The rising dollar will not impact US growth

Here’s a new headline from the Washington Post:

U.S. economy’s surprise risk: The dollar’s surge could weaken growth

The surging value of the U.S. dollar promises new bargains for American consumers and travelers but also presents big threats to the U.S. economy “” in a trend that is shaping up to be one of the most unexpected and significant factors driving the global economy this year.

This is wrong, one should never reason from a price change. There are 4 primary reasons why the dollar might get stronger:

1. Tighter money in the US (falling NGDP growth expectations.)

2. Stronger economic growth in the US.

3. Weaker growth overseas.

4. Easier money overseas.

In my view the major factor at work today is easier money overseas. For instance, the ECB has recently raised its growth forecasts for 2015 and 2016, partly in response to the easier money policy adopted by the ECB (and perhaps partly due to lower oil prices—but again, that’s only bullish if the falling oil prices are due to more supply, not less demand–see below.) That sort of policy shift in Europe is probably expansionary for the US.

However NGDP growth forecasts in the Hypermind market have trended slightly lower in the past couple of months. Unfortunately, this market is still much too small and illiquid to draw any strong conclusions. Things will improve when the iPredict futures market is also up and running, and even more when the Fed creates and subsidizes a NGDP prediction market. But that’s still a few years away. Nonetheless, let’s assume Hypermind is correct. Then perhaps money in the US has gotten slightly tighter, and perhaps this will cause growth to slow a bit. But in that case the cause of the slower growth would be tighter money, not a stronger dollar.

Does that mean exchange rate changes are never informative? Not at all. When we observe exchange rates change in response to monetary policy actions, then we can pin down the direction of causality. Thus the dollar fell 6 cents against the euro on the day QE1 was announced in March 2009. We’ve also seen falls in the yen and euro on QE announcements in Japan and Europe. But you need to know why the exchange rate has moved before drawing any conclusions about causality.

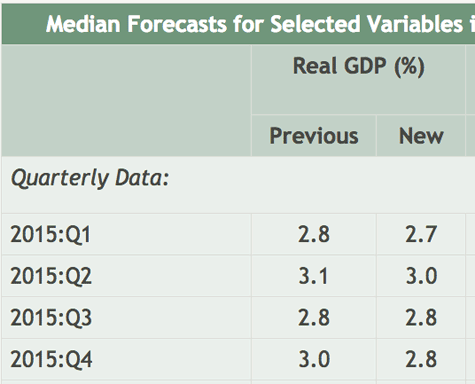

As an aside, late last year there was talk that the huge fall in oil prices would be “like a tax cut,” boosting growth in the US. I was skeptical, and still am skeptical. It’s worth noting that falling oil prices did not raise the consensus forecast for RGDP growth during 2015, indeed forecasts fell slightly between last fall and early 2015, “despite” the huge plunge in oil prices:

Tags:

12. March 2015 at 06:51

Well…I think if the dollar gets too high perhaps Swiss lite situation can develop. That would suggest a lower RGDP.

The solution is easy: print more money. In fact, I advocate the Fed print more money right away, as they are risking financial instability and unintended consequences and rapid accelerating deflation otherwise. And unforseeable bad things too.

12. March 2015 at 06:53

One of the problems of being the reserve currency, is there are impacts everywhere.

1) Since the dollar is mostly gaining on the Euro & oil states and not the yuan & ruppee, the impact on jobs is small and might even be a net positive. (At this point, is the Chinese yuan overvalued? And is Chinese simply following Japan’s 1980s economy?)

2) I am with Matt Yglesias the biggest problem with the Euro it is political decision not an optimal currency area. So Euro is now undervalued because of Greece.

3) At this point, I almost want the Fed to raise rates to .50% just get the market’s (near panic) reaction out of the way.

4) I still think the US economy weirdly counteracts the globe. The worse the global economy gets, the better the US economy goes and visa versa. Right now we are sitting on four global crisis areas, Ukraine Sorta Civil War, South Euro Depression, Middle East ISIS, and the coming Valenzuela/Argentina bust. So investors and corporations are moving back to US growth compared to the 2000s when they focusing on global growth. (Notice China & India avoiding the drama are doing relatively well.)

12. March 2015 at 07:25

The yen stigma: It can only appreciate!

https://thefaintofheart.wordpress.com/2015/03/12/central-bankers-and-comfort-zones/

12. March 2015 at 08:10

As an aside, late last year there was talk that the huge fall in oil prices would be “like a tax cut,” boosting growth in the US.

That might have been true in the pre-fracking era when net imports were enormous, but now the US is the #1 oil producer.

This graph is insane.

12. March 2015 at 09:22

@TallDave,

It’s still like a tax cut, just a smaller one. The U.S. is still a net importer of oil.

12. March 2015 at 09:34

[…] Sumner says much of what I would, namely don’t reason from a price change. I would make a related point, but in reverse, about the now-weaker euro. Yes, it does in the […]

12. March 2015 at 09:46

[…] Sumner says much of what I would, namely don’t reason from a price change. I would make a related point, but in reverse, about the now-weaker euro. Yes, it does in the short […]

12. March 2015 at 09:49

[…] Sumner says much of what I would, namely don’t reason from a price change. I would make a related point, but in reverse, about the now-weaker euro. Yes, it does in the short […]

12. March 2015 at 10:04

Scott, I’m sorry to hijack this comment section with something off-topic, but in case you haven’t seen it already, check this out: https://medium.com/bull-market/how-does-qe-work-a-picture-worth-a-thousand-words-7fe0fca67ac4

I’m wondering what you think of it. I’m not sure what to say except that this phenomenon is super weird and is only compatible with a ridiculously illiquid eurozone sov debt market.

12. March 2015 at 11:04

Ben, The Fed does seem behind the curve.

Collin, The euro is still too strong

David, But is there any reason to believe a tax cut would boost growth?

Dan, I don’t see the purchase of Greek bonds as QE, it seems more like a bailout.

12. March 2015 at 11:20

[…] argues that the strong dollar will not impact US growth. In response to a Washington Post story, he writes: This is wrong, one should never reason from a price […]

12. March 2015 at 11:29

Scott,

was just responding to TallDave’s comment about the import part. But, on basic economic grounds, yes. The price of an input falls due to an increase in world supply, and output rises. During that transition, growth is higher.

12. March 2015 at 11:35

Scott,

On the boosting growth point, what corrections might be needed for an argument that for most of the U.S. economy, oil is an input, and so a reduction in the price of oil lowers their costs, while for only a small segment the U.S. economy, oil is an output, so a reduction in the price of oil lowers their revenues?

12. March 2015 at 11:41

As the U.S. is a very large oil importer, and the demand for oil is rather price-insensitive, falling oil prices should strengthen the dollar, just like they weaken the ruble.

12. March 2015 at 11:45

“I’m not sure what to say except that this phenomenon is super weird and is only compatible with a ridiculously illiquid eurozone sov debt market.”

-What’s super weird about it? Increasing demand for bonds lowers their yield, correct?

12. March 2015 at 12:45

[…] Will the Dollar Impact US Growth?, by Tim Duy: A quick one while I wait for my flight at National. Scott Sumner argues that the strong dollar will not impact US growth. In response to a Washington Post story, he writes: […]

12. March 2015 at 13:07

David, Yes, if due to more supply. But then it’s the extra supply boosting growth, the price is just a side effect.

Taimyoboi, The US gains in terms of trade. But the implications for growth depend on why the price fell. The oil price decline of 2008-09 did not lead to higher growth forecasts.

E. Harding, True, the but eurozone is an even bigger oil importer, and their currency has fallen sharply. My view is that it doesn’t have a big effect on the value of a currency, but yes, other things equal it probably strengthens the currencies of oil importers.

12. March 2015 at 13:57

Scott,

Thanks. Excuse some ignorance here, but what does it mean to say the US gains in terms of trade. Is that just saying that on net, most people in the US benefit from a lower price of oil (because most of our oil is imported, and most people pay to use, as compared to some people who earn income to export it)?

It seems like the 2008-2009 period is a different creature from today. Might the fact that there was a recession in 2008-2009, and what appears to be an increase in supply driving down prices today, give us a clue as to what we would expect the effect to be?

12. March 2015 at 14:06

@Scott,

Yes, if due to more supply. But then it’s the extra supply boosting growth, the price is just a side effect.

Exactly. The way supply gets into the system is by causing the price to drop. I’m following your rule, which is a good one, of not reasoning from a price change.

12. March 2015 at 14:11

@Scott,

Remember, Scott, that you asked me “But is there any reason to believe a tax cut would boost growth?” I answered yes. Now you seem to have changed the subject. But it does sound as if we have agreement that a tax cut would boost growth.

12. March 2015 at 14:35

Low oil prices are certainly helpful to the oil-consuming sector, as they allow in increase in oil consumption to the extent low prices are the result of a supply surge–which is the case.

We would expect, for example, to see a resurgence in vehicle miles traveled (VMT, which in fact was up 5% December compared to the same month previous year. That’s a huge advance. (See my earlier forecast on my blog.) Remember when they told us Americans had fallen out of love with their cars? Dead wrong.

In any event, VMT often tracks closely to GDP, and I think it will this year, too. I will happily take the ‘over’ on the GDP forecasts*. Europe will be substantially stronger than expectations, too–current oil consumption data is already telling us that.

Q2 may well prove the turning point.

I’ll be guest-teaching Steve Levine’s class at Georgetown on the 17th. The topic will be a variant of my Oil Markets Outlook. It’s already been quite a tour: Miami (three weeks ago), Houston (last week), San Francisco (yesterday).

Wouldn’t hurt Mercatus to invite me down sometime.

12. March 2015 at 15:18

David, No, I don’t think a tax cut would boost growth, unless it involved a cut in marginal tax rates. If it was just a tax rebate, or something like that, I don’t think it would have affected growth. That’s why I made the earlier comment. But I agree that a price drop due to more global supply of oil would boost growth.

On the taxes, let me put it this way. Tax cuts can boost growth, but not because they put more money in people’s pockets (more AD). They just move money around. The Fed controls how much money is in people’s pockets.

Taimyoboi, Better terms of trade occur whenever prices change in such a way that your exports are able to purchase more imported goods than before. Higher export prices or lower import prices. Thus recently our exports of airliners and soybeans buys more imported oil than a year ago.

The answer to your second paragraph is yes.

Steven, You said:

“Q2 may well prove the turning point.”

Replace the “2” with an “E” 🙂

12. March 2015 at 16:38

E. Harding,

It’s weird because rates shouldn’t come down for JUST those bond issues the ECB is buying. Just to make up an example, if the ECB is buying Greek ’22s, yes, their yield should come down, but we would also expect the yield on Greek ’21s, ’23s, etc. to come down even if the ECB isn’t buying them, because those bonds are all very close substitutes for one another. You could almost say an arbitrage opportunity has presented itself. Get out of the Greek debt that has tightened and get into the debt that has stayed wide. But why didn’t people take advantage of it?

12. March 2015 at 16:39

Sumner wrote:

“On the taxes, let me put it this way. Tax cuts can boost growth, but not because they put more money in people’s pockets (more AD). They just move money around.”

And poof goes market monetarism.

If more money in people’s pockets doesn’t boost growth, then more money in people’s pockets post-2008 (which is what Sumner has been claiming would have lessened the decline, meaning it would have been followed by higher growth) would not in fact have boosted growth from what it was.

Oops.

12. March 2015 at 17:41

No, I meant “Q2”.

12. March 2015 at 18:35

@MF: “If more money in people’s pockets doesn’t boost growth”

As usual, you don’t understand, and you take quotes out of context. You left out the very next sentence, which was the most critical part of Sumner’s answer: “The Fed controls how much money is in people’s pockets“. (In other words, if the Fed is targeting AD, then tax cuts don’t put more money in people’s pockets.)

You know, I used to think you were a smart guy, but evil, deliberating misrepresenting what other people say. But sometimes I wonder if I’ve overestimated you. Maybe you’re just dumb.

12. March 2015 at 19:41

There are not “four” factors affecting Fx, but more like forty. The excellent Barron’s guide to economics, Table 161. Factors Affecting Value of Dollar, lists: demand for US exports, physical assets, financial assets, US demand for foreign imports, foreign physical assets, foreign financial assets, US price level relative to foreign price level (if US price increase, relatively, US dollar depreciates, and vice versa), US interest rates relative to foreign (same relationship), and, country growth rates (same, though Barron’s has a typo here), and finally, last but not least (China, Japan), government intervention; see more online at: http://www.economicshelp.org/macroeconomics/exchangerate/factors-influencing/ (as you can see, it’s not as simple as Sumner thinks).

12. March 2015 at 20:07

@Scott,

Right, Scott. I assumed all along that the discussion was about marginal tax rates.

12. March 2015 at 21:19

Off-topic: Arthur Burns, despite his flawed tactical vision (he recommended wages and price controls to Nixon) was a strategic genius. Note his brilliant intuition. From: “Arthur Burns and Inflation” by Robert L. Hetzel – Consistent with Burns’s emphasis on using microeconomic tools was his de-emphasis of the direct, aggregate demand effects of macroeconomic (mone- tary and fiscal) policy. His 1957 book Prosperity Without Inflation conveys this theme, emphasizing as it does the near impotence of monetary policy. Burns held the conventional view of monetary policy as working through the cost and availability of credit. Moreover, according to Burns, the cost of credit has only a minimal effect on the decisions of businessmen, and financial innovation makes it hard for the Fed to control the availability of credit. Burns (1957, p. 46)

This last sentence is important, and known to historians (save Sumner): during boom times, banks will find a way to expand the money supply–money is neutral–and you don’t need any central bank to inflate the money supply. Similarly, during busts no amount of Fed pump priming or reckless money printing will induce business to take out loans if they don’t want to. All such money printing does is potentially lead to future inflation.

13. March 2015 at 01:13

Don Geddis:

Ah, the resident psychopath is still smarting.

“As usual, you don’t understand, and you take quotes out of context. You left out the very next sentence, which was the most critical part of Sumner’s answer: “The Fed controls how much money is in people’s pockets”. (In other words, if the Fed is targeting AD, then tax cuts don’t put more money in people’s pockets.)”

Haha, no. That sentence does not do what you claim it does. Sumner’s argument was very specific. He said that “more” money in people’s pockets does not boost growth. He is making a comment about a change in the money supply that people own. Notice the next sentence that YOU left out, which is that more money does not boost growth because “They just move money around”. The content of that comment makes my interpretation correct. Note money does not, according to Sumner, boost growth because “people just move it around.” The only thing that happrns is that money just “moves” from A to B, and that’s it.

Now back to the part you falsely believe makes the above wrong, the point that “The Fed controls how much money is in people’s pockets”. What Sumner is saying is that a country will not experience growth if it goes from a communist system where the state taxes and controls 100% of all spending on capital goods, with money “just moving” from their left hand to their right hand, to a capitalist system where taxes are low, and individual homesteaders and free traders control most or all of the spending on capital goods, with the caveat that total spending of government plus private market remains unchanged. For here, “money just got moved around”.

That is what he is effectively arguing.

But where you totally missed the point, which I guess was likely in your case, the connection to how it contradicts NGDPLT, is that more money in people’s pockets in its connection to growth, was always a theory about capitalist economies. NGDPLT never claimed, and in fact rejects, the notion that two economies eith equal NGDPs will have equal growth even if one of them is communist and the other capitalist.

MM will of course fall back on the “That is fiscal policy not monetary policy”, which is just another way of saying that MM cannot explain why growth would be higher in capitalism versus communism because it only deals with the total spending that it knows boost growth, which is money in private market participants’ pockets rather than statesmen pockets.

What that in turn means is that NGDPLT was and is really about the growth rate of money in market participants’ pockets, not in the pockets of capitalists plus state. MMs are compelled to admit that if starting next year NGDP was reduced in the private market by 90%, that growth would fall even if the state replaced that drop in private market spending with spending of its own.

Again, MM theory would sit back and say “This is not a monetary policy problem, it is a fiscal problem, since total spending remained unchanged. The Fed controls total spending, so market monetarists say the blame is the state, not the Fed.”

This is expert level handwaving. It wants to have it both ways. It wants to believe that more money boosts growth when the money is in market partipant’s hands, but at the same time, it wants to also believe that it won’t boost growth if the increase in spending in the private market took place on the heels of going from communism to capitalism.

So what I said is the correct interpretation, as long as you don’t ignore the above implication. Sumner contradicted the fundamentals of NGDP when constrained to the context that always was, but did not admit, the case.

“You know, I used to think you were a smart guy, but evil, deliberating misrepresenting what other people say.”

No, you are only a priori convinced that I am evil, and that is why you want to have me murdered, and you are going out of your way not to understand the core premises of an argument being presented so as to ex post rationalize that a priori belief. It is what most psychopaths do. All I am doing is WRITING, and you are having a repeated series of intellectual and emotional meltdowns with bloodthirst.

You are evil, not me.

13. March 2015 at 04:29

David, But when people say lower oil prices are like a tax cut, they are referring to demand side effects. Many of the people saying that don’t even believe in supply side economics. They are thinking in terms of a lump sum tax cut.

Ray likes the worst Fed chair in history. Why am I not surprised?

13. March 2015 at 10:22

@ssumner – hahaha! I read your mind. I thought you would say that, since Burns was not a monetarist and in fact an anti-monetarist. Milt Friedman (in the paper I cited upstream) told Burns in 1957 that if he did not believe in monetarism, he should just directly proceed to control the economy (such as, presumably, wage and price controls), which in fact happened in Aug. 1971- ?74 (“In 1957 Milton Friedman wrote Burns a nine-page letter that criticized

Burns’s manuscript Prosperity Without Inflation for confusing monetary policy with credit policy … “). Yet, to give the devil (Burns) his due, notice from http://www.usinflationcalculator.com/inflation/historical-inflation-rates/ that the Nixon price controls from August 1971 worked fairly well from 8/71 to March of 1973 (when fixed exchange rates in the G-10 became floating, arguably allowing inflation to be imported into the USA), and then the Arab Oil embargo of late ’73 killed Nixon / Burns plan, which apparently was abandoned sometime in 1974. But it did ‘work’–at some cost–to taming inflation. Which is more than one can say about Friedman’s ‘indirect’ MM, which never works (even Volcker it is argued did NOT use monetarism to tame inflation in the early 80s). Further, we see today how MM is not working at the zero lower bound–why is that professor Sumner? Could it be the quantity theory of money is bogus due to changing velocity? That ‘animal spirits’ (a fudge factor, but befitting for a non-linear system like the economy) is the real driver of GDP? Hear Nobelian R. Shiller (from a speech): “Well, I’ve written several books on that. My latest is with George Akerlof is called Animal Spirits [2009]. … Animal Spirits is based on Keynes. He said that animal spirits is a major driver of the economy … I’m sure that Ben Bernanke and Austin Goolsbee are influenced by John Maynard Keynes, who was absolutely not a rational-expectations theorist…”). MM = bogus.

13. March 2015 at 10:24

Here is what’s on my mind: “Global consumer staples stocks hit by F/X worries”

http://seekingalpha.com/news/2352296-global-consumer-staples-stocks-hit-by-f-x-worries

It seems very possible that for global stocks like Nestle, Unilever and Colgate, the stronger dollar is harmful in the short-term but positive in the medium-term if the stronger dollar implies faster international NGDP growth. That’s a big “if,” however…..

13. March 2015 at 13:23

[…] the crashing euro to both Europe and the U.S. There are two posts from Scott Sumner worth reading, one here and one here. He argues that the U.S. economy isn’t going to be hurt by the strong dollar, […]

13. March 2015 at 22:10

The market is absolutely agog with speculation/concerns that US rates are about to go up. Removing the word “patient” or not is everything. Expectations are clearly biased towards the Fed doing that and then raising rates in June and/or September and/or December. The Eurozone has two years or more of QE ahead of it.

All this despite RGDP expectations for both blocs not looking too bad. Your US readers should stop harping on about a EZ economic crisis, it’s over. Unemployment is falling in most, many EZ countries now, even S Europe. Greece is just a noisy sideshow.

One huge currency bloc is tightening, the other is loosening – despite not dissimilar economic growth expectations. Result: strong currency movement between them. It’s not rocket science.

13. March 2015 at 22:20

Or, in response to your headline, you are right the rising dollar won’t impact US growth, but rising rates expectations will.

13. March 2015 at 22:39

… if caused by the Fed acting ahead of NGDP growth expectations, which it sooooo obviously would be.

14. March 2015 at 03:25

“It’s not rocket science.”

Well said James, well said!

14. March 2015 at 05:38

Ray, Yes, IMPORTED oil prices cause US NGDP to grow at 11% a year from 1971-81, why didn’t I think of that?

James, The crisis of the 1930s didn’t end when the recovery began, and I’m not certain that Europe’s crisis is over, although I certainly agree they are growing at a slow rate.

The US may be tightening, but so far I don’t see a lot of evidence. You might be right, but I’d hold off any firm judgments until we have more data.

14. March 2015 at 09:33

Krugman comments on this post: http://krugman.blogs.nytimes.com/2015/03/14/a-note-on-dollar-strength/?_r=0

14. March 2015 at 13:17

The historic move in USD vs EUR is some sort of data point that needs some interpretation. Reasoning from it is dangerous I agree, but I was trying to help explain what is driving it.

Maybe financial markets positioning means little, but traders and investors are heavily buying USD and selling EUR, driving the currencies up and down. They are confidently arbitraging the spread in bond yields, 2% vs -0.2%.

And they are made bolder by the expectation the Fed will at worst hold rates steady but most likely raise them as the real money US yield curve shows. While the ECB is expected to at worst hold rates steadily negative or even be forced to go more negative to flush out the bonds it is set to buy.

This latter because the market sees that the ECB’s task practically is tougher than was the Fed’s or the BoE’s, or is the BoJ’s, as it has to buy at a level equal to 2.5x Eurozone net government bond issuance.

Of course, I agree that this all a bit of a farce as QE is but a poor substitute for NGDP Targeting, or even flexible inflation targeting.

14. March 2015 at 14:01

“you are right the rising dollar won’t impact US growth, but rising rates expectations will.”

I have to agree with James In London. The pattern of massively divergent monetary policies in the US and Europe is harmful.

How did we go from 2011, where we had QE in the US while the ECB was raising rates, to 2015, where we will have QE in Europe for years, while the Fed is expected to raise rates 6 times over by the end of 2016.

14. March 2015 at 14:04

And I also think that as the EZ recovery gains strength then these trades will unwind and EZ bonds will drop in price/yields rise. But that is not driving markets right now, liquidity effects are still winning out.

14. March 2015 at 14:04

ssumner wrote:

“I’d hold off any firm judgments until we have more data.”

Uh, oh. Assimilated by the borg; now we know Scott is quietly campaigning for a seat of the FOMC.

😉

15. March 2015 at 04:32

Scott,

You’re quite right that the ECB’s buying of Greek bonds is not QE, but a bailout. The ECB has been explicitly sterilizing the effects in terms of expansionary policy.

15. March 2015 at 05:34

Thanks Foosion.

James, Monetary policy is certainly part of it, but what puzzles me is what sort of new information the markets have received in recent weeks.

Steve, What evidence do you have that monetary policy in the eurozone is more expansionary than in the US?

James, I doubt we’ll see significantly higher eurozone interest rates for a very long time.

Steve, Recall that I take my lead form the markets. Here’s my question—what market data do we have that monetary policy has significantly tightened? Exchange rates—I’ll grant you that. But anything else? Stocks? NGDP futures?

Don’t get me wrong, I think they’ve tightened a bit, and that policy is too tight to hit their goals (best as we can ascertain the goals.) So I’m not quite yet in the Fedborg.

Thanks Scott.

15. March 2015 at 08:02

according to investopedia, tighter money means higher interest rates, or banks are less willing to lend

so, your 1st point is, i think, economy is slowing down, and investors, perceiving more risk, are willing to lend only at higher rates ?

and foreigners are willing to invest in a country which has high rates cause it is slowing down ?

strong economic growth is opposite to point 1….so the dollar can rise when the economy slows and when it speeds up ?

it seems like there are multiple, contradictory reasons; how do you sort them out quantitatively ?

15. March 2015 at 08:15

The new information is the probable removal of “patient” from the Fed statement in the March FOMC. These things are often leaked in advance to test market reactions. Jin Hilsenrath at the WSJ is widely seen as the chief conduit for these authoritative unofficial stories. Is the FOMC kite-flying new data? Yes. A second data point would be the actual removal of the word. If you read the financial press speculation over the FOMC March statement is dominant. Marcus Nunes is on the ball, as usual.

https://thefaintofheart.wordpress.com/2015/03/11/key-word/

15. March 2015 at 08:24

ezra, You said:

“according to investopedia, tighter money means higher interest rates, or banks are less willing to lend”

Remind me to never read Investopedia. Higher rates are not tight money, and less willingness to lend is tight credit, not tight money.

You said:

“so, your 1st point is, i think, economy is slowing down, and investors, perceiving more risk, are willing to lend only at higher rates?”

No, I don’t believe that. Slower growth tends to reduce rates over time.

James, You may be right, but it doesn’t seem like that’s the whole story. If something major was going on wouldn’t it show up in the stock market?

15. March 2015 at 15:03

When it comes to Forex trading you really never know what can be the possibility as rising dollar can have serious impact on US growth but as trader we really don’t mind any situation as long the profit keeps coming so that is really what makes it so great this business and having a superb broker like OctaFX at my service makes it even better as they have outstanding analysis service where I get perfect updates about all currencies and can follow it without any problem.

16. March 2015 at 00:12

You are right re: the stock market. But, as you said elsewhere, it is still partly driven by the very low discount rates on future profits, and its obverse that it is ever more highly valued on non-discount related metrics. NGDP Forecast proxies don’t look good.

http://www.bloomberg.com/news/articles/2015-03-13/surprise-u-s-economic-data-most-disappointing-in-the-world

https://www.frbatlanta.org/cqer/researchcq/gdpnow.cfm

http://efficientforecast.com

http://www.multpl.com/shiller-pe/

16. March 2015 at 02:52

And the Citigroup Economic Surprise Indices for USD and EUR have diverged too.

https://www.citibank.com.cn/homepage/en/pdf/Financial_Market_Analysis.pdf

(Top right chart)

EZ economic strength should eventually lead to a strengthening in the Euro, sure, but these are very early days in EZ QE. The liquidity effect is stIll dominant while the ECB establishes its reflationary credibility.

16. March 2015 at 04:56

[…] Duy is having a debate with Scott Sumner, who insists that the strong dollar won’t hurt US […]

16. March 2015 at 06:19

James, That’s suggestive, but I’d need more data to be convinced the Hypermind forecast is wrong.

16. March 2015 at 06:19

Last year’s first quarter was also weak.

16. March 2015 at 13:38

One quarter’s NGDP or RGDP is often really no better as a guide to underlying nominal growth than a range of other factual data from the period. The Atlanta Fed should be encouraged in their quest for GDPNOW data, it’s quite powerful. Perhaps their innovation could be extended to GDP futures?

The Bloomberg and Citi indices are more about changing expectations, looking for data surprises. The market is constantly adjusting its monetary policy expectations based on all this data. And that interpretation is partly what’s driving the USD. But, hey, you know all this.

The FOMC should definitely be looking at all these data points in the absence of those futures. Waiting for actual, sometimes odd, quarterly GDP figures seems terribly old-fashioned in today’s world. What’s puzzling is your insistence on more data.