Paul Krugman on monetary policy options

Saturos sent me some interesting PowerPoint slides by Paul Krugman:

Krugman overlooks a third option, targeting an alternative variable that is not subject to the zero lower bound. Or perhaps he regards that as a regime change. I can’t be sure. But it need not involve the Fed changing its inflation/unemployment targets, so it depends how one defines ‘regime.’ I believe he regards “regime shift” as something like an increase in the inflation target to 4%.

Krugman overlooks a third option, targeting an alternative variable that is not subject to the zero lower bound. Or perhaps he regards that as a regime change. I can’t be sure. But it need not involve the Fed changing its inflation/unemployment targets, so it depends how one defines ‘regime.’ I believe he regards “regime shift” as something like an increase in the inflation target to 4%.

In any case, alternative targets include foreign exchange rates, the price of actively traded commodities such as gold, and CPI/NGDP futures prices. Fisher’s Compensated Dollar plan was an adjustable gold price peg, aimed at stabilizing the price level.

In the past I’ve argued that Krugman had a sort of blind spot in this area. For instance, he was too pessimistic about the ability of the Swiss National Bank to peg the franc at a lower level vs. the euro. In any case, it’s interesting to compare these schemes to forward guidance. Krugman correctly points out that there is a theoretical possibility of an “expectations trap” with forward guidance. Markets might not believe central bank promises to fully carry through with monetary stimulus, as the initial effect on expectations is all the central bank really wants and needs.

You can think of the alternatives to interest rate targeting (assets that lack a zero bound) as a way of overcoming the expectations trap. When you target a variable with no zero bound (forex, gold, NGDP futures, etc) you are forced by the market to do “enough” to make the promise credible. Hence no expectations trap. In this post Krugman correctly pointed out that the risk of an expectations trap is replaced with the risk of a central bank balance sheet that is bloated to undesirable levels. In practice, I think that’s unlikely to be a problem for any “reasonable” nominal aggregate policy goal. And if it does become a problem the market is telling you that perhaps your inflation/NGDP target path is too low.

And we should not overlook the bright side of a bloated balance sheet. Suppose Japan was still at the zero rate bound after pegging CPI futures at a 2% premium over the spot CPI. That might imply a bloated BOJ balance sheet. But that would prove beyond any doubt that the Japanese government had just spent the past 20 walking down a sidewalk covered with $100 bills (or 10,000 yen bills) without once stopping to pick one up. Not smart, and it’s about time they raised their inflation rate target if they can do so without raising the nominal cost of funding the Japanese debt by one iota. A free bento box.

Krugman also makes this comment:

Once again, this is correct but slightly misleading. The distinction between the direct effect of a policy shift and the effect of a shift in the future expected path of policy is almost equally important when not at the zero bound. Any monetarist thought experiment involving a higher money supply ALWAYS involves the implicit assumption that the increase is permanent, or at least semi-permanent. Alternatively, when markets react very strongly to changes in the fed funs target (Jan. 2001, Sept. 2007, Dec. 2007) the market reaction almost certainly reflects changes in the expected future path of the fed funds rate, not the current setting.

Once again, this is correct but slightly misleading. The distinction between the direct effect of a policy shift and the effect of a shift in the future expected path of policy is almost equally important when not at the zero bound. Any monetarist thought experiment involving a higher money supply ALWAYS involves the implicit assumption that the increase is permanent, or at least semi-permanent. Alternatively, when markets react very strongly to changes in the fed funs target (Jan. 2001, Sept. 2007, Dec. 2007) the market reaction almost certainly reflects changes in the expected future path of the fed funds rate, not the current setting.

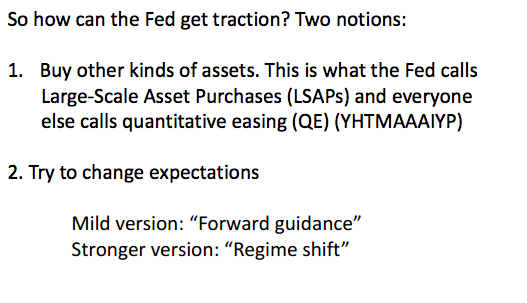

I was also amused by this; from one of his PP slides:

I wondered what had been deleted from this passage, as there seemed to be missing material at the end of each line. Here’s where Google is a miracle of the modern world—I was able to find the Wikipedia source:

I wondered what had been deleted from this passage, as there seemed to be missing material at the end of each line. Here’s where Google is a miracle of the modern world—I was able to find the Wikipedia source:

On September 13, 2012, the Federal Reserve announced a third round of quantitative easing (QE3).[7] This new round of quantitative easing provided for an open-ended commitment to purchase $40 billion agency mortgage-backed securities per month until the labor market improves “substantially”. Some economists believe that Scott Sumner‘s blog[8] on nominal income targeting played a role in popularizing the “wonky, once-eccentric policy” of “unlimited QE”.[9]

Ah, that’s much better!

Tags:

11. April 2014 at 13:02

“Krugman had a sort of blind spot in this area”

It is not a blind spot, it is a belief that optimal interest rate is negative. Swiss experience proves that the optimal rate is less optimal than Krugman thought, but it does not completely prove that it is positive. Perhaps additional 10 percent of devaluation could bring the problem of bloated Swiss CB balance sheet, indicating that the optimal rates are negative when Swiss policy target is credible.

11. April 2014 at 13:10

Vaidas, The Swiss case shows that Krugman was wrong in assuming that currency depreciation results in (or requires) a larger balance sheet—just the opposite.

11. April 2014 at 13:16

Scott, maybe the problem is that the belief in negative optimal rates causes him to miss the fact that the switch to a more sensible policy raises the optimal rate (perhaps to levels that are nonetheless negative – who knows).

11. April 2014 at 13:51

So Krugman acknowledges ‘Scott Sumner Day’ – the “Festivus for therestofus”!

11. April 2014 at 14:16

Vaidas, The optimal rate depends on the expected rate of growth in NGDP and also the size of the central bank balance sheet. In any case, he seems more worried about AD being too low than he is about the interest rate not being at the optimal level. The interest rate is an instrument for Krugman, not a policy goal.

Rajat, That’s what’s so funny, he acknowledged the impact, but left out my name. 🙂

11. April 2014 at 14:18

Scott, so Krugman purposely cut your name out of his slides? That’s hilarious!

11. April 2014 at 14:35

Ain’t it grand?

Krugman and Cochrane agree on only one thing: QE doesn’t work.

And yet the track record in the USA and Japan suggests QE does work.

Before both rockets and atomic power there were prominent scientists who the said the new ideas were not feasible and would not work…

11. April 2014 at 15:15

Re: Wikipedia, that is hilarious!

Benjamin Cole,

A little perspective: Krugman favors aggressive monetary policy while Cochrane doesn’t. He is on Team Demand (and therefore our ally). Krugman >>>> Cochrane.

11. April 2014 at 15:21

Scott, Krugman’s point is that ZLB leaves you with two bad choices: you can target NGDP that is too low, or you can target NGDP that is too high. If you target right NGDP without negative rates, you get enormous central bank balance sheet, and it is possible that te policy will fail.

Swiss experience shows that the expected NGDP was way below the level of expected NGDP where ZLB starts to bite, but it does not prove that the ZLB never constrains policy.

In my view, Swiss conditions (safe haven, open economy) create the best circumstances for ZLB constraint to appear. It is very encouraging that we have not observed the ZLB constraint in Switzerland, as this means ZLB is even less likely to be a problem elsewhere. However it is possible that ZLB problem would appear if Switzerland tried to devalue to 1.40.

11. April 2014 at 15:24

Hah! Hilarious ending to this post.

11. April 2014 at 17:18

“When you target a variable with no zero bound (forex, gold, NGDP futures, etc) you are forced by the market to do “enough” to make the promise credible.”

What is the Zimbabwean central bank targeted NGDP growth of 5%. Would it be credible if they did this and just expanded base at whatever pace necessary to reach the target?

11. April 2014 at 17:21

If the fed expanded the base by just transfering it to the public instead of under asset purchases wouldn’t base increases always be permanent?

11. April 2014 at 17:41

Jesus Christ, there is nothing more needed to prove Krugman is afraid.

Wow.

11. April 2014 at 17:52

Tom, I wish it was purposeful–that would be REALLY funny, but unfortunately it was an accident.

Vaidas, I don’t follow, surely interest rates would rise if they went to 1.40. Or at least there is some value of the franc low enough to cause rates to rise.

I don’t agree with the under or overshoot argument. I do understand that that’s an implication of NK models, but those models are wrong. They assume the transmission mechanism is real interest rates.

Danny, In that case their might be default risk, which could throw things off. I assumed no default risk in the US case.

11. April 2014 at 18:01

O/T: one of those pivotal moments in China…

11. April 2014 at 18:34

Also, you guys might find this amusing (EMH).

11. April 2014 at 19:33

If you look at the actual slide, you’ll see that there’s a huge chunk missing of the right side of every passage, not just the one that mentions you. You can even see how some letters cut off midway for the operation twist section as well.

http://i.imgur.com/7rwcSqo.jpg

It looks like Krugman took a screenshot of the wikipedia page, and tried to cut out the entire entire Q1/QE2/Twist/Q3 block in one piece, but accidentally cut off the right side of it. Or the slide software had margins and it blocked the right side without Krugman noticing.

11. April 2014 at 20:03

A better a picture of my point:

http://i.imgur.com/FbdEh23.jpg

My client pleads Not Guilty on the charges of purposely suppressing Sumner’s name.

11. April 2014 at 20:15

It looks like Krugman took a screenshot of the wikipedia page, and tried to cut out the entire entire Q1/QE2/Twist/Q3 block in one piece, but accidentally cut off the right side of it…

Cropped out like an ex-member of the Politboro.

11. April 2014 at 20:16

Edwin, Sumner did say it was an accident:

http://www.themoneyillusion.com/?p=26571#comment-328960

But I did wonder how he knew that… I don’t know if that’s how, but that’s pretty clear evidence. Thanks.

11. April 2014 at 20:18

“Cropped out like an ex-member of the Politboro.”

Interesting… Nick Rowe was accused of entering a Maoist phase today, and with some reason:

http://worthwhile.typepad.com/worthwhile_canadian_initi/2014/04/on-forgetting-land-in-models-of-secular-stagnation.html?cid=6a00d83451688169e201a73da7b0f9970d#comment-6a00d83451688169e201a73da7b0f9970d

😀

12. April 2014 at 03:15

Scott,

Yes, belief that the ZLB is a problem is correlated with the belief in the primacy of interest rate channel (I am not sure what Krugman’s views on channels are). However ZLB can be a theoretical problem in a any setting where uncovered interest rate parity holds. Suppose global rates are zero, and SNB devalues to 1.40 in a context of a switch to 4 percent inflation target. In this case we should expect a higher Swiss rates that reflect expectations that Swiss franc will continue to depreciate after the initial devaluation. This was a scenario where you get NGDP that is too high.

But there is another scenario – suppose SNB devalues to 1.40 in order to achieve a faster convergence to its current inflation target. When Swiss economy recovers, the equilibrium exchange rate is 1.30. In this case, according uncovered interest rate parity, Swiss rates should be negative to reflect the expected appreciation of Swiss franc after the initial devaluation to 1.40, and this means that ZLB is a problem in this scenario.

Key takeaway from this discussion is that we have never observed a truly binding ZLB in practice yet. No central bank has ever attempted to engineer a recovery so speedy that the ZLB starts to bind.

12. April 2014 at 06:56

If you reduce the remuneration rate, the alternative for CB investments would be to buy short-term securities (those within the short-end segment of the yield curve’s where the yield curve’s umbrella is conveniently inverted). If the CBs buy, e.g., gov’ts from the non-bank sector, then the money stock will also expand (not just IBDDs).

The Phillips curve (unemployment/inflation tradeoff), problem would be solved by simply getting the CBs out of the savings business (i.e., drive savings back thru the non-bank lending/investing sector – where savings are put to work and can be matched with real-investments). This would accelerate the transactions velocity of money – Vt.

LSAPs aren’t even necessary. But the Fed, the economy, & debtors would be much better served by a change in SOMA’s asset allocation to overweight with new issues of student debt.

As for targeting the roc in MVt, this is old news too. The lags in monetary flows (our means-of-payment money times its transactions rate-of-turnover), have been mathematical constants for the last 100 years. RRs are based on transaction type accounts 30 days prior:

Parse: first column = 10 mo roc in MVt, second column = 24 mo roc in MVt:

12/1/2013 ,,,,,,, 0.10 ,,,,,,, 0.22

1/1/2014 ,,,,,,, 0.16 ,,,,,,, 0.34

2/1/2014 ,,,,,,, 0.13 ,,,,,,, 0.38

3/1/2014 ,,,,,,, 0.14 ,,,,,,, 0.32

4/1/2014 ,,,,,,, 0.17 ,,,,,,, 0.35

5/1/2014 ,,,,,,, 0.15 ,,,,,,, 0.39

6/1/2014 ,,,,,,, 0.13 ,,,,,,, 0.35

7/1/2014 ,,,,,,, 0.14 ,,,,,,, 0.30

8/1/2014 ,,,,,,, 0.09 ,,,,,,, 0.26

9/1/2014 ,,,,,,, 0.09 ,,,,,,, 0.27

10/1/2014 ,,,,,,, 0.01 ,,,,,,, 0.23

11/1/2014 ,,,,,,, 0.02 ,,,,,,, 0.22

12/1/2014 ,,,,,,, 0.03 ,,,,,,, 0.16

We’ve already peaked this year. The FRB-NY’s “trading desk” needs to do extra work beginning in July (after inflation begins to slow). Then there is a real potential for a crash in Oct. (the Fed will have to intervene then).

12. April 2014 at 07:05

Edwin, Yes, that’s how I knew it was an accident.

Vaidas, I think it’s simpler than that. An equilibrium negative nominal rate results from an excessively low NGDP target. It’s that simple.

12. April 2014 at 07:12

Corrected/Repost:

If you reduce the remuneration rate, the alternative for CB investments would be to buy short-term securities (those within the short-end segment of the inverted yield curve). If the CBs buy, e.g., gov’ts from the non-bank sector, then the money stock will also expand (not just IBDDs).

The Phillips curve (unemployment/inflation tradeoff), problem would be solved by simply getting the CBs out of the savings business (i.e., drive savings back thru the non-bank lending/investing sector – where savings are put to work and can be matched with real-investments). This would accelerate the transactions velocity of money – Vt.

LSAPs aren’t even necessary. But the Fed, the economy, & debtors would be much better served by a change in SOMA’s asset allocation to overweight with new issues of student debt.

As for targeting the roc in MVt, this is old news too. The lags in monetary flows (our means-of-payment money times its transactions rate-of-turnover), have been mathematical constants for the last 100 years. RRs are based on transaction type accounts 30 days prior:

Parse: first column = 10 mo roc in MVt, second column = 24 mo roc in MVt:

12/1/2013 ,,,,,,, 0.10 ,,,,,,, 0.22

1/1/2014 ,,,,,,, 0.16 ,,,,,,, 0.34

2/1/2014 ,,,,,,, 0.13 ,,,,,,, 0.38

3/1/2014 ,,,,,,, 0.14 ,,,,,,, 0.32 -peaked first week in April

4/1/2014 ,,,,,,, 0.17 ,,,,,,, 0.35

5/1/2014 ,,,,,,, 0.15 ,,,,,,, 0.39

6/1/2014 ,,,,,,, 0.13 ,,,,,,, 0.35

7/1/2014 ,,,,,,, 0.14 ,,,,,,, 0.30 -deceleration in inflation

8/1/2014 ,,,,,,, 0.09 ,,,,,,, 0.26

9/1/2014 ,,,,,,, 0.09 ,,,,,,, 0.27

10/1/2014 ,,,,,,, 0.01 ,,,,,,, 0.23 -real shortfall in AD

11/1/2014 ,,,,,,, 0.02 ,,,,,,, 0.22

12/1/2014 ,,,,,,, 0.03 ,,,,,,, 0.16

We’ve already peaked this year. The FRB-NY’s “trading desk” needs to do extra work beginning in July (after inflation begins to slow). Then there is a real potential for a crash in Oct. (the Fed will have to intervene then).

12. April 2014 at 07:35

Today, there are not 5,844 commercial banks as the FRB_STL’s data base reflects; rather there are another 1,271 S&Ls, 7,094 CUs, & 361 MSBs which are also technically, commercial banks (with the capacity to create new money and credit).

Any institution whose liabilities can be transferred on demand, without notice, & without income penalty, via negotiable credit instruments, or data pathways, & whose deposits are regarded by the public as money, can create new money, provided that the institution is not encountering a negative cash flow (e.g., the thrifts after the 1990 S&L crisis).

The DIDMCA of March 31st 1980 legislation gave these depository financial institutions (DFIs), the power to create new money when they permitted the new instrumentality of: (1) negotiable order of withdrawals – (2) NOW, & automatic transfer service -ATS, accounts, etc.

Thus, CB credit should be expanded to include the CU’s, S&L’s, & MSB’s assets.

12. April 2014 at 09:04

Scott, it is entirely possible that optimal rates would be negative if Switzerland targeted pre-crisis NGDP trend when global rates are zero. That’s why Swiss experience is so informative.

12. April 2014 at 09:50

I did the same search for the missing contents!

12. April 2014 at 12:16

Prof. Sumner,

I’m a little surprised you haven’t posted on Bernanke vs. Rajan yet (1 hr 15 min into this video):

http://www.youtube.com/watch?v=VBmiq_yB8aI

http://blogs.wsj.com/economics/2014/04/10/bernanke-settles-back-into-research-world-2

12. April 2014 at 12:18

As with every socialist ideology, market monetarism is advanced on the basis of the notion that people are too stupid for their own good to be able to help themselves in a free market.

Thus, we’re told silly things like “Interest payments are nominally rigid, and so represent a burden in a world with volatile spending. It’s therefore prudent for a central bank to force spending to be more stable”.

Such lack of imagination! It’s almost as if there is no such as thing as floating interest rate instruments! And, that these instruments could not increase in size and number in a world with more volatile spending.

12. April 2014 at 18:57

Scott,

It appears to me that QE hasn’t worked because it hasn’t entered the money supply. Wouldn’t buying gold from civilians automatically enter the money supply, since civilians have accounts at banks (M1) and not at the Fed (MB)? FDR had no trouble creating inflation and nominal growth when he began to arbitrarily raise the price of gold until he got the price level where he wanted it. Why shouldn’t the Fed do that now? After all, gold is the one commodity that is considered an orthodox policy asset (as opposed to, say, ETFs, JGBs or apartment buildings).

13. April 2014 at 06:24

Yglesias:

Yesterday, “European Central Bank hints more monetary stimulus may be on the way”

http://www.vox.com/2014/4/13/5609930/european-central-bank-hints-more-monetary-stimulus-may-be-on-the-way

13. April 2014 at 11:27

The roc in money flows (MVt), doesn’t go from .14% in July to .01% in Oct without an economic contraction. This is what targeting gDp is all about (preventing a stroke). This is inviolate & sacrosanct.

13. April 2014 at 11:58

http://www.federalreserve.gov/faqs/money_12845.htm

“Over recent decades, however, the relationships between various measures of the money supply and variables such as GDP growth and inflation in the United States have been quite unstable. As a result, the importance of the money supply as a guide for the conduct of monetary policy in the United States has diminished over time”

Actually, there’s been no such degradation. The pundits simply could never accurately define our “means-of-payment” money supply. Money is the measure of liquidity.

In 1931 a commission was established on Member Bank Reserve Requirements. The commission completed their recommendations on Feb. 5, 1938. The study was entitled “Member Bank Reserve Requirements — Analysis of Committee Proposal”

It’s 2nd proposal: “Requirements against debits to deposits”

This research paper was “declassified” on March 23, 1983. By the time this paper was “declassified”, RRs had become a “tax” [sic].

Roc’s in RRs = roc’s in nominal-gDp. But e-mail 11/16/06: “xxxx, this is an interesting idea. Since no one in the Fed tracks reserves…” Senior V.P. Fed’s technical staff.

And the lags for monetary flows (MVt) are not “long & variable”. They have been mathematical constants for 100 years. This is the Gospel. No other metric has a higher R^2.

13. April 2014 at 13:56

Travis, What did you find interesting about that Rajan-Bernanke exchange?

Chris, The reason QE had less impact on inflation than the 1933 program had nothing to do with what the Fed bought. Rather FDR was trying to create inflation and the Fed is now trying to maintain “price stability.” Even if they buy gold, the sellers will simply turn around and deposit the money in the bank. So it makes almost not difference which asset the Fed chooses to buy initially. If the Fed wants to create inflation they need to set a higher inflation target (or preferably NGDP.)

14. April 2014 at 04:26

Prof. Sumner,

I’m curious what exchange rate interventions Rajan was referring to. Were they really just tariffs?

I’m curious which exchange rate interventions are sterilizing and which ones aren’t. For example, if the Fed printed a ton of new U.S. dollars and bought lots of foreign currencies with them, that wouldn’t be sterilizing…..

14. April 2014 at 04:32

JKH has a new lengthy post on Market Monetarism, its dismissal of banks in monetary theory, the BOE paper, etc.:

http://monetaryrealism.com/market-monetarism-monetary-base-overdrive

Nick Rowe has already posted a lengthy response:

http://monetaryrealism.com/market-monetarism-monetary-base-overdrive/#comment-110730

14. April 2014 at 09:27

TravisV, yes I saw JKH’s article too this morning: he’s got links in there to all my favorite MMist posts of late:

“JKH: very good post, despite my many quibbles.” — Nick Rowe

http://monetaryrealism.com/market-monetarism-monetary-base-overdrive/#comment-110704

14. April 2014 at 19:00

Travis, Sterilization is when the intervention doesn’t impact the money supply.

15. April 2014 at 12:57

Tripe. Reduce reserve requirements by 1/3, then permit sweep accounts, etc., will obviously destroy any current facsimile of a multiplier (as in the early 1990’s).

However, “bank reserves are largely driven by bank payments (debits)”. Anyone targeting nominal-gDp would be concerned about the 13 percentage point swing in the 10 mo roc of money flows [MVt], in the upcoming August-October 2014 period.

15. April 2014 at 13:04

“banks are not just financial intermediaries”

Tripe. Never are the commercial banks intermediaries in the savings-investment process.

From a systems viewpoint, commercial banks (DFIs), as contrasted to financial intermediaries (non-banks/thrifts): never loan out, & can’t loan out, existing deposits (saved or otherwise) including existing transaction deposits or time deposits or the owner’s equity, or any liability item.

When CBs grant loans to, or purchase securities from, the non-bank public, they acquire title to earning assets by initially, the creation of an equal volume of new money (demand deposits) — somewhere in the banking system. I.e., commercial bank deposits are the result of lending, not the other way around.

The non-bank public includes every institution (including shadow-banks), the U.S. Treasury, the U.S. Government, State, & other Governmental Jurisdictions, & every person, except the commercial & the Reserve banks.