What the strong euro is telling us

It’s become a cliché that the Japanese yen is a “safe haven currency”, which does well when things are going poorly in the global economy. I’ve never really understood that claim. What makes Japan a safe haven? And why does the yen do well even when Japan itself is the epicenter of the problem, as with the 2011 tsunami? People have offered explanations, but they seem quite weak, very ad hoc.

In the past, I’ve offered an alternative theory, that Japan’s yen appreciated during times of trouble because Japan was at the zero bound. Because the BOJ could not cut rates further, a fall in global interest rates tends to raise Japan’s policy rate relative to the equilibrium interest rate. This makes Japanese monetary policy tighter. In contrast, the Fed tends to cut interest rates when the equilibrium interest rate falls (albeit with a lag.) My theory also explains why the rise in interest rates after Trump’s election had the effect of helping Japan, making their monetary policy a bit looser.

How would we test my theory? Suppose another big economy also hit the zero bound, an economy that could not possibly be regarded as a safe haven. Also assume that the currency in that economy appreciated strongly during a global crisis, even though the epicenter of the crisis was in that very economy.

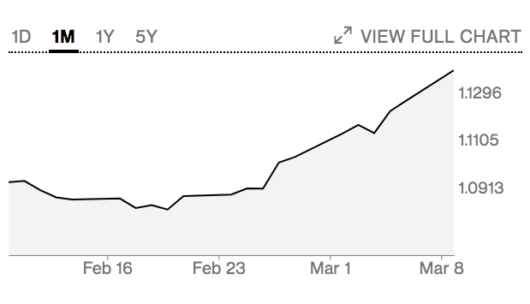

Of course, I’m talking about the eurozone, which is currently at the center of the global coronavirus problem. The euro is appreciating strongly:

PS. My previous post may have created the impression that I thought monetary policy in the US was currently appropriate. Just the opposite is true; policy is far too contractionary. Right now, I don’t think it’s useful to give monetary policy advice in terms of interest rates, as the equilibrium interest rate is so unstable. So here’s what I’d recommend:

1. The Fed should ask Congress for the ability to buy a wide range of assets during an emergency.

2. The Fed should eliminate IOR and buy enough assets to push 12-month inflation/NGDP growth expectations up to the policy target.

NO MATTER HOW MUCH IT TAKES.

But then that’s always been my view.

PPS. File this under “Karma’s a bitch“.

Tags:

9. March 2020 at 13:52

Sumner: “It’s become a cliché that the Japanese yen is a “safe haven currency”, which does well when things are going poorly in the global economy. I’ve never really understood that claim. What makes Japan a safe haven”.

OMG. See: https://www.quora.com/Why-is-the-Japanese-yen-considered-a-safe-haven-to-invest

It’s the carry trade professor. Got nothing to do with anything you posted. What else does the professor not know? Scary.

9. March 2020 at 14:02

its because the yen has been for so long the largest “carry” currency (due to extremely low rates for longer than any other big currency0; sell yen to buy higher yielding assets in another currency, mostly dollars. when those “crash” and the “carry” is now negative, they swap back into yen, thus the rise. its the haven bc the carry punter avoids (or tries to) the evaporation of the reason for the carry: higher yields or higher prices; in a sense the crash in prices, just as in a bond is conversion to a higher discount. so they try to get back to the zero of yen.

9. March 2020 at 14:04

same thing applies to the euro now that its a neg yield bond environment. of course the j curve effect will ultimately hurt the yen and euro ceteris paribus.

9. March 2020 at 14:12

Why am I being moderated? Who’s afraid of Ray Lopez?

9. March 2020 at 14:14

Well, I see since I was first to reply perhaps I was blocked by mistake. My substantive response was that JP Yen is considered a ‘safe haven’ due to the carry trade, see: https://www.quora.com/Why-is-the-Japanese-yen-considered-a-safe-haven-to-invest

Whether or not this contradicts Dr. Sumner’s narrative I’ll leave to the reader.

9. March 2020 at 14:35

But the yen is appreciating against every other major currency, including the euro, despite short rates being lower in the Euro-zone. And what about the Swiss franc?

9. March 2020 at 14:57

Saw a chart that in the long-term currency prices are almost entirely differences of inflation rates. Euro crashes from much higher levels a few years ago and has lower inflation that the US. Could it just be the law of one price kicking in?

9. March 2020 at 15:11

i think the fed stance of being absurdly contractionary right now can be explained very simply:

spending (globally and domestically) is collapsing due to coronavirus. The Fed is currently paying significantly above market (1.10%) for banks to hoard reserves. any IOR above market rates is indefensible, unless the goal is to further slow down spending.

it’s that simple

9. March 2020 at 15:17

yersinia and Ray, If you have something to say about my post, then say it. But just repeating arguments about “carry trades” is not very helpful.

9. March 2020 at 16:29

I agree with this post, and the need for the Fed To be more expansionary.

However, in the current situation perhaps the advice of a Stanley Fischer is correct, and that the tool of helicopter drops needs to be added to the Federal Reserve arsenal.

Some people have characterized conventional quantitative-easing as a “helicopter drop on Wall Street,” when what we need is a helicopter drop on Main Street.

No one is ever wrong in macroeconomics debates, but I think Stanley Fischer is right.

I would like to see a discussion of whether helicopter drops on Main Street will ultimately be too inflationary, vs. helicopter drops on Wall Street.

As for stimulating aggregate demand within the United States, how is conventional quantitative-easing, which is a helicopter drop onto globalized capital markets, effective? I understand the “Hot Potato” effect. Yes, Global asset values might be preserved or even enhanced through conventional quantitative easing.

Of course, it is not an either-or argument, that we must do a helicopter drop on Wall Street or a helicopter drop on Main Street. Perhaps we should do both.

9. March 2020 at 16:51

MrBroegger, Last time I looked Switzerland had some of the lowest interest rates in the entire world. But I’ll say this, it’s much more likely that Switzerland is an actual “safe haven” than is the case for Japan or the eurozone.

Sean, Why now?

9. March 2020 at 16:59

I am banned from commenting on Econlog, so I will comment here on Scott Sumner’s post there that federal fiscal policy is too clunky and slow to be much use now.

From Macromom:

“Get money to people now would be a front line financially. The easiest way is to cut federal tax withholding for the next two months. In 1992, George H. W. Bush issued an executive order, employers used the new withholding tables, and within weeks people got a bump in their paychecks. It worked, people spent the money.”

So evidently in the vast toolkit of President Trump is the ability to issue an executive order to reduce withholding rates on paychecks. This seems like a great idea with the proviso that the tax cuts be considered permanent, in the sense that there will be no attempt to recoup lost income.

I prefer a holiday on Social Security payroll taxes, offset by the Federal Reserve buying bonds and placing them into the Social Security trust fund. However, the legal authority for such an action may not exist.

9. March 2020 at 17:04

Sumner: “yersinia and Ray, If you have something to say about my post, then say it. But just repeating arguments about “carry trades” is not very helpful.” – well, just to beat a dead horse, the link I cited offers various rationales of why Yen are safe haven, such as the Japanese themselves turning to Yen during crisis for I suppose “home bias” reasons, and the carry trade (interest rate differentials) make people borrow in one currency to buy paper in another, which works to make a small profit until it doesn’t. It might be an alternate way of saying what Dr. Sumner is saying in this post, I dunno.

PS–why did France before WWII, while on the gold standard, have a big influx of gold after 1931-1936? Because as B. Eichengreen can tell you, England went off gold in 1931. And why did France have (I think) an outflow of gold after 1936? Because the country was not deemed a safe haven due to war clouds pre-WWII (but the USA was, despite not being on the gold standard after June 1933). You could frame the above as ‘loosening’ and ‘tightening’ in the UK/FR/USA but my simple mind just likes to report the facts as they happened. Note Argentina income/capita *fell* after going *off* the gold standard in 1929, the opposite of the conventional narrative that GDP/capita rose after countries abandoned gold (just sayin’)

9. March 2020 at 17:05

you don’t understand currency issues, clearly. there is no other explanation that is viable and your post posed a question. calm done tonto.

further:

Keynes emphasized (money’s) role as a “store of value.” Why, he asked, should anyone outside a lunatic asylum wish to “hold” money? The answer he gave was that “holding” money was a way of postponing transactions. The “desire to hold money as a store of wealth is a barometer of the degree of our distrust of our own calculations and conventions concerning the future. . . . The possession of actual money lulls our disquietude; and the premium we require to make us part with money is a measure of the degree of our disquietude.”…

(“The Remedist”, Robert Skidelsy, New York Times, 2008)

9. March 2020 at 17:14

From CNBC:

President Donald Trump on Monday said he will be meeting with Senate and House Republicans on Tuesday to discuss “a possible tax relief measure” to provide “a timely and effective response to the coronavirus.”

“We are to be meeting with House Republicans, Mitch McConnell, and discussing a possible payroll tax cut or relief, substantial relief, very substantial relief,” Trump said at a press briefing with coronavirus task force members.

The potential tax incentives come on top of an $8.3 billion spending package President Trump signed last month.

—-30—-

A payroll tax cut! It appears President Trump is on the right track. Give credit where credit is due. The Enfant Terrible ala Orange is formidable!

9. March 2020 at 17:36

Side note to anybody:

It seems children are immune to coronavirus.

9. March 2020 at 18:38

The Fed can make inflation expectations hit target very quickly without any special tools.

9. March 2020 at 18:41

The carry trade is a symptom, not a cause, and hence not an explanation. It’s like saying a stock is rising because some traders are covering their shorts. Why are they having to cover their shorts?

I think Scott is essentially right.

9. March 2020 at 18:47

I’d add to the list. Explain clearly what it is doing and be seen to do it.

9. March 2020 at 18:53

Ray Lopez and Scott Sumner, thank you for the back and forth about the carry trade. I’m always happy to read both of you.

10. March 2020 at 00:24

@ Ray Lopez

It is not only the carry trade. Whenever a political /economical situation gets worser (like North Korea plays with bombs) many investors buy the Yen – independent of the rate differential. Please check the charts. The same is true for the Swiss Franc (although now the effect is weaker than in the past).

10. March 2020 at 01:41

@Brian – you mad bro? 😉 I’m surprised Sumner still lets me post here, most people would have booted me long ago… I like reading Sumner, since his views are so weird. It’s much easier to say money is neutral than go through the machinations he does. But who knows? When money is finally digitalized and banks can go below zero interest, which is the modern trend, I’ll guess we’ll see if money is really neutral or not (short term, since long term even Sumner agrees it is).

10. March 2020 at 03:04

I would guess money is not short term neutral because most people and businesses and politicians and pundits and journalists suspect that it is not. These matters should not be examined in a public forum because of a reason omitted. That’s why this blog is subtle. This comment might get censored.

10. March 2020 at 05:38

brian: that’s why its titled “the money illusion”, the pernicious poison advocated most by keynes

10. March 2020 at 05:53

@Ray—-never reason from a carry trade

Scott—-Agree and all in——but the best the Fed will do is somewhere between what you want and the “running out of ammunition” people want. Congress will never do anything now—-so we better hope the Fed has tools now.

PS—my obsession—-Covid 19 and absurd panic. CDC knows vaccines have about a 50% effectiveness rate in any given year—-hard to predict the forward mix of influenzas. Further we don’t even know how many die—-range this year—20-50K, globally, 500-1250k. And half the globe gets a flu shot—-so, given effectiveness rate, about 75% of humans “have no vaccine”—-and no panic?!. Huge unknown death rate and no vaccines.

One of my favorite aphorisms (because I made it up at age 25 :-)) is “we always confuse familiarity with understanding”. We are familiar with the Flu so we “understand” its danger—-no we don’t —-but we accept it. Good thing, because the cure would catastrophic if Covid 19 is any indication.

Covid 19—I have no aphorism to explain it (like “unfamiliarity causes fear”). Our reaction appears unprecedented. As you have mentioned, it appears we are approaching an equilibrium state faster than I would have thought. My guess it is a maximum 2-10% of flu equilibrium (25000 to 125000). I still would bet under.

10. March 2020 at 06:53

It seems to me like the carry trade narrative, the law of one price narrative, and Ssumner’s narrative in this case all agree.

1. Macro shocks cause the expected long-run price level in Japan to unexpectedly increase relative to the expected long-run price level elsewhere precisely because they are unable or unwilling to ease when such shocks hit the global economy. In other words, Ssumner’s argument to me seems to implicitly rely on the law of one price. Because current nominal exchange rates to some degree anticipate such changes in relative price levels, the Yen will appreciate. It will appreciate more relative to the dollar but still some relative to the Euro precisely because the US is expected to be able/willing to ease more than the Eurozone, and thus prevent the expected long-run price level in the U.S. from increasing as much as it does in the Eurozone.

2. Carry traders thus get caught in a short squeeze and are forced to unwind which accentuates the move. Thus you get some degree of “overshoot” or “panic buying” of the Yen, meaning the Yen will actually appreciate more than it would due to changes in the expected long-run price level alone. Evidence: Look at the Gold/Yen price. No central bank can ease Gold conditions at all, and presumably the Bank of Japan won’t tighten, but you generally see the Yen appreciate with respect to gold in times of crisis. Why? Because there are many more carry traders shorting the Yen than shorting gold because its much easier to borrow Yen, causing the Yen to overshoot. In the long run, the Gold price in terms of Yen recovers.

The carry trade argument alone fails to explain why crises should cause carry traders to unwind. For instance those who shorted most other assets, other than the Yen, actually benefit from a crisis, rather than being forced to unwind. Thus the carry trade argument relies on the law of one price to explain why there is an initial appreciation of the yen (or fear of such appreciation) to trigger the panicked unwind.

Scott Sumner’s argument in turn relies on the law of one price to explain why unexpectedly tight monetary conditions in one country translate into an appreciation of its currency relative to countries who have better monetary policies. Presumably, the countries with better monetary policies will enjoy greater rates of RGDP growth and therefore it is non-obvious that their currencies should depreciate relative to the country with the worse monetary policy. The law of one price explains why countries like Japan can have consistently poor economic growth and lower real interest rates yet still maintain strong currencies.

10. March 2020 at 09:17

Why are people making the Carry Trade critique? Is it because you think that the Carry Trade argument somehow refutes the point of the blog post or is it because you think that nobody believes the yen is a safe-haven currency? I don’t see how the Carry Trade argument could refute the post because the Carry Trade is just a technical factor and the point of the post is that technical factors, not fundamental factors, underlie the flight to the yen. Regarding the second argument, a quick googling of “the yen is a safe haven” brings up a long list of articles by financial sites making exactly the claim that the yen is a safe haven currency or debating the merits of the claim. It seems there are a lot of people out in the world who believe it has fundamental value as a safe haven.

10. March 2020 at 09:56

@Michael Rulle – it’s been said humans have evolved to detect big threats (lion on savanna) not little threats (3.5% death rate rather than 0.1% death rate).

@ Carl, @Tuharsky – good points. And I’ll add that David Stockman, the economist (deceased) not Reagan’s budget chief, wrote a seminal paper in 1989 that Sumner should be familiar with, which pointed out huge swings in nominal values in Fx markets and in foreign exchange factor markets (like terms of trade, like trade deficits, like weak or strong currency) have NO REAL EFFECT on the economy. Re-read this sentence. No. Real. Effect. It’s all a wash, doesn’t matter. It’s actually one piece of evidence some economic commentators have used to say that money is neutral. In fact, right now I’m moving money from the USA to Greece and was shocked the rate went from 1.08 to 1.13 in a week, but it won’t stop me from transferring the money. No. Real. Effect. Interest rates? Pfft. Exchange rates? Please. Sure they have a 3.2% to 13.2% effect (out of 100%, reference to Bernanke’s FAVAR paper) but most people focus on the 90% and ignore the noise. Ignore the noise. Reminds me I should not be reading this blog…but it’s so fun!

10. March 2020 at 10:11

Everyone, There are two kinds of people:

1. Those who think a liquidity effect occurs after a monetary injection because the Fed buys bonds, driving up their price and driving down their yield. These people think of monetary policy in terms of concrete actions in financial markets.

2. Another group understands that a monetary injection can drive down interest rates even if the Fed buys gold, or just showers the money on the public. Rates fall because you need lower rates for the public to be willing to hold larger balances of zero interest cash. It has little to do with the specific assets being purchased by the Fed.

The people babbling on about carry trades remind me of the first group.

11. March 2020 at 08:41

I may be late here, but I recall reading an IMF working paper a few years back that looked into Yen’s safe haven status and concluded it was due to higher expectations of Japanese repatriating their high level of foreign assets (and turning them back into Yen)

As a side note, Scott – I know you’ve previously advocated for the BoJ to buy massive amounts of foreign assets, including equities. The Swiss National Bank is famous for doing this exactly (known as the “world’s biggest hedge fund” in some circles), but inflation there remains low. Are they just not doing enough? Should they be paying each Swiss citizen a massive annual dividend? It’s already doing so to the national and regional governments. I’d be interested in a post on the SNB – they’re definitely doing some unorthodox things there.

11. March 2020 at 15:13

sd0000, I’ve done a number of posts on the Swiss. They made a huge mistake in 2015 when they ended the peg against the euro, and allowed the SF to appreciate. Level targeting of inflation at 2% would also help. They are practicing defensive policy, not offensive policy.

12. March 2020 at 08:32

Scott – thanks for the reply – I do recall your post in 2015 actually. Regarding their practice of aggressively buying international equities (“buying up the world”), isn’t that exactly what you propose for a central bank in the position of a Switzerland or Japan? Why are they not seeing success with it? Is it just not aggressive enough? I’m genuinely curious – I recall reading a post where you suggested Japan should buy foreign equities, then later saw it was exactly what Switzerland does – so was wondering what you thought of the practice.

12. March 2020 at 13:22

“we’re not here to close spreads, this is not the function or the mission of the ECB”-Lagarde

12. March 2020 at 19:43

All of this reliance on monetary policy puts the purchasing power of the currencies at risk. Remember the Wiemar Republic and learn from history. As for the euro, it was dysfunctional in the first place. It can’t coordinate both fiscal and monetary policies.