The PBoC and the Fed both lost credibility

The world’s two largest economies are facing a similar problem, a gradual loss of credibility in monetary policy. In China, the exchange rate is artificially fixed at too high a level for macroeconomic stability. The public recognizes this fact, and expects the Chinese government will eventually devalue. Not surprisingly, people are trying to get their money out of China before the devaluation occurs.

The problem in the US is different. Our government does not fix asset prices at non-equilibrium values. The Fed does peg the fed funds rate, but they do so by adjusting monetary policy tools, until the desired fed funds rate becomes the actual fed funds rate. So there is no disequilibrium in the sense of a shortage of fed funds, or a surplus.

But there can ben macroeconomic disequilibrium, if the fed funds rate is pegged at an inappropriate value. In recent weeks, Fed policy has lost credibility. In America this doesn’t show up as capital flight, but rather in terms of asset price movements:

1. The market is increasingly skeptical that the Fed will raise rates 4 times this year.

2. More importantly, the market is increasingly skeptical that the Fed will hit its long-term inflation objective.

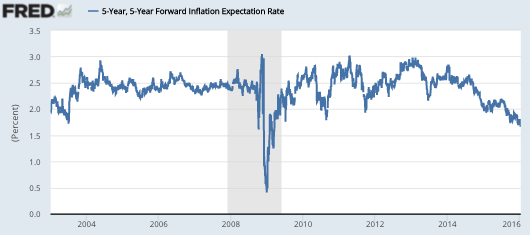

In the past I’ve often discounted the usefulness of TIPS spreads from the 5-year, 5-year forward market. This is the expected inflation rate from 2021 to 2026. The reason I tended to discount this data is that it was being used to claim there was no problem with inflation expectations. But a 2.3% 5-year, 5-year forward TIPS spread is a necessary condition for credibility, not a sufficient condition. Even if the public thinks CPI inflation will eventually return to 2.3% (or 2% PCE inflation), there may be problems with monetary policy over the next 5 years. So my past objections to the 5-year, 5-year forward data was that it ignored the short-term problem of “lowflation” and high unemployment. It was not a sufficient condition for sound policy.

But now the Fed is not even meeting the minimal objective of market confidence that CPI inflation will run about 2.3% in the very long run. Here’s the graph:

It’s even worse than it looks, as the spread has fallen to about 1.58% today, which is consistent with roughly 1.3% PCE inflation. That’s a very low number for 5 to 10 years out, by which time the current problems (strong dollar, falling oil, etc.) should no longer be impacting the inflation rate.

It’s even worse than it looks, as the spread has fallen to about 1.58% today, which is consistent with roughly 1.3% PCE inflation. That’s a very low number for 5 to 10 years out, by which time the current problems (strong dollar, falling oil, etc.) should no longer be impacting the inflation rate.

Now admittedly there is some evidence that TIPS spreads can be distorted at times (as in late 2008), when there is an inflation risk premium in the bond yield. But as Narayana Kocherlakota points out, that doesn’t mean there’s no loss of Fed credibility, just that the loss is spread between growth and inflation:

Let me turn then to the inflation risk premium (which is generally thought to move around a lot more than inflation forecasts). A decline in the inflation risk premium means that investors are demanding less compensation (in terms of yield) for bearing inflation risk. In other words, they increasingly see standard Treasuries as being a better hedge against macroeconomic risks than TIPs.

But Treasuries are only a better hedge than TIPs against macroeconomic risk if inflation turns out to be low when economic activity turns out to be low. This observation is why a decline in the inflation risk premium has information about FOMC credibility. The decline reflects investors’ assigning increasing probability to a scenario in which inflation is low over an extended period at the same time that employment is low – that is, increasing probability to a scenario in which both employment and prices are too low relative to the FOMC’s goals.

. . .

To sum up: we’ve seen a marked decline in the five year-five year forward inflation breakevens since mid-2014. This decline is likely attributable to a simultaneous fall in investors’ forecasts of future inflation and to a fall in the inflation risk premium. My main point is that both of these changes suggest that there has been a decline in the FOMC’s credibility.

Marcus Nunes pointed out that this decline began at roughly the time NGDP growth began slowing, probably linked to tightening monetary policy. I should say that Marcus, James Alexander, Lars Christensen and some other market monetarists have been ahead of me on this issue.

I’m well aware that asset prices bounce around, and that the markets may well recover from this. But what scares me is that current asset prices already reflect the expected Fed response. That 1.3% expected PCE inflation 5 to 10 years out is already pricing in the fact that the Fed will probably respond to this bearish news by raising rates by less than 4 times. To boost PCE inflation up to the target, the Fed would have to do considerably more than the markets currently expect.

Perhaps in the end all will be well, but as of today the Fed has lost credibility on inflation. The case for further Fed rate increases is much, much weaker than even 4 weeks ago.

HT: Julius Probst

PS. TravisV sent me an alternative view, from the Atlanta Fed.

Tags:

15. January 2016 at 19:32

Sumner: “In China, the exchange rate is artificially fixed at too high a level for macroeconomic stability. ” this after a blog post a short while ago arguing that the Renminbi was priced correctly, based on a misguided iPod index akin to the Big Mac index. Sumner = inconsistency.

It also begs the question as to whether exports and imports can tip a country into recession or depression. If a country’s GNP/GDP is 14% due to imports/exports, as it is in the USA/Japan, does a slowdown in imports/exports matter? Not that much. In China it’s 22%, a bigger number, so it matters more. In Germany (surprising) it’s 45%, see more here: http://data.worldbank.org/indicator/NE.EXP.GNFS.ZS

15. January 2016 at 19:46

Good post.

In other news, I’m almost through The Midas Paradox. So dense. I think I need to read it again. It’s not good train reading…

15. January 2016 at 19:51

The Fed wants low inflation and low interest rates and a slow economy. Banks bet on LIBOR, and force their counterparties to bet on higher fixed swaps rates. If that ever changes, we won’t be the first to know, Scott.

Great article, as I got the main points. 🙂

15. January 2016 at 20:38

About the Atlanta Fed pushback, wouldn’t you agree about following criticisms?

(1) No material fall in “true” inflation expectation during the 2008-09 crisis whereas “impure” breakeven rate falls off a cliff. At least in terms of predicting / reflecting a massively bad macro situation, which one is more useful?

(2) Explaining away the remaining “liquidity premium” by attributing it to seasonality of TIPs yields and market illiquidity. This does not sound right. First of all, how can “seasonality” explain such a large fall in expectation over last 4 years? 5Y5Y forward breakeven rates’ Q4 period average for last 6 years.

2010 Q4: 2.65%

2011 Q4: 2.28%

2012 Q4: 2.83%

2013 Q4: 2.61%

2014 Q4: 2.25%

2015 Q4: 1.83% !!

Even worse, the authors provide the following explanation for what is driving the market illiquidity / exacerbating the seasonal swing. “Redemptions, reallocations, and hedging in the TIPS market after oil price drops and global financial market turbulence can further exacerbate this seasonal pattern. Taken together, these factors are the source of correlation between the BEI measures and oil prices.” Arrgh…So market turbulence outside inflation derivatives doesn’t matter, I suppose….

Looking at it differently, they are almost saying that macroeconomists’ erroneous forecasts are the “pure inflation expectation” and markets’ day-to-day panic in the market is just “illiquidity premium”. I am not comfortable with that conclusion. Especially if the “pure measure” was so wide of mark as it was at the onset of global financial crisis.

15. January 2016 at 22:55

HL, I think the Fed wanted to get rid of sticky wage creep, and make the US economy more competitive, but the medicine of the 2008 financial crisis has almost killed the patient and he may not recover. The Fed targeted inflation as an excuse to execute a diabolical financial plan,a conspiracy. That is my opinion.

16. January 2016 at 01:42

Not much discussed here is the recent amazing surge in Trade Weighted Dollar Exchange rates since the tightening began. It has risen from 75 to 95 in the space of 6 months; https://research.stlouisfed.org/fred2/series/DTWEXM. Because of the effective China Yuan peg to the Dollar, this has also driven up the Yuan which is giving the PBOC the problem that Scott mentioned – they need to devalue to maintain their export share but politically they can’t do this.

16. January 2016 at 04:54

Excellent blogging. Maybe the ECB is feeble too.

My monetary weltenschauung on this one tells me that after 30 years of inflation-fighting, central banks are ossified beyond change.

What is needed is a global summit of the world’s major central banks, and a statement issued that for the next five years the emphasis will be on promoting growth, blowing the doors wide open and much higher inflation and/or NGDP targets.

As it stands now I cannot think of a single industry in which output is constrained by capacity. Not in automobiles, computers, commodities, shipping, railroads, office space, factory space.

The world wants way more demand. How simple does it get?

16. January 2016 at 05:13

OT but not entirely: I have no idea if Premier Ki is telling the truth in the Reuters squibb below. But if he is, a 7% annual rate of growth in China is hardly a death gurgle. See below:

BEIJING (Reuters) – China’s gross domestic product (GDP) totaled more than $10 trillion in 2015 and the economy grew by around 7 percent, with the services sector accounting for half of GDP, Premier Li Keqiang said on Saturday.

The premier also said that employment had expanded more than expected with 900 million people making up the country’s total workforce, including 150 million skilled professionals.

Consumption contributed nearly 60 percent of growth, Li said, at the opening ceremony for the China-backed Asian Infrastructure Investment Bank (AIIB) in Beijing….

–30–

Is there something strange about all the happy grave dancing on China, when Singapore is struggling, and the US and Japan can’t get real growth past 2%?

—

Also, FDI into China services is strong. In other words private-sector investors (not professors and pundits) are risking capital in China. Remember our faith in private markets?

(ADP) “Foreign investment into China accelerated in 2015 as cash poured into the country’s service sector, official data showed Thursday, despite slowing expansion in the world’s second-largest economy.

Foreign direct investment (FDI), which excludes the financial sector, rose 5.6 percent from the previous year to $126.3 billion, according to figures from the commerce ministry.

That is more than triple 2014’s growth of 1.7 percent.

Investment from overseas has been a key element of China’s economic boom in recent years, but as it matures the Asian giant is increasingly becoming a source of funds as much as a destination.

Figures for China’s own overseas direct investment will be released at a later date.

Companies that have received foreign investment were responsible for nearly half of China’s foreign trade, around 14 percent of urban jobs and 20 percent of tax revenues, said a statement with the figures.

The pickup in FDI was driven by strong expansion in investment into the service sector, which has held up well despite growth momentum in the overall Chinese economy weakening as it matures.”

–30—

I know of one very smart money manager who has shorted the yuan. He is able to command op-eds and other pieces written to support the idea that a China tumble is imminent. (I agree with Scott the yuan should float). It is interesting to ponder if some of the professional China bashers are carrying water for people short on the yuan, or otherwise staked out…does not mean they are wrong, but it does mean we have “advocate” economists. pundits and bloggers, just as we have advocate lawyers….and being America, we have the best advocate economists money can buy…

Back in the Peak Oil days, a lot of money was floating around supporting hysterical websites, or Op-Eds etc.

My guess is that a constellation of some facts and excellent-quality scaremongering can keep a story going for a year or two…I like EMH, but then people in the USA are more afraid of terrorists than drunk drivers, antibiotic-resistant bacteria, plain-vanilla armed sadomasochists, or any number of hazards that dwarf terrorism. And this fear has persisted for many years.

I still like EMH, but…

16. January 2016 at 06:35

Now that the Fed is using IOR to peg the fed funds rate and employment numbers to guide itself, it can make bigger mistakes. Like pegging a currency, pegging IOR is a visceral tool that they will abandon too late. And since the only variables that have looked good lately are employment related, they’ve latched on to that under a Philips curve type model. But employment is a lagging variable, so they are now increasing the chances of a recession unnecessarily.

IOR seems dangerous to me in this way. When the Fed adjusted the FFR using OMO, the amounts of cash they injected or withdrew to move the FFR were surprisingly small. If the Fed had tried to truly “normalize” it would have ended IOR. But then, to raise the FFR to 50 bps, it would have had to shrink its balance sheet by $3 trillion. Raising 25 bps just sounded tiny in comparison.

16. January 2016 at 07:45

Sumner lost credibility as soon as he purposefully began failing to accept that TIPS bonds contain an implicit inflation call option, which is a positive value to the holder and a factor that can affect TIPS yields.

No, the 5 year 5 year forward TIPS yield is not the expected inflation rate 2021 to 2026. Sigh, forever wrong.

16. January 2016 at 09:18

Mf. It’s a put

16. January 2016 at 10:09

Ray, You said:

“this after a blog post a short while ago arguing that the Renminbi was priced correctly”

Very funny.

HL, Very good points. I was also wondering about some of those issues.

Gary, You said:

“That is my opinion.”

Yup, it is.

ChrisA, They should ignore the politics and just devalue.

Ben, Yes, they should devalue.

Bill, I sometimes wonder if the Fed really understands IOR as a policy tool

16. January 2016 at 11:05

“But there can ben macroeconomic disequilibrium, if the fed funds rate is pegged at an inappropriate value.”

EARTH TO MMs:

The Fed must by necessity always set any target “at an inappropriate value”.

The definition of appropriate is not what maximizes the Fed’s credibility, as if what Sumner needs for him to have credibility is the definition of appropriate. The definition of appropriate is the definition that allows each individual to define appropriateness for themselves, that is, the market definition.

The Fed never had credibility. It merely had the privilege of state guns abolishing competition.

16. January 2016 at 11:34

In my view, the decline in inflation risk premium/long term inflation expectations, which started to accelerate in July 2014 should be attributed Fed discussing policy normalisation and shrinking its balance sheet at the July 2014 meeting. Basically, Fed here committed to start unwinding its QE, i.e. announcing its intend to begin a QT programme in the near future. Fed has since delivered on its promise and the money base is now at the lowest level since 2013. This should further help explain the drop in oil prices since US does consume 20% of world oil.

Bottom line, it should be no surprise that ngdp growth and inflation remains low in the US and recession fears are beginning to surface.

16. January 2016 at 11:41

Jean-Claude Yellen and her Phillips Curve fantasies are on the cusp of short circuiting the business cycle. Stan Fischer and Duds are in the ‘believe us NOT the market’ camp, reinforcing the error. Only Bullard, who inflates and deflates like three martini lunch, seems to be taking tips seriously…

16. January 2016 at 14:17

China: Just a short while ago everyone agreed that the Yuan was seriously undervalued. Now all the smart people agree that is seriously overvalued. Curious.

Fed: I don’t think anyone actually believes that the fed wants 2% inflation despite public comments otherwise. I think the fed wants inflation to be between 1 and 2 percent. Even the Fed’s own projections suggest < 2% inflation.

Yellen's predecessors had suggested that 2% may be too high in their respective terms. The TIPS market appears to be very rationally pricing a most likely path for inflation.

16. January 2016 at 15:43

“Just a short while ago everyone agreed that the Yuan was seriously undervalued. Now all the smart people agree that is seriously overvalued.”

Yes, I think the dollar is overvalued. The Yuan is overvalued only because it is pegged to an overvalued currency. If the Fed eased, China would not have to do anything. Only my opinion 😉

16. January 2016 at 20:12

Remember, for years and years everyone complained the Chinese currency was undervalued, yet now the markets are saying they are overvalued. It is not plausible this could be happening during a period of deflation as claimed by their official statistics (which in any case are explicitly incomparable over any period of several years).

Seems increasingly clear that they are inflating their domestic economy and misreporting RGDP by misreporting inflation, in a bid to put off the pain of recognizing and correcting malinvestment. This remains plausible as long as they can support the peg, but it cannot work at all in a floating currency, because the ratios of yuan to other currencies determine the exchange rates. Thus, they’ve been depleting their reserves at a rate perhaps approaching a trillion dollars a year while letting the yuan slowly depreciate. Most of the new money seems to be going into credit to support the massive malinvestment we see in ghost cities still severely underpopulated 5+ years after construction — the capital depreciation is enormous and the appear to have reached the limits of economic growth possible without severe political reforms.

In short, they are stuck firmly in the middle income trap, and in the process of bankrupting the country to protect the illusion of growth. The massive wealth surplus created in the greatest economic success story in history is being squandered — but it’s not too late! They could still release the peg, take their lumps, reform their political system, and join the ranks of the rich countries.

Watch the reserves.

16. January 2016 at 22:38

@Sumner – Jan. 9, 2016 you wrote: “Given recent events, only a complete moron, or Donald Trump, would claim the yuan is undervalued. ”

Did you forget this piece? Granted, as is common with your prose, your points in this piece are all over the place, as you discuss under-valuation, over-valuation, real exchange rates and nominal exchange rates, but I think my criticisms of you upstream were not off the mark.

17. January 2016 at 00:29

Tall Dave – The Dollar has appreciated 30% over the last six months versus other major currencies. The Yuan is pegged to the Dollar and so has gone up by the same amount. This is why 6 months ago the Yuan could be fairly said to be undervalued and now could be said to be overvalued. It is has gone up in value by 30%. The Chinese export to more than just the US you know.

17. January 2016 at 14:06

Doug, I certainly didn’t agree the yuan was undervalued. Nor did the “smart people”.

Talldave, In the middle income trap? Didn’t you recently say China would fail to even reach that level? That they’d fail to reach the level of Mexico? They’ve already passed Brazil (which is shrinking), while China continues to grow at 6%.) Mexico isn’t all that far above Brazil.

Ray, I mocked you for claiming I thought the yuan was correctly valued. What’s your point?

18. January 2016 at 13:30

Scott — I do not think Chinese living standards can pass those of Mexico without major political reforms. I hope they happen soon, but I do not think they will. Are you really arguing China is already a rich country? China itself says GDP is not comparable across years due to methodology changes, so how do we know if they’ve been growing at 2% or 6% since 2008? Do you really believe Chinese inflation was negative last year?

ChrisA — China has had the dollar peg a lot longer than six months and exchange rates have always fluctuated, but they’ve never been forced to spend hundred of billions of dollars defending the peg before. Clearly something changed in 2015.

18. January 2016 at 13:38

Talldave, You said:

“Are you really arguing China is already a rich country?”

I don’t follow this at all. I just said China was poorer than Mexico. Why do you say I claimed China was rich?

And your comment on the inflation data is irrelevant, as I was using World Bank PPP estimates, which do not depend on Chinese inflation data being accurate.

As far as 2% growth, all I can say is that’s not the China I see on my visits.

18. January 2016 at 13:55

Okay good, I was pretty sure we agreed China was a middle income country, but I wasn’t sure if you considered Mexico rich. To clarify, I’d say any countries below Mexico are middle income, and I do not believe Chinese living standards will pass Mexican living standards.

Not sure if you’ve seen Nakamura’s paper on China and Engel curves, but Chinese data is just very strange — one might even say inscrutable.

http://www.columbia.edu/~en2198/papers/chinainflation.pdf

18. January 2016 at 14:08

Sorry, forget to add, on the World Bank data — don’t they use exchange rates for the PPP adjustment? That was kind of my point above, the peg allows their claimed growth rates to appear plausible, if the yuan floated they couldn’t hide inflation from PPP adjustments.

18. January 2016 at 21:35

@TallDave – “Clearly something changed in 2015” – yes the US Fed increased their target interest rate despite no inflation, which has meant the USD is now rising strongly (since currency traders can understand their intent). I am not sure how I can explain it more simpler.

19. January 2016 at 03:17

[…] Scott Sumner, Director of the Program on Monetary Policy at the Koch-funded Mercatus Center at George Mason University, who recently wrote that the impact that the minimum wage has was not clear to him (SEE: A Mercatus Center Economist Becomes Confused About the Impact of the Minimum Wage), has now stated that the Federal Reserve has lost credibility for not creating enough price inflation. He writes: […]

19. January 2016 at 10:33

“Tall Dave – The Dollar has appreciated 30% over the last six months versus other major currencies”

“the US Fed increased their target interest rate despite no inflation, which has meant the USD is now rising strongly”

A rather selective sampling…

Dollar index is up 1.4% the past six months and has been pretty much oscillating around 97.5 since March 2015.

25. January 2016 at 08:49

[…] Sumner: "I’m well aware that asset prices bounce around…. What scares me is… 1.3% expected PCE inflation 5-10 years… pric[es] in the fact that the Fed […]