The Great Depression

My book on the Great Depression is officially being released on December 1st. At that time I plan to do a few posts discussing the book. But since some have already received copies, I thought it might help to provide a quick overview for what is a fairly complicated hypothesis. The book is certainly not “easy reading”, and I’m hoping the following two charts will make it easier to follow the thread of the argument. (In other words, unlike Garett Jones I didn’t take Bryan Caplan’s advice.)

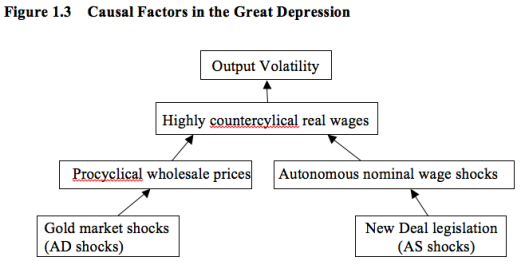

Here is a flow chart in the first chapter:

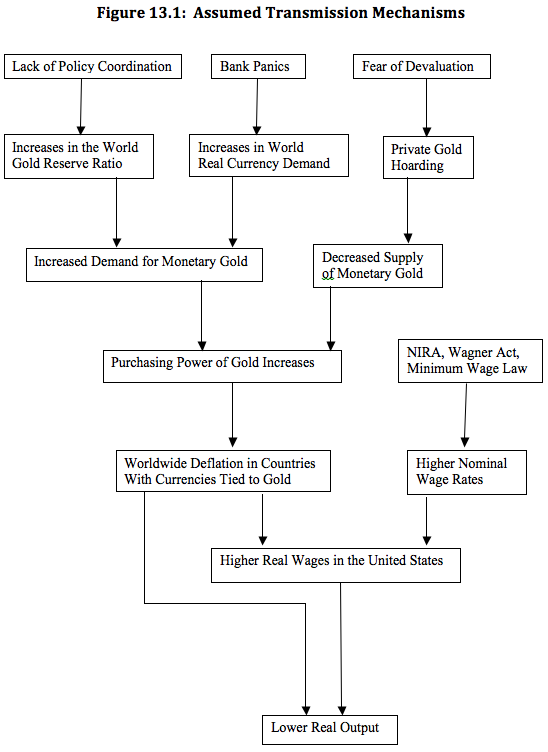

The final chapter (13) includes a more detailed model, intended for serious scholars. In that chapter I also have a more detailed flow chart, which explains how all the pieces fit together:

The final chapter (13) includes a more detailed model, intended for serious scholars. In that chapter I also have a more detailed flow chart, which explains how all the pieces fit together:

If you get confused while reading the book, consult these flow charts. They explain how each piece of the puzzle fits together. When I wrote the book (it was done by about 2005) I had no idea that more than 50 people would ever read it, so I wrote it at a level aimed at specialists. Now it seems that many more people than I expected will read the book. Obviously I’m pleased by the interest, but quite honestly if you only have time to read one economics book this year, make it Garett Jones’s Hive Mind, not my book.

If you get confused while reading the book, consult these flow charts. They explain how each piece of the puzzle fits together. When I wrote the book (it was done by about 2005) I had no idea that more than 50 people would ever read it, so I wrote it at a level aimed at specialists. Now it seems that many more people than I expected will read the book. Obviously I’m pleased by the interest, but quite honestly if you only have time to read one economics book this year, make it Garett Jones’s Hive Mind, not my book.

Tags:

19. November 2015 at 08:51

Scott,

Two questions.

First, do you have a mathy model?

Second, do you have a timeline chart, say, from 1930 to 1940, detailing each nominal and real shock, and its effect on IP, Inflation, and the Dow? Like one of those things they include in Macro models.

These two things would be useful for improved exposition, so you can SEE whats happening.

Look forward to reading it!

19. November 2015 at 10:06

Prof. Sumner,

Two things:

(1) My dad still thinks the critical thing that caused the Great Depression was the buildup of debt during the 1920’s boom–particularly margin debt for stock purchases prior to the 1929 stock market crash. What’s the best way to refute that argument?

(2) Re: “Fear of Devaluation” in your chart, I always have trouble with the idea that widespread “Fears of Devaluation” typically result in negative demand shocks rather than positive demand shocks. That’s really counterintuitive to me.

19. November 2015 at 11:07

Already pre-ordered it! (so you only have to sell another 49 copies to reach your initial goal 😉

19. November 2015 at 11:41

Typo. “High countercyclical real wages.” You can read these things 1,000 times and still miss things up to the very moment it goes to print.

Not one mention of debt-deflationary pressures?

19. November 2015 at 11:43

Preordered Kindle edition.

19. November 2015 at 12:15

A timeline would be useful since harmful New Deal legislation was passed after the worst of the Depression had passed. I’m not disputing that some of the policies of the New Deal were bad; specifically wage and price controls. But, you know, causality and such.

19. November 2015 at 12:17

Test2

19. November 2015 at 12:25

test3 (sorry, Scott)

19. November 2015 at 13:01

Michael Byrnes, thanks for the heads up about the kindle version.

I pre-ordered it as well.

19. November 2015 at 13:11

Isn’t this your magnum opus, and you’re telling people to go read Hive Mind? Is it that unreadable?

19. November 2015 at 13:13

TravisV

I know that Sumner uses a very narrow definition of money… but if you accept a broader definition of money. Margin-debt, also known as “call-money”, is money.

The 1929 crash lead to a a rapid reduction in call-money. This tightening of the money supply triggered the great depression. More tight-money polices exacerbated the problem.

This would mean that you dad is not wrong, and tight money is still the cause of the great depression.

Sumner may say that the 1929 crash reflected expectations of falling NGDP growth. Hence, tight money triggered the crash rather than was a consequence of the crash.

19. November 2015 at 13:48

Is there a reason I got my copy long before everyone else or did I just get lucky?

19. November 2015 at 13:56

Joe, There’s a fair bit of math in chapter 13, but it’s basically accounting math, not a GE model. I use a partial equilibrium approach.

There are lots of graphs in the book, but no single timeline. Way too much info for just one timeline.

Travis, Not sure why margin debt would cause a recession. Is there a model he has in mind? We know from 1987 that big stock market crashes have no impact on GDP.

I don’t see debt deflation as a direct factor, but it certainly contributed to the bank failures, which are mentioned.

Thanks Luis, BTW, one individual ordered 200 copies, so I pretty confident I’ll sell 50.

Michael, I hate Kindle. It’s like watching a movie on TV, you lose something.

jknarr, Thanks, fortunately it’s not in the final version.

Benny, The timing issues are discussed in great detail.

Patrick, Where is test1?

AD, You said:

“Is it that unreadable?”

No, It’s well worth reading if you are interested in the Depression (of course I’m biased), but Jones’s book is great, and more readable.

19. November 2015 at 14:03

Prof. Sumner,

I highly highly recommend you try reading electronic books with an iPad or other tablet. I personally use an iPad rather than a Kindle. It’s my favorite way to read a book! My mom, who reads a lot more books than me, typically uses an iPad Mini rather than a Kindle.

The clarity of the screens on new devices is one of my favorite innovations of recent years…..

19. November 2015 at 14:22

Arnold Kling just listed his favorite books of 2015 on his blog.

Also, I’ve been skimming David Glasner’s classic “Free Banking and Monetary Reform,” and I think it’s an overlooked gem.

19. November 2015 at 15:07

TravisV:

“My dad still thinks the critical thing that caused the Great Depression was the buildup of debt during the 1920’s boom–particularly margin debt for stock purchases prior to the 1929 stock market crash. What’s the best way to refute that argument?”

This comment is proof you put your ideology above reason.

You don’t ask how an argument can be refuted if you don’t even know if is right or wrong by way of an argument. But if you presume the argument is wrong anyway, without even knowing how it is wrong, then that is exact backwards method of rational thought. Rational thought would lead you to right conclusion before you know it is right or wrong at the outset.

It would be like asking “I want to refute an argument I don’t like because it makes me feel bad. Could you provide me with an ex post rationalization for my feelings by using some mumbo jumbo or another I can tell my dad?”

Good grief, and Sumner did not even have the courage to point this out to you. Like a cult or what.

————

Sumner, the demand shocks you witness are caused by the very cure you proposed for past demand shocks

People do not just cavalierly and drastically increase the time of money/gold holding without reason. What you call a “shock” is itself an effect of past money manipulation, as all central bank activity inherently must be.

The crash of 1929 was caused by undue inflation of the money supply during the 1920s. You know, the inflation that you claimed did not exist on the excuse that that Fed agents were not looking at the aggregate money supply back then.

A huge component of this additional money supply was in the form of credit expansion. Credit that is expanded without backing can collapse without backing. The crushing deflation could not and would not have occurred had it not been for the roaring twenties inflation and credit expansion.

TravisV, your dad is smarter than you. You should learn from him.

19. November 2015 at 15:34

“What caused the slump of 1930? (Pt. 4 of 4)”

http://www.themoneyillusion.com/?p=4286

One of my all-time favorite posts, that almost no one ever cites, for some reason….

19. November 2015 at 15:39

https://www.youtube.com/watch?v=8hlpDxdbj5w

Prof Sumner, Milton Friedman at around 26:30 says exactly what you’ve been saying. “It looks to you like you can control how much money you have in your pocket versus in the bank, but for the system as a whole, its a game of musical chairs!!”

I think you’ll appreciate his brevity and brilliance, which i’m sure you are aware of.

19. November 2015 at 16:20

I only use the Kindle E-reader, for me the e-ink is nearly as good as print. And it’s easier to carry lots of books around (or find a “bookstore”) on an e-reader.

19. November 2015 at 16:37

TravisV, I haven’t tried reading on an iPad, but I love my kindle. Strangely enough, I find it’s easier on my eyes than a regular book. Adjustable fonts, margins, colors, etc. The new paperwhite (the type of kindle you can read outside in the sunlight) is supposed to be nice.

I used to hate the very idea of using an e-book reader because I thought it was going to be like reading on my computer screen (which I hate). Boy was I wrong. Thanks to my kindle I read several books a year instead of none. And now, on 1 Dec, my kindle will automatically download Scott’s new book – hopefully a nice addition to my growing library.

19. November 2015 at 18:32

Scott’s book has been very impressively blurbed.

19. November 2015 at 18:39

+1 for jknarr, I also saw the typo that ‘countercyclical’ is misspelled in the flowchart. What else does Sumner have wrong?

Sumner claims this is not the final version, so there’s time to correct any mistakes? Mistakes like “the death of Ben Strong Jr was a factor in the Fed’s tight money” myth (rebutted by a recent paper that came out earlier this year, as I pointed out to Sumner and as he acknowledged he’s not read), and the numerous examples of selective cherry picking by Friedman on ‘bad Fed episodes during Great Depression’ as highlighted by Christina Romer in the paper I referenced the other day.

Further, Sumner says “I don’t see debt deflation as a direct factor, but it certainly contributed to the bank failures, which are mentioned.” – no, professor, I think the poster is referencing Fischer’s “Debt Deflation Trap” aka balance sheet recession meme, not bank panics. But “you are the expert here” (snicker).

19. November 2015 at 18:42

@myself – here is the paper:

“Did the Reserve Requirement Increments of 1936-1937 Reduce Bank Lending? Evidence from a Natural Experiment∗ HAELIM PARK and PATRICK VAN HORN Article first published online: 28 JUL 2015.

And the answer to the titled question is “NO”. Score another one that Sumner got wrong.

19. November 2015 at 18:47

@myself again- the ‘Ben Strong died is bad’ meme is found in another paper, while the above goes to the 1937 contraction that apparently was deemed caused by the Fed’s tightening, when in fact is was not. The Romer paper highlighting how flawed Friedman et al’s GD paper was is found here: Volume Title: NBER Macroeconomics Annual 1989, Volume 4 Volume Author/Editor: Olivier Jean Blanchard and Stanley Fischer, editors Volume Publisher: MIT Press Volume ISBN: 0-262-02296-6 Volume Conference Date: March 10-11, 1989 Publication Date: 1989 Chapter Title: Does Monetary Policy Matter? A New Test in the Spirit of Friedman and Schwartz Chapter Author: Christina D. Romer, David H. Romer Chapter URL: [redacted for WordPress, just Google it]

19. November 2015 at 21:04

OT – On Garett Jones’ Hive Mind: see this critique: http://econlog.econlib.org/archives/2015/11/a_swarm_of_thou.html

Seems that Jones revamped The Bell Curve a bit, and Googled “IQ by Nation”, which anybody can do, and wrote a book on it. Mercifully, it’s a short book. Long story short: IQ depends on a nation’s environment, especially prenatal care and kid’s development. The more smart people in your country the better off you are. And if you believe China’s numbers, they have an IQ equal to the West (lol, fake numbers using only big cities like Beijing and Shanghai, a trick that Sumner also fell for with economic indicators)

20. November 2015 at 06:16

Another book to add to Sumner’s bibliography section, in the second, revised edition of his 2005 book. If Sumner is man enough to read and understand it. Can you handle the truth Sumner? You ***’* ****** *** truth!

Mark Toma, who is endorsed by none other than Lawrence H. White, Professor of Economics, George Mason University:

http://www.barnesandnoble.com/w/monetary-policy-and-the-onset-of-the-great-depression-mark-toma/1117473228?ean=9781137372543

Monetary Policy and the Onset of the Great Depression challenges Milton Friedman and Anna Schwartz’s now-consensus view that the high tide of the Federal Reserve System in the 1920s was due to the leadership skills of Benjamin Strong, head of the Federal Reserve Bank of New York. In this new work, Toma develops a self-regulated model of the Federal Reserve, which stands in contrast to a conventional discretionary model. Given the easy redemption of dollars for gold and the competition among Reserve banks, the self-regulated model implies that the early Fed could control neither the money supply nor the price level. Exploiting an untapped data set, later chapters test the thesis of self-regulation by focusing on the monetary decisions of individual Reserve banks. The micro-based evidence indicates that “Reserve banks really did compete” – and that Benjamin Strong as decisive leader during the 1920s is a myth.

20. November 2015 at 07:47

What part of Bryan Caplan’s advice did you not follow? “Write like Hemingway?”

20. November 2015 at 08:21

[…] 1. Arnold Kling’s books of the year. And Scott Sumner outlines his forthcoming book on the Great Depression. […]

20. November 2015 at 08:28

This looks a lot like the explanation at the start of *The Wages of Destruction*. I imagine you go into much more depth but have you read that book and do you have an opinion on it?

20. November 2015 at 08:39

How does the agricultural commodities fit into the model? My understanding is US farmers had their economic boom in the 1910 – 1920 period with huge exports to WW1 Europe and an investment productivity boom. (If Japan wrote the book on high growth export model from 1960 – 1990, it was the US 1900 – 1930 who wrote the rough draft. Oddly enough it was Wilson who heavily promoted free trade only to have WW1 accelerate the US export markets.) Then in the 1920s the independent farmer started failing in the mid-1920s due to improve European farming and deflationary prices. Then when The Great Depression happened the farmer really suffered and many of them failed.

20. November 2015 at 09:45

I preordered last month and it arrived last week. Curious…

20. November 2015 at 10:22

Travis, Yes, Glasner’s book is an underrated gem, as you’d expect from his blog.

Thanks MichaelPWh, Friedman was always a great communicator.

Ray, You said:

“And the answer to the titled question is “NO”. Score another one that Sumner got wrong.”

Nice try, but I never made that claim. But thanks for reviewing a couple books that you have not read, I’m sure are other commenters are fascinated by what you say about these books that you have not read. Next time could you go into a bit more depth—make your comments on these books longer? I’m sure I’m not the only reader that wishes you gave us more of your informed opinions.

Philo, Make it reader friendly.

Andrew, No, unfortunately I didn’t keep up with the literature after 2005. The field is too vast. I do recall that Hitler followed a low wage policy, which fits with my hypothesis.

Collin, Yes, that’s basically correct.

Thanks Ricardo.

20. November 2015 at 10:54

Got my hardcopy a couple weeks ago, I like how you dived right into gold prices in the preface. Probably won’t get too much into it until I get the ebook.

20. November 2015 at 11:12

BTW, looks like the Kindle edition is available now.

Kindle has just ruined me for regular books, they seem medievally inconvenient now. The scalable fonts let you read with or without glasses, the backlighting lets me read while my little ones go to sleep in my arms, I can search, Wikipedia is at my fingertips, never lose my place, fingers don’t get tired from holding the book open, can lay on my back and hold the book over my face, can carry hundreds of books around everywhere…

20. November 2015 at 11:49

Sorry to be difficult.

But you said that we know from 1987 that the economy can survive a stock market crash.

But the 1987 crash caused the Fed to reverse a tightening it had stated earlier in 1987. So the economy was reacting to the Fed changing policy not the stock market.

20. November 2015 at 20:12

@ Dr. Sumner who says:

Nice try, but I never made that claim. But thanks for reviewing a couple books that you have not read, I’m sure are other commenters are fascinated by what you say about these books that you have not read. Next time could you go into a bit more depth—make your comments on these books longer? I’m sure I’m not the only reader that wishes you gave us more of your informed opinions.

Glad we’re on the same page. Remember, there’s no such thing as irony on the internet, so I take your above comment literally.

“Did the Reserve Requirement Increments of 1936-1937 Reduce Bank Lending?” – the answer is NO and apparently your book agrees. I’d like to see your explanation of why there was a mini-recession in these years, from a monetarist point-of-view. Maybe interest rates? Expectations? Well I might have to just buy the book and find out! 😉

Have your read Christina Romer’s late 1980s paper criticizing Friedman & Schwartz’ magnum opus? She blasts Monetary History for cherry picking data but ends on a happy note by concluding, from an econometrics point of view, that monetarism matters. BTW I am informed by Tyler Cowen that she also believes output was not that different under a gold standard. Therefore (my words not TC’s) any return to a gold standard, as advocated presently by some Republicans, would not be a complete disaster (IMO money is neutral so it doesn’t really matter anyway). Agree? A blog would be nice on this.

Finally, Tomas’ book costs over $100. Thus I am relying on Amazon.com reviews, but his “Ben Strong dying was not that bad” theme is unconventional. Do you agree? Why don’t you buy the book, with your unlimited scholars budget, read it,and comment for your loyal readers? I’m in the Philippines and even if I was willing to shell out $100+ bucks, it takes six weeks for snail mail to get here and stuff disintegrates in this 80%+ humidity and high temps year round environment (like south Texas in summer, but year round, and more lots more rain). Unless you are very careful all paper here ages really fast.

Take care and glad we agree. I will start giving you more benefit of the doubt. If Bernanke et al informs us that monetarism is responsible for 3.2% to 13.2% of any economic variable -trivial but true- then you’re the guy that thinks that’s a big deal, and, like the grammarian that insists you cannot end your sentence on a preposition, we just have to roll our eyes and agree with?

21. November 2015 at 11:02

Matt Yglesias read Tyler Cowen and Ryan Avent and described his personal macro framework:

http://tinyletter.com/mattyglesias/letters/skip-town-slow-down

21. November 2015 at 19:25

I just ordered my copy.

But no Audible/Whispersync version? C’mon!

22. November 2015 at 07:35

‘Patrick, Where is test1?’

I wish I knew. Cybergremlins ate it?

22. November 2015 at 09:52

Talldave, I hate Kindle.

Spencer, The point is that a stock crash doesn’t affect the economy with a stable monetary policy, keeping NGDP growing at a fairly steady rate.

If the Fed does something incredibly stupid after a crash, then yes, the tight money could cause a recession. But that would not be the stock market crash causing a recession, it would be due to a tight money policy.

Ray, Buy two copies; your girl friend might want to read it too. I get about a buck a book in royalties–you need to pay for the online platform I provide you with.

You said:

“Therefore (my words not TC’s) any return to a gold standard, as advocated presently by some Republicans, would not be a complete disaster (IMO money is neutral so it doesn’t really matter anyway). Agree? ”

No.

23. November 2015 at 20:18

[…] to be sure, Scott has a very nuanced theory of how various factors came together to produce the Great Depression. And yet, the title of the […]