The Phillips Curve in the US and Japan

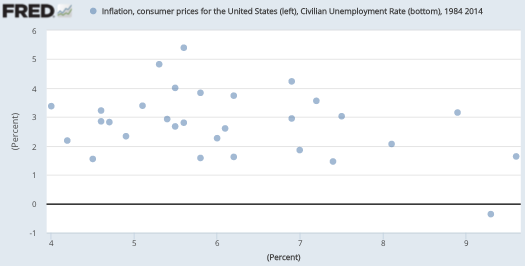

Over at Econlog, I have a post on the Phillips curves for Hong Kong and Singapore. That’s the one to read, if you only have time for one post. Here’s the Phillips Curve for the US:

Notice that there is almost no correlation. With the exception of 2009, when prices fell slightly and unemployed soared, it seems like monetary policy in the US was pretty good after 1984. Supply and demand shocks roughly offset, leading to almost no correlation. This graph is one of the best arguments against the gold standard.

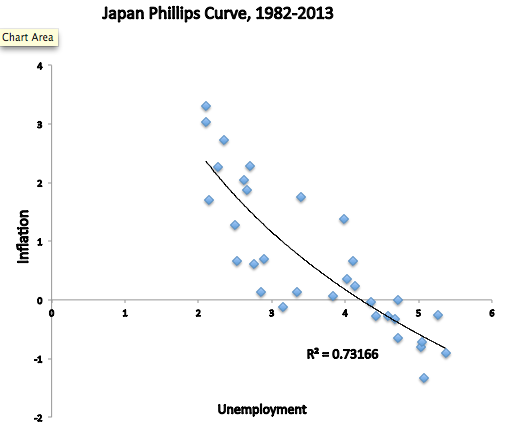

A clearly observed Phillips curve is a sign of procyclical monetary policy, which is poor quality monetary policy. What does a classic Phillips curve look like?

Like Japan:

Japan has a low natural rate of unemployment, and a more flexible labor market than the US. But don’t be fooled by that. The specific role of monetary policy in Japan has been destablizing, as evidenced by the clear Phillips curve relationship. They can and should do better.

This post might be clearer after reading the Econlog post.

Tags:

17. April 2016 at 05:50

Apologies, but no discussion of Japan’s Phillips curve is complete without a reference to this remarkable paper.

17. April 2016 at 05:54

Ironman, Yes, How could I have forgotten that one. I’ll bet the similarity is far more “statistically significant” than 50% of empirical economics papers in leading journals.

17. April 2016 at 06:08

“This graph is one of the best arguments against the gold standard.”

goldbug = someone who is not willing to even consider anything that does not confirm the world must function under an economy based on an ugly yellowish metal. It’s like discussing “creation” with a bible thumper.

17. April 2016 at 06:21

Scott, a few years ago I had “expanded” the “Geography determines the Phillips Curve” idea:

https://thefaintofheart.wordpress.com/2012/07/20/seven-years-on-things-still-look-the-same/

17. April 2016 at 06:51

I don’t remember reading that Japan has a more flexible labor market than the U.S. How does lifetime jobs for most result in a flexible labor market?

17. April 2016 at 07:05

Derivs, Barbarous relic.

Marcus, Amazing.

Jim, It doesn’t, but somehow they have a very low natural rate–that’s what I meant. Perhaps other aspects are very flexible–remember that most jobs are not protected by the lifetime employment. Or perhaps there is mismeasurement in Japan. Remember that Trump pointed out that America actually has 42% unemployment, so you never know!

17. April 2016 at 08:03

Japan’s flexible labor market led to a range of unemployment of only about 3% (2-5) compared to about 5% (4-9) for the US. The range of inflation for both was about 4% with Japan’s middle rate about 2% lower. With flexible labor markets, does monetary policy even matter? Without sticky wages (and prices), isn’t money neutral?

17. April 2016 at 09:01

I also don’t see how the Japanese labor market would be more flexible but okay. Let’s assume it is. Somehow.

17. April 2016 at 10:13

Well, maybe Japan doesn’t have a war on the poor working schlubs, the way we do, say;

http://www.sfgate.com/bayarea/article/SF-to-require-Lyft-Uber-drivers-to-obtain-7250137.php

‘For the first time, San Francisco is going to require the 37,000 Lyft and Uber drivers who work in the city seven or more days a year to obtain a business license.

‘City Treasurer Jose Cisneros wouldn’t fully explain why he is now requiring the license, which will cost drivers $91 annually, when the companies started operations years ago.’

I predict the next shoe to drop will be all the surrounding towns to follow suit. Then the Uber drivers may have to have a dozen or so licenses to be licenses in a dozen or so localities in order to earn a living transporting their fellow man.

‘I’m from the government…and I’m here to make things as difficult as possible.’

17. April 2016 at 11:23

Scott

Im a bit surprised you ran inflation against unemployment as opposed to wage growth against unemployment. I enjoyed your post here which I very much agreed with. http://www.themoneyillusion.com/?p=25583

“Simple, Williamson trashes the American version of the Phillips curve, the one using inflation and unemployment. As you may know I view inflation as an almost worthless concept, which does more to confuse than enlighten.”

17. April 2016 at 15:03

“This post might be clearer after reading the Econlog post.”

I haven’t read your Econlog post yet. But I thought what you said here was very clear – especially after you pointed out that the graph for Japan demonstrates that its monetary policy is procyclical.

17. April 2016 at 17:01

Speaking about mismeasurements, for those curious about the employment rate for working age people in either the US or Japan, according to the latest OECD data (Feb. 2016) it was 69.3% in the US and 73.9% in Japan. That is, people aged 15-64 who are in employment.

https://data.oecd.org/emp/employment-rate.htm

17. April 2016 at 19:06

BC, It doesn’t matter as much. See my Econlog post, which discusses an even more flexible labor market.

Christian, Japan seems to have a lower natural rate of unemployment, if we can believe the figures.

Patrick, That’s depressing.

Aubrey, The US Phillips curve tells you why I’m not a fan. It’s not that the theory never works, but rather that it’s not reliable.

Thanks Gordon.

HW, Thanks for the info.

17. April 2016 at 19:14

@scott

Regarding the flexibility of Japan’s labor market, I would say.

1. 15 to 20 years ago, Japan had a very inflexible labor market in many if not most sectors of the economy.

2. Since then, slower economic growth combined with the difficulty of terminating full time employees and the high social insurance premiums paid by firms for their full time employees, there has been a dramatic increase in the percentage of part time workers. I’d say probably something like an increase from 25% to 40% of the labor force over the last 20 years.

3. This has made the labor force significantly more flexible than before but still much less flexible than in the U.S.

18. April 2016 at 04:48

‘Patrick, That’s depressing.’

Yes, it is, and I have lots of such stories. I know of people who have given up businesses due to the headaches that petty functionaries have erected in pursuit of their own narrow interests. Have my own, in fact.

‘Under capitalism, man exploits man. Under socialism and liberalism, the reverse is true.’

18. April 2016 at 07:06

Perhaps the high employment numbers in Japan are all about culture; grossly underutilizing women (hence not counting them in the labor statistics), a very inefficient service/retail sector, and a fairly efficient manufacturing/export sector that employs a high percentage of males. We don’t seem to understand what works or doesn’t work in our own country, why do you think we will have deep insights to an entirely different one?

Which brings to mind, what the heck is the libertarian/conservative obsession with Singapore? Why would we be looking at a small city-state with an entirely different government, history, and culture for ideas that would be applicable to a vast country with an entirely different development path? I saw Singapore being used as a model for health care reform by people who clearly had very little understanding of the actual Singapore health care system. It seems to me we should first look to similar countries (like first Canada, then Australia, then the island nations of New Zealand and England) for ideas to emulate or cautionary tales to avoid before looking at little city-states.

18. April 2016 at 08:03

dtoh, Thanks for that info.

Patrick, I agree.

Jim, Women are counted in Japan, and I believe their labor force participation is higher than you’d think. Regarding models, we should look at that works best, regardless of where it is. But I agree that we should not blindly copy smaller countries, as there are many real world complexities that make one system difficult to transfer to another. For instance, it would be almost impossible to transfer the UK health care system to the US.

18. April 2016 at 08:29

It seems as if you’re asserting a cause and effect relationship based on very little data or even a direct causative link. You’re saying that inflation/unemployment being uncorrelated implies good monetary policy and vice versa. There are only like a million other variables that might have something to do with what you’re seeing in those graphs, no?

18. April 2016 at 09:33

You are correct, women labor force participation rates in Japan have converged with U.S. rates. In 2014 sixty-four percent of working-age women in Japan were employed, compared to 63 percent of American women

18. April 2016 at 09:39

Are we to infer that US monetary policy was something close to good, or at least sufficiently countercyclical, between the period of 1984 and 2014? Also, the 8 year period since the onset of the great recession hasn’t produced a textbook Philips Curve. How should that be interpreted through the lens of “They can and should do better?”

18. April 2016 at 10:11

Japan has a low natural rate of unemployment, and a more flexible labor market than the US. But don’t be fooled by that.

Since when has Japan been more flexible? Maybe the new generation of workers (under 35) but older ones definitely not. Although Japan has always had an extremely low natural rate of unemployment though. Looking at employment trends since the Great Recession, the main reason the Unemployment Rate has dropped so much are: 1) The labor force dropouts are slowly coming back (and many are not coming back) 2) Weekly jobless claims are at 40 year lows.

I remember one of best posts by Paul Krugman is the US economy has become very Un-COLA since the mid-1980s. Commodity prices can go up or down but the impact to the US growth and unemployment is minimal. That is really a new reality for the US economy which historically not been true. (I suspect most goods prices only have a small percentage of commodity costs.)

18. April 2016 at 11:46

Can someone connect the dots for me on how this relates to the gold standard? Not that I would favor a gold standard, just not seeing how this makes any particular case against it. What’s the idea, “the Fed is reasonably good at it’s job, so why outsource monetary policy to the commodity markets?”

18. April 2016 at 21:52

One other thing about the natural unemployment rate. They ask a different question in Japan. “Have you looked for a job in the last two weeks?” versus 6 weeks in the U.S. When they ask the same question, male unemployment in Japan goes up 60% and female unemployment doubles.

Old data, but I think it’s still true.

18. April 2016 at 23:27

An absurd post by Sumner, as implied by Justin Irving and dtoh above. Sumner reads the opposite of what conventional theory says: (1) Japan is more flexible than the USA, with JP’s aging population and ‘lifetime employment’ conventions? It is not. (2) Gold standard relates to Philips Curve? Hardly. (3) Philips curve is evidence of pro-cyclical and somehow bad monetary policy? It is not.

Money demand is largely endogenous to an economy and largely neutral. That Sumner sees patterns (and draws the opposite conclusions to most sane economists) is merely evidence of his ideological bias.

19. April 2016 at 00:26

A propos Japan.

A very good speech by BOJ governor Kuroda. Very strong phrasing in the end:

http://www.bis.org/review/r160418b.pdf

“QQE with a Negative Interest Rate” is a very powerful framework enabling the Bank

to pursue monetary easing by combining a negative interest rate with quantitative and

qualitative easing. The Bank will continue with “QQE with a Negative Interest Rate,” aiming to achieve the price stability target of 2 percent, as long as it is necessary for maintaining that target in a stable manner. It will examine risks to economic activity and prices, and will not hesitate to take additional easing measures in terms of three dimensions – quantity, quality, and the interest rate – if it is judged necessary for achieving the price stability target. It is probably no exaggeration to say that “QQE with a Negative Interest Rate” represents the most powerful monetary easing in modern central banking history. The Bank of Japan will achieve the price stability target of 2 percent for sure by making full use of “QQE with a Negative Interest Rate.”

19. April 2016 at 07:57

I wasn’t disagreeing with Scott. I actually just want someone to help me understand. My prior is that Scott is right.

19. April 2016 at 08:52

Andrew, For instance?

Dustin, “Good” is a relative concept. But other than 2008-09, policy looks relatively good, at least based on this diagram. By other criteria, the period around 2010-13 was also substandard.

Collin, I think Krugman is reasoning from price changes–it depends whether oil prices rise due to less supply (1974 and 1979) or more demand (2007).

Justin, Under the gold standard there was a strong Phillips curve relationship, which indicates poor monetary policy.

dtoh, Thanks for that info.

Ray, Try to sound funnier.

Julius, That sounds promising.