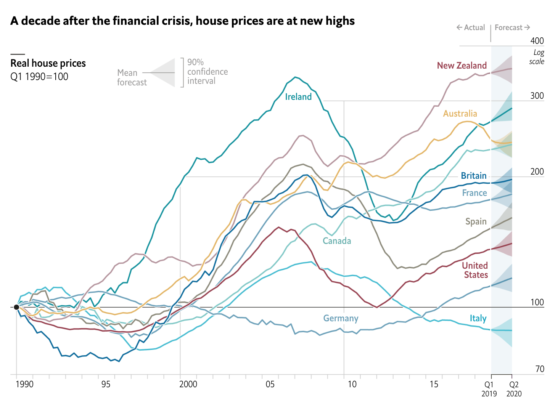

What would real house prices look like in a world without bubbles?

This:

A series of random, unpredictable ups and downs.

A series of random, unpredictable ups and downs.

The Great Recession was not caused by a the bursting of a housing bubble, because there was no bubble. It was caused by tight money.

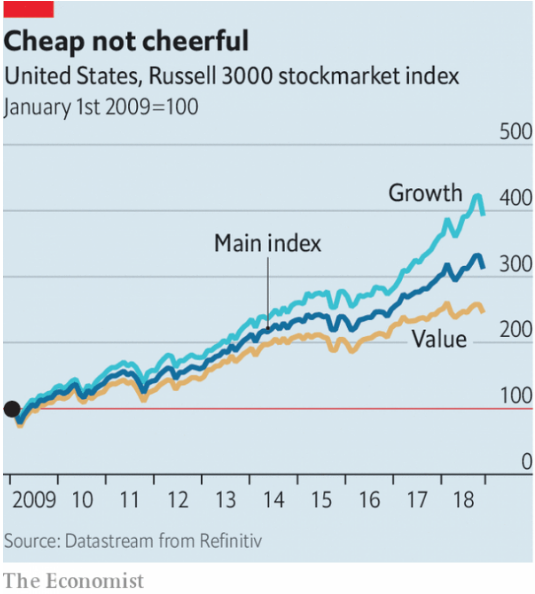

When I started blogging in early 2009, I was told that the EMH was wrong because value stocks outperformed growth stocks. But anti-EMH theories are not useful to me, because as soon as I hear one it stops working.

PS. We’ve added the Hypermind NGDP forecast in the right margin of this blog. The current reading for the 2020 market is 3.05. That means market participants expect NGDP to grow at 3.05% between the first quarter of 2020 and the first quarter of 2021.

Tags:

26. December 2019 at 23:29

Scott, I’d be interested to know what you think of the successes of Jim Simons:

https://www.forbes.com/sites/forbesdigitalcovers/2019/11/08/jim-simons-the-man-who-solved-the-market-gregory-zuckerman-book-excerpt/#251ae33c13b6

When someone refuses to take money from new investors because it will dilute his profits, he’s either very dumb or very smart.

26. December 2019 at 23:52

Unaffordable housing is the macroeconomic story of our time.

It is interesting that housing prices have risen so sharply in the same nations that run chronic current-account trade deficits. Some studies indicate that foreign capital inflows jack up property prices.

Kevin Erdmann contends that house prices follow house rents, so the house price explosion is really a result of property zoning and other restrictions on supply. In other words, we continue to see urbanizing job markets, especially in winning cities, but not urban housing supply.

Tyler Cowen and others have suggested that people are migrating to hip cities more or less because they want to. There may be an element of that, but I think more importantly people migrate to where the jobs are, and have for centuries.

If Milwaukee were to generate 100,000 new jobs annually for the next 10 years I suggest we would see 100,000 new residents in Milwaukee for the next 10 years and that Milwaukee would also become considered a hip city not all that different from Toronto.

If Milwaukee where to put a noose on new housing Supply, while 100,000 new jobs were generated annually, we would see exploding house prices in Milwaukee and duded-up in-town housing and expensive bars and all the rest.

As an issue in the real world, Trump’s trade tariffs are but a molehill next to the mountain that is expensive housing.

27. December 2019 at 07:48

udoh, Good for him. But his story has no implications for me.

27. December 2019 at 09:05

Excellent. I see a lot lately about NGDP targeting, but it’s hard for me to know if that’s just the result of a “bubble” of my own making.

Does Jerome understand that markets expect 3.05% NGDP growth this year? If so, is he cool with that? If only there were something he could do…

27. December 2019 at 09:17

The best asset pricing theory I’ve read is that people optimize on relative wealth as opposed to absolute wealth (as assumed in CAPM), which implies that high risk assets do not have higher expected returns than low risk assets. Relative wealth also fits better with your recent posts on progress.

In practice the risk-return relationship is weakly positive, flat, or negative depending on what assets you’re looking at. Minimum volatility ETFs have kept up with or outperformed cap weighted ETFs. See USMV/EFAV/EEMV versus IVV/EFA/EEM.

27. December 2019 at 10:07

Ben, Ireland has one of the biggest current account surpluses in the world relative to GDP and Spain is also a surplus country. Sure, desperately poor people will move for jobs, but in an affluent society like the US today, most people choose where they want to live and the jobs follow the people. In the Rust Belt, most major peaked in population in the 1950 census (a few in the 1960 census), yet deindustrialization did not occur en masse until the 1970s and 1980s. People moved to the suburbs and Sunbelt not because jobs were there (the South was practically a developing country in the 1950s when large-scale migration to the South began) but because they preferred the weather (summers made tolerable by the invention air conditioning) and amenities, and the jobs followed the people years later.

27. December 2019 at 10:23

@Brian and ssumner:

3.05% seems pretty low. I wonder if there’s an ‘anti-Fed’ bias in the market participants, as they will likely be fairly ‘Sumnerian’ in their attitudes and priors, and believe the Fed is being too tight.

If I was participating I would think it would be closer to 4%. But I’m far from an expert on this stuff.

27. December 2019 at 10:46

Mark, Pittsburgh and Detroit are at their respective locations because of coal and iron ore and shipping. America’s economy has been an energy intensive economy for decades and the only way one can understand the 2001-2008 economy is by understanding that we were undergoing an energy crisis. So the Housing Bubble was a symptom of an underlying energy crisis because Fortune 500 CEOs saw a dearth of investment opportunity due to high energy prices with no good solution on the horizon. High energy prices also created profits and in modern fiat currency economies capital searches for yield. So the capital from those high energy profits not reinvested in energy production is what produced the dysfunctional economy.

We know the 2001-2007 economy was dysfunctional even prior to the Financial Meltdown because every major economic indicator was below average except corporate profits. So corporations were profitable but they didn’t really believe the economy was truly strong. The reason we know the global oil market was a major culprit for the dysfunction of the American economy was because during the commodity supercycle every major commodity increased in price AND supply…except oil (and American natural gas). So any theory developed to explain the 2000-2008 macroeconomic situation must explain why oil production plateaued and why that was either a big deal or no big deal. I think it is obvious it was a big deal with respect to the larger economy.

27. December 2019 at 11:31

Ben Cole, the fact home ownership rate is significantly lower than last decade while housing prices have increased highlights your argument that landlords are reaping the benefits.

So why is this an important contrast from last decade?? Because the 2001-2007 economy was dysfunctional and the smart money was skeptical of investing money into that economy…but capital still searches for yield even if the most qualified investors pass on the credit because they don’t have faith in the economy. Once again, the primary reason for the dysfunctional economy was an energy crisis with no good solution on the horizon. Nuclear power has long lead times and coal produces unacceptable amounts of pollution for Americans and the oligopoly of Big Oil was paralyzed by lazy groupthink and early in the decade the prospect of a stable Iraq stifled investment in oil production overseas.

27. December 2019 at 12:51

There should be a component to this analysis which incorporates population growth generally, rather than urbal-suburbal migration. If we are just at replacement rate, eventually there will be too many houses right? Or there cost will decline relative to renting.

From the census bureau there is this:

“More than half of U.S. counties have experienced net population loss since 2010, with more than 550 counties losing at least 5 percent of their residents, which could result in fewer federal dollars to support local infrastructure and public programs.”

This is either loss due to old age and death, or population concentration. I guarantee houses in those counties are cheap and affordable. there are just no jobs there.

27. December 2019 at 13:14

Derrick, a program I would like to see is a “homeownership opportunity zone”. So you have a contest with cities competing to offer homes and jobs to Americans and the federal government buys Rust Belt homes for $10k and pays property taxes for 3 years and at the end the person living in the home gets to be a homeowner. So it would be like the Amazon HQ2 contest except cities would have to line up jobs and acquire homes on the cheap that are in relatively good shape so Americans can become homeowners with good jobs with benefits. So Fortune 500 companies are always looking to cut costs and one way is to move jobs to cities with lower cost of living…but often those cities aren’t desirable. So this program would solve that problem by providing free homes and a critical mass to change the prospects of the city.

28. December 2019 at 03:54

Gene, here is Cowen’s link to the NIMBY Index: https://marginalrevolution.com/marginalrevolution/2019/12/there-is-now-a-nimby-index.html

Reliance on rising asset prices for prosperity is a thing, a not very good thing in my view, but one won’t find any sympathy for that view here.

28. December 2019 at 07:07

Garrett, Interesting hypothesis.

Rayward, I agree that it is not a good thing.

28. December 2019 at 09:57

rayward, the way I see it is high housing costs are the product of young Americans delaying having children and moving to hip cities. However many companies would prefer to cut costs and a way to do that is creating jobs in cities with a lower cost of living. So I witnessed the perfect scene that explains this a few months ago while watching my young son playing on a playground. A group of young adult men and women playing kickball in a field right next to a craft brewery (1 of 5 in the area along with just as many CrossFit gyms) that after finishing the game went to the brewery which was having fantasy football drafts and if they drank too much they could get an Uber (I bet half the cars I see are rideshare driven by older women and men). Also in the once gritty area are new hip offices in former warehouses.

28. December 2019 at 13:14

@rayward and ssumner:

You guys have the causation arrow going the wrong way. Rising asset prices are a result of prosperity not a cause of it. This is almost tautological.

28. December 2019 at 16:37

3.05% NGDP growth seems low, but multiple voting members of the Fed seem to believe that the Fed should be raising rates. So it seems likely that the Fed will respond to economic headwinds with inaction.

28. December 2019 at 17:05

Mark–

I think people have always migrated to the jobs, or in an earlier era found they could not make a living on a small farm anymore and migrated to cities.

Sure, if you happen to be a knockout female you can move to the West Coast and things will take care of themselves. But for the 90% of the population that are grunts, we go where the jobs are.

In an earlier era, I don’t suppose many people migrated to Detroit or Pittsburgh for the weather.

Be careful regarding statistics and Ireland. Due to certain accounting mechanisms, companies such as Apple claim to make huge percentages of their revenue in Ireland.

Gene— as Adam Smith said, rarely do people in business congregate except that they hatch a plot against consumers. If there is government power to zone property, then you can be rest assured that property owners and financiers will gain control over that power.

In general, given such power, property owners and financiers will extract all income gains out of the renting class, while small property owners (homebuyers) will pay dearly for the privilege of buying.

But, as I always say, there are no atheists in foxholes and there are no Libertarians when neighborhood property zoning is under review.

29. December 2019 at 02:34

Scott, just to follow up regarding Jim Simons. I thought it has to do with you because he has consistently beaten the market over a few decades. Thus the market is not completely efficient, or at least it wasn’t completely efficient before he entered it. So markets are efficient except when they’re not.

29. December 2019 at 07:38

msgkings, I never said that rising asset prices are a cause of prosperity.

uhoh, The fact that he’s done well does not show that markets are inefficient anymore than the fact that someone won a lottery (at a billion to one)shows that lotteries are rigged.

29. December 2019 at 18:46

@ssumner: I thought that’s what you meant when you agreed with rayward saying that.

30. December 2019 at 09:53

It is exasperating when individuals look at short term results (for example–“Value vs Growth”) and conclude that EMH is “wrong”. The standard error alone guarantees certain categories will always outperform other categories by randomness even over 20 year time periods—the problem is knowing which one will. Studies on Mutual Funds beating indexes are unequivocal on this.

RE: James Simons and the Medallion Fund. That fund is the ultimate outlier. They clearly have outperformed markets by a multiple of 10-20 or more on a risk-adjusted basis—this is not a random one in a billion situation—it is by design.

However, so do trading desks at every major investment bank. They are profitable 95% of the days, better than Medallion. Why? They know who is buying and selling at what price because investors tell them. But they have no idea what returns will be in 1 week or even one day. In the end, it is highly likely Medallion does something similar by other means—impressive but it has nothing to do with EMH—it has to do with information capturing.

30. December 2019 at 09:54

I mean Mutual Funds NOT outperforming indexes

30. December 2019 at 10:13

I am glad you are posting NGDP forecasts—-this needs to be in the public consciousness to a greater degree. Interesting it is around only 3%—but not the slightest bit shocking either.

30. December 2019 at 18:01

Best headlines 2019:

More than 1000 Economists Invoke Great Depression in Warning to Trump on Trade

Bloomberg

MAY 02, 2018

—30—

Meanwhile, at yeared….

Dec. 28

S&P 500 Set to Record Highest Return Since 1997

The impressive turnaround by Wall Street in 2019, after the market mayhem of 2018, is set to reach a milestone at the end of this year….the S&P 500 Index is set to return the highest since 1997. The benchmark index is recording fresh highs almost regularly in December.

On Dec 27, the S&P 500 Index achieved a new record high after closing at 3,240.02. Year to date, the broad-market index has rallied almost 29.3%. It is currently at a striking distance to surpass its annual return of 29.6% posted in 2013. Notably, so far, 2013 marked the best annual return for the S&P 500 Index since 1997, when it jumped a little more than 31%.

—30—

31. December 2019 at 07:48

msgkings, I said that I agree that it is not a good idea to try to inflate asset prices in order to create prosperity.

31. December 2019 at 08:31

@ssumner: OK thanks for clarifying. rayward has been posting the same (incorrect) thing for years and I was concerned you agreed with him.

1. January 2020 at 08:00

I love this post for a reason that has nothing to do with housing prices: just the reminder that if you’re trying to prove an effect, the right comparator is not nothing happening, it’s lots of random noise.

1. January 2020 at 16:15

I like the relative wealth story. It conforms to Adam Smith’s claim that reputation was the greatest driver of human motivation. Not to mention a lot of comparative anthropology, evolutionary biology, etc.

This book sets out the relative wealth thesis.

http://www.amazon.com/Missing-Risk-Premium-Eric-Falkenstein/dp/1470110970/ref=sr_1_1?s=books&ie=UTF8&qid=1345223074&sr=1-1

After all, when dealing with various levels of uncertainty, benchmarking to other people uses available information and minimises your status risk.

Also, agree with you on bubbles and house prices, but that is now news.

2. January 2020 at 06:06

– “There was no housing bubble” ?? Yeah, sure. And I was born yesterday, right ?

– There certainly was a housing bubble in the e.g. US, Australia and New Zealand.

– “Unpredictable” ?? Far from, there was one person who predicted the peaking of the US housing bubble BEFORE it happened. This person is called Harry S. Dent.

2. January 2020 at 06:13

– Did one Scott Sumner never look at real estate prices in South Korea in the last say 20 years ? (Hint: housing bubble). The people who read the work of Harry Dent know that demographics played a very important role and that the real estate bubble in South Korea was VERY predictable.

2. January 2020 at 14:49

– I just remembered some charts I have seen on the topic “Housing bubble”:

– From – at least – the late 1960s up to the year 1999/2000 Real Median Household Income – on average – rose steadily, supporting the housing boom in the 2nd half of the 1990s. That was a genuine healthy boom.

– But between the year 2000 and 2008 Real Median Household income remained flat. But US real estate prices kept rising and mortgage credit/debt kept rising. That divergence between Household income and Mortgage debt/credit shows that there was a genuine housing bubble. Because mortgage payments for interest and principal have to come out of the household’s income. Households can’t “print money” like banks can.

– No, falling real estate prices weren’t caused by “tight money/credit”. Because in 2005, 2006 & 2007 the total amount of mortgage credit/debt kept rising at the same blistering rate as between the year 1999 and 2005. So, it wasn’t “tight money” that caused real estate prices to go down.

– The reason real estate prices fell after 2004 was that real estate prices simply became too high, became un-affordable for a(n) (average) household. Keep in mind (as stated above) REAL median Household income remained flat between 1999 and 2008. REAL median Household income actually FELL between 1999/2000 and 2006 and recovered again between 2005 and 2008.

– There was more than one reason why real estate became unaffordable: 1) rising short term rates (think: subprime mortages) 2) rising oil prices 3) falling USD (against e.g. the EUR and CAD) hollowing out the purchasing power of an average wage.

2. January 2020 at 21:34

“Betting against beta” (http://pages.stern.nyu.edu/~lpederse/papers/BettingAgainstBeta.pdf) might be one of those anomalies that survives being published: it’s been well known for a long time, but the conditions keeping it in place remain.

3. January 2020 at 01:45

Scott, thank you. But I propose this as a better gambling analogy: the same guy wins roulette every time he plays. Yes, he could have had a very very unlikely string of good luck. But if he keeps winning, and even after you decide to start monitoring his performance, you kind of have to wonder if something else is going on, whether there are more things in heaven and earth than are dreamt of in your philosophy.

As a test question in this direction, would you be willing to bet on even odds that the Renaissance Medallion fund performs worse than an S&P 500 index fund over any 5-year period of your choosing?

3. January 2020 at 01:49

Michael Rulle, why does the success of the Medallion Fund not disprove the EMH? My (amateurish) understanding of the EMH is that, on average, you can’t beat the market without inside information. Are you saying they are exploiting insider information?

4. January 2020 at 22:52

Willy2, Heh, when is that Aussie recession that you keep promising going to happen?

uhoh, You said:

“why does the success of the Medallion Fund not disprove the EMH?”

Luck?

I bet on the EMH by buying index funds. So far I’m winning.

5. January 2020 at 07:30

House prices that are underpinned by mortgages that borrowers clearly would not be able to repay does strike me as a bubble. I still cannot agree that bubbles don’t exist when credit is given out on a basis of assuming that current trends will not ever change. Saying that bubbles don’t exist is like saying that Ponzi schemes don’t exist. There can be bubbles that are underpinned by a bit of fraud.

5. January 2020 at 14:39

Scott, you said “I bet on the EMH by buying index funds. So far I’m winning.”

Yeah, that’s what I do too. But only because I can’t invest in the Medallion fund anymore. Definitely you and I and the market will beat anyone but a very small group of high-frequency traders which exploit very very small correlations of like 0.01% and huge volumes, and who hire nothing but math and physics PhDs.

Back in the 90s, I had a friend who got a job with them and who therefore was allowed to invest in their fund. (The fact that they won’t take money from anyone but their own employees should tell you something right there.) He asked me if I wanted him to put in some money for me. Being well acquainted with the EMH, I said no. My friend told me stories of his boss insisting that the part of the fund my friend controlled must not be correlated with the market performance. And this is while the market was going through the roof! The next time my friend offered to put some of my money in, I jumped at the chance, and enjoyed 25% a year until my friend bought me out.

Look, I agree that if you have 2^30 people flip 30 coins, it won’t be surprising if 1 of them gets all heads. That might be the situation from your point of view because you didn’t start paying attention to their track record until it was already in the past. But I’ve been watching them for 25 years. So what I’ve seen is a given guy, i.e. in an experiment with N=1, who says “The next 30 coins I flip will come up heads” and then delivers on that. Now you say that he just got lucky, probably thinking I only bring up the one guy in 2^30 who happened to have that lucky streak. But I say no, and that I’m confident enough to ask if you’d be willing to put some money on that. But then you decline to make what should be some easy money from your point of view, on the grounds that the guy couldn’t possibly beat the laws of probability. It seems to me that your revealed preferences constitute an admission of defeat.

15. January 2020 at 09:06

How was it not a housing bubble? Please answer this: How much should housing rise relative to income?

24. January 2020 at 13:11

– O yes, the australian recession is already here for – at least – 2 years but then one has to STOP looking at the GDP ONLY.

– Australia is already in a recession but then you have to ignore the bogus and highly politisized GDP calculations. Use the formula provided by Steve Keen (income + change in debt = aggregate demand). Does the name Steve Keen still ring a bell ??

– Australia didn’t have a recession in the year 2000/2001, not in 2008 & 2009 and not right now when/if one looks at GDP. But when one looks at the “GDP per capita” then Australia is right now in it 3rd recession since the early 1990s.

– Australia is on its way to outright (credit) DEFLATION (= total amount of outstanding credit is contracting). And that would be the 1st time since the early 1930s.

– Another sign Australia is in a recession is that the imports are shrinking (= recession). Australia imports are down as a result of falling car sales. Australia no longer has a car manufacturer since say 2015.

– Foreclosures in Australia are up more than 600% (= sixfold). And that number is already more than 12 months old.

– I have another shocking statement: The US is also already in a recession.

25. January 2020 at 03:59

– Correction: Australia is already in a recession since the 1st quarter of 2016. But then one should not look at the GDP but use Steve Keen’s famous formula (income + change in debt = aggregate demand) instead.

– And now Australia is getting closer and closer to outright DEFLATION (=contraction of credit/debt).

– We saw something similar with the US. Steve Keen shows that the US entered a recession in the first quarter of 2005 (and never came out of it before the last quarter of 2009) whereas the NBER declared the recession had begun in november/december 2007.