Some initial thoughts on John Cochrane

I’ve been trying to work my way through John Cochrane’s recent post on money, inflation, and interest rates. I don’t like the intro:

I’ve been following with interest the rumblings of economists playing with an amazing idea — what if we have the sign wrong on monetary policy? Could it be that raising the interest rate raises inflation, and not the other way around?

Most recently, Steve Williamson plays with this idea towards the end of a recent provocative blog post.

Cochrane implies that, according to conventional monetary economics, raising interest rates is deflationary, and that Williamson is one of the first to suggest otherwise. But here’s Milton Friedman, discussing Japanese deflation:

Low interest rates are generally a sign that money has been tight, as in Japan; high interest rates, that money has been easy.

So it seems like Friedman agrees with Williamson. A monetary policy that produces low interest rates also produces deflation. And of course this is true. And yet Friedman would have obviously been horrified by Williamson’s recent post. Friedman’s views of the liquidity effect were fairly conventional. At a minimum, Cochrane should have been more specific—how does the central bank raise interest rates? Cutting the money supply? Or raising the inflation target to 40% per year?

Now in fairness Cochrane certainly does understand the liquidity effect/Fisher effect distinction I am making:

The first standard story was money. In the past, when the Fed wanted to raise rates, it sold bonds, cutting down on the $50 billion of non-interest-paying reserves. The standard story was, with less “money” in the economy and somewhat sticky prices, nominal interest rates would rise temporarily. The less money would eventually mean less inflation, and then and only then would nominal rates decline. In this view, running the Fed was a tricky job, like driving 68 Volkswagen bus in a crosswind, since the steering was connected to the wheels in the wrong direction in the short run.

An automobile metaphor. No wonder Nick Rowe thought it was a good post! But I don’t like the next paragraph:

However, we are likely to stay with huge excess reserves and interest on reserves. When the Fed wants to raise interest rates now, it will simply pay more on reserves and bingo, interest rates rise. We will remain as awash in interest-paying reserves as before. So this 1960s monetary mechanism just won’t apply. Is it possible that in the interest-on-reserves world, raising interest rates translates right away into larger inflation?

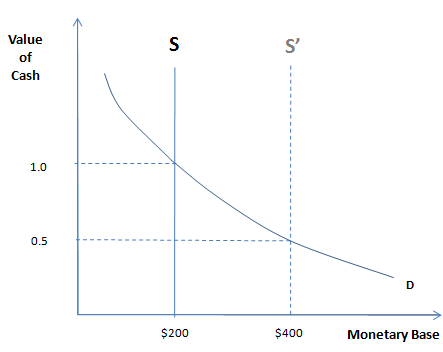

I think Cochrane is confusing “money supply model” with “monetarist model.” The monetarist model is completely symmetrical vis-a-vis (permanent) changes in the supply or demand for base money. Start with the basic graph:

The standard monetarist model uses basic price theory (aka hot potato effect) to argue that printing more money will reduce the value of money. A lower value of money means a higher price level. But the basic model is symmetrical. If the Fed lowers the demand for base money, say via lower reserve requirements, that will shift the demand for base money to the left, which is just as inflationary as a increase in the money supply. More supply or less demand for any asset will reduce the value of that asset, unless it is exchanged for a perfect substitute.

Of course interest on reserves (IOR) is just like reserve requirements, a Fed policy tool that can increase the demand for base money.

Now consider the impact on interest rates. Monetarists assume that prices are not perfectly flexible in the short run. Thus a decrease in the money supply will initially lead to “disequilibrium.” I use scare quotes because the nominal interest rate will rise to equate supply and demand for base money in the very short run. There is a disagreement between me and the other market monetarists as to whether it makes sense to refer to this situation as “disequilibrium” (they say yes, I say no) but that’s merely a semantic debate, no policy implications are at stake.

The tendency of a decrease in the supply of money to raise interest rates in the short run is called the “liquidity effect.” For the exact same reason an increase in IOR raises market interest rates. Higher IOR shifts the demand for money to the right. Because the price level does not immediately decline, there is a short run excess demand for money, and interest rates will rise until the price level adjusts. Once prices adjust, interest rates will return to their original level. Money is neutral in the long run. You can also do the same exercise with rates of change, and get superneutrality in the long run (apart from some second order effects.)

So unless I am mistaken, Cochrane errs in assuming that the world of IOR cannot be smoothly handled by the conventional monetarist model. Here’s the next paragraph:

More recent economic thinking has (rightly, I think) left the money vs. bonds distinction in the dust. The “Paleo-Keynesian” (credit to Paul Krugman for inventing this nice word) models in policy circles state that the Fed raises rates, this lowers “demand,” and through the Phillips curve, lower demand means less inflation. No money in sight here, but yes a negative effect. The first half of Steve’s blog post tearing apart the Phillips curve at least should question one’s utter confidence in that mechanism.

Here I disagree with both Cochrane and the NKs. I like money in my models, and think it is no more similar to bonds than it is to a microwave oven. But I’ll say this in partial defense of Cochrane. Any (NK) economist who has jettisoned money from their model, and describes policy solely in terms of interest rates, has lost any right to get indignant about Cochrane and Williamson. Without money it’s impossible to show that Williamson is saying anything different from what Friedman said about the Japanese back in 1998. And Friedman was right.

PS. Nick Rowe has an excellent post. Nick keeps emphasizing that statements like “The Fed raises interest rates” make no sense unless embedded in a much more detailed and complete policy regime. What else changes between now and the end of time?

PPS. Tyler Cowen’s link says the following:

6. John Cochrane defends Williamson on interest rates and inflation.

Yes, but just to be clear, Cochrane does not endorse Williamson’s claims. He defends Williamson’s right to ask interesting and provocative questions.

PPPS. Ed Dolan has a new post discussing market monetarism.

Tags:

21. December 2013 at 12:05

I call it, ‘I Love Lucy’ monetary theory; the episode where Lucy accidentally inflates a rubber life raft in the apartment after Ricky has gone to the Copa to work.

Hilarity ensues as the birdbrain tries to stuff it into the closet, but it won’t fit and keeps popping out. Not funny when a guy like Cochrane with a Phd in economics tries it.

21. December 2013 at 12:32

Scott: here’s one way to think about it: suppose at time t the Fed announces a new time path for the money supply. That new time path could be any shape you like. It might involve a jump up or down in the level of the money supply, and a change in the growth rate too. Out of the set of all possible time-paths, think of the subset that would cause an immediate upward jump in nominal interest rates. That subset is still very large. Different members of that subset would have very different implications for the time-paths of the price level. Some would cause higher and some would cause lower inflation.

I started to write a post in response to John Cochrane along those lines, but abandoned it. It was getting too complicated and parameter-dependent. It was easier to build a model where we talked about what a higher nominal interest rate implied about the central bank’s inflation target.

What I liked about John Cochrane’s post is that he is one of the very few people who takes seriously the indeterminacy of inflation in a New Keynesian model where the central bank sets a nominal interest rate. Do high nominal interest rates mean tight or loose money, (or lower or higher inflation)? You talk about that. I talk about that. John Cochrane talks about that. Very few others do. Most economists equate the Fed setting a higher nominal interest rate with tighter money.

21. December 2013 at 12:57

FYI the CBO potential NGDP series Ed Dolan uses predates the BEA’s massive revision of GDP released in July 2013 that incorporated investment in intellectual property. The similarly revised potential NGDP series (and its real version) were scheduled to be released by the CBO in November 2013 but that clearly has not yet happened. The updated series will likely show an increase of about 2% in level in recent years.

I left Ed Dolan a comment in case he wants to make note of this.

21. December 2013 at 13:37

Scott, I think you are begging the question when you simply assert that increasing IOER increases the demand for money. This is only true if the very act of increasing IOER doesn’t simultaneously increase inflation expectations. If the CB did this explicitly, i.e., “We are raising IOER to 10% because we are determined to raise our inflation target to 10% and this is the way to get there,” it’s easy to imagine how they might successfully “reverse the sign” and loosen money with higher rates. Depending on the model we could even just jump right into the Fed’s new world (price level doesn’t budge but inflation expectations and nominal rates rise) with no increase in the demand for base money. The whole idea is that the Fed could at least possibly be seen as doing a much more subtle version of this (either actively or passively) by raising rates without explicitly changing the language of their reaction function, but nonetheless getting the same effect — i.e. “selecting” an equilibrium of higher inflation and higher rates (or perhaps just landing in one of many possible equilibria by happenstance).

I think he is allowed to wonder if the message in an IOER but no convenience yield world might be different than the message in a usual world where raising rates is clearly read as a reaction function tightening. If it is, then raising IOER doesn’t necessarily increase the demand for base money.

21. December 2013 at 15:49

“Without money it’s impossible to show that Williamson is saying anything different from what Friedman said about the Japanese back in 1998.”

You seem to think there’s nothing in my work, or related work by other people, that is different from what Friedman had to say. Here are the key differences:

1. We think that all the assets matter – it’s pointless to separate assets into ones that are “money” and ones that are not.

2. Financial intermediation matters. To Friedman, that was a black box.

(1) and (2) are actually a key part of the issues I’m trying to get at. That’s in my published and unpublished “serious” work, if you care to look at it.

21. December 2013 at 16:29

Steve Williamson,

Friedman rule was Friedman’s answer to (2).

21. December 2013 at 18:08

Steve Williamson,

I certainly agree that assets matter and financial intermediation matter for a lot of things. But do they matter for monetary policy? That depends on the monetary offset. Can’t anything in that black box be offset by monetary policy? If not, why not?

So I have two questions of my own:

1. Is there anything that could realistically happen to assets or financial intermediation that would make it impossible for the Fed to hit its NGDP expectation target?

2. Is there anything that could realistically happen to assets or financial intermediation that would make it desirable for the Fed to change its NGDP expectation target?

I submit the answer to (1) and (2) are both no.

21. December 2013 at 19:11

Nick, Good points.

Thanks Mark.

dlr, You said;

“I think you are begging the question when you simply assert that increasing IOER increases the demand for money. This is only true if the very act of increasing IOER doesn’t simultaneously increase inflation expectations. If the CB did this explicitly, i.e., “We are raising IOER to 10% because we are determined to raise our inflation target to 10% and this is the way to get there,” it’s easy to imagine how they might successfully “reverse the sign” and loosen money with higher rates”

Yes, and that’s what I was getting at in my PS. But I’m focusing on the world we actually live in, where increases in IOR are central banks signals of tighter money and lower inflation, not the reverse.

Steve, I didn’t word that as precisely as I should. Of course your work is much different from that of Friedman, even I can see that. My point was different. That on the question of whether a lower interest rate can lead to lower inflation, no one has a right to call your approach crazy if they have a model without money. Because that would imply Friedman’s approach was equally crazy, which it obviously was not.

I’m still not sure how to translate your claims into a monetarist model . . .

On point 1: Money is important because money is the medium of account and other assets are not. If we were still on the gold standard then the gold market would be special, not at all like other assets. But we are on the Federal Reserve Note standard, which makes Federal Reserve Notes really important. The price of other assets can change, the nominal price of Federal Reserve Notes cannot change. That’s why they are special.

21. December 2013 at 20:46

John Cochrane writes: “Could it be that raising the interest rate raises inflation . . . ?” Milton Friedman writes: “Low interest rates are generally a sign that money has been tight . . . ; high interest rates, that money has been easy.” These remarks are not directly in conflict with each other. Cochrane’s remark concerns the effect that a change in the interest rate would have on the rate of inflation; Friedman’s concerns the effect that a change in the stance of monetary policy would have on interest rates. In Cochrane’s remark the change in the interest rate is the cause, in Friedman’s it is the effect. (And in Cochrane’s remark the effect is a change in inflation, while in Friedman’s the cause is a change in monetary policy.)

21. December 2013 at 22:12

Cochrane, by his own description, has been “collecting” anti-QE’isms from all over the web. So you can read that QE is inert, or causes deflation or is hyper inflationary….

Cochrane has averred that the best the Fed can do is shoot for zero inflation. Single mandate, forget any fancy dancing.

This conflicts a bit with Cochrane’s prescription for recessions, and that is a one-time sudden drop in wages and prices that corrects the imbalance between demand and supply.

So, if prices did start to fall in a recession (ignoring sticky wages, real estate removed from market etc), should the Fed stand by and let prices fall, or shoot for zero inflation, which would actually call for stimulus?

A bit ironically, the Fed has actually obtained very stable prices and near zero inflation since 2008–Fed policy, it terms of price stability, has been successful for five years running now. Ain’t it grand?

Cochrane seems insensate to the experience of Japan–or even the not-bad performance of the USA economy since the Fed went to open-ended, somewhat target-driven QE3.

In the end, I think Cochrane is arguing from a premise, and that is traditional conservatism, and that is tight money is good, the Fed should do nothing, and the federal government should be very small (in areas that conservatives think it should be small–it can be huge in areas like agriculture, rural infrastructure, defense, homeland security and the VA).

The social norm among economists now is to rhapsodize about infinitesimal inflation rates, and back-burner real growth concerns–the opposite of the Fed and mainstream in the 1960s and 1970s. Then the social norm was to seek “optimal output” and say that monetary policy would only bash real output, not prices.

In this regard, since the 1970s, the right-wing has captured the profession along with the central bank.

22. December 2013 at 00:23

Because the price level does not immediately decline, there is a short run excess demand for money, and interest rates will rise until the price level adjusts.”

Or real income, of course.

22. December 2013 at 03:14

I’ve been following with interest the rumblings of economists playing with an amazing idea “” what if we have the sign wrong on monetary policy? Could it be that raising the interest rate raises inflation, and not the other way around?

Most recently, Steve Williamson plays with this idea towards the end of a recent provocative blog post.

“”Cochrane implies that, according to conventional monetary economics, raising interest rates is deflationary, and that Williamson is one of the first to suggest otherwise. But here’s Milton Friedman, discussing Japanese deflation:

“Low interest rates are generally a sign that money has been tight, as in Japan; high interest rates, that money has been easy.”

So it seems like Friedman agrees with Williamson. A monetary policy that produces low interest rates also produces deflation.”

How can one call this “agreement” when one party (Friedman) says that low interest rates (and deflation) are a *consequence* of tight money (defined by money supply) and the other (Williamson) is quoted as saying that low interest rates *cause* deflation.

It strikes me that if your notions of cause and effect are completely reversed, Friedman could hardly “agree with Williamson (or vice versa).

22. December 2013 at 06:12

Do we have a smoking gun here?

http://www.npr.org/2013/12/21/256003481/want-to-learn-quantitative-easing-theres-a-computer-game-for-that

22. December 2013 at 06:19

Philo, I agree.

Ben, I wish he’d focus on NGDP and not inflation.

Saturos, Yes, but in the long run it will be the price level that adjusts.

Vivian, My point was that both agree that a policy that causes low interest rates in the long run is also a policy that causes deflation. I also pointed out that Friedman would have been horrified by Williamson’s claim, so I certainly wasn’t asserting that their views were identical.

22. December 2013 at 06:20

Saturos, Thanks, Those games got some discussion in the blogosphere a few months back.

22. December 2013 at 08:26

OK. I tried to organise my ideas better in a post: http://worthwhile.typepad.com/worthwhile_canadian_initi/2013/12/nominal-interest-rates-and-inflation.html

22. December 2013 at 11:13

Scott,

It took a change in the funds rate from 5% to 20% between 1977 and 1981 to change the inflation trajectory. Inflation was 6% in 1977 and peaked at 13.5% in 1980. Inflation than dropped steadily bottoming at 1.9% in 1986.

About this economic period:

#1 It seems that inflation increased as long as the funds rate matched the inflation rate. Only when the funds rate was pushed much higher than inflation did the trajectory of inflation change.

#2: From 1983 to 1989 the economy achieved consistent real growth all while the funds rate was higher than the inflation rate.

Questions:

#1: How much change in the funds rate is needed to effect a change in inflation expectations? Is it possible to realize this change when the funds rate is near zero?

#2: Is real economic growth conditioned on the funds rate (ie safe short term lending rate) being higher than the inflation rate? If yes then why would the Fed keep the lending rate below the inflation rate and insist it will keep doing so?

#3: Are monetarists in “uncharted waters” because ZIRP so completely distorts economic incentives that none of the usual macro levers have the consequence theory says they should?

22. December 2013 at 14:27

Thanks Nick, I did a post.

Dan, You said:

“It took a change in the funds rate from 5% to 20% between 1977 and 1981 to change the inflation trajectory.”

No it didn’t. Interest rates soared because NGDP growth rates were rising, not because money was tight. Interest rates tell us nothing about the stance of monetary policy.

Your first two questions are meaningless. It’s like asking me what the price of strawberries needs to be to produce adequate growth. Interest rates tell us very little about monetary policy. There is no answer to your questions.

Regarding your third question, it is Keynesians who are screwed up by the zero bound on interest rates. It blows their interest targeting policy right out of the water. It has no impact at all on market monetarist proposals to target expected NGDP growth.

23. December 2013 at 09:00

Isn’t the “mistake” here in talking about interest rates as though they are the causal factor instead of a means of signalling intent and changing market expectations? Isn’t an increase or a decrease in rate ambiguous as to “inflation” unless you know how the change compares to expectations?

Or am I confused?

24. December 2013 at 10:55

Adam, Yes, you are right.