When the paradoxical becomes mainstream

Market monetarist ideas often sound quite paradoxical to the uninitiated. Back in 2008 and 2009 it was a struggle to get anyone to even pay attention. How are we doing today? One indication is provided in the cover story of a recent Economist magazine:

The danger is that, having used up their arsenal, governments and central banks will not have the ammunition to fight the next recession. Paradoxically, reducing that risk requires a willingness to keep policy looser for longer today.

. . .

When central banks face their next recession, in other words, they risk having almost no room to boost their economies by cutting interest rates. That would make the next downturn even harder to escape.

The logical answer is to get back to normal as fast as possible. The sooner interest rates rise, the sooner central banks will regain the room to cut rates again when trouble comes along. The faster debts are cut, the easier it will be for governments to borrow to ward off disaster. Logical, but wrong.

Raising rates while wages are flat and inflation is well below the central bankers’ target risks pushing economies back to the brink of deflation and precipitating the very recession they seek to avoid. When central banks have raised rates too early””as the European Central Bank did in 2011″”they have done such harm that they have felt compelled to reverse course. Better to wait until wage growth is entrenched and inflation is at least back to its target level. Inflation that is a little too high is a lot less dangerous for an economy than premature rate rises are.

Here’s the technical explanation. When the Fed tightens monetary policy, the Wicksellian interest rate falls as the market interest rate rises. Why is that important? Because the Fed adopts expansionary monetary policies by reducing its target rate to a level below the Wicksellian equilibrium rate. The lower that rate, the less room central banks have to conduct “conventional” monetary policy (i.e. raising and lowering short term rates.) So if you want the ability to cut rates below the Wicksellian equilibrium rate in the future, the best way of insuring that you can do so is by not raising them today.

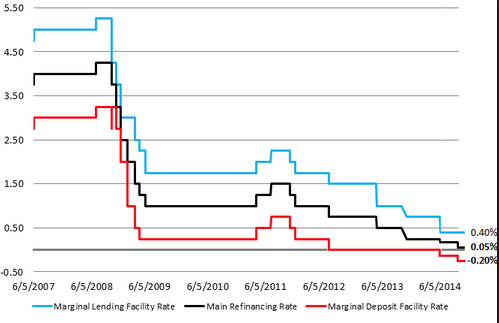

Notice the Economist suggests that the ECB’s tight money policy of 2011 triggered the double-dip recession. This is also progress. A few years ago I recall economists claiming that modern recessions were different. The idea was that earlier recessions were caused by the Fed raising rates to combat inflation, whereas modern recessions were caused by balance sheet issues. This is wrong, as you can see from this graph of ECB target rates:

The ECB raised rates in July 2008, and then twice in the spring of 2011. In 2008 they raised rates because they were worried about high inflation. In 2011 they raised rates because they were worried about high inflation. Of course in both cases they made a mistake, as NGDP growth was weak. But inflation is the ECB’s special obsession. Now for the results. In 2008 the tight money policy caused a mild recession to suddenly become much more severe. This economic downturn sharply reduced the Wicksellian equilibrium rate, so that even later reductions in interest rates were not enough to make the policy expansionary in an absolute sense. And in 2011 the tight money policy also caused a recession, and again later rate cuts were not enough to turn things around. Only when the ECB adopted QE did monetary conditions improve (slightly.)

Before Americans feel too smug about this sorry record, recall that the Fed refused to cuts rates in the meeting after Lehman failed. Their excuse? Worry about high inflation.

I’ll end with a quote from Gandhi:

First they ignore you, then they ridicule you, then they fight you, and then you win.

PS. The rate increases of 2008 and 2011 do not, by themselves, tell us anything about the stance of monetary policy. For that you look to NGDP growth. I simply include them for the “people of the concrete steppes”, who complain that central banks didn’t “do anything” to cause the recent recessions. Yes they did.

PPS. The Great Recession was triggered by a Fed decision in December 2007 to cut rates by 1/4% rather than 1/2%. Frederic Mishkin and Janet Yellen understood what a horrible mistake the Fed was making.

PPPS. Over at Econlog I have a new post comparing fiscal policy during 1937 and 2013.

Tags:

27. June 2015 at 08:23

Excellent blogging.

I have saying the Fed needs to blow the roof off the house, and VSP said “prudence, blah, blah, blah.”

Gadzooks, this Fed tweety-birding around is pathetic and feeble.

Shoot for 7% NGDP growth for seven years, and wake me up after that.

Pile on the QE. Print money until.the plates melt.

When it is boom times in Fat City, then who will whimper about ination?

27. June 2015 at 08:59

Zoinks! Hell’s Bells Margaret! Print and then print more, and then print until we are standing on piles of the sweet sweet cotton and linen! Warp 10 ensign! Logic? Bah! Rationalism? Pshaw! Our children? F em! Golly gee wow! That’s the way uh huh uh huh I like it, KC and the Sunshine band.

—————

That Economist article is neither motivated nor influenced by market monetarism, by the way. Market monetarism is not original. It just says “We can do Keynesianism using the central bank at all times, instead of just some of the time.”

Keynesianism plagues the Economist magazine. Of course you will see passages motivated by a Keynesian worldview, but are something a market monetarist could also have written.

This is not MM becoming more influential, this is Sumner doing the ol’ Pythagorean “We see numbers everwhere!” shuffle.

The entire passage is straight up orthodoxy.

27. June 2015 at 09:05

I’m pretty sure that’s not Gandhi.

Rest of post is good as always.

27. June 2015 at 09:19

> When it is boom times in Fat City, then who will whimper about inflation?

All the boomers I’d imagine because they are not working and will be stuffed.

27. June 2015 at 09:37

“When the Fed tightens monetary policy, the Wicksellian interest rate falls as the market interest rate rises.”

That is incorrect. The Wicksellian interest rate does not move mechanically in only one direction in response to ANY external event(s).

The Wicksellian interest rate is a “natural” interest rate, meaning it is a rate that is independent of monetary policy and all other government activities, as much as this pains socialists to hear.

Summer’s error here is falsely assuming that supply is absolutely unchanging such that if nominal demand AND real supply sold falls, that this is not a fall in supply and demand, but rather a fall only in demand.

This is precisely the false assumption that has led him to advocate for destructive actions from central banks that exacerbate the very problems he claims his advocacy fixes.

The Wicksellian interest rate is a subjective valuation from individuals, a temporal valuation of WHEN they want to consume goods based on the relative quantities of goods through time.

If there is a rise in market preferences for purchasing power through seeking to accumulate cash (which Sumner arbitrarily asserts becomes a “central bank policy” or if large enough a “failure of central banks” at the precise moment when the cash holding leads to an arbitrary decline in spending from 4.5% growth in total spending to 4.499999% growth or less in total spending) there are two other choices that people are making. One is how much less they spend on consumption, and the other is how much less they spend on investment.

What is important to note here is that a rise in cash preference could consist of anything between choosing to only reduce one’s consumption spending at the one extreme, to choosing to reduce one’s investment spending at the other extreme, or, what we should assume if the only event is a rise in cash preference, is an equal reduction in both consumption and investment spending. This is what we should assume because it is the only choices consistent with unchanged time preference. And it is unchanged time preference that cannot be implicitly assumed as having changed when the hypothetical scenario of a rise in cash preference occurs.

With equal reductions in both consumption spending and investment spending, the resulting difference between total aggregate revenues and total aggregate costs, in percent, remains unchanged. This is the foundation of the Wicksellian “natural” rate. It the rate that is associated with true market time preferences.

Therefore, if cash preference in the market rises, which Sumner calls “central banks tightening” if it leads to an arbitrarily sized decline in total spending, then the Wicksellian rate might fall, it might rise, or it might stay the same. It will depend on how much people reduce their consumption spending versus reducing their investment spending.

If history is a guide though, which it isn’t for the subject matter of human action, then the onset of significant rises in cash preference have almost always been associated with a greater reduction in investment spending than reductions in consumption spending. This is in turn associated with a RISE in the Wicksellian “natural” rate, not a fall.

Therefore, what for years Sumner has incorrectly identified as periods of time when the Wicksellian rate fell, were actually periods of time when the Wicksellian rate rose. And as we all know, when the Wicksellian rate rises, this means a central bank policy of lowering nominal rates temporarily through loosening, is a counterproductive, i.e. destructive response.

27. June 2015 at 09:41

Sumner believes in a “Wicksellian interest rate”. But this is metaphysics. Such a rate is unmeasurable, untestable, unscientific. Google: “The Natural Rate of Interest: A Wicksellian Fable” for more info. But metaphysics suits Sumner. Dr. Sumner, I’m still waiting for a econometrics article that proves the Fed moves the economy. … still waiting…

OT: Greece to exit the EU due to the EU ultimatum announced Saturday night. It will be interesting to see how Sumner responds if Greece does not do terribly when it prints its own currency. Conversely, how Sumner will respond if there is disaster. But please note: Sumner will not reply until ex post, not ex ante. He will wait to see which way the wind blows before pulling a metaphysical rabbit out of his bag of tricks. Such a brilliant economist, so typical of his profession.

27. June 2015 at 09:49

“The Great Recession was triggered by a Fed decision in December 2007 to cut rates by 1/4% rather than 1/2%”

No, the Great Recession was triggered by Fed decisions since 2001 and prior to cut rates below the market rates.

That made a recession inevitable, the only difference being sooner through abstaining from continuous acceleration in inflaion, or later through continuous acceleration in inflation.

The sudden widespread rise in cash preferences beginning 2006-2007 was caused by the Fed printing too much money prior, which misled investors by making it impossible for them to know true market relative prices, interest rates and spending, the errors of which will eventually become known and avoided, along with the spending theretofore allocated to it without an instantaneous production of other goods that are sold, I.e. a decline in total spending.

Central banks cause recessions by way of information, not lack of sufficient printing after too much printing.

27. June 2015 at 10:01

“The rate increases of 2008 and 2011 do not, by themselves, tell us anything about the stance of monetary policy. For that you look to NGDP growth.”

NGDP growth by itself also does not tell us anything about the stance of monetary policy. For that we should consider what would have otherwise occurred in the total absence of central banks. That is how we can tell the stance of anything. You consider the counterfactual of that thing not existing in the scenario. Yes, that is very hard for a socialist to do, but that is how we actually know a centralized counterfeiter’s “stance”.

NGDP is an outcome of individual choices, given how much the Fed prints. Just because a psycho can “target” how many yelps his victims elicit, it does not mean that the yelps are a proper stance of the psycho’s actions. And it would be wrong to claim “since we have not yet observed the number of yelps elicited by the people without the psycho being there, it means the standard should not be the number of yelps without the psycho, but rather some number of yelps chosen by the psycho or his crazy court intellectuals.”

NGDP is just as flawed a choice for a “stance” as are prices. Never reason from a spending change.

27. June 2015 at 10:06

E. Harding, I added a link to Gandhi.

27. June 2015 at 10:27

@MF – OT- check out this home page, on debunking Austrian Economics, quite good though the economist is an unrepentant Keynesian: http://socialdemocracy21stcentury.blogspot.com/p/blog-page.html you can email me at raylopez88 at gmail dot com

27. June 2015 at 11:16

Ray,

Sorry, but I don’t visit cesspool websites of the internet.

Insane asylums are my limit.

27. June 2015 at 11:30

An easy way to know that NGDP is not the optimal definition for the “stance” of monetary policy, is to just imagine yourself spending $10 less a week in groceries, which constitutes a change to total spending in the 12th or 15th decimal place.

According to Sumner, ceteris paribus this choice you made would somehow constitute a choice made by Yellen and the rest of the FOMC. You know, like how the devil made you do it. Even though they are not even thinking of either my $10 in spending or even total spending for that matter. Sumner wants us to believe that something the Fed does not even look at or think about, if changed, is somehow the result of a choice made by that same Fed.

Who would have thought? All this time human teleportion is still science fiction because scientists have made the choice not to find a way to teleport humans. Those cruel people! They are responsible for the longest lineups at the airports and bus terminals since the Hoover administration.

27. June 2015 at 11:39

Great post, Scott. Little by little…

27. June 2015 at 18:58

“But inflation is the ECB’s special obsession.”

The ECB put out a game called Economia where you try and hit the 2% inflation target. I was playing it when I was bored and tried to hit 2% following the taylor rule. I averaged 2.01% Inflation with very low variance yet apparently that isn’t good enough for the ECB it needs to be UNDER 2%, yet it can be as low as 1.5%.

A bit silly I know but it is still telling.

28. June 2015 at 06:25

Thanks Brian.

Jesse, The Fed has a similar game.

28. June 2015 at 20:06

Great post. I thought that the Wicksellian rate was determined by a number of economic factors that are outside of the control of monetary policy. Then the central bank sets their policy to meet what they believe the real rate is (even if it is negative).

But by triggering a the recession with by being to tight in 2008 did the Fed significantly lower that rate? I understand the logic, but I am unsure on how much of an impact a central bank could have on the Wicksellian rate.

29. June 2015 at 06:28

One S. Sumner keeps overlooking that not only the FED / ECB / BoJ have a “monetary policy” but corporations & households as well.

It was a change in “Monetary Policy” of the (american/european) corporate sector that broke the back of rising interest rates in the very early 1980s. And it was NOT the FED. The FED follows the market. Mr. Market drove short term rates down to almost zero and NOT the FED.

Milton Friedman accused the FED of being too tight in the early 1930s. But the FED bought (like it did after 2009) tonnes of bonds out of the market. But that failed to stop the slide into the depression of the 1930s. The main reason was that long term rates went through the roof.

It was Mr. Market that pushed up rates from 1% in 2004 to 5.25% in 2006. And the FED was FORCED to follow. And yes, those rising short term rates pushed the US housing into the abyss.

Rising US (long term) rates WILL put the kibash on the ability for central banks & governments to “fight” the next leg of the financial crisis. Just see what happens in Greece !

29. June 2015 at 11:37

@ ssumner

Nope. Jewish guy at an American labor union convention:

http://www.csmonitor.com/USA/Politics/2011/0603/Political-misquotes-The-10-most-famous-things-never-actually-said/First-they-ignore-you.-Then-they-laugh-at-you.-Then-they-attack-you.-Then-you-win.-Mohandas-Gandhi

29. June 2015 at 12:34

Ryan, The claim is that the real rate is not affected by monetary policy. Even that claim is wrong, but everyone agrees the nominal rate is affected.

Bubble, I agree that the Fed usually follows the market on interest rates, such as in the 1980s. But there are times it does not.

E. Harding, But I found the cite on the internet, so how can it not be true?