Way too tight

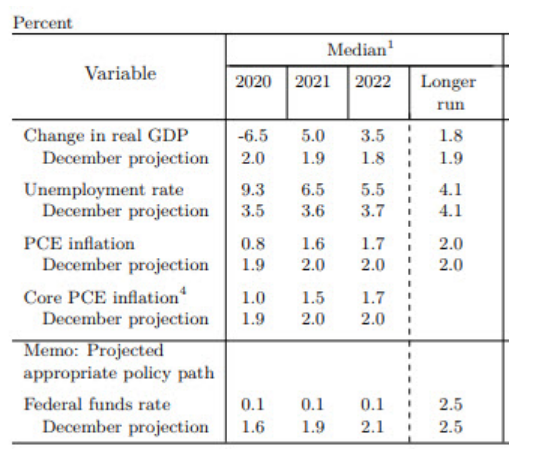

The Fed’s new inflation and unemployment projections show that monetary policy is currently way too tight. Unemployment is projected to remain high through 2022. That may be excused by the Covid-19 pandemic, but there is no excuse for the low inflation, especially low core inflation:

The Fed had the option of switching to level targeting, and blinked. That error will be quite costly in terms of both inflation and growth.

Again, unemployment may be beyond the Fed’s control at the moment, but at a minimum they need to target the inflation forecast. I can’t even comprehend the 1.7% PCE inflation forecast for 2022. Does the Fed plan to acquiesce to this sort of policy failure for two whole years, without even attempting level targeting?

PS. The implied 2019-2021 NGDP growth forecast seems to be about 0.9% (total). By comparison, the total NGDP growth from 2008:Q2 to 2010:Q2 was 0.8%. And unemployment was over 9% throughout 2010. Perhaps they are assuming a greater degree of wage flexibility today.

PPS. Is there anything more annoying than talking heads on Wall Street TV shows saying the Fed has already done too much because stocks are recovering?

PPPS. Powell was asked about inflation forecasts being under target, but sort of dodged the question.

Tags:

10. June 2020 at 13:53

Why would we rely on Fed forecasts? If i’m not mistaken, asset prices have been a better indicator of forward growth than Fed projections…and i don’t think the score is particularly close. Garbage in, garbage out, no?

10. June 2020 at 13:54

I guess that by saying they will “keep” interest rates at 0 for the foreseeable future it is seen as stimulative by the general public. It feels like the the Fed’s heart is in the right place because they want to be accommodative as much as “possible” but they are skeptic about being able to generate inflation in the short or medium term. It is as if they don’t believe in their own power? Or are unwilling to use their power to the fullest. Still Jerome has been a lot faster in reacting to the crisis than Ben was to 2008, and Ben is probably one of the best economist we have. Although it might be baby steps I do believe we are moving in the right direction.

ps. I am buying up all the gold I can because some guy on cnbc said inflation is coming. (sike)

10. June 2020 at 14:37

The simplest explanation is that the Fed strongly avoids admitting that it doesn’t understand the relationships between its policy levers and forward inflation expectations. To admit this would invite even dumber inputs from those even less informed that it is (congress, media commentary, etc.)

10. June 2020 at 15:19

Marklouis. I agree, but asset markets are also predicting lowflation.

Romeo, Maybe, but that doesn’t explain the refusal to shift to level targeting. After nearly 12 years of lowflation they are running out of excuses.

10. June 2020 at 15:20

Scott,

I don’t necessarily agree. We should look at the market forecasts rather than the Fed’s own forecast.

I think it is pretty clear that the FOMC doesn’t dare to be bullish enough on the US economy, but look at 5y5y inflation expectations we are nearly back to where we started in mid-Febuary and in terms of the stock market we are now back to levels similar to where when the shock hit in late-February.

To me that means that the monetary policy stance is more or less the same as prior to the crisis. Fed really isn’t making things worse. This is not a repeat of the errors of 2008-9.

Obviously we would be having this discussion if the Fed had a NGDP level target, but that is another discussion.

10. June 2020 at 15:26

Scott,

Yes, there are very few things more annoying that hearing that the fed has done too much.

10. June 2020 at 15:34

I agree with this post.

Even worse, the Fed’s forecasts are probably high in regards to pce core inflation. The Cleveland Fed forecast for the next 10 years is about 1% on the CPI, so cut that a little bit to get the forecast for the PCE.

https://www.clevelandfed.org/our-research/indicators-and-data/inflation-expectations.aspx

If ever the Fed should overshoot its inflation target, now is the time. Surely, there is a connection between urban unrest and mass unemployment.

BTW, housing construction has been criminalized in large parts of the US, such as the West Coast. Any macroeconomist or observer concerned about measured inflation should prominently mention the restrictive effect on supply of property zoning.

10. June 2020 at 15:43

Lars, I don’t think the 5y5y is at all useful. It’s the 5-year spread that matters—2020 to 2025.

And even if inflation between 2025 and 2030 is likely to be reasonable, the next 5 years look bad. But the 5y5y forward spreads are also too low.

I predict the price level will fall well below a 2% level target path over the next few years. NGDP will do even worse.

bb, Especially when people cite the stock market as evidence, even as average Americans face below 2% inflation and high unemployment, and the Fed itself says it will fall short.

10. June 2020 at 16:10

I disagree that Powell dodged the question about inflation forecasts. Here is what he said

“ you’ll know that we had a 128 month expansion and we never did quite get inflation back to 2% on a symmetric, sustained basis. We got close for the last couple of years, but we never did quite get there. So I think we have to be humble about our ability to move inflation up. And particularly when unemployment is going to be above most estimates of the natural rate, certainly above the median in our SEP, well past the end of 2022.”

My takeaway from that is that he, and maybe the rest of the Fed’s voting members, believe that unemployment must be below the NAIRU for inflation to rise. And they don’t believe that they have the power to get unemployment there, so they don’t believe that they can substantially raise the inflation rate.

Am I misunderstanding what Powell was attempting to communicate?

10. June 2020 at 17:27

–“Why would we rely on Fed forecasts? If i’m not mistaken, asset prices have been a better indicator of forward growth than Fed projections.”–

Asset prices can rise because of many things: higher expected cash flows, certainly, but also from Fed balance sheet expansion (sellers of fixed income assets may choose to buy stocks and other assets), substantially lower interest rate expectations, etc.

–“You’ll know that we had a 128 month expansion and we never did quite get inflation back to 2% on a symmetric, sustained basis. We got close for the last couple of years, but we never did quite get there. So I think we have to be humble about our ability to move inflation up”–

The Fed spent 2015-2018 continuously raising the Fed Funds rate and concluded that, after undershooting on inflation by several tenths of a percent, that it might be *unable* to hit its target???

10. June 2020 at 17:58

The nonsense from sumner continues…

“ Marklouis. I agree, but asset markets are also predicting lowflation.”

-Asset prices predicting “lowflation,” yet amzn trading at 126x earnings. Zim trading at 1200x earnings….. And don’t think about countering this by referencing break even spreads.. As you know, CPI is a garbage measure. Also, if you were a government issuing debt linked to an inflation index that you happened to control, would you have any incentive to manipulate it? Neverrrr!!

Sumner- if you’re so confident about “lowflation” then put your money where your mouth is. Although I know that’s tough given your ivory tower situation…

10. June 2020 at 18:37

So Lars is kind of really optimistic at the moment and Scott not so much. Both have good arguments.

Scott’s investment advice, even though never labeled as such, has been the best over the years.

I’m excited to see how the assessments will turn out.

10. June 2020 at 20:34

It’s really interesting, isn’t it… As an academic, Bernanke quipped that QE works in practice but not in theory, whereas most academics would agree that level targeting works in theory but they aren’t completely sure it will work in practice. As you’ve said before (https://www.themoneyillusion.com/qe-works-in-practice-because-qe-works-in-theory/), all this hand-wringing over central bank ‘credibility’ amounts to hill of beans – it’s really all in the hands of the practitioners and the determination they exhibit or signal.

But I do wonder if the greater academic support for level-targeting over ‘QE’ creates something of a bind for central bankers. If QE is seen as ‘not working’, they can shrug their shoulders and distance themselves from the failure or ramp up their efforts a notch, all without putting their intellectual reputation on the line. But if level targeting is regarded as having failed, the whole edifice of Krugmanian-Woodfordian NK macro comes tumbling down. Level targeting requires a leap of faith – one either does or does not, there are not the same degrees to play with as with the dollar value of LSAPs, “there is no try”. I’m not saying this is right, but my guess is academics’ mindset is: “It either works or my own intellectual credibility is shot forever”. It reminds me of the Lakatosian idea that scientists are willing to subject their auxiliary hypotheses in their protective belts to testing but are too unwilling to permit falsification of their hard core ideas.

11. June 2020 at 00:01

“The chart above speaks for itself.”?

“In the year to May the M3 measure of money – which corresponds to the M2 measure favoured by Milton Friedman and Anna Schwartz in their 1963 A Monetary History of the United States – increased by just over 25.5%. This was the highest increase in the quantity of money in modern American peacetime history. . . .

Today the situation is very different. Banks are not being asked to raise more capital and, on the contrary, capital adequacy rules have been relaxed. (Quite right too in the circumstances.) Particularly in the USA, and to a lesser extent elsewhere, governments have ballooned their budget deficits and financed them from banking systems, creating extra money balances. QE exercises have also been undertaken, with further additions to the quantity of money over and above those due to monetary financing of the budget deficit. The fiscal and monetary sprees have been so huge and permissive that broad money growth rates have risen to extraordinary levels. As I have pointed out above, and about which I have in fact been hinting for some weeks, the USA now has the highest annual growth rate of the quantity of money in its peacetime history. So – unlike late 2008 and early 2009 (and indeed for a few years thereafter) – I am very worried about a sequel in which annual inflation takes off into the double digits, at least in the USA. The chart above speaks for itself.“

https://mailchi.mp/8f126f390556/which-economic-thoughtcomes-out-best-from-the-last-decade-1336071?e=260ed9002a

11. June 2020 at 00:46

Food for thought. The Fed is doing about $120 billion a month in QE (buying of Treasures and mortgage-backed securities).

“Summary of the Latest Federal Income Tax Data, 2020 Update. In 2017, 143.3 million taxpayers reported earning $10.9 trillion in adjusted gross income and paid $1.6 trillion in individual income taxes.”

Okay, if the US would send to every taxpayer a check for $1,000 a month, that would come to about $143 billion a month, a little larger than the Fed’s QE program.

The Fed/US is willing to print money and monetize debts. But to what end?

11. June 2020 at 02:56

Lars,

“Fed really isn’t making things worse. This is not a repeat of the errors of 2008-9.”

Not ‘beautifully calibrated’?

“In late 2008 and early 2009 the big problem was that officialdom’s demands for large increases (of over 60%) in banks’ capital/asset ratios were leading to the destruction of money balances, with severe deflationary consequences. In my work – which is very different from, for example, that of Ben Bernanke in the USA and the research department at the Bank of Japan – the purpose of QE was to create new money balances which would keep the overall rate of money growth positive despite the money destruction. That is roughly what happened, and in fact in the USA and UK the QE exercises were beautifully calibrated to deliver money growth of a bit less than 5% a year . . . Both economies recovered and stabilised, etc.“

https://mailchi.mp/8f126f390556/which-economic-thoughtcomes-out-best-from-the-last-decade-1336071?e=260ed9002a

11. June 2020 at 05:22

It’s somewhat baffling that the Fed is forecasting it will fall short of its inflation target without taking action. I suspect it means the FOMC thinks its out of ammo, with regard to supporting NGDP, or still fears overshooting more than undershooting.

After leavin the Fed, in a discussion with Krugman, Bernanke revealed that he thought there was a limit to the effectiveness of QE, at least under the current regime.

11. June 2020 at 05:54

It’s extremely baffling that the Fed is not taking further action. Does this suggest they will take further action in the coming weeks? Or that they are too terrified of overshooting and getting blamed for that? They know they are never out of ammunition. Very strange signals coming from them.

11. June 2020 at 06:24

If there is a shortage of $s, then why is the $’s exchange rate declining?

The $ started dropping when the FED increased foreign liquidity swaps:

“To improve the swap lines’ effectiveness in providing U.S. dollar funding, these central banks have agreed to increase the frequency of 7-day maturity operations from weekly to daily. These daily operations will commence on Monday, March 23, 2020, and will continue at least through the end of April. The central banks also will continue to hold weekly 84-day maturity operations.”

If the FED tries to target N-gDp (which they always have but just can’t forecast), then it shouldn’t be subverting its policy abroad.

11. June 2020 at 07:04

Interesting.

So how would the Fed make policy looser from here?

Would you impose negative rates? Or make more/larger asset purchases.

Thanks

11. June 2020 at 07:10

Life comes at you fast Jerome. The Fed’s job is never done. Today’s stock market may shut the hawkish Fed critics up a bit.

11. June 2020 at 07:19

I was pretty encouraged by asset price levels until the Fed came out and said “we expect to fail, we expect short term rates and inflation to remain low”.

The Fed seems to be operating under a false constraint. They think, like the vulgar financial press and random cranks in the comments sections, that asset prices are analogous to a motor or a biological organ which can be driven “too fast, too soon”. There’s clearly a fear that asset prices will become “overloaded” by “extra” monetary stimulus, in the way a motor could be driven out of spec.

It seems the concern is that if you targeted the forecast so that NGDP were about 4.5% from 2021Q1 through 2022Q1, that asset prices would rise too fast, and then there’d be some catastrophic debt crisis within a few years that the Fed was unable to counteract.

Operating under uncertainty about the true dynamics of the economy, the FOMC chooses to do too little, this way they can’t be blamed if there is a market reassessment that results in some major asset class being re-priced downward, and they get street cred for low inflation.

11. June 2020 at 08:15

It was not much more than a month ago when Powell was saying we will do “whatever it takes” and that the Fed had plenty of “ammunition”….now he says we are locked into a below target inflation level. Maybe it just appears like he has changed his mind, but it sure looks like he has. Does the Fed have a powerful “lifer” bureaucracy like State? I don’t get it.

11. June 2020 at 08:37

Burgos, But elsewhere in the talk he said the Phillips Curve model that says unemployment determines inflation doesn’t seem to work any longer.

In addition, it’s weird to cite 2017-2019 because the Fed was trying to REDUCE inflation during that period, through repeated increases in the target interest rate.

Rajat. The problem is that you need the right target and the right policy to hit the target (level targeting and target the forecast). What if you only do one of the two and it fails? Does that discredit the policy, or suggest you should have done both? Level targeting makes it easier, but the Fed could do “target the forecast without level targeting. And they are not doing so. Which means they don’t wish to do so.

Academics cannot fix flawed systems, only policymakers can do so.

Ben, You said:

“Okay, if the US would send to every taxpayer a check for $1,000 a month, that would come to about $143 billion a month, a little larger than the Fed’s QE program.”

Umm, You do realize . . . I guess not.

Mike, They never run out of ammunition, and they know this.

Henry, Switch to level targeting. Then target the forecast.

Michael, You asked:

“Does the Fed have a powerful “lifer” bureaucracy like State?”

Yep, and it’s way more powerful than at the State Department.

11. June 2020 at 10:45

Touché. One day after Scott expressed his concerns, and the stock markets are already correcting.

Similar things happened in February, when the market just wouldn’t crash, even though we already had a pandemic. Or in mid-March, just before the Fed made its announcement. The list goes on, this is just this year.

Is Scott’s neurological system somehow connected to the stock markets?

Scott, maybe you should become an investment advisor and start charging fees.

11. June 2020 at 11:23

Scott,

What gives you confidence that the Fed thinks they never run out of ammo? Bernanke used to say the Fed can’t run out of ammo, but listen to him 8 months ago, at about the 23:35 mark:

https://www.youtube.com/watch?v=JmZkpqwtlKU

I know a lot of Fed officials say they can’t run out of ammo, but why should I believe they’re being honest?

11. June 2020 at 11:25

Scott,

And I’m referring to running out of ammo using the current inflation targeting regime with QE, not adding some form of level targeting, for example.

11. June 2020 at 12:24

Christian, Someone should make a comprehensive list of all the times I was right, to boost my ego. My EMH philosophy makes me prone to depression.

Mike, You need to recall that to people like Bernanke my “whatever it takes” approach to monetary stimulus is basically “fiscal policy”, as it envisions the purchase of risky assets if necessary. Bernanke never denies that a central bank could inflate if it bought enough assets.

Also note that Bernanke favors level targeting, so presumably he agrees with me that monetary policy is currently off course.

11. June 2020 at 12:28

[…] Original Post […]

11. June 2020 at 12:46

@Prof. Sumner

Thanks for pointing that out.

What is your explanation for the logical inconsistencies? I can square the idea that the Philips curve doesn’t work as a guide for policy anymore with a belief that the Fed doesn’t know how to raise inflation. But the inconsistency between actively trying to lower inflation during one period of time and then claiming bafflement that inflation was too low is something that I cannot at this moment explain.

That said, I still think something more than a dodge on inflation is going on at the Fed.

11. June 2020 at 16:10

The simplest explanation is that the Fed strongly avoids admitting that it doesn’t understand the relationships between its policy levers and forward inflation expectations.

Actually, it’s just the opposite. The Fed loves to tell the Congress that they don’t understand very much. If they admitted to knowing the effects of their policies, they would have to take responsibility for them. And the number one imperative of any bureaucracy is to avoid accountability.

11. June 2020 at 18:38

The Fed may not have announced level targeting but any day of the week it cares to, they could enter the TIPS market as set inflation expectations at 2% PCE equivalent.

12. June 2020 at 02:58

Thomas – Seriously? So to boost inflation expectations, you want the Fed to start buying government bonds which are indexed to a BS index created and maintained by the government, to artificially boost their price and signal higher inflation expectations to the market? What fairy land are we living in? People are not as stupid as you think. Why we’re at it, next time we’re in a recession, let’s have the government issue bonds linked to GDP, and have the fed buy those up too. Problem solved.

12. June 2020 at 06:32

re: “In addition, it’s weird to cite 2017-2019 because the Fed was trying to REDUCE inflation during that period, through repeated increases in the target interest rate.”

Apparently you don’t understand money and central banking. The FED eased monetary policy in the last half of 2017. It responded to the stagflationists: “Rethink 2%”. Monetary flows, volume times transactions’ velocity then rose (not fell).

That drove savings into the banking system which destroyed money velocity. You are clueless

12. June 2020 at 09:09

@Nick S

As long as they can hit their mandate, they’d be making a profit. Buy the treasuries at implicit inflation rates less than 2% and then when the rates come in at 2%, it’s a profit. Or just resell them as soon as expectations reach 2%, no need to wait for maturity.

Granted, this assumes the Fed can actually manage to create inflation (which any central bank should be able to do easily if desired).

Scott, Jokingly, this is one piece of evidence that there are still parts of the government that haven’t reached banana republic status. We can’t seem to create inflation and are coming in under desire on inflation. Banana republics tend to inflate over reasonable targets.

12. June 2020 at 09:29

Burgos, I don’t believe that Fed chairs always say what they really think. They must represent the consensus view of the Fed. Bernanke was clearly uncomfortable explaining why the Fed did not do more. I would have felt the same.

Dan, Yes, that’s one consolation. 🙂

12. June 2020 at 14:38

Scott: You do realize that the Bureau of Labor Statistics’s derivation of the Producer Price Index drives down inflation? When BLS economists increase the real dollar value of shipments by adding an estimated value of quality increases it lowers the deflator. Therefore, an actual increase in the nominal dollar value of such shipments will lead an inflation decline.

14. June 2020 at 09:01

Art, I understand that estimates of inflation are lower when estimates of RGDP growth are higher. But the Fed doesn’t target actual inflation, they target actual measured inflation.

14. June 2020 at 20:00

Scott: Thanx for you response. I guess it comes down to the fact that you and most economists have no problem with the impact that the BLS deflation process has on vital economic data.

Not sure what the difference between “actual inflation” and “actual measured inflation” is. My concern is the BLS measure of inflation (is that “actual inflation”or is that “actual measured inflation”?). What inflation measure is used in models, in calculating productivity, in calculating real GDP? Is it not the BLS measure?

The hooker is that BLS employees estimate quality increases of goods and monetize these increases. These estimates have no connection with any market transaction. They impact the output side of the Accounts but not the input side.

Economists use these real values in their models with no idea how much of an impact the deflation process has and they don’t seem to care. As a result you accept productivity measure that have no relationship to nominal wages or that the increase in real shipments as estimated by the BLS has lowered measures of inflation.

BEA has a number of minor adjustments to the National Accounts such as Food Consumed On Farms and the Inventory Valuation Adjustment that insure that both sides of the accounts balance. In its deflation process the BLS calculates the dollar value of the quality adjustment both in total and by industry which can easily be released with the PPI. Wouldn’t it be of value to see how the impact that estimates of quality change have on Real GDP, productivity and inflation measures?

My basic concern is that the introduction of quality increases inflates the real dollar output but it is ephemeral and not felt nor seen by the workers.