The Fed’s targeting inflation at 1%; it just doesn’t know it yet

It’s odd, but the best way to forecast price inflation is to look at wage inflation. In the years leading up to the Lehman crisis wage inflation ran about 3.4% and price inflation (PCE core) ran around 2.4%. The gap reflects productivity (and changes in the share of national income going to labor.) Headline inflation reflects core inflation plus food and energy. However food and energy are essentially unforecastable, at least if you look out more than a few months. So core inflation is the best way to forecast headline inflation. And core inflation is mostly wages, minus productivity gains.

For some reason core inflation slowed a bit less rapidly than wages over the past 4 and 1/2 years. PCE core inflation has run about 1.4%, whereas wages are rising at a tad less than 2.0%. But in the past 12 months the predictable pattern is coming into view. PCE core inflation has dropped to 1.05% (the lowest ever recorded), which is roughly 1% under wage inflation. Headline PCE inflation is down to 0.7%.

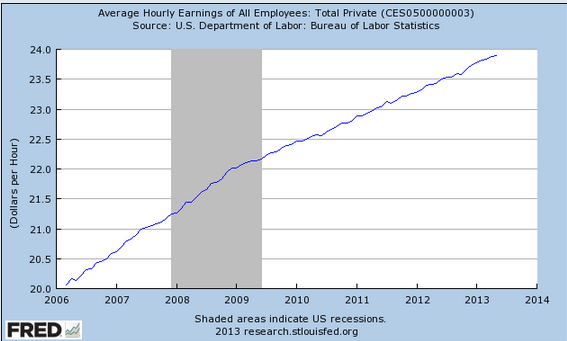

The following graph of average hourly wages tells you all you need to know about inflation since late 2008:

You can clearly see the inflection point in late 2008, when the asset markets crashed. Markets saw the huge disinflationary shock, but the Fed did not. It takes a lot of unemployment to suddenly drive nominal hourly wage growth down to 2%.

The trend in nominal wage growth seems unlikely to change soon. That means PCE core inflation will stay close to 1%, or a bit higher, and headline inflation will fluctuate unpredictably above and below 1%, because commodity prices are unforecastable.

The Fed will gradually become aware of the fact that money is too tight for it to hit its inflation target. That will give the doves the upper hand, and if I didn’t believe in the EMH I’d tell my readers to buy long term bonds—I think rates will stay low for longer than the markets currently seem to assume.

It’s odd that James Bullard is the only FOMC member who sees what’s going on.

Marcus Nunes and Justin Wolfers express similar views.

PS. I don’t own any bonds, I invest in stocks.

PPS. The Fed’s mandate calls for it to adopt policies likely to lead to above 2% inflation during periods of high unemployment, and below 2% inflation during periods of low unemployment. They don’t seem to understand their mandate. Indeed they are acting exactly like a central bank would act if its mandate were stable prices and high unemployment.

Tags:

24. June 2013 at 05:42

At what point do we stop pretending that the Taylor rule has any value and that John Taylor is a good economist?

24. June 2013 at 05:44

Another blind spot (yours and theirs) is that the “austerity” is consists almost entirely of tax increases. Government spending continued to rise.

Even more important is the refusal to make the structural

changes necessary to resume growth. Corruption, limitations

on companies ability to fire people and therefore unwillingness to hire them as well as grow have created very large segments of the population that are operating in the so-called `shadow` economy.

These actions/inactions are far more important than monetary policy.

http://www.nationalreview.com/corner/350225/spending-cuts-tax-increases-and-austerity-veronique-de-rugy

24. June 2013 at 06:15

What’s the problem with low inflation? http://macromarketmusings.blogspot.com/2013/06/the-tapering-talk-and-rising-yields-are.html

24. June 2013 at 06:21

To steal a line I recently read from Thomas Sowell, ‘It’s like watching Mickey Mantle try to hit Hoyt Wilhelm.’

24. June 2013 at 06:23

[…] See full story on themoneyillusion.com […]

24. June 2013 at 06:29

Aldrey, There is no problem with low inflation, there is a problem with low NGDP, or with failing to hit your inflation/employment mandate.

24. June 2013 at 06:34

Wow, apropos my suggestion a few posts back that economists just drop, completely drop, the term ‘interest rates’ from their vocabulary when talking about monetary policy, I just heard this guy on the radio in Seattle;

http://www.hillsdale.edu/academics/display_profile.asp?cid=858990001

He gave a textbook perfect explanation of the QTM, and why the policy of paying interest on reserves has kept the funds with which the Fed paid for its bond buying, out of the broader economy and inflation low. Not even a whisper on ‘interest rates’.

His prediction that eventually the Fed will have to raise reserve requirements to keep those reserves ‘quiet’ is interesting speculation too.

24. June 2013 at 07:04

“and if I didn’t believe in the EMH I’d tell my readers to buy long term bonds”

Today is an excellent day to buy bonds. It takes a while to digest the liquidity effect, especially after a major policy shock. But expectations are now ready for a reset toward a 1% inflation objective, and probably 2.5-3.0% NGDP.

24. June 2013 at 07:35

Stupid follow up to Aldrey: What’s wrong with low NGDP growth? Adding 1% inflation to 2% real growth would be 3% NGDP growth. In the past you have been (somewhat) ambivalent about exactly what NGDP target they should use; certainly 5% is not a magic number. So with 2.5% real GDP growth, they are skittish, and want to tighten to get less than 1% inflation. When real growth was <1%, they were more comfortable with 2% inflation. Your plot of hourly wages since 09 looks a lot like what you would see with NGDP targeting, just at a pretty low annual rate.

I'm not exactly suggesting that they are targeting 3% NGDP, but it would seem to be a natural result of a central bank that is willing to risk 3% inflation only when real growth is almost nothing, but otherwise wants basically no inflation, and a large, advanced economy that can't easily support greater than 2% real growth.

So if that is where they are, is the only real problem that they aren't communicating it as such? Or is the selection of an NGDP growth target of greater than 4% necessary?

24. June 2013 at 08:13

Nick,

But the high wage to NGDP ratio and the stagnant employment numbers suggest that the real economy has a little catch-up to do. Until the wage to NGDP ratio is down and inflation up, it doesn’t make sense to assume that potential growth has slowed enough or that human capital has been destroyed enough to eliminate the demand shortfall.

24. June 2013 at 09:22

How much of the problem in recent years (i.e. since 2009) is driven by our recent evidence that the Fed is:

1. Unable or unwilling to offset large nominal shocks that impact the real economy.

2. Unwilling/unable to correct past mistakes.

In other words, the expectation that a large nominal shock might occur in the future is much greater today than it was at this time in 2007, simply because we’ve seen it happen. And we have also seen that the Fed response to the crisis was to let bygones be bygones.

In the past few years, the Fed has seemed to establish a new trend path for NGDP, and the Fed has defended that trend against some nominal shocks (Euro-madness, Tax hikes, sequester, etc.).

But how certain can we be that the Fed will continue to defend this trend? How certain can we be that the Fed will not screw up again, as it did five years ago? And if it does screw up, how confident can we be that it will not let bygones be bygones?

Wouldn’t uncertainty on these points tend to undermine the recovery?

24. June 2013 at 10:33

Didn’t the Fed talk about temporarily accepting inflation higher than 2% so long as unemployment was above 6.5%? That talk is no longer heard; what happened to it?

25. June 2013 at 05:44

Patrick, That’s good to hear.

Nick. There is nothing wrong with a 3% NGDP target path, if they’d been doing it all along. The problem is when they suddenly switch to it, especially in the midst of a financial crisis.

The other problem is that it’s inconsistent with their announced policy regime, and hence will create economic instability when they return to their announced policy regime, as they will eventually.

Michael, Those are good questions. I’d add that the Fed created the nominal shock with a tight money policy in late 2007 and early 2008.

Philo, Good question.

28. June 2013 at 23:27

Here’s a way to make a convincing graph to visually demonstrate a change in slope of a curve at a certain point. Say we are plotting y=f(x) and we think the slope changes at x=A. Fit the curve to a line y=mx+b using the data with xA. Let M = (m+n)/2 be the average slope. Now plot y-Mx against x, and magnify the vertical scale so the points fill the plotting area. The slope to left of A will appear to be m-M, and the slope to the right will appear to be n-M. The two slopes will have opposite signs but equal magnitude, making an impressive visual effect.

20. February 2017 at 06:46

[…] http://www.themoneyillusion.com/?p=21974 […]

19. March 2017 at 05:55

[…] doesn’t know it yet which is hard to argue with based on performance. http://www.themoneyillusion.com/?p=21974 Still, Yves is being just a little hyperbolic in saying that mortgage rates have […]