Two ways of thinking about the Phillips curve

There are two ways of thinking about the Phillips curve relationship:

1. Falling inflation causes higher unemployment.

2. Higher unemployment causes falling inflation.

Irving Fisher invented the Phillips curve back in the early 1920s, and employed the first interpretation. Milton Friedman also approached it that way, although he refined the model by emphasizing unanticipated changes in inflation. In a world of sticky nominal wages, an unanticipated fall in inflation tends to raise real wages, resulting in more unemployment.

New Keynesians use the second interpretation. In their view, higher unemployment creates “slack”, which drives inflation lower. That’s become the standard approach, although I’ve never liked it for reasons I’ll explain in a moment.

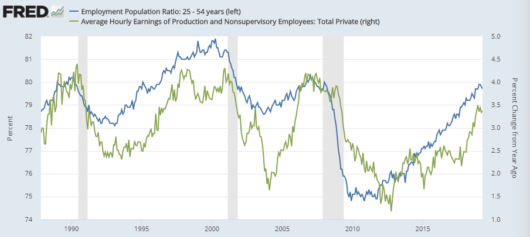

Greg Mankiw has a new post that suggests the Phillips curve is alive and well. Interestingly, he uses nominal wages:

Reading Mankiw’s post I suddenly got a brainstorm. Start with the fact that inflation is obviously not the right variable for the Phillips curve. Every day that goes by, that becomes more and more obvious to me. But what is the right variable? There are two directions one could go, depending on whether one wants to highlight the Fisher/Friedman approach, or the New Keynesian approach.

Mankiw points to a paper that he co-authored with Ricardo Reis to justify the use of nominal wages. I think he’s right that wages are the correct nominal aggregate in the new Keynesian model, not prices. If you want to argue that slack reduce inflation, it’s most likely to show up in wages, as prices reflect both AS and AD shocks. And wages are stickier than prices, and thus a better target for monetary policy.

Using the Fisher/Friedman interpretation of Phillips curve causality (nominal shocks have real effects), NGDP is the right nominal aggregate. Recall that nominal wages are sticky in the Fisher model, and unexpected changes in inflation cause movements in real wages, and hence unemployment. But that’s obviously much more true of NGDP than price inflation. Unexpected NGDP shocks clearly do drive changes in employment when wages are sticky. Again, price inflation reflects both AS and AD shocks.

So we have a world where the true model of the economy is all about NGDP and nominal wages. NGDP shocks in a country with sticky wages create business cycles. But we’ve weirdly decided to use an ambiguous intermediate variable—price inflation—which is sort of like NGDP and sort of like wage inflation. Because it is ambiguous, its causal role in the Phillips curve model can be interpreted in two radically different ways, as either the cause of business cycles or the result of business cycles.

If we dump the ambiguous price inflation from macro and replace it with the very unambiguous NGDP and nominal wages, we get a much clearer sense of what’s going on. Cause and effect are immediately obvious.

PS. I can’t even imagine what our undergraduates make of textbook macro. Taken as a whole, it MAKES NO SENSE. Inflation comes from MV=PY? Or does it come from having less “slack”? If you replace the textbook model with NGDP and wages, everything suddenly becomes clearer. Monetary policy (including velocity shocks) drive NGDP. Real GDP fluctuations are caused by NGDP fluctuations interacting with sticky wages. And once you have growth rates for NGDP and RGDP, then price inflation is simply the difference.

PPS. Sorry for being so long-winded. I wish I could write like Mankiw, a man of few words. Or zero words in the post I linked to, to be precise.

PPPS. If only I could write my own textbook. Oh wait, I did.

. . . If only I could write a textbook without worrying about sales figures.

Tags:

23. June 2019 at 10:01

Are you going to write your “dream” macro book for a small audience? It doesn’t have to be an actual textbook, it could be a semi-popular book.

23. June 2019 at 11:43

What I recall from intro to macro and intermediate macro as an undergrad was that nothing made sense so I should just memorize the textbook causes for curve shifts and regurgitate them on the exams. IS-LM seemed useless (I took intermediate macro in the fall of 2010).

It wasn’t until your posts about AD as a function of money supply/demand and sticky wages causing the upward sloping SRAS that macro started to make sense to me.

23. June 2019 at 12:30

AC, Yes, I’ve already written the first draft, and am revising based on comments.

Thanks Garrett.

23. June 2019 at 14:36

“1. Falling inflation causes higher unemployment.

2. Higher unemployment causes falling inflation.”

Or maybe inflation and unemployment are both the effects of the same underlying causes. Tight money policies cause inflation to fall while causing unemployment to rise, while easy money policies cause inflation to rise while also causing unemployment to fall.

23. June 2019 at 15:12

Scott,

Of course, you could write your own textbook 100% your way, if you’d be willing to essentially just donate your effort or market it unconventionally as you blog. Your readers could help on social media.

You could make it available as a free or very low cost e-book, adding a moral dimension to your marketing. “Here’s the world’s best, easiest to understand econ education content at the most economical price. Text books shouldn’t be expensive.”

While traditional textbook publishers may know more about what approaches econ professors are demanding, they don’t necessarily know much about spurring demand unconventionally, like marketing to students. And some of that would be against their interests anyway, as it would cut them out.

At least from my lay, outsider perspective, colleges seem much more sensitive to influence from students than they were when I attended college too many years ago. Enough students demanding low cost textbooks would likely get their way, to a degree.

And even if you couldn’t sell a textbook successfully that way, you might be able to sell a guide for students to help them understand their econ material better.

Perhaps I’m naive, but I think the future will see an extreme rise in the celebrity professor, who will teach many more students at once, facilitated by technology, and will increasingly vertically integrate in response to increased competition among such celebrities. Over time, even the number of TAs will diminish, as the better teaching methods and more automation are widely applied.

I think the gulf between research and teaching professors will grow, to the benefit of both teaching and research. The awkward, cautious, quiet academic teacher will be replaced by marketable personalities.

23. June 2019 at 15:29

Or falling inflation is caused by tight money which also causes higher unemployment. Think of the lessons from the broken windows fallacy and Humes on money. What happens when people stop spending? What happens when money is taken out of the supply?

23. June 2019 at 16:23

I think this post is correct. If one wants to look for a Phillips Curve, then connecting nominal wages to in GDP is probably the best approach.

The Phillips Curve is probably of much less utility than before. For example, presently the United States has deflation in unit labor costs due to even modest productivity gains. (By the way, productivity gains seem to follow sustained economic expansions.)

Also, much inflation in the United States is caused by housing costs which are caused by property zoning and other impediments to building. Kevin Erdman regularly posts that the CPI course and housing is running at about 1%. Housing costs are rising at about a 3% annual rate.

Thus, the Orthodox macroeconomics profession tends to look at the wrong things. The Federal Reserve’s Beige Books, for example, exhibit a squeamish hysteria about Labor shortages). Today, among macroeconomists, there should be prominent discussions about how to reduce housing costs and also perhaps how to sustain an economic expansion that results in productivity gains.

Given that labor markets still exhibit a lot of slack, due to adults re-entering the labor force (adults not previously in the labor force are taking most of the new jobs, while large fractions of currently employed respond they want more to work more hours) discussions about Labor inflation are premature and unproductive.

Besides all that, I can imagine no better tonic for America then a couple generations of very tight labor markets (well, unless it be a total abolition of property zoning).

23. June 2019 at 16:47

I like to think of it in terms of multiple cointegration between NGDP, employment, and nominal wages.

23. June 2019 at 17:32

The post is very clear and informative, no apology required.

23. June 2019 at 21:14

Mike, Yes, that’s my view. But I see NGDP as part of the mechanism. Tight money causes falling NGDP, which then causes lower inflation and higher unemployment.

Michael, You said:

“Of course, you could write your own textbook 100% your way”

I’d have no ability to do that on my own. A new textbook costs over a million dollars. Do you seriously think I’d do that as charity? What would my wife say?

24. June 2019 at 03:03

“Of course, you could write your own textbook 100% your way”

I’d have no ability to do that on my own. A new textbook costs over a million dollars. Do you seriously think I’d do that as charity? What would my wife say? — Scott Sumner

You wife would talk to you about it? Mine would first raise a cleaver….

But…I think the whole idea of a textbook industry is hopelessly outdated.

Surely Scott Sumner and some like-minded colleagues could produce an excellent online macro text. Yes, it would be charity, or if you made it right-wing enough, you could get a grant from the Kochs or someone.

I would contribute a page or two on property zoning and housing costs, and the ramifications thereof.

24. June 2019 at 08:51

Scott,

Yes, it may cost a lot of money to publish traditionally, but some self-publish ebooks and try to market at zero financial cost. There are free econ textbooks online.

24. June 2019 at 10:35

Interestingly enough, the relationship in Mankiw’s chart breaks down in the pre-1985 period. I suspect the reason it is so pretty is that inflation expectations are relatively more stable over this period. Any regression over the post-war history would need to take into account the impact of changing inflation expectations or how unanticipated inflation affects real wages.

24. June 2019 at 12:00

Michael, I’m not going to devote years of my life to sell a few dozen books to students that never read them.

John, That’s right, changing inflation expectations

24. June 2019 at 17:56

Scott,

That’s understandable. You could try, but don’t really have the attention-seeking personality, drive for money, or personality otherwise to try to make something like that work. It would take someone like Tyler Cowen who was hyper-interested in profit, more entreprenurial, and more into self-aggrandizement. He seems happy being an academic and just providing a lot of free, cleverly conveyed econ education, which probably helps his for-profit textbook sales, but isn’t going to launch an independent, for-profit alternative to traditional college education.

24. June 2019 at 18:11

I just have this feeling that college kids won’t be paying the prices for materials such as books that they do today in 20 years.

25. June 2019 at 02:03

Speaking of self-published books, Jason Smith just released his second:

https://www.amazon.com/dp/B07T8T9G93/ref=as_li_ss_tl?&linkCode=ll1&tag=arandomphysic-20&linkId=1eb9647354ffde791afaa9392f8dec4d&language=en_US

It is a very interesting short read, even if you don’t buy his general outline for an alternative macro model. Understanding his information equilibrium econ model isn’t necessary to read and understand most of his arguments in the book. They are based on economic “seismograms” which list many metrics in the history of the US since 1948, with some surprises in terms of which changed first before various economic shocks.

It’s a lot of food for thought, if nothing else, and the commentary on social changes in America over the period is really good.