Take me to your leaders

Back in the Great Depression the inflation hawks said two things; monetary stimulus would do nothing (it was just pushing on a string) and it would do too much, producing hyperinflation. Keynes is now viewed as a genius, because he just made one of these two errors; assuming monetary stimulus would do nothing.

In the 1990s the BoJ said that monetary stimulus would no nothing, or else it would produce runaway inflation. For some strange reason Japan could not produce the 2% inflation almost all other developed countries were experiencing. It was all or nothing.

And here’s Richard Fisher:

Until then, I argue that the Fed is, at best, pushing on a string and, at worst, building up kindling for speculation and, eventually, a massive shipboard fire of inflation.

I don’t even know that that means. Does it mean he doesn’t see a demand shortfall, and hence hopes QE fails? It would seem so because “at best” policy will completely fail to boost AD. That’s right, 2% inflation is not the best outcome, it would be better if policy failed and inflation stayed below 2%

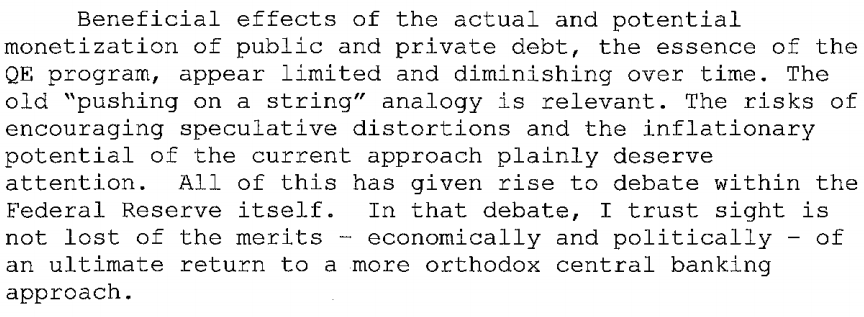

And here’s Paul Volcker.

I actually couldn’t block and copy this because it’s typed on such a old rusty typewriter than it could not even be transferred to notepad (or text edit.) So I took a photo and copied the paragraph.

In any case, I don’t even know what that means. If you assume the most logical interpretation, then he might be saying something like Fisher. But in that case the grammar is poor. Or maybe there is some other meaning that went way over my head.

Here’s another way of making my point. Current Fed policy has led to below target inflation. I assume that the “pushing on a string” outcome means inflation might stay below target. And I assume the other risk is that inflation will be above target. In that case, precisely what monetary policy does Volcker think is needed to actually hit the target?

The conservatives started by claiming the various QE policies were too inflationary. When the inflation didn’t showed up the fallback position was that it was just pushing on a string. Can someone point me to the macro model that says an expansionary policy might produce 0% inflation, or high inflation, but nothing in between? And who are the intellectual leaders that created this model?

PS. I apologize for mocking Volcker’s old typewriter. I still lack a laptop, type with two fingers, and got my first cellphone a year ago. Who am I to talk?

PPS. And what did Fisher mean by this?

If the Fed’s monetary policy were the stuff of Shakespearean drama with a prototypical five acts, one might say we are in the last scene of the third act of a play titled “The Grand Experiment in Modern Monetarism.” We will not know until the next two acts whether the play will end felicitously or otherwise.

There aren’t any monetarists on the FOMC, are there? And if there were, they’d be in the hawkish wing, wouldn’t they? So what does Fisher mean by “modern monetarism.” And who are its leaders? Friedman, Schwartz and Brunner are all dead, and Meltzer’s in his mid-80s. I don’t get it.

I feel like the little green man getting out of the flying saucer—“take me to your leaders.”

PPPS. I suppose Fisher might have been referring to . . . no, even I’m not that deluded.

HT: Ricardo

Tags:

5. June 2013 at 05:03

The governor of the bank of Israel, Stanley Fischer:

“There are those who support setting a nominal GDP target. I think that this is very impractical. The data that we receive on nominal GDP are very unstable. There are changes of whole percentage points between the various estimates of GDP. For this reason, I think that there is no reason to use nominal GDP as a target”.

http://www.boi.org.il/en/NewsAndPublications/PressReleases/Pages/4-6-2013-I.aspx

(I had only the Hebrew version yesterday. Now there is also an English translation)

5. June 2013 at 05:05

It is important that he said it, because some people believe he inexplicitly did target NGDP during his 8 years as a governor.

5. June 2013 at 05:08

Are you blogging all this from an iPad then? Is that why you type with two fingers? I thought that news profile of you said you have a Mac?

Btw, I hope everyone has seen this by now (just had to post it): http://dilbert.com/strips/comic/2013-06-03/

5. June 2013 at 05:09

Jonathan, that’s weird, Evan Soltas assured us that Fischer was essentially an NGDP targeter. Perhaps he approves of working according to an implicit discretionary target, but doesn’t want to be bound by the official figures?

5. June 2013 at 05:12

Noah Smith is another commentator who has explicitly stated the argument you have just set forth:

That any “unconventional” monetary stimulus might produce discontinuous effects on inflation, where stimulus builds and builds, right up until the moment when the market realizes that the Fed is serious, and then a sudden shift in expectations produces hyperinflation.

http://noahpinionblog.blogspot.com/2012/12/the-omnipotent-fed-idea.html

And if you’re wondering why in the world this story would be true, I agree. It seems ludicrous.

5. June 2013 at 05:15

Saturos, I’m not surprised by that comment. I’ve done some posts showing why revisions are not a significant problem.

I use two fingers on my iMac.

5. June 2013 at 05:16

SG, Interesting, but I can’t imagine a model with ratex where that would be the outcome.

5. June 2013 at 05:18

Sorry, I meant Jonathan.

5. June 2013 at 06:02

“Jonathan, that’s weird, Evan Soltas assured us that Fischer was essentially an NGDP targeter. Perhaps he approves of working according to an implicit discretionary target, but doesn’t want to be bound by the official figures?”

Perhaps he meant Stan Fischer – the Israel central banker – and not the ultra-hawkish Richard Fisher?

Scott, I’ve always said monetary hawks seem to have forgotten Rolle’s Theorem from calc class.

5. June 2013 at 06:09

That is an amusing dichotomy. Unfortunately, I suspect Keynesian prescriptions of massive fiscal debt may be pushing us toward a situation where there is in fact less margin for error between “no effect” and hyperinflation.

I don’t know if you saw Tyler’s post on Japanese debt and how a rise in rates would reduce the value of debt holdings — I said at the time I thought you would view this effect as small potatoes relative to the problem of continued zero growth — but there’s a fiscal corollary to that too where I’m less sanguine…

5. June 2013 at 06:14

Prof. Sumner,

It seems like these guys are focusing just on the amount of Fed action and ignoring the result. As in, $85 billion a month sounds like an awful lot, so they don’t even pay attention to the fact that it’s not achieving the desired outcome.

One thing that I’m not clear on (and I’m sure this is an elementary level question) is why all of this stimulus is seemingly going nowhere. Truth be told, $85 billion “is” a lot, but it’s obviously not enough. Why is that? Because the demand for dollars is so high that the markets just absorb all of the new cash?

5. June 2013 at 06:35

I think we are heading for a world of hurt. The Fed is so focused on employment numbers right now that it isn’t even paying attention to inflation (below 1%!!!). When the Fed announced it was going to target employment “in the context of price stability” (yeah right), I thought it was a good thing because it mandated expansionary policy. Now I see that the Fed only seems to care about employment and doesn’t care if inflation craters. How can these people not see that this is the road to lost decades (low unemployment and no growth for decades)? How can they not see that this is exactly the path Japan went down.

Stupid Fed. It should be printing something north of $200B/month right now (or whatever it takes to at least get inflation back to 2%). Instead, the only thing they want to talk about is how fast they can cut back asset purchases.

5. June 2013 at 06:57

Professor Sumner,

I believe the discontinuous inflation crowd believe that somehow the Fed is only capable of creating inflation close to target by encouraging speculation and bubbles (I’d like to, for once, see a model for this argument). People like Cochrane seem to be nervous that, in the current situation, higher inflation (even though 2% inflation would not be above normal) would quickly become runaway inflation. It’s not that inflation would jump but that inflation would become unsustainable and require a major contraction to keep under control. I suppose he believes that the risk of such a contraction is worse than the possible benefits of more inflation.

5. June 2013 at 07:00

Scott:

Is “ratex” a word? Is it “ray – tex” Or is it “rat tex”

Anyway, I think the discontinuity isn’t just a problem with rational expectations but also a problem with any consistent view of expectations.

5. June 2013 at 07:21

‘Pushing on a string’ is ‘that old time religion’. I believe I first heard it from Walter Heller in his NYU debate with Milton Friedman. Here’s James Buchanan’s explanation;

http://www.econlib.org/library/Buchanan/buchCv8c4.html

———-quote———-

Immediately after World War II, the Keynesian economists came close to convincing the Truman-era politicians that a permanent regime of low interest rates, of “easy money,” could at long last be realized. But the fiscal counterpart to such an “easy money” regime, one that required the accumulation of budgetary surpluses, did not readily come into being. As the inflationary threat seemed to worsen, money and monetary control were rediscovered in practice in 1951, along with the incorporation of a policy asymmetry into the discussions and the textbooks of the time. “You can’t push on a string”””this analogy suggested that monetary policy was an appropriate instrument for restricting total spending but inappropriate for expanding it.

8.4.16

This one-sided incorporation of monetary policy instruments makes difficult our attempt to trace the conversion of politicians to Keynesian ideas. Without the dramatic shift in the potential for monetary policy that came with the Treasury-Federal Reserve Accord in 1951, we might simply look at the record for the Eisenhower years to determine the extent to which the Keynesian fiscal policy precepts were honored. But the shift did occur, and there need have been nothing specifically “non-Keynesian” about using the policy instruments asymmetrically over the cycle. A regime with alternating periods of “easy budgets and tight money” suggested a way station between the rhetoric of the old-time fiscal religion and the Keynesian spree of the 1960s and 1970s.

————endquote———–

5. June 2013 at 07:32

Dr. Sumner,

I think you meant it was over your head rather than over your “heard.”

5. June 2013 at 07:53

Someone should acquaint Stanley Fischer with the idea of *targeting the forecast*.

5. June 2013 at 08:33

“Can someone point me to the macro model that says an expansionary policy might produce 0% inflation, or high inflation, but nothing in between? And who are the intellectual leaders that created this model?”

I have seen the models.

First, we have to say that the Fed doesn’t create money, banks create money.

The Fed creates base money, but banks lend against their reserves to create “higher order” money.

In order to create money, the bank writes new loans. And if the bank is writing new loans, they must have borrowers who want to take out these loans.

The bank’s incentives to write loans is determined by the banks cost of funds (fed funds), the size of their reserves, capital requirements, the rate at which they can lend money (the market interest rate), and their perception of the riskiness of their borrowers.

The borrowers take out new loans when their demand is sufficiently high as to pay the market interest rate (consumer credit), or when the perceived return on a new projects, adjusted for the risk of the project, is greater than the market interest rate (investment).

The level of the long term rate and perceptions of growth drive investment loan demand. The difference between Fed Funds and the market rate drives loan supply. The monetary base provides a governor, preventing banks from loan too much money.

The Fed targets the short term rate. the market sets the market rate.

In an normal environment the Fed can lower the short term rate, increasing banks incentives to write new loans.

At the zero bound, QE does not lower Fed Fund rate. It could drive down the market rate, creating a disincentive to lend, actually lowering AD.

However, QE does increase the base.

Now, if you go for long and variable lags, it is conceivable, that money growth could spontaneously begin to expand, and in a self-reinforcing cycle, shoot right through the Fed’s growth targets, and become inflationary fuel. Because of lags, prices would inflate and be slow to respond to the Fed’s efforts to tighten. The economy would cycle through a rapid bust-boom-bust with decling RGDP.

5. June 2013 at 08:43

Scott — it matters what you mean by “policy”.

If the Fed bought gold and expanded its balance sheet by $3t, and created $3t excess reserve liabilities with 10% IOR, you would have zero inflation.

If the Fed knocked on every other door in the US and offered to buy rusty nails for $100 each, and expanded its balance sheet by $3t, and paid $3t in cash, you would get high inflation.

Two notional $3t “policies”, very different outcomes. “Pushing on a string” is a dishonest critique of monetary policy. Bernanke clearly knows about these differences, or else he would not known to talk of “printing press technologies” that could produce base money at zero cost.

Tight money is official policy, but is not under any debate or scrutiny, largely because there is not even a hint of understanding in the analytical community.

5. June 2013 at 08:53

p.s. Central bankers favor opaque mysterious discretionary decision-making because they have to often willingly enact bad monetary policies for political reasons.

A monkey with a big “base money” button could enact NGDP targeting algorithms. NGDP targeting takes huge power away from banks, politicians, and their sponsors. It would simply put the central banks out of business.

5. June 2013 at 09:26

There is no such thing as a “demand shortfall.”

This is a money illusion derived from a misunderstanding of the nature and causes of (seen) partial relative over production and (unseen) partial relative underproduction, which is founded on prior miscalculation, which is founded on the very “cure” advocated to solve the non-existent problem.

5. June 2013 at 10:00

I’ve been saying for half a decade that Volcker has lost his faculties. In fact, one of Obama’s biggest mistakes was choosing Volcker as an advisor.

No disrespect, but a mandatory retirement at the ripe young age of 80 would’ve kept Volcker out of the ring during the entire financial crisis.

5. June 2013 at 14:14

Sumner asks: “Can someone point me to the macro model that says an expansionary policy might produce 0% inflation, or high inflation, but nothing in between?”

You can probably get there with “long and variable lags”, can’t you? Make a claim that no Fed action can affect inflation in the short run, so we’re stuck with the 0% for now. Meanwhile, Fed actions have effects in the medium/long term. We’ve got a dam, and we’re filling up the lake behind it. I’m not sure what’s keeping the dam there — the zero bound liquidity trap? — but in any case, some day that dam will burst (when the economy begins to recover, and rates rise above the zero bound), and then all that Fed balance sheet will start pouring into the rest of the economy, and we’ll get hyperinflation. And the more we try to do today, the worse the problem will become, once it starts.

I think that’s a model _without_ expectations, where the proposed transmission mechanism of monetary policy is something more direct. Maybe via something like the infamous austrian Cantillon effects? If the only transmission mechanism was a slow spread of prices from industry to industry, perhaps that would create sufficient lags. (And might provide a mechanism for the dam, if the initial injection were blocked up due to something like a zero lower bound, and thus the shocking interchangeability of currency with other financial instruments.)

OK, I just made that all up, and it’s not a very good theory … but it does seem to describe a bit about what these odd folks seems to be thinking.

5. June 2013 at 14:15

Geoff: always a pleasure, to read your wacky combination of ignorance with arrogant confidence. Keep fighting the good fight!

5. June 2013 at 15:41

Ashok, I forgot Rolle’s theorem. I took calc 40 years ago.

TallDave, Yes, I see that as a minor problem.

Jake, Check out my next post, it addresses some of those issues.

Scott, I suggested they ratchet up by 20% per month.

J, I’m not sure if younger people realize this, but bubbles play no role in serious macroeconomics, and they shouldn’t play a role. The idea that monetary policy works through bubbles is simply crazy. Of course you are only reporting what others are saying, so don’t take this personally.

Bill, Certainly in a ratex model you would not have that discontinuity.

Randomize, Thanks, I’ll correct that.

Philo, That’s right.

Doug, You haven’t told me who the intellectual leaders are who created that model.

BTW, Any shock that is might create high inflation, should ipso facto create some inflation merely on that expectation.

Jknarr, Yes, and of course the pushing on a string concept assumes no IOR. Otherwise you could simply cut rates.

Steve, That paper was certainly disappointing.

Don, But the pushing on string concept means no inflation over the time period in which M affects P. If it was expected to create inflation in the future, it would create inflation right now, or at least within 12 months.

5. June 2013 at 15:51

“Ashok, I forgot Rolle’s theorem. I took calc 40 years ago.”

It’s just jargon for common sense, my bad. 😉 It says (more/less) that if there’s a continuous function where a < b and f(a) = f(b) some c between a and b is the maximum.

So if you take "monetary stimulus" as your x and "effect on growth" as your y, eventually it will get "too aggressive" dimming effect on growth, and too stingy which suffers from sticky wages.

So there's an optimum and hence some monetary stimulus has to be good.

So ipso facto the hawks are wrong!

(I can only imagine any model to the contrary to have some crazy nonlinearity and threshold, but as long as it's continuous nothing changes).

5. June 2013 at 16:02

I guess the argument is that the extra base money does not increase demand but does increase financial speculation. The argument could go like this:

1. The Fed prints X dollars and buys Treasuries with it.

2. The people who owned Treasuries were fine collecting interest, but now they have to do something crazy with that money to get yield.

3. The crazy thing is either real misallocation of capital or a derivative which will be a zero-sum transfer to the “smart money.”

There are two big issues with this argument. First of all, Treasuries have been used in a similar manner as base money for awhile now, through their use as collateral in repo. Secondly, these arguments never square with markets being efficient. If markets act with perfect knowledge, then there just isn’t any possibility of bubbles or capital misallocation. I have never understood how Austrians can both be for nearly pure free markets AND have convoluted arguments which rest on markets being inefficient.

However, efficient markets do square perfectly with the possibility that monetary policy unexpectedly became tight. A true capital misallocation would mean that, even if NGDP growth stayed at the same level, the capital from the misallocation would remain underutilized. If ALL capital became underutilized, then no particular sector could have been misallocated. Instead, markets had the correct valuation for the capital before tight money, based on a small probability of hitting the zero-bound, and then market prices digested the news of tight money.

There is not a “true” market price, but a price which reflects the Nash equilibrium where each economic actor cannot increase their own personal gain by unilaterally acting alone. Given a generally constant inflation/NGDP in the decades before, the market used an equilibrium point for constant inflation/NGDP growth. We have been shifting equilibrium points since 2008, which is why markets have become so much more correlated.

All that to say Fisher and likely Volker do not understand this. They see the fact the stock market declined precipitously in 08-09 as evidence that the market was overvalued. Inefficient markets are not some sideshow to their views, but they are the foundation. Therefore, it’s not a stretch to say that the *only* two possibilities for QE money is either excess reserves of misallocated capital. In the real world, the misallocated capital would cause high enough inflation that the Fed would start tightening. However, Fisher and Volker have also said that the Fed somehow “got credibility” in fighting inflation and that the credibility could slip away unless we have another supposedly heroric bout of fighting inflation (really, raising rates to where they needed to be was not that difficult).

5. June 2013 at 16:03

Uh, that should be “excess reserves or misallocated capital” in the last paragraph.

5. June 2013 at 21:24

[…] Scott writes: […]

5. June 2013 at 23:50

Slightly off topic: for recognizing short texts, like this paragraph, you can use

http://www.onlineocr.net/

Almost the same amount of work, you just upload it to them, not here.

Regards.

6. June 2013 at 01:36

Scott, it seems to me that inflation is not the only way in which excessive monetary intervention can be harmful. It can also distort incentives, thus causing market participants to “game” the system in a way other than trying to productively innovate, as a result removing the sole driver behind economic growth.

6. June 2013 at 03:47

Rademaker, your comment is incredibly vague. What do you define as excessive monetary intervention? When you said “excess”, did you mean an intervention that causes positive inflation? Or higher than expected inflation? Or inflation over target?

How do market participants game “the system”? What is “the system”? Why would any inflation cause a participant to not want to innovate? If excess monetary intervention can distort incentives, then why are you only talking about attempts at expansionary intervention? Wouldnt excess disinflation do the same thing?

This is a great example of the “unspecified risks” we always hear about. You say “monetary intervention” “distort” and “inflation”, nod your head sagely, and act like you’ve said something constructive.

6. June 2013 at 06:26

Rademaker, people will game any system or policy, and people will game the lack of any system or policy.

6. June 2013 at 06:52

Matt, Two issues:

1. Banks earn higher interest on reserves than T-bills.

2. If it did lead to “risk on” that would boost NGDP. No pushing on a string.

Thanks ps.hu

Rademaker, Yes, but of course many would argue that you are merely describing one of the well known side effects of high inflation. But I certainly agree that very high inflation can lead to all sorts of distortions.

However if it does not lead to excessive NGDP growth, then those “gaming” problems do not occur.

6. June 2013 at 08:08

“1. Banks earn higher interest on reserves than T-bills.

2. If it did lead to “risk on” that would boost NGDP. No pushing on a string.”

Yes, #1 is true today. Treasuries were used though before the crisis in a way similar to base money through repo agreements.

“Risk on” can be both real investments and derivative/secondary market. The latter does not increase NGDP, except for the transaction costs. Their thinking is that the extra base money would cause both to go up, with both real investments and derivatives being misallocated investment. If the new investments are mostly derivatives, then NGDP does not go up but you get “financial instability” and such. If the base money does lead to NGDP increases, then they would also say that the Fed would “lose credibility” as far as fighting inflation and inflation would spiral out of control.

The argument assumes inefficient markets and lack of power for the central bank to tighten money. The first is generally wrong and the second is categorically wrong, which is why I don’t agree with their argument.

6. June 2013 at 08:27

Matt,

Banks run balanced books, and excess reserves are essentially a permanent capital asset. They need more liabilities on the other side.

They ought to make loans, but there is not enough balance sheet quality outstanding for this to absorb enough of their need for creditworthy liquid liabilities. Instead, they underwrite downside risk in financial markets — write puts, write CDS — and get income. Look at the JPM whale trade.

Don’t overlook the need for liquidity in their liability exposure — they are dancing close to the door. Selling puts and getting income can almost by itself explain the SPX run up — there has been an explosion in implied vol open interest via the CTFC.

Bank liability management is the excess reserve – risk on nexus.

6. June 2013 at 15:26

The catch is that asset quality needs future income for the borrower to make payments. Asset quality, loan demand and future income (NGDP) goes up and down together. There is not one that drives the other. They’re all determined by different economic players, but the economic players have to choose based on what other economic players are doing. This is where expectations come in and how monetary policy could have substantial effect even if it’s OMO mechanics suggest that they shouldn’t.

Is asset quality from the previous boom simply too poor to enable lending? Poor asset quality is bad news for banks, but it should not have anything to do with the ability of other lenders to make loans which are creditworthy with consistent NGDP growth. Banks may have to write off bad loans from the previous boom, but the amount of base money is the same or increasing. Equityholders or depositors have to take losses from poor loans, but that doesn’t immobilize base money. Print enough base money or drive down real rates low enough, and the money will be mobilized through either consumption or investment.

The SPX runup also does not need put underwriting. You could look at prices of Treasuries and see a similar upward trend. Do Treasuries need puts for the run-up in their prices? No, their prices have gone up due to continued low interest rates and the unlikelihood of the Fed raising rates any time soon. SPX’s price increase makes sense if you compare earnings yield to the yield of other invesments.