Rethinking recessions

Recently, there’s been a tendency for people to try to expand the definition of recessions. You see people talking about declines per capita GDP in Australia, or “manufacturing recessions” in various countries.

I’d like to see us go in the other direction, tightening the definition. In the past, I’ve discussed three “phony recessions” in Japan during the past nine years. In each case there was a brief period of negative RGDP growth, and then a rebound, with no increase in the unemployment rate. Because Japan has a rapidly falling population, its trend rate of RGDP growth is quite low. It doesn’t take much to drive them into a brief mild recession. But it’s not really much of a “business cycle”. Here’s the Japanese unemployment rate:

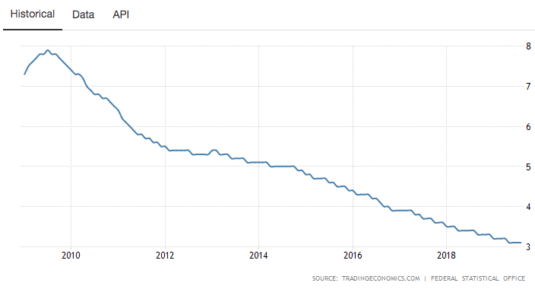

The smaller the economy, the more erratic is the rate of growth in RGDP, as individual sectors can have a bigger impact on the total. Germany’s important manufacturing sector is currently in a slump, and it threatens to push Germany into a technical recession:

Germany’s central bank warned the country’s economy may have shrunk for its second consecutive three-month period, which would mean the eurozone’s biggest economy has entered its first recession in six years.

But does this actually matter?

The labour market has cooled in Germany recently, but unemployment continues to fall, the Bundesbank said. In September the number of people registered as unemployed fell by 10,000 from the previous month to 2.28m, its first fall in four months.

Does this look like a country in recession?

Keep in mind that manufacturing is a relatively small share of the economy in most developed countries, and a slump in capital-intensive manufacturing can affect output more than employment.

Keep in mind that manufacturing is a relatively small share of the economy in most developed countries, and a slump in capital-intensive manufacturing can affect output more than employment.

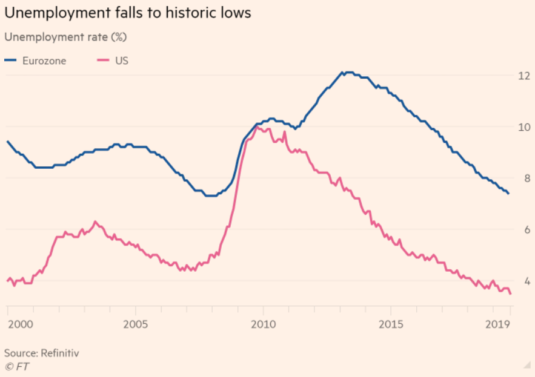

If storm clouds are gathering over trade, investment and manufacturing, they are not, however, seriously affecting households. Unemployment is at long-term lows in many advanced economies and with real incomes rising, consumer spending is preventing recessionary forces taking over.

The US unemployment rate fell to its lowest level in 50 years at 3.5 per cent in September; UK levels are at 45-year lows; and the eurozone rate of 7.4 per cent in August was the lowest for 11 years and within a whisker of the lowest rate since the single-currency area was created.

The recent problems at Boeing are a perfect example of the disconnect between output and employment. The pause in the construction of 737s does have a discernible impact on US output, but does not have a noticeable impact on US employment.

BTW, this graph illustrates a point that I frequently make. Even if the central bank undershoots its inflation target for an extended period of time, the unemployment rate will eventually fall back to the natural rate. The ECB needs a much more expansionary policy, but primarily so that it can hit its inflation target. The unemployment rate is already close to the natural rate (albeit still a bit above, as the European natural rate is trending downward.)

My suggestion is that we start defining the term ‘recession’ as a substantial rise in the unemployment rate. For the US economy, a jump of one percentage point might work. Using that criterion, all the recessions and non-recessions since WWII would be exactly the same. In the US, there are no “debatable recessions”. It’s always 100% clear as to whether we are in a recession or not. (The lack of mini-recessions in the US is perhaps the most important unsolved mystery in macroeconomics.)

Going forward, however, the unemployment criterion might yield different results from the 2 quarters of falling RGDP criterion, or the more complex formula used by the NBER in the official recession dating decisions. We already see mini-recessions in other countries. (BTW, contrary to popular opinion, the NBER does not use 2 quarters of falling GDP.) Let’s get ahead of the problem, and not change the definition only after an ambiguous situation shows up. Do it now.

Prediction: The world will see an increasing number of “phony recessions” in the 21st century—recessions with falling output but strong labor markets. The Phillips Curve is now defunct; Okun’s Law is next.

PS. I have a new piece at The Hill that actually praises the Fed for improving its monetary policy, and I suggest that this is why the current expansion is the longest in US history. Of course with my luck you should now expect a recession within 12 months! 🙂

Seriously, I do say in the Hill piece that money continues to be too tight, and that recession risks remain elevated. I see a roughly 30% risk of recession, which is too high.

Tags:

22. October 2019 at 09:45

Even Shadowstats has to admit that US unemployment has fallen – all the way down to 20.9%:

http://www.shadowstats.com/alternate_data/unemployment-charts

22. October 2019 at 09:46

Also, since when did a monetarist take control of the Fed (or the “FED”)?

http://www.shadowstats.com/charts/monetary-base-money-supply

22. October 2019 at 11:03

“My suggestion is that we start defining the term ‘recession’ as a substantial rise in the unemployment rate. For the US economy, a jump of one percentage point might work.”

This seems similar to the Sahm Rule: “The Sahm Rule predicts the start of a recession when the three-month moving average of the national unemployment rate (U3) rises by 0.50 percentage points or more relative to its low during the previous 12 months.”

https://research.stlouisfed.org/publications/research-news/fred-adds-sahm-rule-recession-indicators

22. October 2019 at 11:04

One glaring omission kept from explanations about secular stagnation is population growth. Three nations mentioned here: Germany, Japan, U.S. The U.S. has the lowest unemployment and the largest growth of the three correct? It also has the highest population growth, though still only slightly above replacement. Japan has stagnated since the 80’s. We can compensate by driving money into the economy and boosting inflation for awhile, but the velocity of money will never reach the growth seen in the 60’s unless there is a new growth paradigm.

22. October 2019 at 11:12

Good post. Who gets credit for the current half-assed definition of ‘recession’?

22. October 2019 at 11:18

Another interesting point is that the 2014 VAT-increase-induced japanese “downturn” is nowhere to be found in the employment data.

I’d bet that last month’s VAT increase will not lead to an increase in unemployment either.

22. October 2019 at 13:39

There is an important difference between Japan and the U.S. when there is a downturn: Japanese companies will try to keep employees but will reduce their hours.

22. October 2019 at 13:43

Unemployment feels odd in that it’s typically a lagging indicator of a “real” recession but… I don’t have a better metric for a leading one.

Todd makes a great point. US companies (or maybe workers?) definitely seem to choose maintaining wage levels over maintaining staff.

22. October 2019 at 14:04

LK, I’ve argued that anything more than 0.6% signals a recession, but picked 1.0% to be on the safe side .

And yes, I’ve made that point about 2014 as well.

Todd, Yes, but keep in mind that Japanese unemployment did rise in 2008-09, that’s very clear in the data. The UK also had a phony recession a few years back.

The key point is that Japan’s trend RGDP growth is now very low, so a mild decrease is not much of a change from trend.

22. October 2019 at 14:42

Scott: Great piece, I wonder if Per-Capita GDP might be a good indicator for measuring recessions as well. Of course, this assumes no massive population shifts in either direction, so it might work for countries with a stable population decline like Japan and not like countries like the US where immigration may create masking composition effects.

I was curious about Germany’s and Japan’s economic growth so I checked their per-capita incomes at the WorldBank website, and was really shocked at how well the US is doing in comparison. Out of all the East Asian and Western European nations of any particular size, the only ones to gain in absolute terms with the US was Korea. Even the absolute gap between the US and China increased! This is true for constant and current international dollars.

https://data.worldbank.org/indicator/NY.GDP.PCAP.PP.CD?locations=US-DE-FR-JP-GB-CN-KR

Hong Kong did slightly better, and Singapore is just hilarious. Are those numbers even accurate?

https://data.worldbank.org/indicator/NY.GDP.PCAP.PP.CD?locations=US-SG-HK-CN

22. October 2019 at 14:47

Scott, I thought you made some very good points in your opinion piece for The Hill if you were writing that for someone who is a normal reader of your blog who understands the importance of monetary policy and how it’s managed. But in looking at the comments of the article on The Hill, it seems like many of the readers there very badly lack the necessary knowledge to understand the importance of monetary policy. And that’s not a surprise given that the vast majority of people know very little about this topic. When you write such things for such a news outlet, you may need at least a couple of paragraphs to explain the importance of monetary policy, how it’s been managed by looking at past data and future projections, and the changes of how those projections are being made.

22. October 2019 at 14:56

Scott: I am actually curious question with respect to how we characterize growth.

The US is adding more in Per Capita Gdp than China year by year, but China grew more in relative terms, but which “grew” faster?

China has grown faster than the US in growth percentages for the last 40 or so years, yet the gap in per-capita GDP has growth since then, with the average American being more richer with to respect to the average Chinese today than they were in 1978.

Yeah China started from a low base, but it bridged to some respect the absolute gap against other Western European countries and Japan, so it obviously grew faster than the latter. But did it grow faster than the United States, or Korea for that matter where the gap widened even more dramatically?

Maybe I am being a complete idiot, but doesn’t absolute differences matter more than relative differences? Or is it the other way around?

22. October 2019 at 15:43

Yup.

Anyway, Canada isn’t going to become great. Its TFR is pathetic. Israel might become great, though, despite brain drain.

22. October 2019 at 16:09

Interesting post.

It still begs the question of what is the presumed natural rate of unemployment, if there is such a thing. For decades the Federal Reserve considered 5% or just a little under 5% unemployment as measured by U3, as the natural rate of unemployment or a rate of unemployment below which would trigger higher rates of inflation. There is NAIRU with the ever-useful Boogeyman of accelerating rates of inflation.

One huge positive in the current economy are the trending up lines for labor participation rates. I think this must be a huge positive, unless it actually reflects lower living standards and the needs of more and more of the population to work in order to sustain themselves.

Anyway, I hope for several generations of “very tight” labor markets for the United States. The leading candidates for the presidency are Donald Trump and Elizabeth Warren. What does that tell you about the voting public?

22. October 2019 at 16:11

This definition of recession seems inarguably reasonable. Unemployment is the ultimate measure of cyclical change, though not the only one.

22. October 2019 at 17:48

Scott, my condolences for the comment section on your piece at The Hill. It’s pretty abysmal.

I quite liked your article itself there.

22. October 2019 at 18:04

Benjamin, alas, there’s no single universal natural rate of unemployment.

That rate depends on technology, societal organization and government laws and regulations. Eg West-Germany had a pretty low natural rate during the post-WW2 Wirtschaftswunder, but they moved away from Ordoliberalism, and the government interfered a lot more with labour markets making unemployment creep up with every recession without falling back down properly.

That trend only peaked and reversed in 2005.

There were some changes in the welfare system, at the time. But also longer running changes in the private economy, like a greater move towards Zeitarbeit (temporary work, via a private agency that is the official employer and loans out the workers).

Zeitarbeit is a reaction to the rigid German laws about hiring and firing. It works around the worst, but it’s not a cure and has itself been regulated away to big extents whenever it became popular.

For comparison, the US were never so rigid in the first place, so tended to have lower unemployment (both natural and observed). But you see a similar impact from the likes of Uber: almost anyone can sign up with Uber and get as many working hours as they want. Of course, those working hours are at the market clearing price, Uber is not a charity.

(And predictably, the government has started piling on regulations, like applying minimum wage laws.)

22. October 2019 at 19:06

Matthias:

All I know is when business is crying about “labor shortages,” you have a happy nation.

I prefer less, rather than more regulation.

That said, First World nations need to consider the impact of open borders for trade and immigration upon the employee class, and also the effects of a chronically tight money supply. And, of course, property zoning.

There is discussion above of per capita GDP PPP. This is a useful measure, but seems undercut by “hedonics.”

Hong Kong scores high on per capita GDP PPP. This is misleading, as so much personal income is drained off by rents. People literally do not reproduce in Hong Kong, 1.2 babies per women.

Yet the “value” of housing in Hong Kong is regarded as high, and people are getting value for the money, and so on a per capita GDP PPP basis, Hong Kongers have more income than US residents.

There are other bogeys in the data, such as Ireland having much higher per capita GDP PPP than the US. And per capita GDP PPP might be higher due to more hours worked. Americans work far more hours than Germans.

The World Bank per capita GDP PPP has some other oddities. US shows up at $62,600, while Canada rates at $48,100. US living standards are 30% higher than Canada’s? Anyone visiting Montreal would be surprised to hear that.

https://data.worldbank.org/indicator/NY.GDP.PCAP.PP.CD?most_recent_value_desc=true

I can tell you this: Living standards in Los Angeles are lower now than in the late 1960s.

We may yet see AOC in the White House.

22. October 2019 at 19:26

Benjamin: LA is an overpopulated city, so that isn’t really surprising. Of course, people stupidly still think America is an empty nation just because we don’t build houses in the desert, but all the nice areas to build are full nowadays.

If you live in some of the suburbs in America though, the real differences become apparent. I am convinced that suburban America has the highest living standards of any people in the entire world, with any #2 not even in the rearview windows.

I now live in the Austin suburbs, and the quality of life is far, far above what you would find in Canada.

And this was true when I lived in California’s suburbs as well.

22. October 2019 at 19:28

Also Benjamin, you have to take into account composition effects.

LA is poor because of all the immigrant Hispanics, but their low crime rates and pleasant nature make it very nice for the existing White population. So all groups, including African Americans and Asians, benefit, but the composition makes the living standards look worse.

22. October 2019 at 19:54

John Arthur, (and Scott)

re: Singapore / Hong Kong, and the US. Scott always emphasizes that consumption matters more than income. So now, redrawing the GDP /capita data as household consumption /capita, you get this:

https://data.worldbank.org/indicator/NE.CON.PRVT.PC.KD?locations=US-SG-HK-CN-DE

I’ve added Germany to the mix for an example of a wealthy EU country.

Now the riddle reverses: The US wildly ahead of both HK and SG. SG significantly behind HK – SG’s recent dash of GDP/capita growth not translating into consumption gains. Germany catching up dramatically in the 2000s, pulling ahead of SG and narrowing the gap to the US quite significantly.

Sadly this database has GDP at PPP but household consumtion is not PPP corrected. Still, with such large differences I’d assume there is something to be discussed here.

22. October 2019 at 20:14

Thanks mbka!

I agree that consumption matters more for income, but I feel like buying an expensive house and paying long run costs is also a form of consumption. You are enjoying the benefits of a nice neighborhood, low crime, pleasant neighbors, etc. Singapore and Hong Kong are expensive because it is nice to live with those kind of folk. Same for Los Angeles.

But this consumption data is cool. I have long suspected that consumption lags significantly below what is expected in China,

as the Chinese Economy requires tremendous investment to maintain growth in a very inefficient economy. To adjust for PPP, I would just multiply these numbers by two, its pretty much the difference between China’s nominal and PPP data.

As expected, HK and Singapore’s high housing costs reduce consumption, and more affordable US and Germany have higher relative consumption to their GDP. Data isn’t perfect, but it is interesting.

The biggest problem in HK and Singapore is that they have money, but not land. Even though both city states have the wealth to build American type suburbs, they don’t have the physical land to do so. As a result, they pay more for worse housing.

I added Japan to this list, and their lowered population seems to have been good for them consumption wise. However, the corresponding general economic slowdown has harmed consumption growth. But considering that Japan is dramatically poorer than the US, HK, and Germany, the fact that it has higher consumption than HK and Germany is very important.

https://data.worldbank.org/indicator/NE.CON.PRVT.PC.KD?locations=US-SG-HK-CN-DE-JP

22. October 2019 at 20:19

mbka: This data does place the Singapore data into some sort of reasonable light. Since HK ranks higher than Singapore in economic freedom, and both are majority Han Chinese, it seemed silly for Singapore to be nearly twice as richer as Hong Kong.

22. October 2019 at 20:23

John, Those graphs don’t surprise me at all; the US has been richer than other developed countries for . . . . well for almost a century.

I’d say relative differences matter more. Going from $5000/year to $15,000/year is much more dramatic than going from $70,000 to $80,000.

Gordon, Good point. The problem is the limit on the number of words. It’s very hard to explain monetary policy to the average reader in just a few words, so my columns are aimed at the upper end of the reading public.

Matthias, I never read their comment section.

mbka, As you know, housing is where we have a huge lead, especially over HK (but also Singapore.) PPP would help those two in terms of restaurants and other services. HK has 370,000 maids in a city with only 7 million people—that suggest a lot of upper middle class families. Maybe a million people live in families with maids? That’s insane.

I grew up in an affluent area of Madison and I never once saw a maid until I was in grad school at Chicago, visiting a prof’s house. I was already 24 years old. But then I never saw salt water until I was 21 years old.

Of course Ben says we were better off in the 1960s. LOL.

22. October 2019 at 20:37

mbka, John Arthur—

Great charts, but as pointed out, not PPP-adjusted, and also there are snags in “hedonics,” that is figuring out if renters and home buyers are just house-poor (as in Hong Kong), or getting good value for their money by living in a wonderful place with lots of amenities.

Add on, hours worked to get to any level of consumption.

Hours worked per year—

Mexico – 2255 hours per year

Costa Rica – 2212

South Korea – 2069

Greece – 2035

Chile – 1974

Russia – 1974

Poland – 1928

Latvia – 1910

Israel – 1889

Lithuania – 1885

Iceland – 1879

Estonia – 1855

Portugal – 1842

Turkey – 1832

Ireland – 1820

US – 1783

Czech Republic – 1770

Hungary – 1761

New Zealand – 1757

Slovakia – 1740

Italy – 1730

Japan – 1713

Canada – 1703

Spain – 1695

Slovenia – 1682

UK – 1676

Australia – 1669

Finland – 1653

Sweden – 1621

Austria – 1601

Switzerland – 1590

Belgium – 1551

Luxembourg – 1512

France – 1472

Netherlands – 1430

Norway – 1421

Denmark – 1410

Germany – 1363

Egads, those Germans work 400 hours a year less than Americans, or about 10 extra weeks off (40-hour week).

International comparisons are always very foggy, which is why macroeconomists can prove any point they like, manipulating the data (and overlooking other realities).

For example, the German economy is much more regulated and socialized than the Mexican economy, yet the Germans have much higher living standard than the Mexicans and work nearly 1000 hours a year less. And much lower crime rates.

Ergo, socialism rules.

John Arthur:

I once bantered to a friend of mine than American cities are not very charming, and often just blah, certainly compared Europe and Asia.

He retorted, “Oh, we have nice cities. What about Montreal?”

I lived in Austin in the late 1970s. I understand it is now expensive and crowded. When I arrived there, I was told Austin used to be nice, but had become to urbanized, and had lost its friendly town feeling in the 1970s. Also, the girls went topless at Barton Springs.

22. October 2019 at 20:53

Scott: Thanks for the point on relative vs absolute. But I wonder what is “harder” to achieve. A poor country going from $3000 to $6000, or a country at the technological frontier going from $70000 to $80000, both over a similar time frame. One country doubled, but had convergence growth. One country grew a measely 1/7%, but added more in absolute dollars at the technological frontier.

In that regard, will the gap in per-capita GDP for China and the US grow, or will it shrink?

This kind of question has important implications for the future of convergence between countries.

22. October 2019 at 21:01

Benjamin: American inner cities tend to have a lot of crime, so people try to get as far as possible from each other, while still leaving just little distance to commute to a good paying job. It’s not a perfect equilibrium, but it works out overall. If America had crime rates as low as East Asia and Europe, I bet we would have really nice cities. San Diego, San Franciso, and Miami are really nice, Asian style cities, but all three have very low crime.

23. October 2019 at 00:06

To the point that Todd and LK made, the 2014 VAT-increase-induced Japanese “downturn” cannot be seen in aggregate hours worked either, when looking at the Labour Force Survey data

23. October 2019 at 01:40

John, Scott,

re: Singapore, the finer point is that 85% of Singapore’s population is housed at very reasonable prices in government-built flats. US$ 200-300,000 buys you a government flat new at subisidized prices if you fulfill the conditions. So I don’t think housing explains the lower consumption data. (Private or resale is another matter, then you’re looking at US$400,000 or more for more desirable government flats, and a million plus for private condos, and at least $3 Mio for a US style single family home – very hard to get a reasonable PPP value out of those diverging values). Some other data points – Singapore’s GDP reportedly has a low % going to salaries, less than 50% of GDP, but I’d have to dig out the data to confirm that. This and very high investment rate by government and industry.

Re: maids – similar maid data in Singapore and HK. 200,000 maids for a total population of 5.5 Mio, of which just 3.5 Mio are SG citizens and 500,000 permanent residents. If you assume 1 maid for 4 people, then 1 in 4 households have a full time live in maid. But the maid salaries are very low and tightly controlled. So this isn’t a large factor in consumption, money wise. Conversely a Toyota Corolla sets you back about US$ 70,000 dues to taxes, and there’s about 1 Mio vehicles on the roads in Singapore despite these prices. So this would actually decrease the PPP. Restaurant prices, it depends on the mix. Government food courts, a family eats for US$15. Private pizzeria next door, you spend $50 for the same family. I’d love to know what exactly they use to establish PPP.

If I had to guess: PPP data would help China’s consumption data, maybe really doubling it. But if anything it would further depress SG and HK data: HK for housing and food, SG for cars and food. I can tell you one thing, making “6 figures” in SG means you can barely afford one car per family, but maybe you won’t, because it actually hurts. If you want a life similar to a typical US sub-urbanite, point for point (car, housing type and size etc) you’re looking at a quarter million US$ family income.

23. October 2019 at 03:06

mbka–

I realise the government of Singapore is deeply enmeshed into every aspect of the Singapore economy….

“But the maid salaries are very low and tightly controlled.”

What does this mean?

23. October 2019 at 04:18

“Todd, Yes, but keep in mind that Japanese unemployment did rise in 2008-09, that’s very clear in the data. The UK also had a phony recession a few years back.”

Unemployment in the U.S. went from 5.0% in April 2008 to 9.0% in April 2009, peaking at 10.0% in October 2018.

Japan’s unemployment went from 4.0% in November 2008 to a peak of 5.5% in August 2009.

So two completely different labor outcomes during the worst recession in decades.

23. October 2019 at 05:06

“The UK also had a phony recession a few years back.”

—–

I don’t see one. The UK’s quarterly growth in 2012 and 2013 was:

0.6%, -0.1%, 1.2%, -0.2%, 0.6, 0.5%, 0.6%, 0.9%, 0.5%.

No one would call that a recession.

23. October 2019 at 08:07

Sumner, which of the following are examples of 2015 recessions:

1. Russia

2. Wyoming

3. Oklahoma

4. Brazil

5. Venezuela

6. Argentina

?

23. October 2019 at 09:08

I have always wondered if the equivalent of PPP could be calculated among the states in the US. I think it is clear that one can make money in high income states and then retire in low cost states and benefit. Also that can get conflated with savings and consumption rates at different points in life—-but back to the point—is it possible to do PPP among states? Income can be higher, but cost much more so (and vice versa) from state to state. Superficially, at least, this seems very plausible. Of course tax differentials may matter—but in efficient markets in one nation this should seem to not matter. Yet, again, superficially, it seems like the value of our currency is different in different states.

23. October 2019 at 12:58

ssumner writes:

Would it make more sense to define ‘recession’ as a substantial decline in the level of employment rather than a rise in the unemployment rate? Otherwise, given how it is calculated, if there were a sudden surge in the size of the labor force without a corresponding change in employment (say because of demographic changes), that could raise the red flag of recession without there ever having been any change in the economy’s output or employment levels….

23. October 2019 at 13:53

“Those graphs don’t surprise me at all; the US has been richer than other developed countries for . . . . well for almost a century.”

Actually three centuries.

23. October 2019 at 15:08

E. Harding.

“Actually three centuries.”. No, Australians had higher average incomes than Americans in the late C19th. Evidence suggests that US per capita GDP did not definitively overtake UK per capita GDP c.1880 or Australian per capita GDP until c.1940. Of course, UK had a very unequal income distribution, so it was easier for Americans to be more prosperous than a lot of Brits.

Data taken from here.

https://www.rug.nl/ggdc/historicaldevelopment/maddison/releases/maddison-project-database-2018

23. October 2019 at 17:33

Benjamin,

re: maid employment, the maids in Singapore are usually foreign domestic workers. They are sourced from neighboring countries that are much poorer than Singapore. As a result, their wages are low, and there are minimum wage rules imposed by the Singapore government often in negotiation with the governments of the source countries. The government also imposes levies on employers for the employment of all low-wage foreign workers (maids, construction workers etc) to protect low-wage Singaporean workers. And of course there are immigration and labor rules to obey, that are specific to maids. To make the process easier, employers almost exclusively go to privately run agencies that source maids or workers from their origin countries and deal with the paperwork.

24. October 2019 at 08:09

John, It’s easier for a small country to grow fast. I’d guess the absolute gap will stay fairly stable, although I don’t think that matters at all.

Michael Makdad, Yes, I’ve done many posts on the phony 2014 recession.

mbka, Thanks for that info. Keep in mind that few Americans have maids, so in that respect those countries are richer than America. It’s apples and oranges. Few cars, but lots of maids.

Todd, That supports my point. Japan’s unemployment rose by 1.5%, which is less than the US but that’s typical of Japan (the 1993 and 1998 recessions had similar increases). In the recent Japanese phony recessions it doesn’t rise at all.

This link explains my UK “phony recession” claim:

https://www.bbc.com/news/business-22290407

The data was later revised so that the second recession never happened.

Harding, States don’t matter. Some of those countries had supply side recessions.

Michael Rulle, State costs of living have been calculated.

Ironman, Maybe, but that’s not really an issue for the US. And unemployment solves the problem of changing trend rates of growth in employment.

24. October 2019 at 19:35

Lorenzo, fine, point taken. Although if you read the documentation (p. 28):

https://www.rug.nl/ggdc/html_publications/memorandum/gd174.pdf

there were three Lindert/Williamson benchmarks that weren’t included which suggest the UK/US gap was pretty sizeable during the nineteenth century. Don’t know which benchmarks to trust, though. If you read old books, they always talk about how U.S. has higher wages. Even Adam Smith mentioned it. Australian per capita incomes do seem to have been higher than American in the 1870s and 1880s.