The British jobs recovery

Over at Econlog I have a new post discussing the German jobs miracle. The punch line is that both NGDP and wages in Germany behaved in about the same way as in America. This means that my “musical chairs model” predicts that job creation would also be about the same. However Germany employment is up 6% over the past 6 years while US employment is down 0.7%. The mystery is resolved if you look at labor income as a share of NGDP–it did far better in Germany than in the US.

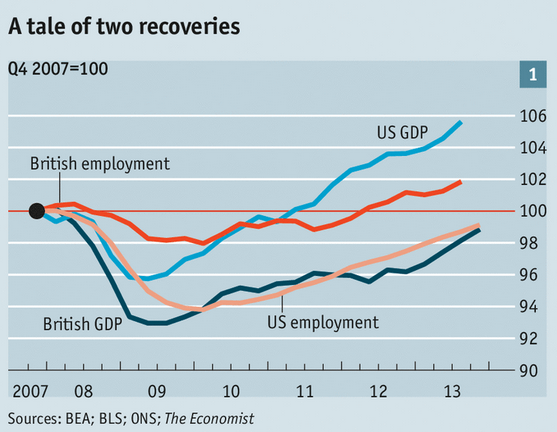

This graph over at Free Exchange made me want to take a look at the British data:

Notice that US RGDP has risen far faster than British RGDP, and yet Britain has created significantly more jobs.

Here’s some data I collected, 4th quarter of 2007 to 4th quarter of 2013:

Country —– United States Britain

RGDP growth 6.2% -1.3%

NGDP growth 14.2%16.3% 13.1%

Change in U-rate +2.2% +2.1%

Employ. change -0.7% +2.5%

Weekly wages 13.6% 10.7%

When considering job creation in the UK, it’s tempting to focus on slow wage growth and/or productivity. But in a sense the US is the outlier. I couldn’t find data on the share of GDP going to labor in the UK, but the data I do have (weekly wage growth plus employment growth) indicates that total labor income probably grew by just over 13%, about the same as NGDP. Thus labor’s share was probably stable. In contrast, in the US labor’s share of GDP fell by 3.6%, and this largely explains why employment fell, despite NGDP growing a bit faster than weekly wages.

So Germany saw strong wage growth due to a rising share of income going to labor, in the UK employment grew more slowly with a stable share, and in the US employment fell with a declining share of income going to labor.

Is that pattern likely to repeat in future cycles? I doubt it–it seems more like a coincidence. Something that happened in each country for reasons unrelated to the recession. In my view the keys are still nominal hourly wages and NGDP growth.

Also notice that British NGDP grew a bit faster than German NGDP (which grew 12.8%.) Thus when Keynesians argue that Germany did better than Britain because of a more expansionary fiscal policy, they are doubly wrong. First, because Britain ran far bigger deficits than Germany–only with creative accounting (lower GDP implies a smaller cyclically-adjusted deficit) do you get Britain having tighter fiscal policy. And second, because Britain actually saw faster growth in nominal spending—the UK RGDP shortfall (relative to Germany) was 100% supply-side. Thus arguing that British AD did worse than German AD due to a less expansionary fiscal policy is absurd, as there is no relative AD shortfall in Britain that needs explanation!

Tags:

14. April 2014 at 06:37

So we have a ‘supply shock’ the equivalent of 7% of GDP between the US and UK, yes?

This is Mark Sadowski’s unexplained supply shock is it? 7% of GDP difference? But we can gloss over that? Other than the shooting, Mrs. Lincoln, how did you like the play?

It’s Germany which I find more perplexing. Did Germany export its unemployment to the southern tier via the Euro? Can the UK, with a floating exchange rate, and Germany with an exchange rate set to German preferences, be compared apples to apples? Or is it fairer to consider the Euro area as a whole?

Also, here’s the latest from me. http://blogs.platts.com/2014/04/09/citi-chevron-oil-price/

And there should be some meat for you here, Scott. Exxon sees oil prices at $109 in 2017; Chevron at $110. 2017 futures are at $95. Comment.

14. April 2014 at 07:08

Scott,

Sorry if this is a dumb comment, but I just want to make sure I’m understanding your point…

Iis it correct to say that a primary (only?) weakness of NGDPLT is that it fails to account for shifts in labor’s share of income? Is this why targeting hourly wages is a superior monetary policy in theory?

14. April 2014 at 07:29

The Germans decide to make their labor market worse;

http://www.themunicheye.com/news/Germany%27s-first-minimum-wage—8.50-Eur-2869

————quote————

Germany’s first ever legislation for a minimum wage has been set by Chancellor Angela Merkel at 8.50 euros an hour (£7; $11.75). The law will come into effect on Jan 1st, 2015. Currently, Germany is one of only seven countries in the EU without a minimum wage level. The change came about due to the power-sharing deal with the Social Democrats (SPD).

The SPD was in favour of the move, but the conservative CDU and CSU parties had been less eager to adopt the policy. The Bundestag is expected to debate the proposal in the summer. It will then move to the upper house for approval in September.

The SPD’s labour market policy spokesperson, Katja Mast, commented: “Labour has won its dignity back with a fair payment of 8.50 euros, whether in the East or West and with no industry exceptions.” However, the wage does not cover minors, interns, trainees or long-term unemployed people for their first six months at work. Additionally, employers, such as those using temporary or seasonal workers, will have two years to phase in the new minimum wage. For the rest of Germany’s employers, the regulations will come into effect on 1 January 2015 and the wage will be reviewed annually from 1 January 2018.

———–endquote———-

14. April 2014 at 07:45

Nice post. The Germany/US/UK comparison is very interesting.

I am on vacation and can’t check the actual data but from memory you are right about the UK labour share.

Steven Kopits, that 7-8% figure is correct for the divergence of UK and US labour productivity over 2007-13.

14. April 2014 at 10:22

Rather than talk about productivity, which certainly is the story, in the US technology adoption is faster.

And that is the story.

But the key thing here, I keep trying to explore, is that the baseline of employment in US in 2007 was “inflated” and also less productive.

Had we not had a buildup of construction 2004-2007, the technology industry would have grown faster than it did otherwise. We basically weren’t becoming as productive as we could be 2004-2007, because we had far too many unproductive people flipping houses and living off loans.

Which is why when the crash happened, it was so easy for companies to cut fat from balance sheets, not only did they have some marginal workers laying around, there was a ton of tech that had been READY for them to use and adopt earlier than they did…. because they didn’t have to.

The a small sliver of the story I’m telling here is that say Netflix would have moved to streaming much faster, bc studios would have given up better contract terms, bc more people would be staying home and illegally downloading movies in a recession.

We saw the explosion of broadband in US 2001-2003, precisely for this reason. There was literally NO reason to broadband in 2001 (there was zero content being created) except to use p2p music trading software.

Which BTW begat the iPod/iPhone/iPad Apple reemergence.

People suddenly had thousands and thousands of songs – free recession entertainment.

14. April 2014 at 10:47

Steven Kopits (re: oil futures): Isn’t that just normal backwardation?

Morgan: The housing boom solved the problem of the mismatch of production and consumption with the millions of baby boomers who are currently very productive but need to make sure they can consume in 30 years when they are unproductive. The housing boom effectively moved production back in time. Far from being a distortion, this was the most efficient way to bridge this demographic gap. The recession helped to undo most of that progress, so now when we might have seen labor move into new sectors, we have a higher need for housing (as a savings mechanism) than we should have.

14. April 2014 at 11:07

So if wages fell and unemployment rose in the US but not in Germany doesn’t that suggest sticky wages is a myth?

14. April 2014 at 11:14

“When considering job creation in the UK, it’s tempting to focus on slow wage growth and/or productivity. But in a sense the US is the outlier. I couldn’t find data on the share of GDP going to labor in the UK, but the data I do have (weekly wage growth plus employment growth) indicates that total labor income probably grew by just over 13%, about the same as NGDP. Thus labor’s share was probably stable. In contrast, in the US labor’s share of GDP fell by 3.6%, and this largely explains why employment fell, despite NGDP growing a bit faster than weekly wages.”

Compensation of employees rose from 52.9% of GDP in 2007Q4 to 53.2% of GDP in 2013Q4 according to the UK’s ONS. It averaged 53.1% of GDP for all of 2007 and 53.7% of GDP for all of 2013.

14. April 2014 at 11:43

The graph you posted prompts this slightly over-the-top comment. I (like most people) don’t give a fig about NGDP, but I do care about the job market. I believe in class warfare, and I want the class I belong to (the middle class) to win. Screw the rich, screw the poor, I’d like to see them all be middle class. Nothing, but nothing is better for the average working person than a very tight labor market. The only line in the graph I care about is the US employment line. If your macro-economic prescription isn’t forcing that line up as far as I am concerned it is a failure.

14. April 2014 at 11:49

Benny, I ran down that alley with Scott earlier when we looked at Roger Farmer’s bit showing real wages fell quickly in the Great Depression.

Apparently, it’s not that there can’t be “some” give on wages, its that there’s a limit to how much they can give.

Kevin, on paper thats what gets said, but thats not what happened.

What happened is millions of people who couldn’t afford the future balloon payment, not lots of baby boomers, got loans via inflated LTV and took out cash. Taxi cab drivers suddenly owned 4 homes, and ads ran on craigslist looking for people with a decent credit report who could be paid to use it.

My point is the corrupt stuff didn’t happen, we wouldn’t have had the boom in prices.

NGDPLT at 4.5% from 2000, would never have let housing boom happen.

I suspect moreover, that it would have led to FASTER TECHNOLOGY ADOPTION.

That’s the thing I’m wrestling with: Necessity is the mother of invention.

And it seems like anything, including monetary policy, that make adopting new technology not necessary – is bad.

14. April 2014 at 11:59

Kevin –

It’s not normal backwardation if you’re buying on margin. If you’re playing a WTI convergence along with Brent coming up to $110, returns well over 100% are available.

If were Chevron, why wouldn’t I just buy oil futures until they come up to the NPV my replacement cost? Hell of a lot easier than drilling in 10,000 ft of water off Angola.

14. April 2014 at 12:15

Jim Scheltens—

Class warfare? Sorry, we lost the war without a shot fired in our defense. Although if you live in rural America you are so heavily subsidized you are probably winning regardless of class….

14. April 2014 at 12:24

Kevin –

OK. Let’s see if I get the math right.

To buy a futures option of 1000 barrels, you have to plonk down about 7% of the notional amount. If we have a Dec. 2017 WTI future at $82, then we have to place $5700 to secure an option.

If we allow near convergence of WTI to Brent in Dec. 2017 at $107 barrel (given that Chevron is calling for $110 Brent for the year), then the profit would be $25,000 on committed capital of $5700, or a return of 430%.

14. April 2014 at 12:46

Scott,

Off Topic.

Philip Pilkington does a post on the yield curve and I drop by to nitpick.

http://fixingtheeconomists.wordpress.com/2014/04/11/the-yield-curve-and-recessions-against-us-centricism/

“…Okay, so let’s take the UK first. This graph is pretty rough but the green lines are the starts of recessions and the thinner black lines are points when the short-term interest rate rose above the long-term interest rate without causing a recession. The short-term interest rate is the blue line and the long-term interest rate is the red line.

[Graph]

As we can see, the story here is a bit more complicated than in the US. Only three out of the five recessions were precipitated by an inverted yield curve. Meanwhile the yield curve inverted seven times without causing a recession.

This does not bode well for the notion that this correlation might be constant across time and space.

So, let’s turn to Japan. Unfortunately, the data available for Japan is only from during the so-called Lost (Two) Decade(s) and so we will be dealing with a rather unusual period. Nevertheless, it should still prove interesting.

[Graph]

As the reader can see I have not bothered to mark the recessions in this chart. Why? Because it is quite clear that the yield curve never inverted in this period. The short-term interest rate (blue) always stayed below the long-term interest rate (red). What’s more, in this period Japan had five recessions. Including a massive one at the beginning of the 1990s. Clearly these were not correlated with and therefore not caused by an inverted yield curve…”

1) Although typically the central bank policy rate is close to the short term rate on the central government securities, it’s customary to measure the slope of the yield curve using a short-term security yield and not the central bank policy rate.

2) At least on a monthly average basis, the UK yield curve did *not* invert in 1976 or 1981, and it *did* invert in 1973. Given the fact that short term rates are near zero and the 10-year gilt has never yielded much less than 1.6% it could not have been easily inverted before the UK’s most recent recession.

3) The Japanese rate labeled the “overnight” rate is really the rate for Treasury Bills, which is actually appropriate since it’s a central government security. (Note however that the Japanese overnight rate, or “call” rate as its known, was above the 10-year Treasury bond yield from July 1989 through March 1992 with the exception of February and March 1990.) Moreover the Treasury Bill yield has been at or below 0.75% since June 1995 and the 10-year Treasury bond yield has never been much less than 0.5%, so again it would have been rather difficult to invert the yield curve in the past 20 years.

Here’s a paper that looks at eight advanced nations (including the US, the UK and Japan) during the 1970s, 1980s and early 1990s and concludes that the yield curve was useful for predicting recessions in nearly all of them:

http://www.bis.org/publ/work37.pdf

Here’s a paper that looks at the emerging nations and interestingly finds that for nations pegged to the US dollar the US yield curve has more predictive power than the local yield curve:

http://www.ecb.europa.eu/pub/pdf/scpwps/ecbwp691.pdf

14. April 2014 at 13:31

Steven, is there a risk-free arbitrage available?

Morgan:

annualized 4Q to 4Q log growth

GDP C-S 10 city housing index

4.9% 11.1% 1997-2003

5.8% 11.2% 2003-2006

There were a couple years (mid 2003- mid 2005) where high NGDP and high home price growth coincided, but that period would account for maybe 10% of unusual home price growth at the top. So, CS10 went from 83 in 1998 to 226 in 2006. So, you might be able to argue that loose Fed policy from 2003-2005 took CS10 to 226 instead of 200. You still have 117 points of home price growth to explain.

14. April 2014 at 13:55

Kevin, I’d likely put it down to this:

1998-2000 slightly outsized home price growth due to Internet boom.

2001-2002 a more accurate reality

2003-2006 using housing to have the next boom

Again, I’m not arguing against steady growth of housing, even above inflation, I’m going by a sense of excess.

Meaning I had a front seat to the Internet boom and the housing boom, and in both there was an exact moment when things were just NUTS.

And the best part of NGDPLT is that it makes a pie of nominal growth – an exact amount, that if X sector starts eating it, there is nothing for Y Sector to eat.

Which makes “booms” in a given sector actually operate under the gravity of every other sector having to give up and get out of the way.

Pay raises for public employees? No-look loans for subpar credit homebuyers? Investments in software?

Anything can go NUTS, but only if everything goes fetal. And even then, it won’t be as nuts as it was back then.

Could home prices have increased without doing subpar loans? YES. And thats what should have happened.

By how much?

WHO CARES.

What matters is finding out how much ONLY AFTER we make sure the Nutty shit stops.

The danger of trying to shave off the nuttiness with a given model, make it seem like it isn’t worth focusing on ending nuttiness.

And that’s wrong.

14. April 2014 at 13:59

Steven, Any of those oil prices seem plausible to me.

There is some interesting stuff going on with the supply side of the UK economy, which is not well understood. But this post focused on AD and wages. The best way to explain unemployment is to look at NGDP growth and wages.

SG, Yes, that’s one weakness. I’d look at either total compensation, or average hourly wages, if it becomes too much of a problem. However, I still think NGDP would work fine in most cases.

Patrick, Yes, I mentioned that over at Econlog.

Thanks Britmouse.

Benny, No, wages rose about the same in all three countries.

Mark, Thanks for the UK data. Glad to hear the change was pretty small, so my numbers aren’t far off.

Jim, I also focus on jobs.

Mark, I agree that the yield spread is a better business cycle forecaster than most, albeit obviously far from perfect.

14. April 2014 at 14:23

Morgan, we basically agree about NGDP targeting. Except, “booms” in asset prices don’t come out of NGDP, so rising home prices wouldn’t have to come out of anyone’s hide any more than rising bond prices would….which is another reason why it’s a superior Fed target, because it would have prevented them from over-tightening as a result of the same misinterpretation you are making about housing in the 2000’s.

😉

14. April 2014 at 17:29

Kevin,

Well it does tho! NGDPLT ran up over 4.5% right away. It blew past 5%, and all of that would have been a monthly if not weekly ratchet of loan prices higher and higher, until the piper was paid.

The extra construction labor, the taxi cabs drivers with money to spend from taking money out at closing.

I knew an actor couple in Hollywood that lived for three years on a house that they refi’d THREE TIMES from $475K to $1.1M.

All that spending goes poof.

14. April 2014 at 18:28

Morgan,

Those refinances weren’t a product of high NGDP (at least until the last gasp of the boom). They were a product of low long term interest rates. Their house had a higher face value just like a long term bond on the secondary market would have had a higher face value. Just like your friends that refinanced, corporations could add to financial cash flows by paying off old long term bonds that had high rates and issuing twice the amount in new bonds with the same coupon payment at lower rates. Do you believe that low long term interest rates are a sign of a loose monetary policy? Do you believe that low long term interest rates add to NGDP?

15. April 2014 at 00:32

One thing the US is far better at than any other country is hedonic adjustments to the calculation of inflation. Most countries don’t bother, a few countries like the UK bother a little bit. This may account for a lot of the difference in US GDP over Europe, but won’t show up in income data.

For the record, the US is correct to make the attempt to measure the nearly unmeasurable.

15. April 2014 at 04:32

One thing to remember about the UK is that for the last few years there has been an almost limitless supply of high quality 25 to 35 year old labor coming in from the depressed economies of southern Europe. So this is doing some strange things to the UK labor market, good old sticky wages are ensuring current incumbents wages are not falling in nominal terms, but employers are finding no need to raise wages to attract good quality people. So business are not investing in labor saving technologies. So productivity stalls. Just speculation on my part, but I bet a lot of the reasons that this is not translating into overall growth for the UK economy, is that a lot of the newcomers are remitting salary back to their home countries.

15. April 2014 at 04:56

Yikes!

“Chinese Stocks Decline Most in Five Weeks as Money Growth Slows”

http://www.bloomberg.com/news/2014-04-15/china-stocks-drop-as-financial-shares-fall-before-new-loan-data.html

“China GDP Gauge Seen Showing Deeper Slowdown”

http://www.bloomberg.com/news/2014-04-14/china-gdp-gauge-seen-showing-more-drop-than-main-measure.html

15. April 2014 at 05:06

Prof. Sumner,

I don’t understand why there hasn’t been more discussion of Germany’s success with long-term NGDP growth of 2.2% (which seems ultra-low)…..

http://thefaintofheart.wordpress.com/2014/04/14/there-was-no-breakdown-in-the-musical-chairs-model

15. April 2014 at 05:14

Scott – The point I was making was that the oil companies have basically stated in their SEC investor documents that they think the futures curve is dramatically wrong. That’s highly unusual, and a very aggressive and public posture at the same time. As an economist, how do you feel about that? Does the futures curve embody all knowledge? If so, how can the oil companies argue against it? If you were, say, Tom Eizember, Exxon’s chief economist, would you endorse Exxon’s chosen price strategy? On what basis?

Kevin – You’re past my pay grade. I personally think oil futures are the best investment opportunity in the oil markets since the collapse of prices in late 2008. If I can make a 400% return simply following the formal opinion of Exxon and Chevron, well, that’s pretty inviting, isn’t it?

Are there risk free arbitrage opportunities? Wow, I’d have to think about that. I personally think that the oil companies are about right on the price outlook; indeed, it’s not hard to make a case for something of an oil crisis in the 2016/2017 time period. As I have stated many times before (http://blogs.platts.com/2013/11/05/carrying-price/), I think the IOCs business model is unraveling, and pretty fast. Chevron, for example, increased its budget price from $79 / barrel last year to $110 this year. That’s astounding. A budget price, except during recessionary periods, is never above spot. It’s clear why they did this: they needed to in order to make their free cash flow forecasts positive to the investment horizon (call it 2017). That’s a bad place to be, if you’re an IOC.

As a result, I think that oil prices will tend to stay elevated, and the oil business–particularly the high capex end and their service/technology providers–are going to come under intense pressure.

But I don’t know if there’s a risk free play in the deck.

15. April 2014 at 05:38

Kevin,

“They were a product of low long term interest rates.” Yes.

Once NGDPLT went above 4.5%, they would have gone up FAST, if NGDP kept growing to 4.6%, the next month interest rates should ratchet to recover the overshoot, if NGDPLT went to 4.7%, the machine should have raises rates so much, that banks would have decided subpar folks can’t get a loan.

So by memory, sometime in 2004, 30 year fixed interest rates would have pushed to like 7% for prime borrowers in the space of three months, from like 5.5%.

Since we use the term musical chairs here a lot…

When we overshoot NGDPLT in month 1, there are just a few chairs removed, if that doesn’t do it, by month 2 , then 3, so many chairs have been removed EVERY OTHER sector of economy is paying thru nose to borrow money, forcing “give taxi drivers 4 mortgage loans where they take cash out” to die.

15. April 2014 at 08:51

Get rid of inflation, and maximize the willingness of workers and employers to cut wage rates when there is a change in the nominal demand for labor. Won’t be instanteous though.

In a free market, with gradually falling prices, and increasing population, at some point people will learn to connect rising standards of living with falling prices and not rising nominal incomes. No need for a central bank.

15. April 2014 at 09:52

“Benny, No, wages rose about the same in all three countries.”

Doesn’t stickey wages suggest that they would have the same unemployment? We aren’t seeing that. If stickey wages were true we would see the lowest unemployment in the country where wages fell the most. But we didn’t.

15. April 2014 at 10:23

Marcus Nunes:

“Svensson is disgusted with the Riksbank”

http://thefaintofheart.wordpress.com/2014/04/15/svensson-is-disgusted-with-the-riksbank

Wow!

15. April 2014 at 10:45

Prof. Sumner,

Gold has crashed today as a result of a World Gold Council analysis of Chinese gold demand. Interesting read below:

http://goldnews.bullionvault.com/china-gold-041520141

15. April 2014 at 11:28

ChrisA, But remittances shouldn’t prevent that labor from boosting RGDP.

Travis, I think it’s because the growing share of GDP going to German workers has been accompanied by low wage growth and no minimum wage. So neither the left nor the right sees any policy implications.

Steven It’s not at all surprising that people who work in the oil industry might have differing views on where oil prices are likely to go. And those differences actually don’t seem that large to me, given that oil has fluctuated between $40 and $147 in recent years.

Benny, I think you missed the whole point of the two posts—the share of income going to labor differed substantially between the three countries.

15. April 2014 at 16:22

Scott – on remittances, I agree that the immediate salary payments show up in RGDP, but if the money is then sent abroad, there is no multiplier effect on the rest of the economy. Another way of looking at this is the living costs of these newcomers to the UK economy are very low compared with the living costs of the long term population. For instance housing is much more densely occupied, they eat out a lot less and so on. They are in the UK to save money not to have an enhanced lifestyle.

15. April 2014 at 16:46

Chris, I view the mystery as a supply side issue, whereas multipliers (if they exist) affect the demand side.

16. April 2014 at 05:53

Scott –

At $95 / barrel, the oil side of the IOCs’ business is not viable. Even at recent prices around $108, the big oil companies are reducing capex by 4.8% for 2014. Now imagine what would happen at $95!

To better understand this, imagine Bentley College’s President said that nominal tuition would remain unchanged through 2017 at $41,000. Now imagine there were a futures market in Bentley tuition which anticipated that Bentley’s nominal tuition would be only $35,400 in 2017. For a refundable and transferable deposit of $2,100, you could lock-in a $35,400 tuition from Bentley’s tuition which Bentley would have to accept.

Now, either Bentley’s President is right and Bentley will have to absorb costs associated with inflation; or the market is right, and Bentley will have to absorb inflation and reduce tuition by %5,600 per head.

In the former case, Bentley would find itself under a moderate amount of stress. In the latter case, Bentley would have to rethink its whole business approach.

That’s where the IOCs are today.

16. April 2014 at 16:43

Steven, OK, but I was thinking more in macro terms. Those two prices don’t have major implications for the macroeconomy.

17. April 2014 at 05:54

To get from $110 / barrel to $95, you’d probably have to increase the oil supply by something like an additional 0.6 kbpd, representing 0.7% of the oil supply. The coefficient into GDP growth is something like 0.6, so figure the difference between $110 and $95 oil is on the order of 0.3-0.4% of global GDP.

17. April 2014 at 05:55

That’s 600 kbpd, the rest is good as written.

17. April 2014 at 15:44

Steven Kopits,

The futures price of oil isn’t an unbiased predictor of the future price of oil. It is possible for the futures price of oil in 2017 of $95 to correspond to an expected price $110. You need to account for the different discounts & premiums that are inherent in the futures price structure.

That might mean that it is worth it for you to go long on oil futures. It doesn’t necessarily mean that the oil company forecasts are wrong. It just means that the risk premiums inherent in the oil futures market are premiums you are willing to bear.

17. April 2014 at 16:31

Steven, Both supply and demand can move price.

18. April 2014 at 05:57

Kevin –

Let me repeat my comment from above.

Kevin –

OK. Let’s see if I get the math right.

To buy a futures option of 1000 barrels, you have to plonk down about 7% of the notional amount. If we have a Dec. 2017 WTI future at $82, then we have to place $5700 to secure an option.

If we allow near convergence of WTI to Brent in Dec. 2017 at $107 barrel (given that Chevron is calling for $110 Brent for the year), then the profit would be $25,000 on committed capital of $5700, or a return of 430%.

******

If you think the risk premium is 400%, well, guy, let’s hear the narrative.

18. April 2014 at 06:12

Scott –

Both supply and demand can move the price? Well, golly, yes. So your point is?

Interestingly, by the way, in a supply-constrained scenario, neither supply nor demand moves the price very much as long as you stay in the supply-constrained portion of the curve.

If you were in that portion of the curve, the analysis looks much like that of a monopoly price. If you increase the price, demand falls away. If you drop the price, demand revives quickly. Thus, you’d expect a high degree of price stability, even at a high price.

So what do we see in practice?

The oil price has stayed very high in historical terms. But volatility has collapsed. Historically, the standard deviation of the Brent oil price compared to the previous 365 calendar days has been around 10% of the average price. Since late 2011, this has fallen progressively and is now at an all-time historical low of 3.6% (since Brent started trading in 1988).

So where are we as a practical matter? You have a gaping hole between US and UK after 2007 which remains unexplained, other than that US oil import dependency fell by half and the UK went from being a net exporter to an import dependency of 50% during that period. And UK oil consumption has fallen by 19% compared to 2005, putting it within spitting distance of the PIGS, which are down 25-32%, and twice as big a fall as the ordinary oil importers like Germany, the Netherlands, or Sweden. You think that matters? That’s a hell of drop of a key transportation input.

But wait, there’s more. US oil consumption has fallen during that period, too, down 9% since 2005 and actually down a bit since the start of the shale oil revolution. So if dropping oil production and consumption is the leading candidate for the poor supply side performance of Britain–which you yourself have remarked–should we then assume that falling oil consumption in the US was GDP neutral? I don’t think so.

18. April 2014 at 11:50

Steven, My point is that you claimed supply would have to increase to lower the price. I wondered why.

Regarding the UK, I claimed falling oil production was an adverse supply shock, not falling oil consumption.

18. April 2014 at 13:13

Scott,

Oil consumption could fall to reduce the oil price. It virtually never happens outside a recession (if you’re not supply-constrained). So falling oil consumption is unlikely.

Having said that, oil demand in China was actually down in the last few months. Oil is usually a coincident indicator for GDP growth, so take it for what it’s worth. I know, everyone tells me everything is fine in China, but the oil data looks like crap and I really don’t know why. It’s not just sectoral rotation. Everything (gasoline, diesel, etc.) was down in the latest Barclays report.

As for production and consumption, yes, I figured you’d say that. Here’s the counter argument. As production falls, the economy has two choices to meet current or capital account requirements (assuming there’s finite scope for greater trade deficits). It can either find other things to export or it has to reduce domestic consumption of oil, or both.

Now, if you have to reduce domestic oil and gas consumption–by twice as much per capita as Germany or the Netherlands, as it turns out–wouldn’t that show up as a broad based supply shock of the sort that Mark Sadowski has suggested? Isn’t your economy now not broadly impaired for anything requiring oil or gas?

18. April 2014 at 21:07

Steven Kopits,

“Now, if you have to reduce domestic oil and gas consumption-by twice as much per capita as Germany or the Netherlands, as it turns out-wouldn’t that show up as a broad based supply shock of the sort that Mark Sadowski has suggested?”

Are seriously claiming that decreased UK oil consumption is the reason why productivity has declined in government services, wholesale and retail trade, professional, scientific and technical services, and accomodation and food service activities?

Incidentally, here is the change in oil consumption and productivity (GDP per hour worked) between 2007 and 2012 for the 30 OECD nations for which we have oil consumption data via BP, ranked by productivity change.

Country-oil-productivity

1.Korea(+2.5)(+20.6)

2.Poland(+2.1)(+16.4)

3.Chile(+5.3)(+12.5)

4.Ireland(-33.5)(+11.0)

5.Spain(-20.8)(+10.0)

6.Slovakia(-4.2)(+8.2)

7.US(-10.3)(+6.5)

8.Portugal(-23.7)(+5.5)

9.New Zealand(-3.8)(+4.8)

10.Japan(-6.7)(+3.9)

11.Israel(+9.5)(+3.8)

12.Australia(+8.8)(+3.5)

13.Austria(-6.8)(+3.5)

14.Canada(+2.1)(+2.8)

15.Hungary(-23.4)(+2.6)

16.Sweden(-13.8)(+1.6)

17.Germany(-1.0) (+1.4)

18.Czech Rep.(-5.3)(+1.4)

19.Mexico(+0.3)(+1.2)

20.France(-11.7)(+1.0)

21.Denmark(-20.0)(+0.8)

22.Turkey(-4.3)(-0.1)

23.Switzerland(-1.1)(-0.6)

24.Belgium(-6.0)(-1.1)

25.Netherlands(-12.4)(-1.3)

26.Italy (-22.7)(-1.5)

27.Norway(+4.0)(-2.0)

28.Finland(-14.5)(-3.2)

29.UK(-14.5)(-3.6)

30.Greece(-28.0)(-5.8)

The R-squared value is 4.7%. There is no correlation.

19. April 2014 at 07:24

And yet there’s the UK. Second to last on both lists.

It’s a big delta, Mark. What are you proposing as the explanation? What’s the narrative, guy?

19. April 2014 at 09:53

Steven, You said:

“Oil consumption could fall to reduce the oil price. It virtually never happens outside a recession (if you’re not supply-constrained). So falling oil consumption is unlikely.

Having said that, oil demand in China was actually down in the last few months.”

I’m all confused. Are you discussing oil consumption or oil demand?

BTW, a few days ago over at Econlog David Henderson made the following comment:

“I’ve even seen one sharp petroleum economist from the American Petroleum Institute make the same mistake: he presented data on consumption and referred to it as “oil demand.”

http://econlog.econlib.org/archives/2014/04/rudebusch_on_ho.html

19. April 2014 at 10:05

That’s not how statistics is done Steve.

The null hypothesis is that there is no relationship between two variables. The alternative hypothesis is that there is a relationship.

As it turns out, the largest residuals are not from the UK, but from the five countries with the fastest rates of productivity growth, where oil consumption fell an average of 8.9% and productivity increased by an average of 14.1%. And even then the line of best fit only has a slope coefficient of 0.115 (and a p-value of 24.9%).

So this is not a very promising theory.

19. April 2014 at 13:20

Steven, are you honestly arguing that the expected future price of oil is a product of CME margin rules? The expected return of everything is huge when you leverage it 14 to 1. The question is how much do you expect to make compared to your expected variance.

19. April 2014 at 15:25

Mark A. Sadowki,

You once made a comment here specifying exactly what the Fed is allowed to buy, i.e. how much gold, what subset of municipal bonds (there’s a maturity limitation IIRC), other assets (bonds), and of course it can lend in excess of that. I did not save the link… 🙁

19. April 2014 at 15:55

Tom Brown,

I’ve posted some version of that comment dozens of times. The trick is to find the most recent version with the most up to date figures. I believe that is this one:

http://www.themoneyillusion.com/?p=26304#comment-322387

19. April 2014 at 16:54

Mark, thanks!

20. April 2014 at 12:40

Demand vs Consumption

For an observed quantity and price, demand and consumption are often used interchangeably in the oil business.

To quote the FAO (the only place I found discussing this distinction): “In practice, the distinction between demand (as a schedule of quantities as a function of price, other factors held constant) and consumption as an equilibrium quantity at a given price, is frequently ignored. The development of “gap” type models illustrate the common approach of projecting ‘demand’ as a fixed quantity independent of price.”

I tend to think of demand as the demand curve, as a theoretical set of price/quantity relationships at a point in time. However, under most circumstances, demand can only be observed at an equilibrium point, and generally over a larger period of time, in oil markets typically a month or more. I generally work with three month moving averages as my minimum unit of analysis for prices and quantities.

Notwithstanding, for any given period of time, observed consumption for the price prevailing will be the same as demand, to my way of thinking. As a result, consumption and demand tend to be used interchangeably for observed equilibria.

Demand is sometimes misused as a term when forecasts are made. As the FAO writes, future demand is often given as a quantity irrespective of price. When the EIA writes, “we expect China’s oil demand to grow at 5% next year,” I assume that that’s the anticipated growth in consumption, incorporating some implicit view of price changes over the period. It’s not the growth of demand for a given price.

In any event, that’s how I think of the distinction between demand and consumption, and I’d certainly appreciate your view of the matter.

20. April 2014 at 13:13

Kevin –

The price of oil at a specific point in the future should be a function of demand and supply conditions (plus or minus) prevailing at the time.

The value of the oil futures (on the NYMEX) will be a function of i) beliefs about future oil prices, ii) exchange margin rules, and iii) cost of capital. It may also be a function of the availability of capital (eg, Dodd Frank effects) and time preferences of those selling futures. Dodd Frank seems to have materially thinned the ranks of the traders, who look long in futures as a group.)

http://www.zerohedge.com/news/2014-04-16/crude-alert-gartman-now-long-oil

By contrast, the sellers of WTI futures are primarily US independents. Now, WTI spot is $104 and mid 2017 WTI futures are $83. If I believed that WTI would be $104 in 2017, why would I sell futures at $83? That’s more the $20 / barrel, perhaps half or more of profits. Could it because the independents are capital-constrained, and are using hedges as collateral to borrow money to keep the drill bits turning?

Is this about differences of opinion about future value, or a business model that’s either so good that $20 a barrel is cheap, or one so poor that capital at any price is a good deal if it keeps production growing?

21. April 2014 at 03:07

Kevin –

Let me think about this a bit.

I’m featured in Phil Verleger’s morning note today. (I’m moving up to the D-list, much like yourself…)

Phil reviews my Platts articles (http://blogs.platts.com/2014/04/09/citi-chevron-oil-price/), noting:

“In the long run, companies betting on much higher prices will likely have a very unpleasant surprise: potential bankruptcy….The IOCs do not know it but they are manufacturing the equivalent of steam engines in an era where diesel locomotives are becoming the norm.”

Two months ago, Chevron was budgeting with $79 oil; last month they moved it up to $110 / barrel. The futures price has remained in the same vicinity (down a bit). Thus, if the futures price is the guide, Chevron was much too low last year. But it is very, very rare for an IOC to use a budget price above spot and well above the futures value. It happens, but only in recessions when oil prices tank. To do so at a time when oil prices are steady and near historic highs, well, that’s a big deal. (Faced with the same challenge, Shell simply discontinued production and price guidance.)

I think historically in the industry we’ve tend to use the actual value as a rough guide. If spot is $108 and the 3 year future’s at $100, I don’t think that would be too unusual. If spot is at $104 (as is WTI now) and the future’s at $83, well, that will raise some eyebrows.

Now, back to your question. What does a futures price imply about the spot price at that time? I’ll have to think about that a bit and consult some literature.

21. April 2014 at 03:16

Mark –

If you asked me what would happen to an economy if it reduced oil consumption by one-fifth in five years, I would expect that to ding GDP substantially.

If you asked me how much faster such a country could increase oil efficiency in GDP compared to a country with oil consumption dropping at half that rate, I’d say between 0-1% per annum.

Thus, if UK oil consumption fell by 10% more than US oil consumption, then I would expect GDP to be 5-10% lower in the UK. As it turned out, it was 7%.

But it could also be, I suppose, as you seem to contend, that you could reduce oil consumption to zero over any given period without impact on GDP growth.

21. April 2014 at 05:48

Steve, You said;

“Notwithstanding, for any given period of time, observed consumption for the price prevailing will be the same as demand, to my way of thinking. As a result, consumption and demand tend to be used interchangeably for observed equilibria.”

Thus is a very serious error. The terms ‘supply’ and ‘demand’ have absolutely nothing to do with equilibrium quantity consumed. Observations of Q tell us absolutely nothing about changes in either supply or demand. It’s very important to keep these terms distinct in any discussions of the oil market. I know that practitioners often equate the terms, but they are making a very serious error. A change in Q is equally likely to reflect a change in supply as a change in demand.

Never reason from a quantity change.

21. April 2014 at 07:17

Scott –

I’m not reasoning from a quantity change.

But at some point, if 100 units of X change hand, then at the given price and under the given supply conditions, demand was 100 units. Or put another way, as I understand it, consumption is the equilibrium point at any moment in time where the supply and demand curves intersect. For that point (and that point only), demand equals consumption.

Further, when we say “consumption will grow by 5%”, we are saying that the volume at the next period’s equilibrium value will be 5% higher, given the price, supply and demand conditions pertaining at that time.

Or is that wrong?