voices here in the forum asked why the US stock market is not reacting at all.

We are currently experiencing quite some uncertainty because of corona, but also relations with China are unclear, not to mention that there are currently riots on the streets.

I don’t see that this uncertainty and these unclear scenarios are priced in. So why this extreme cofindence in the very best scenario that is possible right now? I can only assume that the market participants are looking mainly at the past and at the statements of the FED, and firmly assume that every NGDP wobbler will be balanced out by monetary policy in the medium run, which means that the S&P index will probably be at 9000 points in about 10 years.

I’ve checked it again: GDP has risen by 50% since 2009, the S&P index has tripled, i.e. 200%.

2. June 2020 at 07:39

And yet, we have done so almost routinely, within a relatively narrow margin of error, every Monday for years. Even in the current environment.

Can confirm it wasn’t ever true. Still, his work has great value in that his stock price data helped contribute to making our accomplishments in the field possible. Even so, there is still a lot we don’t know, which comes up often in the series.

2. June 2020 at 10:16

Christian, You said:

“A common story might be that central banks around the world create money, buy a lot of bonds, and thereby keep bond interest rates low,”

Yeah, that worked so well in 1965-81.

Garrett, That make sense. So the risk in risk spreads roughly offsets the fall in risk free rates.

Ironman, I’m so happy for you.

3. June 2020 at 08:22

ssumner: I appreciate the sarcasm ;-). In truth, it’s an exciting time in that the last three months have provided the biggest test of the theory behind the forecasts since we originated it back in late 2008, early 2009. So far it’s passing, which is something that wasn’t clear would be the case as recently as 30 March 2020, where we’ve also validated a portion of the original theory we proposed, but had never been able to observe until recent months.

3. June 2020 at 13:08

Scott,

their narrative is “convincing” to the extent that today really, according to certain measurements, noticeably more bonds are bought than in the past, or not?

I assume if you measure it in purely nominal terms, but also quantitatively, but perhaps even as a percentage of debt, or not?

What percentage of Japan’s national debt is now held by the Bank of Japan?

And isn’t the ECB already buying corporate bonds and the Fed wants to do the same because they are running out of treasuries to buy?

And this situation was the same in 1965-1981? What kind of corporate bonds did they buy back then? What kind of ETFs? Wasn’t it mostly fiscal policy debt back then? Do you think it would have been the same back then if fiscal policy had been in order?

I also don’t immediately see the mechanism by which bond interest rates are supposed to rise when the central banks buy up huge parts of the market.