What if the spotlight had been on the Fed in 2009?

This is an addendum to my previous post.

I think some commenters are underestimating how different the intellectual climate would have been in 2009 absent ANY fiscal stimulus. The Fed would have been seen as the only game in town. Instead of the near total blackout of discussion of monetary policy, the pundits would have been talking about little else. They would have immediately dug up Bernanke’s writings on Japan (instead of waiting months for Marcus Nunes to do so), and asked why the Fed couldn’t do the same in America. Recall that we were in DEFLATION at the time, just like Japan.

My PLT hypothesis still embedded a 2% inflation target, albeit with level targeting. Does anyone seriously believe that would have been viewed as too radical if our fiscal policymakers were doing nothing to prevent a depression? If anything, I’d expect many economists would have been suggesting a 3% or 4% inflation target. My counterfactual was fairly conservative. And the Fed usually does roughly what a consensus of economists wants them to do.

And yet . . . as conservative as it sounds, it still would have led to considerably faster NGDP growth than we actually got.

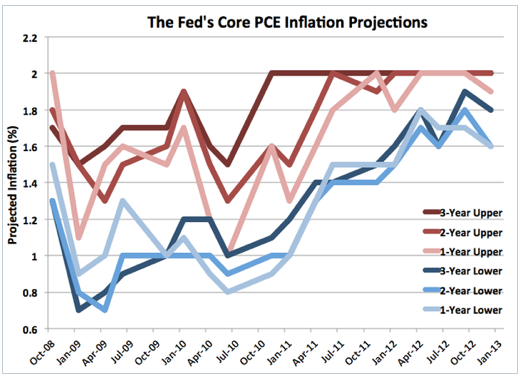

BTW, anyone who thinks the Fed is aiming for some “catch-up” with the price level, needs to consider this excellent article by Matt O’Brien from a few weeks back. He shows that since the recession got bad the Fed has never once forecast above 2% inflation, on any time horizon. Even though we are well below the 2% trend line from late 2008. Here’s the money shot:

Premature exit strategy.

PS. In the comment section of the previous post Matt Rognlie pointed out that fiscal stimulus can increase output via supply-side effects. So I was a bit sloppy there. When I said the multiplier was zero under inflation targeting I was referring to demand-side effects. Obviously if the multiplier is defined in terms of RGDP then it isn’t necessarily exactly zero, it might be positive or negative depending on supply-side effects.

Tags:

13. March 2013 at 13:27

Another political thought, which is that voters expect elected officials to act in the face of a crisis. It may not be realistic to expect any set of elected officials to do nothing while the Fed directs the economy.

13. March 2013 at 13:40

I’m not an economist, so these just a naive question, but:

1) Would QE have been an option in 09? Since the Fed did in fact choose QE when it had to do something, why would it have been more likely to do PLT absent the stimulus?

2) The question I’ve been picking up from this and other sources is: why isn’t Bernanke following his Japan prescription? Political constraints from the other Fed officials or from Congress might explain it, or maybe he just doesn’t think it’s necessary. But since he didn’t do it as the US slid into a nasty recession and approached depression, why would we think he would have done it in the counterfactual?

13. March 2013 at 14:14

I’m trying to understand the logic path, forgive me…

– Bernanke is a smart person who wants to meet the dual mandate

– Bernanke can be constrained by hawkish elements at the Fed or political winds

– ARRA is proposed in 2009

– ARRA turns attention away from Bernanke

– ARRA may or may not have been effective

– Now we’re at 7.7% unemployment

I guess I have some random questions, then:

– Judging by Bernanke’s grilling the other week, most of the people who pay attention to monetary policy are inflation hawks. When attention turned away from Bernanke, why didn’t he see that as a plus, and “debase the currency” until full employment? Why would attention lead to more action, instead of less?

– An obvious question: why does Bernanke keep saying he wants more stimulus policy, if the Fed doesn’t need it, and politicians won’t deliver it?

– I guess I don’t see how monetary policy changes are so discrete (inflation targeting -> price level targeting -> NGDPLT). Can’t the Fed increase its balance sheet continuously? And if so, couldn’t it have hypothetically exactly counteracted ARRA, to the dollar?

13. March 2013 at 14:25

I understand why you prefer monetary action, but do you really think it would have been wise for the legislature and WH to skip on fiscal stimulus and trust the fed to do the necessary work? That seems like an awfully risky bet to take if you think fiscal stimulus will help but you don’t know how the fed is going to respond.

It took the fed quite a while to finally do QE despite low inflation, low project inflation, low inflation expectations and a crashing economy. Would a greater magnitude disaster have increased their response speed? Probably. Enough for that path to be a preferable one? Let’s just say I’m glad we didn’t try. My perspective is that the attitudes of people calling the shots to fiscal stimulus are actually less dumb than their attitudes towards monetary policy.

13. March 2013 at 15:05

Off topic… have you guys seen this yet ?

What’s the best way to design a carbon tax? Lawmakers ask for suggestions.

Posted by Brad Plumer on March 13, 2013

“On Tuesday, four Democrats in Congress unveiled a brand-new proposal for a carbon tax. The set-up is simple: The U.S. government would slap a fee on fossil-fuel emissions and refund the revenue back to the public.

But there’s a twist: The precise details of the carbon tax have yet to be thrashed out. The four lawmakers are soliciting public comments …”

http://www.washingtonpost.com/blogs/wonkblog/wp/2013/03/13/lawmakers-unveil-a-choose-your-own-adventure-carbon-tax/

Just maybe the some of the pubic will be interested in the carbon tax debate. Who’s voices will be heard ?

13. March 2013 at 15:08

Scott:

I fear that the “we promise to keep the interest rate at zero for an extended period of time” and promise to target inflation at 2%, would have been the policy for a substantial period of time.

I fear that the reality is that things might be better now, but it would have been a situation of “things must get worse before they get better.” That is, perhaps Bernanke would have been replaced and Obama would have actually filled the vacancies on the Board of Governors.

But…. Are we really sure that he wouldn’t have gone with nominees who would work really hard to make sure that future borrowers were not exploited by the evil lenders?

Maybe they would have asked Woodford what they should do. Maybe.

13. March 2013 at 15:14

No Fiscal action? I take it that that means no bailout either…

Then I see the Fed buying swapping large amounts of “toxic” paper for clean new money. This would recapitalize the banks, and may have proved more effective in ultimately resolving the bad debt problems, but it would open a large can of political worms for the fed.

Some criticism would be justifiable, but all of the usual cranks, left and right, would come out and say how the Fed is an undemocratic instution that is either out to line the pockets of greedy bankers, or to debase the currency.

The fundamental question would be, how did the Fed arive at its marks those transactions.

13. March 2013 at 15:27

Bill Elis,

Carbon tax? The simpler the structure the better.

Cap’n Trade is out.

I would say tax the fuel directly.

Everyone pays for the CO2 they create.

There would be a gasolene tax.

There should probably be a beef tax.

No credits for current poluters.

No protections for “Big Oil” or “Big Power.”

However, I would encourage municipal utilities districts and local regulators to allow the power providers to pass at a significant fraction (but definately not all) of their increased costs on to consumers.

No credits for tree planting or other “offsets.”

Let the money go straight into the General fund of the US Treasury.

13. March 2013 at 15:27

Scott, what do you think would have happened if McCain won in 2008 and appointed someone like John Taylor, who publicly opposed both asset purchases and a higher inflation target? How do you think he would have responded to an absence of fiscal stimulus (not that I think Republicans wouldn’t have enthusiastically supported stimulus had they won)? If Bernanke is about as close to market monetarism as you’re going to get in a Fed chair, does your counterfactual still hold up if he was replaced by someone with a very different view of monetary policy from yours?

13. March 2013 at 15:27

Scott – that previous post I think was your best since the very first (or one of the first) on George Warren.

13. March 2013 at 15:33

Scott, do you think that fiscal stimulus is worth it in absence of Fed action? For me, I rather suffer out the recession normally without the goverment blowing money on there friends and increasing debt. Probebly producing negative supply factors.

13. March 2013 at 16:46

Adam, I agree, and have argued they should have cut employer-side payroll taxes to boost jobs.

J Mann, They did do QE in 2009, and if things had been even worse (no fiscal stimulus) the Fed would probably have done a more powerful stimulus.

Sam, Yes, they can increase their balance sheet continuously, and they could have offset a lack of ARRA. They tend to do what a consensus of economists favors, not what loud-mouthed Congressmen demand.

mpowell, I think ARRA was an incredibly risky bet. Spend $700 billion when it might well make things even worse? When in doubt, do nothing, especially if doing something costs $700 billion.

The Fed did QE1 in March 2009, so it didn’t take that long after rates had hit zero in December 2008.

The Fed moved late last year partly due to the expected fiscal tightening, and so far it seems to have roughly offset it.

Bill Ellis, How about cutting taxes for the poor? Lower the cigarette tax and increase the EITC.

Bill Woolsey, I gave my best guess, but obviously anything is possible. Still, the policy arena would have looked vastly different with the spotlight on the Fed.

Aidan, My hunch is that Taylor would be more dovish than his recent statements, but I can’t be certain. It’s an interesting question.

Thanks Tommy.

Nickik, I think tax cuts and some types of infrastructure and some additional aid to the poor would be worth it if it did boost NGDP. I’d still oppose extra military spending however.

13. March 2013 at 16:54

Prof Sumner: Apologies if a bit off topic for this specific thread, but your mention of catch-up inflation is interesting. What if the FED, or BoJ, whoever said that over a 10-20 year period, or even longer, it would guarantee that inflation over that period would average, retrospectively, 2% or 3% a year, or whatever target it chose as optimal? Thus, even if (relatively) powerless at the zero bound now, during a recession, over a stated period of time, the Central Bank would guarantee inflation averaging whatever the target is when the economy recovered. In other words, if too low early in the cycle, it would tolerate higher inflation — even very high inflation — in the later years, to make up for it. And vice versa — if inflation runs way above target in some intermediate years, it would pull back/tighten in later years, after the economy has recovered, to meet the target. Would this not make monetary policy more effective an d credible at the zero bound? Would it not also decrease concerns about near term inflation, if needed to spark a recovery? I doubt that you would favor this as a NGDP targeter, but would it not accomplish much the same thing?

13. March 2013 at 19:29

From a political economy perspective, maybe the no-stimulus counterfactual’s success would hinge on this: maybe the GOP would have avoided its anti-Friedman turn if it had seen monetary policy as an alternative to fiscal stimulus, rather than a tag-along. It’s tough to imagine PLT if the GOP was shouting about debasement, but not if both parties were at least tacitly supportive.

14. March 2013 at 03:24

[…] See full story on themoneyillusion.com […]

14. March 2013 at 05:43

“Premature exit strategy.”

Don’t you mean Premature Withdrawal?

Sorry, 7th grade humor…

By the way, I find your story plausible Scott, but I also find Bill W’s plausible too. I admit in 2009 I was scared, and I favored the stimulus mostly because I was afraid of what might happen if it did _not_ pass.

But it’s also worth noting that the markets continued to collapse anyway after the stimulus passed, until the Fed finally did something real in the spring. It’s also worth considering who was on the voting board at the time.

14. March 2013 at 09:20

So now we’re only talking about the discretionary spending part of the ARRA? There was also aid to states in there who were cutting spending and also some big tax cuts – I don’t know if the payroll cuts were formally part of the ARRA or not, but that counts as fiscal stimulus right? I would agree that trying to ramp up federal spending as an immediate response is not the best fiscal policy or probably even a good idea at all. But aid to the states (I mean, does it really make sense to start laying off teachers during a recession?) and payroll tax cuts seem like pretty low risk/high reward moves if you are not sure about what the fed is going to do. The bigger the economic collapse, the more unrecoverable damage. If a viable business goes out of business because NGDP falls precipitously, the loss of capital is real and largely permanent.

14. March 2013 at 11:31

maynard, It might well be better, however I believe they can hit their target fairly quickly, even at the zero bound. I certainly agree that level targeting is better than growth rate targeting.

Josh, Very good point.

Statsguy, Those are very good points.

And I had the same thought after I typed “money shot”

mpowell, I agree that employer side payroll tax cuts can help, but unfortunately they did employee side payroll tax cuts.

15. March 2013 at 10:07

If your argument is that fiscal stimulus can work at increasing NGDP in the presence of an incompetent fed, but that the gov spends money wastefully, why would you object to an employee side payroll tax cut? Or are you just saying that an employer side cut would be better?

16. March 2013 at 06:23

mpowell, Because soimething “can” work doesn’t mean it will. I said an incompetent Fed is a necessary condition, but it’s not a sufficient condition. The Fed must be incompetent in a particular way. I’m skeptical that it is.