The best economics data set ever (#1)

Update: People asked for a graph. Marcus Nunes has one for a very similar (but slightly different) data set.

I’m working on turning my blog into a book, and in order to do that I need to give readers an idea of how I ended up where I am today. One obvious need is to explain how I adopted a quantity theoretic approach to monetary analysis, rather than some alternative like the interest rate approach. For me it all goes back to the Great Inflation of the 1960s to the early 1980s.

As an aside, the quantity theory can be defined in several ways:

1. An X% rise in M will be associated with an X% rise in P

2. An X% rise in M will be associated with an X% rise in NGDP

3. An X% rise in M will cause both P and NGDP to be X% higher than otherwise, in the long run.

The third definition is probably the most accurate, and the first is the least accurate.

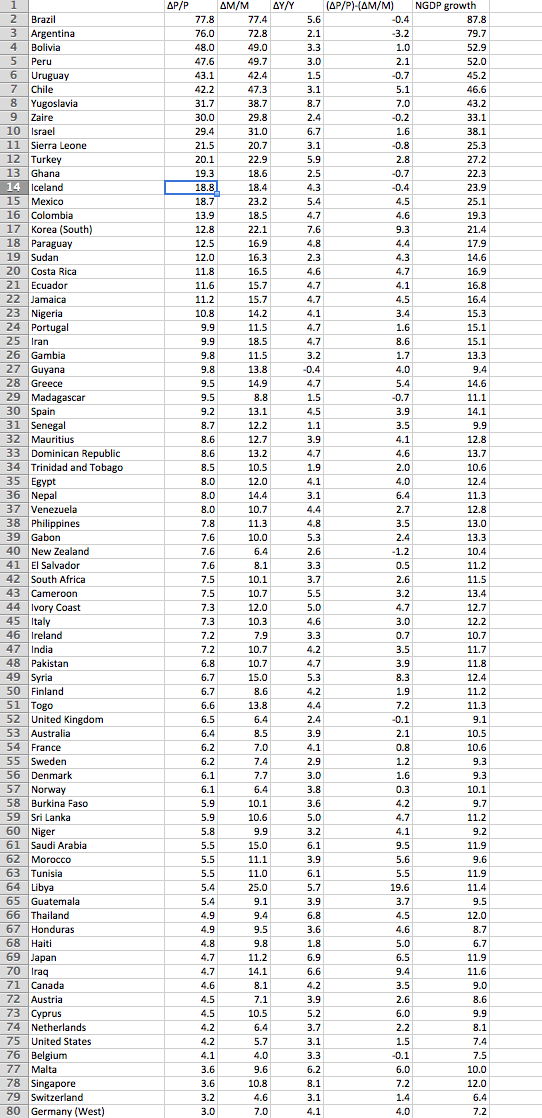

The following data set (from a Macroeconomics textbook by Robert Barro) is so rich in information, that we will spend many posts investigating all the implications. It shows average inflation, money growth and real GDP growth rates over 30 or 40-year periods around 1950-90, for 79 countries:

Right off the bat one notices the strong correlation between the growth rate of M (the monetary base) and P (the price level.) David Hume didn’t have this data set in 1752, but just using his brilliant mind he was able to figure out that if you double the money supply, the only long run effect is for prices to double. Money is just a measuring stick. For about 40 years Argentina and Brazil were doubling the money supply, on average, once every 14 months. And prices were doubling just as Hume predicted. All good, the Quantity Theory of Money (QTM) is triumphant.

Except it’s all downhill from here. I’ve just provided the best possible data set for convincing you of the QTM. Suppose I had only given you the bottom half of the data set? Now the correlation is much harder to see. Or suppose we’d looked at shorter time periods. Again, not so good. Or suppose we’d looked at countries at the zero bound? Now the QTM would have major problems.

The key to understanding the QTM is to hold two thoughts in your mind at the same time. In one sense the theory is logical, indeed blindingly obvious. It’s incredibly powerful, incredibly true. But in all sorts of situations it seems to fail. That’s what we need to figure out.

Before moving on, let’s remind ourselves why it’s the bedrock of monetary theory, and why all other theories fall short. In this data set we are doing the economic equivalent of when scientists expose objects to great heat, pressure, or speed, to get at the essential qualities. We’re looking at what happens with very fast money growth

No other model can explain the correlations we see. Yes, the growth in the money supply might have “root causes” elsewhere, such as budget deficits. But you can’t figure out that Brazil and Argentina would have 75% inflation for 40 years, whereas Iceland would have 19% and the US would have 4% by looking at budget deficits, you need the money supply growth rates to even get in the right ballpark. Note that some countries (the US in the 1970s) printed lots of money w/o big budget deficits.

Nor do interest rate models work. Ironically the only interest rate model that would even come close is NeoFisherism, as the nominal interest rates in these countries would also be highly correlated with inflation. But that model doesn’t tell you how you get those high nominal interest rates. Again, you need money supply data.

Nor will an exchange rate model work. Yes, the (depreciating) exchange rate for Brazil and Argentina was closely paralleling their inflation rate. They saw the local currency price of US dollars rise at around 70% per year over those 40 years. But that doesn’t explain how you cause the currency to depreciate so rapidly over 40 years. Again, you need money supply data. Both the Fisher effect and PPP are just appendages of the QTM.

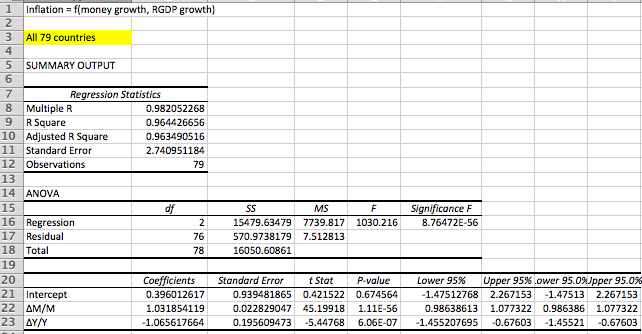

Let’s finish today’s post with the first of several regressions that I’m going to give you–all provided by Patrick Horan of the Mercatus Center:

This is the Mona Lisa of macro regressions. The t-statistic on money growth is 45.2. Yup, I’d say there’s some truth to the QTM. The P-value? One over . . . umm . . . how many atoms are there in the universe? And the coefficient is pretty close to one, within two standard errors. When you raise the money supply at 75%/year for 40 years, you’ll get roughly 75% inflation.

This is the Mona Lisa of macro regressions. The t-statistic on money growth is 45.2. Yup, I’d say there’s some truth to the QTM. The P-value? One over . . . umm . . . how many atoms are there in the universe? And the coefficient is pretty close to one, within two standard errors. When you raise the money supply at 75%/year for 40 years, you’ll get roughly 75% inflation.

Later we’ll see there’s a reason the coefficient is slightly greater than one. Can you guess? (It’s a very hard question.) But let’s finish up by noticing the coefficient on real GDP growth (delta Y). You’ve all been taught that economic growth is inflationary. The people at the Fed tell us that inflation will rise as we approach full employment. Maybe it will, but not because growth is inflationary. As you can see from the regression, economic growth is deflationary, indeed almost exactly as deflationary as money growth is inflationary. So are the Keynesians wrong?

Yes they are! And they are wrong in an interesting way. Let’s suppose their predictions turn out right, and inflation does rise as we approached full employment. Will I admit that I’m wrong? Of course not!! I’m an arrogant economic blogger. Instead I’ll claim that this bizarre outcome is proof of the Fed’s incompetence. They so botched monetary policy that they made inflation procyclical. Indeed they do this so often that some of my commenters think this is natural. Poor Mr. Ray Lopez found a dictionary somewhere that says inflation naturally falls during recessions and rises during booms.

And it’s all a myth. Don’t worry, we’ll explain the mystery of deflationary growth in the next post. And we’ll explain why the coefficient on money growth was a little bit bigger than one in the post after that. All our money/macro questions are answered in this data set, if we know where to look. Put on your David Hume thinking hat, you have lots more info to work with than he had. Indeed Milton Friedman became the second most famous economist of the 20th century mostly by figuring out how this data set allowed us to go “one derivative beyond Hume.”

PS. Here are the two “money quotes” (pun intended) from Friedman:

Double-digit inflation and double-digit interest rates, not the elegance of theoretical reasoning or the overwhelming persuasiveness of serried masses of statistics massaged through modern computers, explain the rediscovery of money.” (1975, p. 176.)

As I see it, we have advanced beyond Hume in two respects only; first, we now have a more secure grasp of the quantitative magnitudes involved; second, we have gone one derivative beyond Hume.” Friedman (1975, p. 177.)

Tags:

10. August 2015 at 18:11

“Maybe it will, but not because growth is inflationary.”

Our definition of “growth” is bogus. GDP is about money supply not wealth creation, so it’s hardly any wonder that people claim growth is inflationary because they *should* skip the incorrect term and say “money creation is inflationary”.

Vancouver, we are told, is booming. They create money via land speculation and then every now and then Ottawa has to shout “everyone devalue!” then off we go again. Meanwhile people decry Quebec for not “making money”.

Will the great age of un-reason ever end?

10. August 2015 at 19:12

An ensemble of random markets gives you this same result:

http://informationtransfereconomics.blogspot.com/2015/06/the-quantity-theory-of-money-as.html

I show that the ensemble average (in angle brackets):

〈i〉= 〈m〉

where i is inflation and m is monetary base growth.

10. August 2015 at 19:57

I assume that lower demand for base money with higher inflation would make the coefficient larger than one.

10. August 2015 at 19:59

Scott, I’ve found the David Hume of our age!

10. August 2015 at 20:33

-Ah, but the person who didn’t rethink that logic would have been right, wouldn’t he have (even if for the wrong reasons)?

10. August 2015 at 20:34

Just one question. You are trying to relate money to prices and NGDP.

Is money used to buy financial assets?

If not, with what are financial assets bought?

10. August 2015 at 20:56

It doesn’t have to be right away, but would you mind providing others with access to this database? Also, how was the data collected?

Not saying that any of your conclusions are wrong in the least, just interested in playing around with it. (A few graphs would also be much more helpful than trying to read through a giant table.)

10. August 2015 at 21:07

Which money aggregate does M represent here?

10. August 2015 at 21:50

Brilliant post! Our world-saving blogger found out that:

1) the two NGDP leaders, Brazil and Argentina, are at the top of his list of countries, while at the bottom is West Germany. Brazil has just been (as of yesterday) downgraded to fall to “junk bond” status, while Argentina is a textbook example of poor performance from initial promising conditions (the country is scarcely populated and rich in natural resources, like Norway is in a way). West Germany was torn asunder by war but outperforms. West Germany has sound money. Coincidence? Probably, though you could argue the society that values sound money is also sound in other areas, like economic productivity.

2) Some metaphysical nonsense is mentioned where Keynesians are right, but Sumner refuses to agree. Since IMO both monetarists and Keynesianists are both wrong (flip sides of the same coin) I won’t go there.

3) My name is dropped, always worth style points, along with Milt Friedman’s. Modesty prevents me from saying I’m a greater economist than M. Friedman, but since Friedman contributed nothing but rhetoric and misinformation (he himself says his greatest theoretical contribution was an obscure correction to the Cobbs production function), you could say that’s true.

I eagerly await Scott’s book…on the usual pirated torrent sites. It would actually be an honor for Sumner if some pirate thought his book is worthy enough to be copyright infringed. Somehow, I doubt I’ll see it however.

10. August 2015 at 21:51

“[David Hume] was able to figure out that if you double the money supply, the only long-run effect is for prices to double.”–Scott Sumner.

Oaky, am I missing something?

What if transactions increase? Could not transactions double in the long run too?

Or is this Hume observation a “ceteris paribus” type of posit?

10. August 2015 at 23:55

David Glasner might quibble on the last quote, as he holds that Friedman was wrong to follow Hume on the price specie flow mechanism (PSFM).

My view is the PSFM works in a network trade world (no global markets) but does not work in a mass trade world (with global prices). Hume looking backwards was correct; Adam Smith, with a better sense of the contemporary Atlantic economy, let his friend’s theory slide for good reason.

http://lorenzo-thinkingoutaloud.blogspot.com.au/2015/08/the-three-ages-of-trade-and-distorting.html

But that is perhaps a footnote to your major point, which I enjoyed.

11. August 2015 at 02:29

Selgin has a good post on Friedman (with a link to a good appreciation of Friedman from David Ladler):

http://www.alt-m.org/2015/08/10/milton-friedman-monetary-freedom/

11. August 2015 at 02:48

Any chance of getting that data somewhere – or should I do OCR?

11. August 2015 at 03:18

As someone who has experience with macro data, I can’t help but feel that some “adjustments” were made. Scott, I suggest you look at it the IMF datasets as they are quite comprehensive (https://www.imf.org/data#global)

11. August 2015 at 03:42

Peter, That’s right, although the full explanation is a bit more involved—the change in the inflation rate is what matters. I’ll explain later

Bob, Good post. I suppose they’d say that inflation falls during the period of high unemployment, which is a lagged effect of recession.

Philip, The money used here is the base. Suppose you buy stocks with a personal check. Then base money is transferred from your bank to your stockbroker’s bank account.

Aaron, The data was collected by hand from an old textbook by Barro.

Mark, The base.

Ben, Hume said transactions rise in the short run.

Lorenzo, I’ll address fixed exchange rate regimes in a later post.

Juhani, What you see is all I have, it takes 10 minutes to enter it by hand.

HoneyOak, Can you be more specific? Every similar data set I’ve ever seen for the period shows essentially the same pattern. What do you find odd?

11. August 2015 at 03:53

Scott, don’t you think the RGDP / inflation stats are a bit endogenous? Also, can you post a scatter plot? Maybe it would be more fair to do natural log of your explanatory variables and see how the regression looks.

-Ben

11. August 2015 at 04:59

Suppose the truth is: y = bx + cz, but you estimate a simple regression y = Bx, so you have omitted variable bias.

Moving down your list of countries:

If the variance in x is very big, relative to the variance in z, this omitted variable bias won’t matter much. You get only a small bias in B, and the R-squared will be high.

If x and z are uncorrelated, you get no bias in B, but a lower R-squared.

If x and z are negatively correlated, you get a downward bias in B. In the limit, you get Milton Friedman’s thermostat result, where B = 0.

That’s my explanation for why the QTM performs worse and worse as you go down the list of countries.

11. August 2015 at 05:07

Scott: Okay, that is what Hume said in his time and place in a relatively ststic economy…but today we have a globalized economy and capital gluts—it would seem an increase in demand or money supply would be met by an increase in trade and added productive capacity, and we see permanent increases in transactions…

This seems obvious to me…I must be missing something

11. August 2015 at 05:11

Ben, As far as natural logs, these are already percentage changes.

Inflation is certainly endogenous, but I’ll later argue that long run growth is not related to money growth.

I’m not sure why people keep asking for a scatter plot, isn’t it obvious what it would look like? The points will all lie close to a 45 degree line.

Nick, That’s right, and I was going to point to Bretton Woods and inflation targeting as two examples of regimes where the coefficient on money would be biased for that reason.

11. August 2015 at 05:12

Ben, Yes, Hume said that too, but only in the short run. On the long run money is neutral.

11. August 2015 at 05:35

Ben is correct. if you are going to do a regression on ratios you should take logs first. If you run off non log values then your large values are too large.

Also, instead of deltaX/X it should just be Xt / X0, the ratio of the ending value to the starting value (which is close because Xt/X0 = deltaX/X + 1), unless there is reason to believe that this relationship did not hold prior to X0.

If you can put the data in a copyable format and repost we can definitely tighten up the analysis.

11. August 2015 at 05:55

Njnnja, Are you saying that the percentage changes should have been first differences of logs? If so, I agree. However it’s not going to make much difference, as it will effect the money growth and inflation in a similar fashion. And to be honest, I’m not sure whether Barro did that already, I am at home and don’t have the textbook with me.

If someone can get the textbook, they might be able to figure out where he got the data, and whether he used logs, but the easiest solution might just be to use data from the IMF or world bank, or something like that.

In any case, I’m nearly 100% certain that all the theoretical implications I draw from this data set would hold up with a more rigorous study. I’m not saying anything that’s even mildly controversial for people who have studied money demand. This is just an intro for outsiders.

11. August 2015 at 06:00

Scott,

Some related literature:

McCandless & Weber, Some Monetary Facts. https://www.minneapolisfed.org/research/quarterly-review/some-monetary-facts

Emiliano Basco, Laura D’Amato, Lorena Garegnani. Understanding the money – prices relationship under low and high inflation regimes: Argentina 1970-2005. http://www.bcra.gob.ar/Pdfs/Investigaciones/WP%202006%2013_i.pdf

And finally a plot showing Argentina´s fiscal deficit (with and without interest payments) and money printing.

https://pbs.twimg.com/media/CMIgUYdW8AAqF1j.jpg:large

11. August 2015 at 06:21

With respect to your point about the coefficient on the real GDP term, I would think it would be relatively simple in terms of the AS/AD model. For instance, if you have a right-ward shift in long-term aggregate supply, then in equilbrium you would think that there is also a right-ward shift in short-term aggregate supply. In this case, the increase in Real GDP would be consistent with a decrease in inflation.

11. August 2015 at 06:30

One interesting point on the chart is the top 7 nations were in South America which was the main area of US/Soviet blundering Foreign Policy until 1974 Oil Embargo made the Middle East our/Soviet blundering focal point. (Growing up in the 1970s/1980s I remember the nightly news had reports of South/Latin American coups once aweek and was not treated like a major event.) So how much of the correlation of money supply and inflation was a function of an era of consistent Civil War? How does the data change after 1990 or even 1980?

11. August 2015 at 06:52

Yes combining the 2 recommendations would get ln(Xt/X0) = ln(Xt) – ln(X0) = first difference of log values is the better metric.

I’m sure it won’t make much difference to the overall conclusion, but it should make a difference to the coefficients and especially the residuals. The residual error of 2.74 means that your 95% confidence interval corresponds to something like a window of 4% inflation (annual compounded) for a relatively low inflation country like the US – so anywhere from 2% to 6% compounded over 35 years. And second if something is worth doing it’s worth doing right so that other bloggers don’t have something to say what a dummy prof. Sumner is. 😛

11. August 2015 at 06:58

Njnnja, Fair point. As you know, when dealing in ordinary percentages you can’t add inflation and real growth to get NGDP growth. If you look at the final column, which I had Patrick calculate, we assumed that Barro was suing ordinary percentages, so we adjusted the math accordingly. But perhaps Barro was already reporting first differences of logs, that would be more useful in a table structured to look vaguely like the Equation of Exchange.

11. August 2015 at 07:03

Alex, Thanks for that info. What does the green line (MB) for Argentina represent? What units?

John, That’s right.

Collin, Inflation gets dramatically lower after 1990, but even today places like Argentina and Venezuela have very high inflation, and Brazil is a bit higher than western countries.

11. August 2015 at 07:06

Scott, same data set used here to illustrate your “Quizz”;

https://thefaintofheart.wordpress.com/2013/03/26/scotts-quiz-illustrated/

11. August 2015 at 08:06

Scott, I used to work as an RA that involved researching macro data-sets used in publications. Without a fault (out of 16 ish) there was always some unaccounted filter or adjustment that was applied to the data by the academic researcher. I suspect that since there is little quality control in the standard publication process, the academics have a tendency to do what they like without sufficient documentation. Institutions such as the IMF, BEA, World Bank, and the OECD have strict data preparation/cleaning processes that ensure that at least one person (who is not an overworked phd student) has looked at the data. It could be that these adjustments do not impact your results however they may impact the specific examples that you choose to highlight the theory. Considering how easy it is these days (I would not feel comfortable excluding anything past 1990) I recommend that you collect a modern data set.

11. August 2015 at 08:28

Scott, how do you know which direction the causation runs? A regression is not enough for that.

11. August 2015 at 09:08

That growth is deflationary is simply a mathematical consequence of the fact that we measure growth by taking NGDP and deflating it using a price index P. If P correlates with money growth, and money growth correlates with NGDP growth, “real” GDP growth *has* to be negatively correlated with inflation. It literally could not be otherwise. Saying saying RGDP%c negatively correlates with P%c is the same thing as saying (NGDP/P)%c negatively correlates with P. Uh, duh, you put P in the denominator right there.

However, if we defined growth as something other than increasing “real” GDP we might come up with reasons that aren’t tautological why growth should be deflationary. Those reasons will be correct, for the definition of growth they are associated with. But technically, they’re unnecessary. If we believe RGDP is a “real thing” then growth is deflationary by definition.

Personally I think RGDP is an illusory fiction, but I actually agree with the idea that “growth is deflationary”-in fact it’s something I’ve been saying for quite some time now. So I don’t want you to think I’m giving you a hard time, but you’re hardly discovering fire here.

11. August 2015 at 09:13

Thanks Marcus, I added a link.

Honeyoak, I assure you that you get almost exactly the same results with any data set from this period. I’ve seen others and the results are always like this.

I’m not interested in post-1990 data because of the widespread adoption of inflation targeting. I’ll explain that problem in a few days, in the 4th post of the series.

People need to focus on the big picture, none of these regression results are driven by quirks in the data, they are all 100% rock solid, and uncontroversial.

Ilya, For that you need theory. We have theory explaining M–>P, but not in the other direction. Plus you have some natural experiments, like when monetary easing in 1933 caused inflation.

11. August 2015 at 09:28

Scott,

The green line is the change in the monetary base (currency in circulation + bank reserves at the central bank) from t-1 to t (end of period values) divided by NGDP in t.

Alex.

11. August 2015 at 12:30

Barro has a page on his profile linking to all the datasets he uses.

http://rbarro.com/data-sets/

11. August 2015 at 13:54

@Nick Rowe

The direction of the bias depends not only on the sign of the correlation between the regressors, but also on the sign of the coefficient. E.g. for c < 0 and x and z negatively correlated, the bias in B is positive.

Also, you can have low R-squared in a correctly specified model where the disturbance has much higher variance than the regressors.

11. August 2015 at 16:35

Actually this is a well written post.

Only quibble is the comment that money is a “measuring stick.”

Other than that, great from top to bottom.

11. August 2015 at 16:50

@Nick Rowe

The direction of the bias depends not only on the sign of the correlation between the regressors, but also on the sign of the coefficient. E.g. for c < 0 and x and z negatively correlated, the bias in B is positive.

Also, you can have low R-squared in a correctly specified model where the disturbance has much higher variance than the regressors.

11. August 2015 at 17:14

Sumner’s “This is the Mona Lisa of macro regressions. The t-statistic on money growth is 45.2. Yup, I’d say there’s some truth to the QTM.” is misleading. The question is not whether there’s ‘some truth’ in the QTM but whether it predicts anything. It does not, simply cause velocity V on the LHS of the equation varies.

BTW, short term money neutrality (which Sumner disputes, though he concedes–IMO rather strangely–that long term money is neutral, which he should not concede but at least he’s a bit honest) also would give a “45 degree plot”. It’s in the definition of money neutrality.

11. August 2015 at 17:24

Ray:

“The question is not whether there’s ‘some truth’ in the QTM but whether it predicts anything. It does not, simply cause velocity V on the LHS of the equation varies.”

No, the question is whether there is some truth to the QTM. There is. There is no reason to expect V to fluctuate in the long run because of an increase in the quantity of money (subject to certain considerations of course).

If everyone’s money balances doubled, why would that lead to any permanent change in V? It shouldn’t, which is why despite all the myriad of factors that can affect V, despite the millions of possible choices people can make, we are still able to see some stable correlation between M and P in the long run, most of the time.

This is not to say that a rise in M causes a proportional rise in P, only that even with all the factors that might affect P, sound economic theory concludes that the cause of the rise in P over the long run, is the rise on M.

Surely you are not so misinformed so as to believe that the reason prices have risen since 1913, was caused by something other than the rise in M? Please wake up, you’re starting to disappoint.

11. August 2015 at 17:37

Ray,

Put it this way:

You agree that P = D/S.

Price equals demand (in dollars spent) divided by supply (quantity of goods).

This is a mathematical necessity.

There is no possible concievable way that prices can change OTHER than through a change in demand, or a change in supply, or both.

Agreed? Good.

Now we know that prices have risen quite substantially since 1913. Even the government’s fudged and constantly changing statistical methods designed to hide price inflation, has reported a significant rise in prices since 1913.

Agreed? Good.

So there are two and only two (actually three) reasons for why prices could have risen.

Either nominal demand has gone up, or supply has gone down, or a combination of the two.

Agreed? Good.

Now ask yourself if the cause for prices having risen since 1913 is only a fall in supply. That we can rule out without even thinking more than 2 seconds, since in order for prices to have risen that much by way of a fall in supply, would be if the country has undergone a collapse on par with the collapse of the Roman Empire. So you should agree that we can mathematically rule out falling supply as a cause.

This leaves rising demand in dollars as the ONLY cause. It is literally impossible for there to be any other cause, since there is only supply and demand, and we just ruled out supply.

The argument that the cause for the rise in prices since 1913 must be a rise in the quantity of money (and the concomitant volume of spending), IS the QTM.

Yes velocity can fluctuate. But there is no way in hell that the rise in prices since 1913 could have occurred only by a rise in velocity without any additional inflation in the supply of money. It is unthinkable. The rise MUST have been caused by an increase in M, period. That’s the QTM.

If you deny this, then you have no business discussing economics, no business anywhere but with your nose inside textbooks and on historical price trend reports, until it sinks in.

11. August 2015 at 17:51

@MF – I think you’re making a big mistake in dealing with aggregate figures, which is not your area of expertise. Your equation: P = D/S is not sourced, and I’ve never seen it in that form. At best you can say Demand and Supply are correlated by a price. And actually the Equation of Exchange does a good job in capturing this dynamic, but price and quantity are not divided into each other but multiplied by each other on the RHS.

Anyway, none of this math goes to my central thesis: we can agree that the inflation of money has produced changes in price, but so what? Money creation is neutral, and any inflation usually (unless you are foolish, like a senior citizen relying on a fixed income from government) is harmless: people will adjust. Short term, as Ben S. Bernanke says in his econometrics paper of 2003, it has between 3.2% to 13.2% effect out of 100% on the economy’s change, year to year. Most people would agree with Ben S. Bernanke that while this may be statistically significant, it is de facto trivial, don’t you agree?

11. August 2015 at 17:55

@myself – a correction – I see your attempt is D = P*S, which roughly correlated to the Equation of Exchange. Still, it does not address why this accounting identity has any relevance looking into the future. The issue is whether monetarism has any predictive effect. Looking backwards, monetarism via the Equation of Exchange simply says: “what is, is”. Hardly of any use. David Hume would agree. Sumner btw has conceded that long-term monetarism is useless, and him and the neo-Keynesians cling to the fantasy that 3.2% effect is a big deal. Trying to justify their existence.

11. August 2015 at 20:18

Ray,

“@MF – I think you’re making a big mistake in dealing with aggregate figures, which is not your area of expertise. Your equation: P = D/S is not sourced, and I’ve never seen it in that form. At best you can say Demand and Supply are correlated by a price. And actually the Equation of Exchange does a good job in capturing this dynamic, but price and quantity are not divided into each other but multiplied by each other on the RHS.”

No, that is incorrect.

If the demand for a supply of goods is $100, and there are 100 units of that good, then the average price per unit must be $1.

This is equivalent to P=D/S.

Price is not merely correlated with demand and supply. Price IS the ratio between money spent on a good or goods, to the supply of that good.

When you exchange $5 in spending for 2 hamburgers, you are paying an average price of $2.50 per hamburger.

The equation P=D/S works at both individual exchanges and all exchanges together. In the aggregate, which is actually an area of my expertise thank you very much, which is why I know to use it so sparingly, P=D/S can be understood as the price level equalling total dollars spent divided by all goods sold. The common denominator is an existant, a conception of goods being homogeneous.

Yes goods are not actually homogeneous, but it is absurd to say that we have no idea if prices in general are rising over time or falling over time. We know that prices in general are rising over time. As soon as you say that, you are presuming the equation P=D/S is meaningful, but not literal.

“Anyway, none of this math goes to my central thesis: we can agree that the inflation of money has produced changes in price, but so what?”

Your thesis is not the point here. The point here is an increase in the supply of money since 1913 is not only “a” factor that explains the rise in prices, but is the SOLE factor.

Do you deny that? Do you actually believe that the rise in prices since 1913 was caused by something other than an increase in the quantity of money?

If you do not deny this, then you are conceding that the QTM is correct.

“Money creation is neutral, and any inflation usually (unless you are foolish, like a senior citizen relying on a fixed income from government) is harmless”

No, I already explained to you multiple times how and why money is not neutral on any timescale.

You already conceded that money is not neutral when you said you believed the effect of central banking is in the range of 3.2% to 13.2%. That means money is de facto, effectively, non-neutral.

A neutral money is a contradiction in terms.

“Short term, as Ben S. Bernanke says in his econometrics paper of 2003, it has between 3.2% to 13.2% effect out of 100% on the economy’s change, year to year.”

Which means money is not neutral. Money having a non-zero effect, of anything higher than 0%, implies money neutrality. 3.2% is not zero. It is non zero.

“Most people would agree with Ben S. Bernanke that while this may be statistically significant, it is de facto trivial, don’t you agree?”

No, it is de facto non trivial. Higher than or equal to 3.2% is de facto non-neutral.

I already explained this, why on Earth are you asking me if I agree? Are you drunk?

“I see your attempt is D = P*S, which roughly correlated to the Equation of Exchange.”

No, I did not “attempt” to write D=P*S. If I attempted to write that, then I would have written that.

I meant to write P=D/S (which is mathematically equivalent), so as to show you that if a price or a set of prices changes, then it MUST be by way of either demand changing, or supply changing, or both.

There is no other way for prices to change.

Do you deny this? Answer the question.

“Still, it does not address why this accounting identity has any relevance looking into the future.”

You are still missing the point.

Economic theory is not meant to, nor is it capable to, predict the future.

The QTM, the law of marginal utility, the law of demand, these are economic principles that are always true, but that does not mean they have to allow us to predict our own future learning paths and our future actions.

Mathematical laws, laws of logic, economic laws, these are rationally grounded concepts that allow us to know what it even means to predict future economic phenomena. They are not obligated to predict my own future learning. If they could allow me to predict my own future learning, then I would have learned something before I actually learned it, a clear contradiction.

This contradiction is reality’s way of telling us that there are TWO classes of knowledge, not just one as you are implying by demanding that all knowledge be positivist/empirical.

“The issue is whether monetarism has any predictive effect.”

No, the issue the explanation for prices rising over the long run, given that production and supply is increasing in the long run.

The only explanation for that is an increase in the money supply.

But this cannot predict the future, because the QTM does not predict what the future supply of goods will be, and it does not predict what the future demand for money will be.

“Looking backwards, monetarism via the Equation of Exchange simply says: “what is, is”. Hardly of any use.”

Then mathematics and formal logic are of no use to you.

But that does not mean they are of no use to everyone.

Some of us find logic and deductive reasoning highly useful, not as predictive tools but as tools that help us understand what IS going on in the world.

“David Hume would agree.”

Ugh.

” Sumner btw has conceded that long-term monetarism is useless, and him and the neo-Keynesians cling to the fantasy that 3.2% effect is a big deal. Trying to justify their existence.”

Don’t care. You already conceded money is not neutral.

11. August 2015 at 20:20

Typo:

Meant to write:

“Money having a non-zero effect, of anything higher than 0%, implies money non neutrality.”

11. August 2015 at 20:48

US printing seems to activate spare capacity in far-flung places on the Pacific Rim. isn’t long-run growth probably improved when we accelerate 3rd world development and improve Indonesian IQ via nutrition, for example? these convergences r to be expected in the long run, maybe, but it seems like improving demand and therefore improving the returns to the easiest aspects of sound capitalism in poorer countries should make emergence from the frustratingly stable deadbeat political equilibria a bit easier, likelier

12. August 2015 at 00:52

As a potential international reader of your future book, I’d like to let you know that I hope very much it is not going to be a U.S.-centric one on the explanation of the Great Recession. So, should you explain the Great Recession with the restrictive monetary policy by the Fed (which I would support), you should in my opinion keep in mind that that was a global phenomenon. So far, I have not found a satisfactory and compelling answer to the question why so many countries experienced a deep recession at the same time. Was it because they also had restrictive monetary policy or because of trade linkages? In my opinion, your book would gain a lot if it touches on this question. I am aware though, that this is hard to do and you probably know U.S. data best.

12. August 2015 at 07:48

@fran- indeed, good observation. Charles Kindleberger asked whether the smaller trade linkages of the late 1920s could have caused a Great Depression world wide, and concluded, as do I, that it was not the trade linkages per se that caused world depression, but the ‘contagion’ factor akin to shouting ‘fire’ in a crowded theatre. Sounds plausible and is also a reason that economics will never be a repeatable, exact science (much to the chagrin of our host).

12. August 2015 at 07:55

@MF – you think 3.2% out of 100% is important? Well then, if we ever discover $1 M dollars, finder’s keepers, then you can have $32k and I will get the remainder, $968k. Fair’s fair.

As for your conceding that economics is only backwards looking, with no predictive power, I would agree, and while you may find economics interesting given this fact, I bet 96.8% of the population will ignore economists if that fact was accepted. And it’s one reason professional economists like Sumner pretend they can divine the economy short term; it gives them relevance to the 96.8% of the population that expects economists to predict the future.

12. August 2015 at 08:03

Alex, Thanks. Note that this data point doesn’t, by itself, get us the inflation rate.

Thanks James, I don’t think that includes this data set, does it?

Dotsn, Always keep in mind that money is neutral in the long run.

fran, Very good point, I’ll try to remember that.

12. August 2015 at 12:29

Scott,

“No other model can explain the correlations we see”

You could explain the correlation by choosing to read the MV=PQ equation from right to left, rather than from left to right, with MV being seen as the dependent variable and PQ being seen as the independent variable. This interpretation would also help to explain why the correlation you highlight sometimes breaks down.

12. August 2015 at 12:43

Apparently, many people do not understand the difference between an equation and an identity.

12. August 2015 at 12:52

Beefcake the Mighty,

Which is weird, given that this is textbook stuff. Knowing the difference between the quantity theory and the equation of exchange really is the first thing you should learn to understand the QTM.

12. August 2015 at 13:27

Scott defines the quantity theory as: “An X% rise in M will cause both P and NGDP to be X% higher than otherwise, in the long run.”

This amounts to assuming that the equation of exchange expresses a causality which goes from left to right, rather than from right to left.

He then says that “No other model can explain the correlations we see”. But you can actually explain the correlations by simply dropping the assumption that causation runs from left to right in the equation of exchange. Dropping this assumption can also help to explain why the correlations break down.

12. August 2015 at 13:28

@Ray Lopez: Personally, I don’t find the pure contagion argument convincing. To me, this is at odds with efficient markets and rational expectations and it doesn’t really offer an in depth explanation. I can understand that in a crowded theatre a panic can be offset if someone screams fire. But it matters if the theatre is crowded or more than half empty, in which case everyone ‘knows’ the exits can be reached safely.

With regard to the Great Recession: I think that in many countries the stance of monetary policy could also have been restrictive at the same time prior to the crisis. The argument could go as follows: The steep rise of the oil prices at the time prior to the crises turned central banks around the world blind on the eye that should focus on business conditions. Instead, they only focused on inflation and by doing so, they ultimately made monetary policy conditions more restrictive than necessary. This is just a guess though, I have no data or other support for that claim. But it could be evaluated, f.e. by looking at how often monetary policy communications contain the word ‘oil’ prior to the crisis in different countries. (Maybe something for Scott and his book?)

12. August 2015 at 17:01

Ray:

“MF – you think 3.2% out of 100% is important? Well then, if we ever discover $1 M dollars, finder’s keepers, then you can have $32k and I will get the remainder, $968k. Fair’s fair.”

That comment is ridiculously absurd. You are rhetorically asking me whether 3.2% is “important”, because YOU are the one saying that 3.2% to 13.2% (again, why do you keep saying 3.2% as if the lower bound is what it is on average? 3.2% to 13.2% means on average it is somewhere in the middle) is “de facto” unimportant.

You were trying to convince me to dismiss 3.2% to 13.2% as unimportant.

Now you’re saying on that basis I would have no problems with giving away the obverse of that?

What you should be saying if you’re going to put your money where your mouth is, is that because YOU don’t think 3.2% to 13.2% is important, then YOU should have no problems with giving me 3.2% to 13.2% of everything you earn.

Well? Fair’s fair right? According to you, you would be giving me “de facto” zero, right?

Oh what’s that? The percent 8%, which is very much in the range Bernanke found, is an “important” number of dollars to you after all? That it is not de facto zero?

Are you drunk? You write such contradictory, fallacious, obviously wrong comments.

As for whether 3.2% is “important”, all I am saying is that a range of 3.2% to 13.2%, IS BY YOUR OWN CRITERIA, and your own admission, merely sufficient evidence that money is not neutral.

You are just making an arbitrary assertion by denying a fact, totally ignoring the implication that if the range of 3.2% to 13.2% is not enough to make money non-neutral, then you would be having to explain what WOULD the range have to be to make money non-neutral, and importantly, which you had better address, is why THAT range, but not 3.2% to 13.2%.

Well?

You would be compelled to pull a range of numbers out of your derriere, because you have already left the realm of logic and science by unscientifically dismissing the range of 3.2% to 13.2%!

“As for your conceding that economics is only backwards looking, with no predictive power. I would agree…”

How in the world can I “concede” that to you when I was the one who tried to convince you of it after you said economics should be predictive?

I could only “concede” something to you if I previously held a particular opinion that you convinced me was wrong. Then I would have “conceded” something to you.

But in this case, now you’re actually agreeing with the argument that economics is not predictive?

Wtf!?

First you said the QTM should be dismissed because it doesn’t predict.

Now you’re saying I have “conceded” to you that economics is not predictive and that you agree!?!?

Huh!?!?

Ray your ideas are massively corrupted. If there was such a thing as a brain defragmenting or reformatting treatment, I would pay for your treatment.

“…and while you may find economics interesting given this fact, I bet 96.8% of the population will ignore economists if that fact was accepted. And it’s one reason professional economists like Sumner pretend they can divine the economy short term; it gives them relevance to the 96.8% of the population that expects economists to predict the future.”

YOU JUST SAID BEFORE that the QTM should be dismissed because it doesn’t predict. That to be useful, economics principles and ideas have to be able to predict.

Now you’re cavalierly guffawing at Sumner trying to do exactly what you just said economics should do?

Do you know how much of a chore it is to wade through the contradictions in your posts?

You say one thing, but then you say a totally opposite thing as if you never said what you said previously.

Try to imagine what it would be like for someone to read comments that constantly contradicts.

Do you think that would be fun?

12. August 2015 at 19:10

@Philippe – “you could explain the correlation by choosing to read the MV=PQ equation from right to left, rather than from left to right, with MV being seen as the dependent variable and PQ being seen as the independent variable” – right on brother! This is of course tantamount to saying that monetarism is dead, and the Fed follows the market. I concur.

@MF – due to tax reasons working offshore, I paid no US taxes last year, as my AGI was zero. Been that way for years. So you can have 3.2% to 13.2% of zero. And these numbers are from Ben S. Bernanke’s 2003 FAVOR paper, showing the Fed has very little influence over the economy. If Bernanke is saying this, you should be paying attention.

13. August 2015 at 03:56

[…] the data set of 79 countries (in this post) there were 12 cases where inflation was higher than the money supply growth. In each case, real […]

13. August 2015 at 04:21

Philippe,

I think you need to re-examine the equation and also what Scott says before you go on discussing this topic.

13. August 2015 at 05:06

[…] 3. Money and inflation chart […]

13. August 2015 at 05:42

Philippe, That’s not a model. For a model you need a causal mechanism. Furthermore, the advanced QTM can explain the various discrepancies better than any alternative.

And don’t forget that the QTM says that money supply increases will be inflationary if exogenous, even if done for many different reasons. No other theory gives you that.

15. August 2015 at 20:53

[…] Believe it or not, I actually like Scott Sumner’s recent series (1, 2, 3, and 4) using empirical data to discuss the quantity theory of […]